Download as pdf or txt

You might also like

- Cash NarrativeDocument4 pagesCash NarrativeCaterina De LucaNo ratings yet

- Cash ManagementDocument8 pagesCash ManagementDeirdre Mae Kindipan100% (1)

- Larson12e 04Document60 pagesLarson12e 04samas7480No ratings yet

- Bank Branch Internal Audit Work ProgramDocument31 pagesBank Branch Internal Audit Work Programozlem100% (1)

- Deposit Function PDFDocument75 pagesDeposit Function PDFrojon pharmacyNo ratings yet

- Internal Controls-Accounting DepartmentDocument9 pagesInternal Controls-Accounting DepartmentInes Hamoy JunioNo ratings yet

- Sample Revenue PolicyDocument6 pagesSample Revenue Policyvb_krishnaNo ratings yet

- Financial & Accounting Policies & ProceduresDocument34 pagesFinancial & Accounting Policies & ProceduresAnnabel Strange100% (6)

- CH 2.0-PLAN THE CASH EXAMINATIONDocument12 pagesCH 2.0-PLAN THE CASH EXAMINATIONBon Carlo Medina MelocotonNo ratings yet

- MBOF912D-Financial Management-Assignment-1Document15 pagesMBOF912D-Financial Management-Assignment-1Utkarsh Singh0% (1)

- Books 5Document53 pagesBooks 5Nagesh BabuNo ratings yet

- Chapter No.02: Internal ControlDocument28 pagesChapter No.02: Internal ControlMasood khanNo ratings yet

- Chapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashDocument35 pagesChapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashEmey CalbayNo ratings yet

- Balance Means Misstatement of Some Other AccountsDocument3 pagesBalance Means Misstatement of Some Other AccountsKaila Mae Tan DuNo ratings yet

- Unit 2 Audit of Cash and Marketable SecuritiesDocument9 pagesUnit 2 Audit of Cash and Marketable Securitiessolomon adamuNo ratings yet

- 4.account Opening RequirmentsDocument16 pages4.account Opening RequirmentsTaonga Jean BandaNo ratings yet

- CashDocument9 pagesCashHenok EnkuselassieNo ratings yet

- Chapter 2 Audit Cash PDFDocument6 pagesChapter 2 Audit Cash PDFalemayehu100% (2)

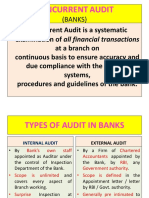

- Concurrent-Audit GuideDocument71 pagesConcurrent-Audit GuideFenil RamaniNo ratings yet

- Section X 185 - Internal Control SystemDocument12 pagesSection X 185 - Internal Control SystemThessaloe B. FernandezNo ratings yet

- Cash Handling and Accounts Receivable Policy PresentationDocument22 pagesCash Handling and Accounts Receivable Policy PresentationJSNo ratings yet

- Sample Internal Controls Policy: 1. GeneralDocument2 pagesSample Internal Controls Policy: 1. Generalvb_krishnaNo ratings yet

- AUD Module 3 - Audit of CashDocument25 pagesAUD Module 3 - Audit of CashChristine CariñoNo ratings yet

- 03 Audit of CashDocument14 pages03 Audit of CashJoyce Anne GarduqueNo ratings yet

- Cash Management:: Revenue DepositsDocument26 pagesCash Management:: Revenue DepositsMomel FatimaNo ratings yet

- Annexure I (Scope of Audit - Concurrent Auditor)Document29 pagesAnnexure I (Scope of Audit - Concurrent Auditor)Niraj JainNo ratings yet

- Chapter 4 - Cash and Internal ControlsDocument10 pagesChapter 4 - Cash and Internal Controlsvictoria.05.santosNo ratings yet

- RICS - Client's Money - 04 April 2011 (HC)Document10 pagesRICS - Client's Money - 04 April 2011 (HC)jawadkollackanNo ratings yet

- 6 Cash TransactionsDocument29 pages6 Cash TransactionsZindgiKiKhatirNo ratings yet

- Vouching of Trading Transactions: Unit 2Document6 pagesVouching of Trading Transactions: Unit 2Muskan TyagiNo ratings yet

