BA 513: Ph.D. Seminar On Choice Theory Professor Robert Nau Fall Semester 2008

BA 513: Ph.D. Seminar On Choice Theory Professor Robert Nau Fall Semester 2008

You might also like

- Kripke The Question of LogicDocument35 pagesKripke The Question of LogicSenpai PandaNo ratings yet

- Solutions Exercises Decision Analysis Week 2 PDFDocument22 pagesSolutions Exercises Decision Analysis Week 2 PDFWesam WesamNo ratings yet

- The Impact of Behavioral Finance On Stock Markets PDFDocument11 pagesThe Impact of Behavioral Finance On Stock Markets PDFprema100% (1)

- Handbook of Risk TheoryDocument1,202 pagesHandbook of Risk TheoryMuhammad Defri SkmNo ratings yet

- Rationality: Lawrence E. Blume and David EasleyDocument19 pagesRationality: Lawrence E. Blume and David EasleyGabriel RoblesNo ratings yet

- 03 - Thaler - Misbehaving - Cap 4Document14 pages03 - Thaler - Misbehaving - Cap 4Victoria GuevaraNo ratings yet

- Nash Equilibrium and The History of Economic TheoryDocument16 pagesNash Equilibrium and The History of Economic TheoryNathaniel SauraNo ratings yet

- Breve Historia de La NPDocument12 pagesBreve Historia de La NPChaVizz ParraNo ratings yet

- Narrative Form and ConstructionDocument23 pagesNarrative Form and ConstructionDdrordNo ratings yet

- Mathematicians As Great Economists - NashDocument14 pagesMathematicians As Great Economists - NashAnonymous j6r5KRtrH2100% (1)

- The Role of Mathematics in EconomicsDocument7 pagesThe Role of Mathematics in EconomicsPhạm KhoaNo ratings yet

- Axiomatics of Classical Statistical MechanicsFrom EverandAxiomatics of Classical Statistical MechanicsRating: 5 out of 5 stars5/5 (1)

- Kocovic P.Document8 pagesKocovic P.geokaran1579No ratings yet

- A Quantum Theory of Money and Value - David Orrell (2016)Document19 pagesA Quantum Theory of Money and Value - David Orrell (2016)Felipe CorreaNo ratings yet

- A Conceptual History of The Emergence of Bounded RationalityDocument32 pagesA Conceptual History of The Emergence of Bounded RationalitySatyabrataNayakNo ratings yet

- BienvenuShaferShen PDFDocument40 pagesBienvenuShaferShen PDFgauravroongtaNo ratings yet

- Moscati 2016Document18 pagesMoscati 2016Julio ValladaresNo ratings yet

- Micro I - RationalityDocument17 pagesMicro I - RationalityTheDarkendedNo ratings yet

- (Dawid) Probability, Causality and The Empirical World - A Bayes - de Finetti - Popper - Borel SynthesisDocument14 pages(Dawid) Probability, Causality and The Empirical World - A Bayes - de Finetti - Popper - Borel SynthesisDoctor_CicladaNo ratings yet

- Expected Utility TheoryDocument11 pagesExpected Utility TheoryKhyber BaktashNo ratings yet

- Math EdDocument7 pagesMath EdAmber HabibNo ratings yet

- Only For Referece: Prospect Theory: Decision Making Under Risk"Document3 pagesOnly For Referece: Prospect Theory: Decision Making Under Risk"Michaella Claire LayugNo ratings yet

- History of Behavioral Economics PDFDocument17 pagesHistory of Behavioral Economics PDFAntonio Garcês100% (1)

- WP 038Document118 pagesWP 038carminatNo ratings yet

- Saiber, Turner - Mathematics and The Imagination - A Brief IntroductionDocument19 pagesSaiber, Turner - Mathematics and The Imagination - A Brief IntroductionAnonymous kg7YBMFHNo ratings yet

- The Crisis in The Foundations of MathematicsDocument14 pagesThe Crisis in The Foundations of MathematicsMaximiliano ValenzuelaNo ratings yet

- Creating Mathematical Infinities Metapho-49333255Document25 pagesCreating Mathematical Infinities Metapho-49333255Preye JumboNo ratings yet

