Download as xlsx, pdf, or txt

You might also like

- Allen Lane Case Write UpDocument2 pagesAllen Lane Case Write UpAndrew Choi100% (1)

- Question 6 - Genentech CaseDocument1 pageQuestion 6 - Genentech CaseApurv AgarwalNo ratings yet

- 17020841116Document13 pages17020841116Khushboo RajNo ratings yet

- GRP 8 - Roche and GenentechDocument9 pagesGRP 8 - Roche and GenentechRohit ShawNo ratings yet

- Genentech Case StudyDocument8 pagesGenentech Case StudyM H Dinesh Chowdhary100% (1)

- CH 12Document29 pagesCH 12Jean-Paul Moubarak100% (1)

- Tomtom Case Study AnswersDocument2 pagesTomtom Case Study AnswersSyedMuneebBukhari100% (1)

- Airline Simulation Instructions 2019Document22 pagesAirline Simulation Instructions 2019EK SystemsNo ratings yet

- Strengths and Weakness of Airborne FedexDocument2 pagesStrengths and Weakness of Airborne FedexSrilakshmi ShunmugarajNo ratings yet

- Case 3 PDFDocument14 pagesCase 3 PDFARE TVNo ratings yet

- Ch10 Martingale Lowvol RGDocument14 pagesCh10 Martingale Lowvol RGmaciel.gabrielaNo ratings yet

- 729318397Document4 pages729318397cavvas7201No ratings yet

- Exhibit 1Document2 pagesExhibit 1Natasha PerryNo ratings yet

- SFM Case4 Group7Document5 pagesSFM Case4 Group7AMAAN LULANIA 22100% (1)

- Fedex Vs UpsDocument8 pagesFedex Vs Upskevin316No ratings yet

- QuestionsDocument2 pagesQuestionsRza Rustamli0% (2)

- Porsche KeyDocument28 pagesPorsche KeyFaisal AlibrahimNo ratings yet

- M&A Analysis Roche GenentechDocument11 pagesM&A Analysis Roche GenentechtaposhdrNo ratings yet

- Jet Blue IPO CaseDocument4 pagesJet Blue IPO Casedivakar6250% (2)

- Sealed Air Corporation v1.0Document8 pagesSealed Air Corporation v1.0KshitishNo ratings yet

- CESIM CaseDocument8 pagesCESIM CaseDhawal PanchalNo ratings yet

- Harley Davidson Case Study - Building Brand CommunitiesDocument19 pagesHarley Davidson Case Study - Building Brand CommunitiesViet Long PlazaNo ratings yet

- ATH TechnologiesDocument3 pagesATH TechnologiesAnurag PGXPM15No ratings yet

- Attractive M&a Targets PART 1 v2Document24 pagesAttractive M&a Targets PART 1 v2Aman SrivastavaNo ratings yet

- LoeaDocument21 pagesLoeahddankerNo ratings yet

- Questions USX RevisedDocument1 pageQuestions USX RevisedShyngys SuiindikNo ratings yet

- M&A Case Competition: - Roche Acquisition of GenentechDocument19 pagesM&A Case Competition: - Roche Acquisition of GenentechJuan Diego Vasquez BeraunNo ratings yet

- USTDocument4 pagesUSTJames JeffersonNo ratings yet

- Stand-Alone Valuation (Dollars in Millions) : PPG Industries Metric Actual Projected 2011 2012E 2013EDocument4 pagesStand-Alone Valuation (Dollars in Millions) : PPG Industries Metric Actual Projected 2011 2012E 2013EStefanny cardonaNo ratings yet

- WACC Professional Management GudanceDocument17 pagesWACC Professional Management GudanceMagnatica TraducoesNo ratings yet

- Renault-Nissan Alliance Perspective: Thierry MOULONGUETDocument11 pagesRenault-Nissan Alliance Perspective: Thierry MOULONGUETSathish KumarNo ratings yet

- Introduction To Thomas Cook GroupDocument25 pagesIntroduction To Thomas Cook GroupDhaval PatelNo ratings yet