- VouchingDocument8 pagesVouchingGyanesh DoshiNo ratings yet

- Scope of Concurrent AuditDocument17 pagesScope of Concurrent AuditAnandNo ratings yet

- Roles and Responsibilities & Taking Over: Module-1Document15 pagesRoles and Responsibilities & Taking Over: Module-1kailas bankNo ratings yet

- Unit-2 Audit of Cash and Marketable SecuritiesDocument6 pagesUnit-2 Audit of Cash and Marketable SecuritiesKiya AbdiNo ratings yet

- Infolink University Collge Coursetitle: Auditing Principles and Practics Ii Credit HRS: 3 Contact Hrs:3 InstructorDocument94 pagesInfolink University Collge Coursetitle: Auditing Principles and Practics Ii Credit HRS: 3 Contact Hrs:3 InstructorBeka AsraNo ratings yet

- Chapter-2: Audit of Cash and Marketable SecuritiesDocument27 pagesChapter-2: Audit of Cash and Marketable Securitiesbikilahussen100% (1)

- Chapter 6 - Cash & Internal ControlDocument12 pagesChapter 6 - Cash & Internal ControlHareem Zoya WarsiNo ratings yet

- The Deposit FunctionDocument17 pagesThe Deposit FunctionNigel N. SilvestreNo ratings yet

- Chapter 20 - Answer PDFDocument10 pagesChapter 20 - Answer PDFjhienellNo ratings yet

- Bank AlfalahDocument19 pagesBank Alfalahsaba_qmarNo ratings yet

- Cash Receipts CycleDocument4 pagesCash Receipts CycleYenNo ratings yet

- 13application of Audit Process To Transaction Part 1Document5 pages13application of Audit Process To Transaction Part 1palicpicestepanyaNo ratings yet

- Clearing House OperationDocument22 pagesClearing House Operationshivam_7074k100% (1)

- Sub Treasury Training ReportDocument7 pagesSub Treasury Training ReportsrmurralitharanNo ratings yet

- Universal Teller - Hyderabad, Sukkur & GujranwalaDocument2 pagesUniversal Teller - Hyderabad, Sukkur & GujranwalaBilalTariqNo ratings yet

- E2C-FMP-008 Accounting and Finance ProcedureDocument12 pagesE2C-FMP-008 Accounting and Finance ProcedureVPN NetworkNo ratings yet

- Accounting For Government Revenue and Expenditure.Document19 pagesAccounting For Government Revenue and Expenditure.ERICK MLINGWANo ratings yet

- Branch Operations ControlDocument49 pagesBranch Operations ControlCASIDSID, JONALYN A.No ratings yet

- Chapter 2 AUDIT OF CASH& MARKETABLE SECURITYDocument7 pagesChapter 2 AUDIT OF CASH& MARKETABLE SECURITYsteveiamidNo ratings yet

- Approach For Safety of Loans Follow Up and Monitoring Process Q3Document6 pagesApproach For Safety of Loans Follow Up and Monitoring Process Q3maunilshahNo ratings yet

- Unit 2Document11 pagesUnit 2fekadegebretsadik478729No ratings yet

- RB Chapter 2A-Current Account-MITCDocument9 pagesRB Chapter 2A-Current Account-MITCRohit KumarNo ratings yet

- Internal Control Procedures Chapter 4Document32 pagesInternal Control Procedures Chapter 4lukeNo ratings yet

- F.2. Basic Bank Documents and Terminologies Related To BankDocument28 pagesF.2. Basic Bank Documents and Terminologies Related To BankSecret DeityNo ratings yet

- BankingDocument47 pagesBankingDeepansh GoyalNo ratings yet

- Secretarial Accounting 2Document98 pagesSecretarial Accounting 2NabuteNo ratings yet

- Sample Sacco Internal Controls PolicyDocument11 pagesSample Sacco Internal Controls PolicyAmulioto Elijah MuchelleNo ratings yet

- Bank Reconciliation Best PracticesDocument3 pagesBank Reconciliation Best Practiceshossainmz100% (2)

- Universal Teller - Karachi, Lahore, Islamabad, Abbottabad, KhairpurDocument2 pagesUniversal Teller - Karachi, Lahore, Islamabad, Abbottabad, KhairpurBilalTariqNo ratings yet