- The Synthetic A Priori and What It Means For EconomicsDocument5 pagesThe Synthetic A Priori and What It Means For Economicsshaharhr1No ratings yet

- History of Constructivism in The 20th Century: A.S.TroelstraDocument32 pagesHistory of Constructivism in The 20th Century: A.S.Troelstrarajat charayaNo ratings yet

- Paty M 1990f-ProbRealBungeDocument23 pagesPaty M 1990f-ProbRealBungevictor_oxleyNo ratings yet

- Mises' Apriorism - Tautology or Theory of Praxis?Document26 pagesMises' Apriorism - Tautology or Theory of Praxis?Liberty AustraliaNo ratings yet

- Steiger, J. H. (1979) - Factor Indeterminacy in The 1930s and The 1970s Some Interesting Parallels. Psychometrika, 44, 157-167.Document11 pagesSteiger, J. H. (1979) - Factor Indeterminacy in The 1930s and The 1970s Some Interesting Parallels. Psychometrika, 44, 157-167.AcatalepsoNo ratings yet

- Weber's Ideal Types As Models in The Social SciencesDocument22 pagesWeber's Ideal Types As Models in The Social SciencesinfiereNo ratings yet

- Math Lecture NotesDocument52 pagesMath Lecture NotesJoelNo ratings yet

- Entropy 23 01286 v2Document15 pagesEntropy 23 01286 v2Erika BennaiaNo ratings yet

- Causality in Qualitative and Quantitative ResearchDocument29 pagesCausality in Qualitative and Quantitative ResearchOmar MsawelNo ratings yet

- The Role of Mathematics in Contemporary Theoretical PhysicsDocument6 pagesThe Role of Mathematics in Contemporary Theoretical PhysicsSuraj YadavNo ratings yet

- STRAUSS - Mathematics and The Real World PDFDocument27 pagesSTRAUSS - Mathematics and The Real World PDFvictor_3030No ratings yet

- 10.1515 - Humaff 2015 0039Document17 pages10.1515 - Humaff 2015 0039tonygh2023No ratings yet

- Criticisms and Discussions. 6 1 3: Wartung)Document8 pagesCriticisms and Discussions. 6 1 3: Wartung)a4558305No ratings yet

- هام شرح مخطط نظرية الكارثةDocument35 pagesهام شرح مخطط نظرية الكارثةsemon iqNo ratings yet

- Interpretation of ProbabilitiesDocument13 pagesInterpretation of ProbabilitiesJaume TornilaNo ratings yet

- Essays On Probability and Statistics - 1962 - Editor - M.S. BartlettDocument139 pagesEssays On Probability and Statistics - 1962 - Editor - M.S. BartlettJESUS ELVIS CASTAÑEDA CASTILLONo ratings yet

- Mathematics Introduction For MSCDocument52 pagesMathematics Introduction For MSC34plt34No ratings yet

- Mathematics Is InventedDocument4 pagesMathematics Is InventedNorul-Izzah PaguitalNo ratings yet

- The Identity Problem For Realist Structuralism - Keranen PDFDocument23 pagesThe Identity Problem For Realist Structuralism - Keranen PDFRocío SKNo ratings yet

- Science Core TheoryDocument32 pagesScience Core TheoryathagalialuminequinevaNo ratings yet

- Neuman and MorgensternDocument32 pagesNeuman and Morgensternvadim3108No ratings yet

- The Concept of Rationality in Neoclassical and Behavioural Economic TheoryDocument9 pagesThe Concept of Rationality in Neoclassical and Behavioural Economic TheoryBruno Soares PinheiroNo ratings yet

- Economic Rationality and Human Behavior: Can False Assumptions Become Reality?Document15 pagesEconomic Rationality and Human Behavior: Can False Assumptions Become Reality?Mohamed AbdisalanNo ratings yet

- James Buchanan and The AustriansDocument30 pagesJames Buchanan and The AustriansLibertarianVzlaNo ratings yet

- ProbabilityDocument3 pagesProbabilityairul93No ratings yet

- Paper 2009 Homo-EconomicusDocument14 pagesPaper 2009 Homo-EconomicusMatías Alonso Araneda CabelloNo ratings yet

