Download as doc, pdf, or txt

You might also like

- Module 3 Answers To End of Module QuestionsDocument40 pagesModule 3 Answers To End of Module QuestionsYanLi100% (3)

- Lyari Expressway Rehabilitation ProjectDocument32 pagesLyari Expressway Rehabilitation ProjectKamran KhanNo ratings yet

- SAP BO Developer Interview Questions and AnswersDocument7 pagesSAP BO Developer Interview Questions and AnswersPruthve RaajNo ratings yet

- Operations Management MBA AssignmentDocument20 pagesOperations Management MBA Assignmentaloy157416767% (6)

- Operations Management MBA AssignmentDocument20 pagesOperations Management MBA Assignmentaloy157416767% (6)

- Anantha PVCDocument71 pagesAnantha PVCMasthan ValiNo ratings yet

- Corporate Finance Chapter1Document29 pagesCorporate Finance Chapter1Kavin Ur FrndNo ratings yet

- Order Under Sections 11 and 11B Against Acme Craft P. Ltd. and Its Directors, Viz. Mr. Jigar Jagdish Pandya and Mr. Akash GanachariDocument23 pagesOrder Under Sections 11 and 11B Against Acme Craft P. Ltd. and Its Directors, Viz. Mr. Jigar Jagdish Pandya and Mr. Akash GanachariShyam SunderNo ratings yet

- OBLICON Midterms ReviewerDocument14 pagesOBLICON Midterms ReviewerMichael LagundiNo ratings yet

- Portfolio InvestmentDocument74 pagesPortfolio InvestmentMOHITKOLLINo ratings yet

- Leave License Agreement - GBM - 150613Document17 pagesLeave License Agreement - GBM - 150613Bharat Prakash MahantNo ratings yet

- E Lecture Notes For PPC Unit 1Document38 pagesE Lecture Notes For PPC Unit 1Vinoth RajaguruNo ratings yet

- How To Deal With ContractorsDocument4 pagesHow To Deal With ContractorsAntonioMouraNo ratings yet

- A Project Report On Kotak Mahindra BankDocument50 pagesA Project Report On Kotak Mahindra BankMansi Prashar100% (1)

- Built-In Advantageand The Law Will Have To Be Applied As ItisDocument4 pagesBuilt-In Advantageand The Law Will Have To Be Applied As ItisgorgeousveganNo ratings yet

- Procedure of Audit GG& InspectionDocument8 pagesProcedure of Audit GG& InspectionZaman31No ratings yet

- Pointers 2Document17 pagesPointers 2cynemesisNo ratings yet

- The Punjab Industrial Relations Act 2010Document28 pagesThe Punjab Industrial Relations Act 2010Syed Ali Naqi KazmiNo ratings yet

- Sentence Boundary PunctuationDocument36 pagesSentence Boundary PunctuationBBA730No ratings yet

- Online - Wed - Planner ProjectDocument31 pagesOnline - Wed - Planner ProjectKennyBestKen0% (1)

- Apollo Group Riordan Manufacturing: Riordan's Human Resources Implementation & Testing PlanDocument10 pagesApollo Group Riordan Manufacturing: Riordan's Human Resources Implementation & Testing Planapi-250711275No ratings yet

- Strategic Management and Business Policy-1Document17 pagesStrategic Management and Business Policy-1gvenkatrNo ratings yet

- Multiple Choice Questions Unit-I: Operations Management Question Bank Unit-1Document5 pagesMultiple Choice Questions Unit-I: Operations Management Question Bank Unit-1divyaimranNo ratings yet

- Module 2 SolutionsDocument61 pagesModule 2 Solutionsrasmussen123456No ratings yet

- Distance Warning SystemDocument26 pagesDistance Warning SystemPraveen ReddyNo ratings yet

- A Brief Check List of Labour Laws: Apprentices Act, 1961Document17 pagesA Brief Check List of Labour Laws: Apprentices Act, 1961Sourabh JainNo ratings yet

- 1970 Declaration On PrinciplesDocument9 pages1970 Declaration On Principleslauj_1No ratings yet