- Textbook of Urgent Care Management: Chapter 13, Financial ManagementFrom EverandTextbook of Urgent Care Management: Chapter 13, Financial ManagementNo ratings yet

- The beautiful side to border townsDocument2 pagesThe beautiful side to border townsjoachimjackNo ratings yet

- La Estrella, AragonDocument9 pagesLa Estrella, AragonjoachimjackNo ratings yet

- Metrobank List of RequirementsDocument1 pageMetrobank List of RequirementsjoachimjackNo ratings yet

- Review of Scruton's book On Human NatureDocument7 pagesReview of Scruton's book On Human NaturejoachimjackNo ratings yet

- Adoro te devote translationDocument1 pageAdoro te devote translationjoachimjackNo ratings yet

- PQF LevelsDocument2 pagesPQF LevelsjoachimjackNo ratings yet

- Whose Common Good CountsDocument19 pagesWhose Common Good CountsjoachimjackNo ratings yet

- Michel Foucault (from Fazio book)Document4 pagesMichel Foucault (from Fazio book)joachimjackNo ratings yet

- Answering a leading questionDocument3 pagesAnswering a leading questionjoachimjackNo ratings yet

- Derrida and Rorty (from Fazio book)Document5 pagesDerrida and Rorty (from Fazio book)joachimjackNo ratings yet

- Finnis-What Is A LawDocument7 pagesFinnis-What Is A LawjoachimjackNo ratings yet

- PECR Petroleum Area Map FDocument1 pagePECR Petroleum Area Map FjoachimjackNo ratings yet

- The Spanish-American War, 1898: MILESTONES: 1866-1898Document2 pagesThe Spanish-American War, 1898: MILESTONES: 1866-1898joachimjackNo ratings yet

- dc2007-5847 EDCDocument1 pagedc2007-5847 EDCjoachimjackNo ratings yet

- SCMAPDocument1 pageSCMAPjoachimjackNo ratings yet

- The Role of History in ScienceDocument9 pagesThe Role of History in SciencejoachimjackNo ratings yet

- POs and PEOsDocument8 pagesPOs and PEOsjoachimjackNo ratings yet

- Historical Case Against Roe v. WadeDocument7 pagesHistorical Case Against Roe v. WadejoachimjackNo ratings yet

- PSALM - Industry ProspectusDocument15 pagesPSALM - Industry ProspectusjoachimjackNo ratings yet

- Sec Cert - Simlong Energy Increase of Capital Stock 07-13-21Document1 pageSec Cert - Simlong Energy Increase of Capital Stock 07-13-21joachimjackNo ratings yet

- Committee On Accountability of Public Officers and Investigations (Blue Ribbon)Document38 pagesCommittee On Accountability of Public Officers and Investigations (Blue Ribbon)joachimjackNo ratings yet

- Active Petroleum Contracts RevisedDocument2 pagesActive Petroleum Contracts RevisedjoachimjackNo ratings yet

- Why Did CJ Roberts Disagree With Overturning Roe V WadeDocument4 pagesWhy Did CJ Roberts Disagree With Overturning Roe V WadejoachimjackNo ratings yet

- Philippine Historiography and Colonial DDocument26 pagesPhilippine Historiography and Colonial DjoachimjackNo ratings yet

- Summa Theologica On LawDocument2 pagesSumma Theologica On LawjoachimjackNo ratings yet

- Archbishop Niederauer On Pelosi's Abortion RemarksDocument4 pagesArchbishop Niederauer On Pelosi's Abortion RemarksjoachimjackNo ratings yet

- Dovie Beams and Philippine Politics A PRDocument42 pagesDovie Beams and Philippine Politics A PRjoachimjackNo ratings yet

- On The Code of MaragtasDocument7 pagesOn The Code of MaragtasjoachimjackNo ratings yet

- Statement of Income and Expenditures (CY2002) Provinces/Cities/Municipalities CombinedDocument19 pagesStatement of Income and Expenditures (CY2002) Provinces/Cities/Municipalities CombinedjoachimjackNo ratings yet