- Hilbert's Significance For The Philosophy of Mathematics (1922) Paul BernaysDocument18 pagesHilbert's Significance For The Philosophy of Mathematics (1922) Paul BernaysOscar VallejosNo ratings yet

- Novo Artigo 3Document16 pagesNovo Artigo 3Rodrigo LimaNo ratings yet

- Murray N. Rothbard - Toward A Reconstruction of Utility & Welfare EconomicsDocument41 pagesMurray N. Rothbard - Toward A Reconstruction of Utility & Welfare EconomicsJumbo ZimmyNo ratings yet

- Economía DinámicaDocument32 pagesEconomía DinámicaEnrique Barrientos ApumaytaNo ratings yet

- F C E L: Acts and Ounterfactuals IN Conomic AWDocument46 pagesF C E L: Acts and Ounterfactuals IN Conomic AWSalvador Membrive YesteNo ratings yet

- Yates Mises-Hoppe PDFDocument25 pagesYates Mises-Hoppe PDFionelam8679No ratings yet

- How To Improve Bayesian Reasoning Without Instruction: Frequency FormatsDocument21 pagesHow To Improve Bayesian Reasoning Without Instruction: Frequency FormatscsuciavaNo ratings yet

- History of Constructivism in The 20 CenturyDocument32 pagesHistory of Constructivism in The 20 CenturyjgomespintoNo ratings yet

- Claudia Jones Nuclear TestingDocument25 pagesClaudia Jones Nuclear TestingDaniel Lee Eisenberg JacobsNo ratings yet

- Why The Euro Will Rival The Dollar PDFDocument25 pagesWhy The Euro Will Rival The Dollar PDFDaniel Lee Eisenberg JacobsNo ratings yet

- 1st International: Djacobs November 2020Document5 pages1st International: Djacobs November 2020Daniel Lee Eisenberg JacobsNo ratings yet

- Beta Anomaly An Ex-Ante Tail RiskDocument104 pagesBeta Anomaly An Ex-Ante Tail RiskDaniel Lee Eisenberg JacobsNo ratings yet

- Conference Group For Central European History of The American Historical AssociationDocument9 pagesConference Group For Central European History of The American Historical AssociationDaniel Lee Eisenberg JacobsNo ratings yet

- Theophilus Capital Against: Fisk Labor1Document9 pagesTheophilus Capital Against: Fisk Labor1Daniel Lee Eisenberg Jacobs100% (1)

- Continuity Change State of Process of Task ofDocument1 pageContinuity Change State of Process of Task ofDaniel Lee Eisenberg JacobsNo ratings yet

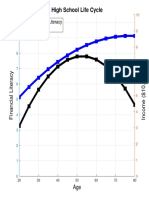

- High School Life Cycle: Financial Literacy IncomeDocument1 pageHigh School Life Cycle: Financial Literacy IncomeDaniel Lee Eisenberg JacobsNo ratings yet

- Karl Kautsky Republic and Social Democra PDFDocument4 pagesKarl Kautsky Republic and Social Democra PDFDaniel Lee Eisenberg JacobsNo ratings yet

- Borel Sets PDFDocument181 pagesBorel Sets PDFDaniel Lee Eisenberg Jacobs100% (1)

- Cover FERCDocument1 pageCover FERCDaniel Lee Eisenberg JacobsNo ratings yet

- Individualization of Robo-AdviceDocument8 pagesIndividualization of Robo-AdviceDaniel Lee Eisenberg JacobsNo ratings yet

- Gpebook PDFDocument332 pagesGpebook PDFDaniel Lee Eisenberg JacobsNo ratings yet

- Teach-In: Government of The People, by The People, For The PeopleDocument24 pagesTeach-In: Government of The People, by The People, For The PeopleDaniel Lee Eisenberg JacobsNo ratings yet

- The Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDocument8 pagesThe Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDaniel Lee Eisenberg JacobsNo ratings yet

- Simple BeamerDocument25 pagesSimple BeamerDaniel Lee Eisenberg JacobsNo ratings yet

- Necessary and Sufficient Conditions For Dynamic OptimizationDocument18 pagesNecessary and Sufficient Conditions For Dynamic OptimizationDaniel Lee Eisenberg JacobsNo ratings yet