- WDDIDocument1,541 pagesWDDIRahul KadamNo ratings yet

- Standard 3 322Document22 pagesStandard 3 322Luminita StefanNo ratings yet

- Contract Labour ActDocument24 pagesContract Labour ActnklrathinamNo ratings yet

- Luc RareDocument29 pagesLuc RareGabriela Anca BarbuNo ratings yet

- Memorandum: Articles AssociationDocument13 pagesMemorandum: Articles Associationaraza_962307No ratings yet

- GSA 2014 Information BookDocument11 pagesGSA 2014 Information BookthegsaNo ratings yet

- Vector Control of Ac DrivesDocument61 pagesVector Control of Ac Drivessureshy-ee213No ratings yet

- Buildingcontrolact 2012Document22 pagesBuildingcontrolact 2012Yashveer TakooryNo ratings yet

- Pramati Educational & Cultural Trust and Ors. v. Union of IndiaDocument75 pagesPramati Educational & Cultural Trust and Ors. v. Union of IndiaBar & BenchNo ratings yet

- Project Proposal Form: High School Student Council OfficersDocument4 pagesProject Proposal Form: High School Student Council OfficersasdfghjklostNo ratings yet

- Domestic Corporation TableDocument3 pagesDomestic Corporation TableAicka Bustamante SingsonNo ratings yet

- Prashant AlavandiDocument4 pagesPrashant AlavandiPrashantAlavandiNo ratings yet

- Tania Textile: A Concern of A Hussein GroupDocument7 pagesTania Textile: A Concern of A Hussein GroupShajiaAfrinNo ratings yet

- Propagation Data and Prediction Methods Required For The Design of Terrestrial Line-Of-Sight SystemsDocument46 pagesPropagation Data and Prediction Methods Required For The Design of Terrestrial Line-Of-Sight SystemsJomil John ReyesNo ratings yet

- 7.4.14 Red Notes TaxDocument41 pages7.4.14 Red Notes TaxRey Jan N. VillavicencioNo ratings yet

- What Is ISO17799 Copy VersionDocument5 pagesWhat Is ISO17799 Copy VersionGDJhonesNo ratings yet

- Cs507 Midterm Paper Solved With RefernceDocument9 pagesCs507 Midterm Paper Solved With RefernceMuhammad Zahid FareedNo ratings yet

- Infosys.110 Business Systems: Deliverable 2: Business Section 2014Document10 pagesInfosys.110 Business Systems: Deliverable 2: Business Section 2014Ellen Strange'No ratings yet

- Labor Law Principles General PrinciplesDocument19 pagesLabor Law Principles General PrinciplesMandamusMeowNo ratings yet

- Government of India Ministry of RailwaysDocument10 pagesGovernment of India Ministry of Railwaysrdas1980No ratings yet

- Chapter 2 Lecture Notes: Consolidation of Financial Information - Date of AcquisitionDocument7 pagesChapter 2 Lecture Notes: Consolidation of Financial Information - Date of AcquisitionAbraham Maharba BaezaNo ratings yet

- Acca P1 Exam Notes: Part 1: Framework Chapter 1: Introduction of CG (Corporate Governance)Document26 pagesAcca P1 Exam Notes: Part 1: Framework Chapter 1: Introduction of CG (Corporate Governance)Tanim Misbahul MNo ratings yet

- Economics 461 Final Exam 2Document32 pagesEconomics 461 Final Exam 2Zehao QiuNo ratings yet

- Index: CNDI 06 Increase Topicality LAB: Arnett/Burshteyn/LinDocument15 pagesIndex: CNDI 06 Increase Topicality LAB: Arnett/Burshteyn/LinIMNo ratings yet

- Current State of Internal Control System in Local GovernmentDocument12 pagesCurrent State of Internal Control System in Local GovernmentLee Ja NelNo ratings yet

- Judge Sinco Poli ReviewerDocument58 pagesJudge Sinco Poli ReviewerNo WeNo ratings yet