- HBS Article - The Process of Strategy Definition and ImplementationDocument9 pagesHBS Article - The Process of Strategy Definition and ImplementationSHAILY KASAUNDHANNo ratings yet

- Erp Implementation of Ifrs For Smes: DissertationDocument68 pagesErp Implementation of Ifrs For Smes: DissertationGaurav Kumar Kureel100% (1)

- 1q Entrep Module Week 1 MidtermDocument29 pages1q Entrep Module Week 1 MidtermjerrilynagaraoNo ratings yet

- Domestic Travel ReadingDocument3 pagesDomestic Travel ReadingBenian TuncelNo ratings yet

- Adam SmithDocument13 pagesAdam Smithshabbar aliNo ratings yet

- Triveni Turbine PDFDocument144 pagesTriveni Turbine PDFmpgzyahNo ratings yet

- International Cha 2Document26 pagesInternational Cha 2felekebirhanu7No ratings yet

- Management by Objectives (MBO)Document25 pagesManagement by Objectives (MBO)John BerkmansNo ratings yet

- Senior Relationship ManagerDocument1 pageSenior Relationship ManagerParamjit singh MakkarNo ratings yet

- Thomas L. Wheelen J. David HungerDocument19 pagesThomas L. Wheelen J. David HungerAriel AlvarezNo ratings yet

- Bridgeport CT Adopted Budget 2010-2011Document552 pagesBridgeport CT Adopted Budget 2010-2011BridgeportCTNo ratings yet

- Agri TourismDocument5 pagesAgri TourismPradeep Reddy BoppidiNo ratings yet

- 5 - Econ - Advanced Economic Theory (Eng)Document1 page5 - Econ - Advanced Economic Theory (Eng)David JackNo ratings yet

- FROM: 4. TO:: LM - PodDocument1 pageFROM: 4. TO:: LM - PodBewabaNo ratings yet

- REVENUE MEMORANDUM CIRCULAR NO. 64-2020 Issued On June 24, 2020 CircularizesDocument2 pagesREVENUE MEMORANDUM CIRCULAR NO. 64-2020 Issued On June 24, 2020 CircularizesAceGun'nerNo ratings yet

- ECO 306 Final Project II Sarai SternzisDocument8 pagesECO 306 Final Project II Sarai SternzisSarai SternzisNo ratings yet

- Appellants Memorial - RDocument42 pagesAppellants Memorial - RNiteshMaheshwari100% (1)

- Case On Restrutthis Case Is To Understand Capital RestructuringDocument17 pagesCase On Restrutthis Case Is To Understand Capital RestructuringPriyanka DwivediNo ratings yet

- Lange - On The Economic Theory of Socialism PDFDocument2 pagesLange - On The Economic Theory of Socialism PDFCarlosAntonioPerezGuzmanNo ratings yet

- JVZOO Cash Ebook PDFDocument38 pagesJVZOO Cash Ebook PDFderic soon100% (2)

- Industryanalysis-Porter'S Five Forces FrameworkDocument9 pagesIndustryanalysis-Porter'S Five Forces FrameworkHaseeb TariqNo ratings yet

- COBIT OverviewDocument17 pagesCOBIT OverviewPriambodoNo ratings yet

- Catherine Morris - Demystifying SustainabilityDocument34 pagesCatherine Morris - Demystifying SustainabilityshivalikaNo ratings yet

- Southern University BangladeshDocument1 pageSouthern University BangladeshRaihanNo ratings yet

- Uw 19 Phy Bs 059Document1 pageUw 19 Phy Bs 059Afghan LoralaiNo ratings yet

- Paper The Prophet of InnovationDocument11 pagesPaper The Prophet of InnovationDiogo FidelesNo ratings yet

- Topic: Key Account Management, Strategies & Practices in Pharmaceutical Industry of India. A SynopsisDocument5 pagesTopic: Key Account Management, Strategies & Practices in Pharmaceutical Industry of India. A Synopsissanjeev_soni725951No ratings yet

- Bharathidasan University, Tiruchirappalli.: M.B.A.November-2021 Examinations Time TableDocument3 pagesBharathidasan University, Tiruchirappalli.: M.B.A.November-2021 Examinations Time TableSiva MoorthyNo ratings yet