- Bank Loan Loss ProvisioningDocument17 pagesBank Loan Loss ProvisioningDaniel Lee Eisenberg JacobsNo ratings yet

- Full Download Book Microeconomics and Behaviour 3Rd European Edition PDFDocument41 pagesFull Download Book Microeconomics and Behaviour 3Rd European Edition PDFdanny.broad150100% (26)

- Behavioral Finance Lecture 1Document45 pagesBehavioral Finance Lecture 1Bas KelderNo ratings yet

- Neuman and MorgensternDocument32 pagesNeuman and Morgensternvadim3108No ratings yet

- An Introduction To Utility Theory - JohnNorstadDocument27 pagesAn Introduction To Utility Theory - JohnNorstadwagndaveNo ratings yet

- Utilitiy Functions From Risk Theory To Finance PDFDocument27 pagesUtilitiy Functions From Risk Theory To Finance PDFjc_asidoNo ratings yet

- Health InsuranceDocument41 pagesHealth InsuranceVidya OrugantiNo ratings yet

- 2.2.1 Stock Market PuzzlesDocument30 pages2.2.1 Stock Market PuzzlesdivyanshNo ratings yet

- Tax Compliance and AdministrationDocument44 pagesTax Compliance and AdministrationDavid Adeabah OsafoNo ratings yet

- Chapter 3 - Utility Theory: ST Petersburg ParadoxDocument77 pagesChapter 3 - Utility Theory: ST Petersburg Paradoxabc123No ratings yet

- Game and Decision Theoretic Models in EthicsDocument39 pagesGame and Decision Theoretic Models in EthicsBernardo BarrezuetaNo ratings yet

- Paul Anand: Theory and Decision 23 (1987) 189-214. by D. Reidel Publishing CompanyDocument26 pagesPaul Anand: Theory and Decision 23 (1987) 189-214. by D. Reidel Publishing CompanyIván SalazarNo ratings yet

- PreferencesDocument119 pagesPreferencesJhorland Ayala GarciaNo ratings yet

- A Critical Analysis of HRD Evaluation ModelsDocument24 pagesA Critical Analysis of HRD Evaluation ModelsDouglas Patrick UtiyamaNo ratings yet

- Managerial Economics, Allen, CH 14 Test BankDocument11 pagesManagerial Economics, Allen, CH 14 Test BankSB100% (1)

- ISC239 Political Economy - SyllabusDocument2 pagesISC239 Political Economy - Syllabusjhy000197144No ratings yet

- Theory of Choice Under UncertainityDocument35 pagesTheory of Choice Under UncertainityPsyonaNo ratings yet

- Chapter ThreeDocument27 pagesChapter ThreeMinhaz Hossain OnikNo ratings yet

- Investment Decision Making and RiskDocument10 pagesInvestment Decision Making and RiskEdzwan RedzaNo ratings yet

- EJ1304430Document17 pagesEJ1304430Ilu AbrahimNo ratings yet

- Frontiers of Mathematical Psychology Essays in Honor of Clyde CoombsDocument226 pagesFrontiers of Mathematical Psychology Essays in Honor of Clyde CoombsSaúl VelásquezNo ratings yet

- 2000 - Behavioral Portfolio Theory - Shefrin & StatmanDocument26 pages2000 - Behavioral Portfolio Theory - Shefrin & StatmanNicolas FañaNo ratings yet

- Chapter 12 Hal Varian UncertaintyDocument10 pagesChapter 12 Hal Varian UncertaintySparsh KapoorNo ratings yet

- Modeling Attitude Toward RiskDocument11 pagesModeling Attitude Toward RiskFaizan Ul HaqNo ratings yet

- Making Decisions Under Uncertainty and RiskDocument11 pagesMaking Decisions Under Uncertainty and RiskDanielle WilliamsNo ratings yet

- State Preference Theory: - J. Hirshleifer, "Efficient Allocation of Capital in An Uncertain World,"Document27 pagesState Preference Theory: - J. Hirshleifer, "Efficient Allocation of Capital in An Uncertain World,"Toledo VargasNo ratings yet

- Science The Framing of Decisions and The Psychology of ChoiceDocument7 pagesScience The Framing of Decisions and The Psychology of Choicedambelen04No ratings yet