- Question Bank: Unit1Document3 pagesQuestion Bank: Unit1rajeevv_6No ratings yet

- Computable General Equilibrium (CGE) Models and Tourism EconomicsDocument21 pagesComputable General Equilibrium (CGE) Models and Tourism EconomicsMuna AhmadNo ratings yet

- Comelec Rules of ProcedureDocument41 pagesComelec Rules of ProcedureJuan LennonNo ratings yet

- WLDoc 13-10-10 8 - 58 (AM)Document8 pagesWLDoc 13-10-10 8 - 58 (AM)Gyan PrakashNo ratings yet

- Alm-Course Outlines-For Two DaysDocument40 pagesAlm-Course Outlines-For Two Daysrashed03nsuNo ratings yet

- Divided States: Strategic Divisions in EU-Russia RelationsFrom EverandDivided States: Strategic Divisions in EU-Russia RelationsNo ratings yet

- Loose Coarse Pitch Worms & Worm Gearing World Summary: Market Sector Values & Financials by CountryFrom EverandLoose Coarse Pitch Worms & Worm Gearing World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Scales & Balances World Summary: Market Values & Financials by CountryFrom EverandScales & Balances World Summary: Market Values & Financials by CountryNo ratings yet

- SalesDocument3 pagesSalesaloy1574167No ratings yet

- Joint Venture - UnlockedDocument17 pagesJoint Venture - Unlockedaloy1574167No ratings yet

- Research PublicationsDocument1 pageResearch Publicationsaloy1574167No ratings yet

- University of Jaffna-Sri Lanka Department of AccountingDocument1 pageUniversity of Jaffna-Sri Lanka Department of Accountingaloy1574167No ratings yet

- Leave Letter 10.06.2014Document1 pageLeave Letter 10.06.2014aloy1574167No ratings yet

- C - Nti T N A D and Int RN Tio N - S Ov Tto RD Con RG eDocument1 pageC - Nti T N A D and Int RN Tio N - S Ov Tto RD Con RG ealoy1574167No ratings yet

- Mintzberg's Management Roles Identifying The Roles Managers PlayDocument6 pagesMintzberg's Management Roles Identifying The Roles Managers Playaloy1574167No ratings yet

- RRRRR 5 TTTTTDocument1 pageRRRRR 5 TTTTTaloy1574167No ratings yet

- NSB Internet Bank UserGuideDocument5 pagesNSB Internet Bank UserGuideSadeep Madhushan50% (2)

- Mrs.P.Muraleetharan Personal File 2014: ACC 3235: Advanced Business Accounting Mr.S.BalaputhiranDocument1 pageMrs.P.Muraleetharan Personal File 2014: ACC 3235: Advanced Business Accounting Mr.S.Balaputhiranaloy1574167No ratings yet

- Computing Additional Profit (LKR)Document2 pagesComputing Additional Profit (LKR)aloy1574167No ratings yet

- Corporate Responsibility Reporting 2 ECTSDocument1 pageCorporate Responsibility Reporting 2 ECTSaloy1574167No ratings yet

- LKR LKRDocument2 pagesLKR LKRaloy1574167No ratings yet

- ST NDDocument6 pagesST NDaloy1574167No ratings yet

- Workshop On Industrial Training by Industrialist On 21st & 22nd of October, 2013Document1 pageWorkshop On Industrial Training by Industrialist On 21st & 22nd of October, 2013aloy1574167No ratings yet

- 11.20lkas 202-Inventories PDFDocument0 pages11.20lkas 202-Inventories PDFaloy1574167No ratings yet

- (EXERCISE) Bond ValuationDocument1 page(EXERCISE) Bond Valuationclary fray100% (1)

- Listing Particulars For BP Amoco-Arco CombinationDocument277 pagesListing Particulars For BP Amoco-Arco CombinationAmanda CunninghamNo ratings yet

- Investing ActivitiesDocument7 pagesInvesting ActivitiesMs. ArianaNo ratings yet

- 9-1b PT Pohan, PT Sohan, PT TohanDocument23 pages9-1b PT Pohan, PT Sohan, PT TohanToys AdventureNo ratings yet

