Download as doc, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Group8-Baldwin Bicycle CompanyDocument9 pagesGroup8-Baldwin Bicycle CompanyChandrachuda SharmaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Sample Corporate Bylaws by Laws of "Company"Document8 pagesSample Corporate Bylaws by Laws of "Company"Cherlene TanNo ratings yet

- A Winning Formula: Debrief For The Asda Case (Chapter 14, Shaping Implementation Strategies) The Asda CaseDocument6 pagesA Winning Formula: Debrief For The Asda Case (Chapter 14, Shaping Implementation Strategies) The Asda CaseSpend ThriftNo ratings yet

- Cost ControlDocument3 pagesCost ControlAndry DepariNo ratings yet

- Internal Control - CMA LessonsDocument2 pagesInternal Control - CMA Lessonsbarakkat72No ratings yet

- DMC C Company Regulations Full VersionDocument76 pagesDMC C Company Regulations Full VersionAshutosh PandeyNo ratings yet

- Engineeringinterviewquestions Mcqs On Requirement Engineering AnswersDocument6 pagesEngineeringinterviewquestions Mcqs On Requirement Engineering Answersdevid mandefroNo ratings yet

- Sprint25a Rules November Start ENDocument7 pagesSprint25a Rules November Start ENsaraNo ratings yet

- A Case Study: Dara's DilemaDocument5 pagesA Case Study: Dara's DilemamaggyxhianNo ratings yet

- Bus Trans Taxes Key Solution PTVAT 2013 2014Document17 pagesBus Trans Taxes Key Solution PTVAT 2013 2014Jandave ApinoNo ratings yet

- Inflation. Interest Rates. Balance of Payments. Government Intervention. Other FactorsDocument2 pagesInflation. Interest Rates. Balance of Payments. Government Intervention. Other FactorsEmmanuelle RojasNo ratings yet

- DCartwright CV - 260510Document1 pageDCartwright CV - 260510nlcartw1No ratings yet

- What Is The Difference Between BOQ and EstimateDocument3 pagesWhat Is The Difference Between BOQ and Estimatemszsohail100% (1)

- Ralph LaurenDocument11 pagesRalph LaurenAnushkaNo ratings yet

- Pahalwan's: Need For A New Marketing StrategyDocument7 pagesPahalwan's: Need For A New Marketing StrategySrajan GuptaNo ratings yet

- Six Sigma Approach - NarrativeDocument10 pagesSix Sigma Approach - NarrativeBlairEmrallafNo ratings yet

- FQP Informative PricingDocument8 pagesFQP Informative PricingkingxyzgNo ratings yet

- Financial Accounting A Critical Approach Canadian Canadian 4th Edition John Friedlan Test BankDocument42 pagesFinancial Accounting A Critical Approach Canadian Canadian 4th Edition John Friedlan Test Bankmeganmooreobwypjenim100% (36)

- Bond Valuation: A Basic IntroductionDocument2 pagesBond Valuation: A Basic IntroductionAnooshayNo ratings yet

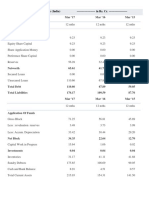

- Balance Sheet of Shakti PumpsDocument2 pagesBalance Sheet of Shakti PumpsAnonymous 3OudFL5xNo ratings yet

- Ôn Thi GK CSTMQTDocument14 pagesÔn Thi GK CSTMQTK60 Võ Nguyễn Ngọc HânNo ratings yet

- Module 1 Introduction To Business PolicyDocument54 pagesModule 1 Introduction To Business Policycha11100% (1)

- Law 346Document2 pagesLaw 346Nuradilah BahardinNo ratings yet

- 2012 MBA/IMBA Salary Survey: Career Development CentreDocument9 pages2012 MBA/IMBA Salary Survey: Career Development CentreLaura MontgomeryNo ratings yet

- Lean Customer Returns (BDD - MX) : Test Script SAP S/4HANA - 29-09-22Document31 pagesLean Customer Returns (BDD - MX) : Test Script SAP S/4HANA - 29-09-22Enrique MarquezNo ratings yet

- Treatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusDocument14 pagesTreatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusAnanthakumar ANo ratings yet

- Customer Buying Behavior: Retailing Management 8E © The Mcgraw-Hill Companies, All Rights ReservedDocument30 pagesCustomer Buying Behavior: Retailing Management 8E © The Mcgraw-Hill Companies, All Rights ReservedDavid Lumaban GatdulaNo ratings yet

- Sap S4hana Technical Lead. C201904-498-Saptl-SapDocument2 pagesSap S4hana Technical Lead. C201904-498-Saptl-SapRam PNo ratings yet

- Kaizen Costing: A Catalyst For Change and Continuous Cost ImprovementDocument16 pagesKaizen Costing: A Catalyst For Change and Continuous Cost ImprovementnoorNo ratings yet

- MCQ Set 1Document18 pagesMCQ Set 1Venkateswaran Sankar100% (1)