- Behavioral Finance Foundations For InvestorsDocument46 pagesBehavioral Finance Foundations For InvestorsMUHAMMAD IRFAN KHAN0% (1)

Download as pdf or txt

You might also like

- Kripke The Question of LogicDocument35 pagesKripke The Question of LogicSenpai PandaNo ratings yet

- Solutions Exercises Decision Analysis Week 2 PDFDocument22 pagesSolutions Exercises Decision Analysis Week 2 PDFWesam WesamNo ratings yet

- The Impact of Behavioral Finance On Stock Markets PDFDocument11 pagesThe Impact of Behavioral Finance On Stock Markets PDFprema100% (1)

- Handbook of Risk TheoryDocument1,202 pagesHandbook of Risk TheoryMuhammad Defri SkmNo ratings yet

- Rationality: Lawrence E. Blume and David EasleyDocument19 pagesRationality: Lawrence E. Blume and David EasleyGabriel RoblesNo ratings yet

- 03 - Thaler - Misbehaving - Cap 4Document14 pages03 - Thaler - Misbehaving - Cap 4Victoria GuevaraNo ratings yet

- Nash Equilibrium and The History of Economic TheoryDocument16 pagesNash Equilibrium and The History of Economic TheoryNathaniel SauraNo ratings yet

- Breve Historia de La NPDocument12 pagesBreve Historia de La NPChaVizz ParraNo ratings yet

- Narrative Form and ConstructionDocument23 pagesNarrative Form and ConstructionDdrordNo ratings yet

- Mathematicians As Great Economists - NashDocument14 pagesMathematicians As Great Economists - NashAnonymous j6r5KRtrH2100% (1)

- The Role of Mathematics in EconomicsDocument7 pagesThe Role of Mathematics in EconomicsPhạm KhoaNo ratings yet

- Axiomatics of Classical Statistical MechanicsFrom EverandAxiomatics of Classical Statistical MechanicsRating: 5 out of 5 stars5/5 (1)

- Kocovic P.Document8 pagesKocovic P.geokaran1579No ratings yet

- A Quantum Theory of Money and Value - David Orrell (2016)Document19 pagesA Quantum Theory of Money and Value - David Orrell (2016)Felipe CorreaNo ratings yet

- A Conceptual History of The Emergence of Bounded RationalityDocument32 pagesA Conceptual History of The Emergence of Bounded RationalitySatyabrataNayakNo ratings yet

- BienvenuShaferShen PDFDocument40 pagesBienvenuShaferShen PDFgauravroongtaNo ratings yet

- Moscati 2016Document18 pagesMoscati 2016Julio ValladaresNo ratings yet

- Micro I - RationalityDocument17 pagesMicro I - RationalityTheDarkendedNo ratings yet

- (Dawid) Probability, Causality and The Empirical World - A Bayes - de Finetti - Popper - Borel SynthesisDocument14 pages(Dawid) Probability, Causality and The Empirical World - A Bayes - de Finetti - Popper - Borel SynthesisDoctor_CicladaNo ratings yet

- Expected Utility TheoryDocument11 pagesExpected Utility TheoryKhyber BaktashNo ratings yet

- Math EdDocument7 pagesMath EdAmber HabibNo ratings yet

- Only For Referece: Prospect Theory: Decision Making Under Risk"Document3 pagesOnly For Referece: Prospect Theory: Decision Making Under Risk"Michaella Claire LayugNo ratings yet

- History of Behavioral Economics PDFDocument17 pagesHistory of Behavioral Economics PDFAntonio Garcês100% (1)

- WP 038Document118 pagesWP 038carminatNo ratings yet

- Saiber, Turner - Mathematics and The Imagination - A Brief IntroductionDocument19 pagesSaiber, Turner - Mathematics and The Imagination - A Brief IntroductionAnonymous kg7YBMFHNo ratings yet

- The Crisis in The Foundations of MathematicsDocument14 pagesThe Crisis in The Foundations of MathematicsMaximiliano ValenzuelaNo ratings yet

- Creating Mathematical Infinities Metapho-49333255Document25 pagesCreating Mathematical Infinities Metapho-49333255Preye JumboNo ratings yet

- The Synthetic A Priori and What It Means For EconomicsDocument5 pagesThe Synthetic A Priori and What It Means For Economicsshaharhr1No ratings yet