- Pernod RicardDocument18 pagesPernod RicardSarsal6067No ratings yet

- Evolution of Circus InduatryDocument2 pagesEvolution of Circus InduatrySiddhant Kumar DalmiaNo ratings yet

- Whirlpool Europe ERP CaseDocument7 pagesWhirlpool Europe ERP Casee3tester0% (1)

- Case Exhibits Roche GenentechDocument65 pagesCase Exhibits Roche GenentechheartxannaNo ratings yet

- Word Note Battle For Value FedEx Vs UPSDocument9 pagesWord Note Battle For Value FedEx Vs UPSalka murarka100% (1)

- UVA-F-1264: Printicomm's Proposed Acquisition of Digitech: Negotiating Price and Form of PaymentDocument14 pagesUVA-F-1264: Printicomm's Proposed Acquisition of Digitech: Negotiating Price and Form of PaymentKumarNo ratings yet

- Wikler Case Competition PowerpointDocument16 pagesWikler Case Competition Powerpointbtlala0% (1)

- Hausser Foods SCDocument6 pagesHausser Foods SCHumphrey OsaigbeNo ratings yet

- Diageo Was Conglomerate Involved in Food and Beverage Industry in 1997Document6 pagesDiageo Was Conglomerate Involved in Food and Beverage Industry in 1997Prashant BezNo ratings yet

- APO Group-6 Calveta Dining Services IncDocument10 pagesAPO Group-6 Calveta Dining Services IncKartik SharmaNo ratings yet

- Anuary 2008 Société Générale Trading Loss IncidentDocument7 pagesAnuary 2008 Société Générale Trading Loss IncidentgabikubatNo ratings yet

- Debt Policy at Ust Inc Case AnalysisDocument23 pagesDebt Policy at Ust Inc Case AnalysisLouie Ram50% (2)

- $RA3R8K9Document4 pages$RA3R8K9SamitRanjanNo ratings yet

- CalvetaDocument11 pagesCalvetaAnonymous 3Pk0Oj100% (1)

- I Introduction: Globalization: Globe Assignment QuestionsDocument11 pagesI Introduction: Globalization: Globe Assignment QuestionsKARTHIK145No ratings yet

- Turnaround StrategyDocument2 pagesTurnaround Strategyamittripathy084783No ratings yet

- Acova Radiateurs (v7)Document4 pagesAcova Radiateurs (v7)Sarvagya JhaNo ratings yet

- Financial Management E BookDocument4 pagesFinancial Management E BookAnshul MishraNo ratings yet

- Transworld Xls460 Xls EngDocument6 pagesTransworld Xls460 Xls EngAman Pawar0% (1)

- Was Robert Cizik's Diversification Strategy Consistent With The Company Priorities?Document8 pagesWas Robert Cizik's Diversification Strategy Consistent With The Company Priorities?minionNo ratings yet

- Bed Bath Beyond (BBBY) Stock ReportDocument14 pagesBed Bath Beyond (BBBY) Stock Reportcollegeanalysts100% (2)

- Applied Research Technologies PDFDocument18 pagesApplied Research Technologies PDFsandunNo ratings yet

- Hulu or Not To HuluDocument24 pagesHulu or Not To HulufadhlulNo ratings yet

- Roadshow Natixis Mar09Document47 pagesRoadshow Natixis Mar09sl7789No ratings yet

- Bank of Kigali Announces Q1 2010 ResultsDocument7 pagesBank of Kigali Announces Q1 2010 ResultsBank of KigaliNo ratings yet

- Background KnowledgeDocument7 pagesBackground Knowledgeanamsaeed1No ratings yet

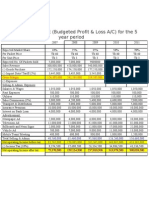

- Financial Statement (Budgeted Profit & Loss A/C) For The 5 Year PeriodDocument1 pageFinancial Statement (Budgeted Profit & Loss A/C) For The 5 Year PeriodShakhawat Hossen MunnaNo ratings yet