- Bir Form 1600Document9 pagesBir Form 1600Vincent De GuzmanNo ratings yet

- Identification of Contributory Assets and Calculation of Economic Rents: ToolkitDocument68 pagesIdentification of Contributory Assets and Calculation of Economic Rents: ToolkitRizalNo ratings yet

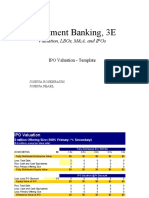

- IPO Valuation 3E TemplateDocument3 pagesIPO Valuation 3E TemplateLohith Kumar ReddyNo ratings yet

- Valuation & Fin Moduling PDFDocument14 pagesValuation & Fin Moduling PDFTohidul Anwar ChyNo ratings yet

- Profit and Loss Account For The Year Ended 31st March, 2011: CroresDocument1 pageProfit and Loss Account For The Year Ended 31st March, 2011: CroresKritika AgarwalNo ratings yet

- MBA Finance Resume Sample For ExperiencedDocument2 pagesMBA Finance Resume Sample For Experiencedpry_kumNo ratings yet

- Corporate Governance in IndiaDocument15 pagesCorporate Governance in IndiaRashmiPandey100% (2)

- Capital Structure Under Asymmetric Information: Problem Sets. 4 Part SeriesDocument8 pagesCapital Structure Under Asymmetric Information: Problem Sets. 4 Part SeriesVedBakshi100% (1)

- Bus 5111 Discussion Assignment Unit 7Document3 pagesBus 5111 Discussion Assignment Unit 7Sheu Abdulkadir BasharuNo ratings yet

- Meaning of A CompanyDocument28 pagesMeaning of A CompanyAman GautamNo ratings yet

- VOUCHER Latest FormatDocument1 pageVOUCHER Latest FormatVee MaNo ratings yet

- Topic 18-22 - Investments and Basic Derivatives (Compiled)Document37 pagesTopic 18-22 - Investments and Basic Derivatives (Compiled)Eki OmallaoNo ratings yet

- Current Liabilities Management: Multiple Choice QuestionsDocument24 pagesCurrent Liabilities Management: Multiple Choice QuestionsRodNo ratings yet

- BONDS and STOCK 33Document3 pagesBONDS and STOCK 33Bloody HunterNo ratings yet

- Learnovate Task No. - 02Document5 pagesLearnovate Task No. - 02Nikita DakiNo ratings yet

- Week 1 - Principle of AccountingDocument38 pagesWeek 1 - Principle of AccountingMai NgocNo ratings yet

- Ae 211 Module 6 - Exercise 6-5 To 6-9Document7 pagesAe 211 Module 6 - Exercise 6-5 To 6-9Nhel AlvaroNo ratings yet

- Rnis College of Financial Planning - 15 Mock-Test - Module-IVDocument10 pagesRnis College of Financial Planning - 15 Mock-Test - Module-IVAbhilash ParakhNo ratings yet

- Cash Forecasting: Tony de Caux, Chief ExecutiveDocument6 pagesCash Forecasting: Tony de Caux, Chief ExecutiveAshutosh PandeyNo ratings yet

- Company ProjectDocument14 pagesCompany ProjectMayank Sahu0% (1)

- ABM101 - M9 - Business Transactions and Their Analysis As Applied To Accounting Cycle of A Service Business Pt.3Document8 pagesABM101 - M9 - Business Transactions and Their Analysis As Applied To Accounting Cycle of A Service Business Pt.3stephaniefaithbrina28No ratings yet

- Business Law A2 Mai Huong (Recovered)Document6 pagesBusiness Law A2 Mai Huong (Recovered)Mai HươngNo ratings yet

- CH 11Document51 pagesCH 11Quỳnh Anh Bùi ThịNo ratings yet

- GM Test Series: Top 50 QuestionsDocument96 pagesGM Test Series: Top 50 QuestionsSarvesh JoshiNo ratings yet

- 2016 AICPA FAR - ModerateDocument51 pages2016 AICPA FAR - ModerateTai D GiangNo ratings yet