- History of Constructivism in The 20th Century: A.S.TroelstraDocument32 pagesHistory of Constructivism in The 20th Century: A.S.Troelstrarajat charayaNo ratings yet

- Paty M 1990f-ProbRealBungeDocument23 pagesPaty M 1990f-ProbRealBungevictor_oxleyNo ratings yet

- Mises' Apriorism - Tautology or Theory of Praxis?Document26 pagesMises' Apriorism - Tautology or Theory of Praxis?Liberty AustraliaNo ratings yet

- Steiger, J. H. (1979) - Factor Indeterminacy in The 1930s and The 1970s Some Interesting Parallels. Psychometrika, 44, 157-167.Document11 pagesSteiger, J. H. (1979) - Factor Indeterminacy in The 1930s and The 1970s Some Interesting Parallels. Psychometrika, 44, 157-167.AcatalepsoNo ratings yet

- Weber's Ideal Types As Models in The Social SciencesDocument22 pagesWeber's Ideal Types As Models in The Social SciencesinfiereNo ratings yet

- Math Lecture NotesDocument52 pagesMath Lecture NotesJoelNo ratings yet

- Entropy 23 01286 v2Document15 pagesEntropy 23 01286 v2Erika BennaiaNo ratings yet

- Causality in Qualitative and Quantitative ResearchDocument29 pagesCausality in Qualitative and Quantitative ResearchOmar MsawelNo ratings yet

- The Role of Mathematics in Contemporary Theoretical PhysicsDocument6 pagesThe Role of Mathematics in Contemporary Theoretical PhysicsSuraj YadavNo ratings yet

- STRAUSS - Mathematics and The Real World PDFDocument27 pagesSTRAUSS - Mathematics and The Real World PDFvictor_3030No ratings yet

- 10.1515 - Humaff 2015 0039Document17 pages10.1515 - Humaff 2015 0039tonygh2023No ratings yet

- Criticisms and Discussions. 6 1 3: Wartung)Document8 pagesCriticisms and Discussions. 6 1 3: Wartung)a4558305No ratings yet

- هام شرح مخطط نظرية الكارثةDocument35 pagesهام شرح مخطط نظرية الكارثةsemon iqNo ratings yet

- Interpretation of ProbabilitiesDocument13 pagesInterpretation of ProbabilitiesJaume TornilaNo ratings yet

- Essays On Probability and Statistics - 1962 - Editor - M.S. BartlettDocument139 pagesEssays On Probability and Statistics - 1962 - Editor - M.S. BartlettJESUS ELVIS CASTAÑEDA CASTILLONo ratings yet

- Mathematics Introduction For MSCDocument52 pagesMathematics Introduction For MSC34plt34No ratings yet

- Mathematics Is InventedDocument4 pagesMathematics Is InventedNorul-Izzah PaguitalNo ratings yet

- The Identity Problem For Realist Structuralism - Keranen PDFDocument23 pagesThe Identity Problem For Realist Structuralism - Keranen PDFRocío SKNo ratings yet

- Science Core TheoryDocument32 pagesScience Core TheoryathagalialuminequinevaNo ratings yet

- Neuman and MorgensternDocument32 pagesNeuman and Morgensternvadim3108No ratings yet

- The Concept of Rationality in Neoclassical and Behavioural Economic TheoryDocument9 pagesThe Concept of Rationality in Neoclassical and Behavioural Economic TheoryBruno Soares PinheiroNo ratings yet

- Economic Rationality and Human Behavior: Can False Assumptions Become Reality?Document15 pagesEconomic Rationality and Human Behavior: Can False Assumptions Become Reality?Mohamed AbdisalanNo ratings yet

- James Buchanan and The AustriansDocument30 pagesJames Buchanan and The AustriansLibertarianVzlaNo ratings yet

- ProbabilityDocument3 pagesProbabilityairul93No ratings yet

- Paper 2009 Homo-EconomicusDocument14 pagesPaper 2009 Homo-EconomicusMatías Alonso Araneda CabelloNo ratings yet

- Hilbert's Significance For The Philosophy of Mathematics (1922) Paul BernaysDocument18 pagesHilbert's Significance For The Philosophy of Mathematics (1922) Paul BernaysOscar VallejosNo ratings yet

- Novo Artigo 3Document16 pagesNovo Artigo 3Rodrigo LimaNo ratings yet

- Murray N. Rothbard - Toward A Reconstruction of Utility & Welfare EconomicsDocument41 pagesMurray N. Rothbard - Toward A Reconstruction of Utility & Welfare EconomicsJumbo ZimmyNo ratings yet

- Economía DinámicaDocument32 pagesEconomía DinámicaEnrique Barrientos ApumaytaNo ratings yet

- F C E L: Acts and Ounterfactuals IN Conomic AWDocument46 pagesF C E L: Acts and Ounterfactuals IN Conomic AWSalvador Membrive YesteNo ratings yet

- Yates Mises-Hoppe PDFDocument25 pagesYates Mises-Hoppe PDFionelam8679No ratings yet

- How To Improve Bayesian Reasoning Without Instruction: Frequency FormatsDocument21 pagesHow To Improve Bayesian Reasoning Without Instruction: Frequency FormatscsuciavaNo ratings yet

- History of Constructivism in The 20 CenturyDocument32 pagesHistory of Constructivism in The 20 CenturyjgomespintoNo ratings yet

- Claudia Jones Nuclear TestingDocument25 pagesClaudia Jones Nuclear TestingDaniel Lee Eisenberg JacobsNo ratings yet

- Why The Euro Will Rival The Dollar PDFDocument25 pagesWhy The Euro Will Rival The Dollar PDFDaniel Lee Eisenberg JacobsNo ratings yet

- 1st International: Djacobs November 2020Document5 pages1st International: Djacobs November 2020Daniel Lee Eisenberg JacobsNo ratings yet

- Beta Anomaly An Ex-Ante Tail RiskDocument104 pagesBeta Anomaly An Ex-Ante Tail RiskDaniel Lee Eisenberg JacobsNo ratings yet

- Conference Group For Central European History of The American Historical AssociationDocument9 pagesConference Group For Central European History of The American Historical AssociationDaniel Lee Eisenberg JacobsNo ratings yet

- Theophilus Capital Against: Fisk Labor1Document9 pagesTheophilus Capital Against: Fisk Labor1Daniel Lee Eisenberg Jacobs100% (1)

- Continuity Change State of Process of Task ofDocument1 pageContinuity Change State of Process of Task ofDaniel Lee Eisenberg JacobsNo ratings yet

- High School Life Cycle: Financial Literacy IncomeDocument1 pageHigh School Life Cycle: Financial Literacy IncomeDaniel Lee Eisenberg JacobsNo ratings yet

- Karl Kautsky Republic and Social Democra PDFDocument4 pagesKarl Kautsky Republic and Social Democra PDFDaniel Lee Eisenberg JacobsNo ratings yet

- Borel Sets PDFDocument181 pagesBorel Sets PDFDaniel Lee Eisenberg Jacobs100% (1)

- Cover FERCDocument1 pageCover FERCDaniel Lee Eisenberg JacobsNo ratings yet

- Individualization of Robo-AdviceDocument8 pagesIndividualization of Robo-AdviceDaniel Lee Eisenberg JacobsNo ratings yet

- Gpebook PDFDocument332 pagesGpebook PDFDaniel Lee Eisenberg JacobsNo ratings yet

- Teach-In: Government of The People, by The People, For The PeopleDocument24 pagesTeach-In: Government of The People, by The People, For The PeopleDaniel Lee Eisenberg JacobsNo ratings yet

- The Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDocument8 pagesThe Saving Behavior of Public Vocational High School Students of Business and Management Program in Semarang SitiDaniel Lee Eisenberg JacobsNo ratings yet

- Simple BeamerDocument25 pagesSimple BeamerDaniel Lee Eisenberg JacobsNo ratings yet

- Necessary and Sufficient Conditions For Dynamic OptimizationDocument18 pagesNecessary and Sufficient Conditions For Dynamic OptimizationDaniel Lee Eisenberg JacobsNo ratings yet

- Bank Loan Loss ProvisioningDocument17 pagesBank Loan Loss ProvisioningDaniel Lee Eisenberg JacobsNo ratings yet

- Full Download Book Microeconomics and Behaviour 3Rd European Edition PDFDocument41 pagesFull Download Book Microeconomics and Behaviour 3Rd European Edition PDFdanny.broad150100% (26)

- Behavioral Finance Lecture 1Document45 pagesBehavioral Finance Lecture 1Bas KelderNo ratings yet

- Neuman and MorgensternDocument32 pagesNeuman and Morgensternvadim3108No ratings yet

- An Introduction To Utility Theory - JohnNorstadDocument27 pagesAn Introduction To Utility Theory - JohnNorstadwagndaveNo ratings yet

- Utilitiy Functions From Risk Theory To Finance PDFDocument27 pagesUtilitiy Functions From Risk Theory To Finance PDFjc_asidoNo ratings yet

- Health InsuranceDocument41 pagesHealth InsuranceVidya OrugantiNo ratings yet

- 2.2.1 Stock Market PuzzlesDocument30 pages2.2.1 Stock Market PuzzlesdivyanshNo ratings yet

- Tax Compliance and AdministrationDocument44 pagesTax Compliance and AdministrationDavid Adeabah OsafoNo ratings yet

- Chapter 3 - Utility Theory: ST Petersburg ParadoxDocument77 pagesChapter 3 - Utility Theory: ST Petersburg Paradoxabc123No ratings yet

- Game and Decision Theoretic Models in EthicsDocument39 pagesGame and Decision Theoretic Models in EthicsBernardo BarrezuetaNo ratings yet

- Paul Anand: Theory and Decision 23 (1987) 189-214. by D. Reidel Publishing CompanyDocument26 pagesPaul Anand: Theory and Decision 23 (1987) 189-214. by D. Reidel Publishing CompanyIván SalazarNo ratings yet

- PreferencesDocument119 pagesPreferencesJhorland Ayala GarciaNo ratings yet

- A Critical Analysis of HRD Evaluation ModelsDocument24 pagesA Critical Analysis of HRD Evaluation ModelsDouglas Patrick UtiyamaNo ratings yet

- Managerial Economics, Allen, CH 14 Test BankDocument11 pagesManagerial Economics, Allen, CH 14 Test BankSB100% (1)

- ISC239 Political Economy - SyllabusDocument2 pagesISC239 Political Economy - Syllabusjhy000197144No ratings yet

- Theory of Choice Under UncertainityDocument35 pagesTheory of Choice Under UncertainityPsyonaNo ratings yet

- Chapter ThreeDocument27 pagesChapter ThreeMinhaz Hossain OnikNo ratings yet

- Investment Decision Making and RiskDocument10 pagesInvestment Decision Making and RiskEdzwan RedzaNo ratings yet

- EJ1304430Document17 pagesEJ1304430Ilu AbrahimNo ratings yet

- Frontiers of Mathematical Psychology Essays in Honor of Clyde CoombsDocument226 pagesFrontiers of Mathematical Psychology Essays in Honor of Clyde CoombsSaúl VelásquezNo ratings yet

- 2000 - Behavioral Portfolio Theory - Shefrin & StatmanDocument26 pages2000 - Behavioral Portfolio Theory - Shefrin & StatmanNicolas FañaNo ratings yet

- Chapter 12 Hal Varian UncertaintyDocument10 pagesChapter 12 Hal Varian UncertaintySparsh KapoorNo ratings yet

- Modeling Attitude Toward RiskDocument11 pagesModeling Attitude Toward RiskFaizan Ul HaqNo ratings yet

- Making Decisions Under Uncertainty and RiskDocument11 pagesMaking Decisions Under Uncertainty and RiskDanielle WilliamsNo ratings yet

- State Preference Theory: - J. Hirshleifer, "Efficient Allocation of Capital in An Uncertain World,"Document27 pagesState Preference Theory: - J. Hirshleifer, "Efficient Allocation of Capital in An Uncertain World,"Toledo VargasNo ratings yet

- Science The Framing of Decisions and The Psychology of ChoiceDocument7 pagesScience The Framing of Decisions and The Psychology of Choicedambelen04No ratings yet

- Behavioral Finance Foundations For InvestorsDocument46 pagesBehavioral Finance Foundations For InvestorsMUHAMMAD IRFAN KHAN0% (1)