Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Marketing Analytical Nano DegreeDocument6 pagesMarketing Analytical Nano DegreemanedeepNo ratings yet

- Snow Itsm OvervDocument5 pagesSnow Itsm OvervmanedeepNo ratings yet

- Utility GuideDocument630 pagesUtility GuidemanedeepNo ratings yet

- HCM92ERDInstructions FinalDocument8 pagesHCM92ERDInstructions FinalmanedeepNo ratings yet

- Poweredge Made DetailsDocument15 pagesPoweredge Made DetailsmanedeepNo ratings yet

- Simpleworkflow in The Cloud: Poa June 17, 2010 Alan Robbins and Rick SearsDocument99 pagesSimpleworkflow in The Cloud: Poa June 17, 2010 Alan Robbins and Rick SearsmanedeepNo ratings yet

- Cheques The Facts 2012Document35 pagesCheques The Facts 2012manedeepNo ratings yet

- Changing Character Set To UTF8 For Oracle DatabaseDocument9 pagesChanging Character Set To UTF8 For Oracle DatabasemanedeepNo ratings yet

- About Peoplesoft Feature PackDocument15 pagesAbout Peoplesoft Feature PackmanedeepNo ratings yet

- Bearing The Burden of DSTDocument3 pagesBearing The Burden of DSTchris cardinoNo ratings yet

- Ethics of Tax AvoidanceDocument13 pagesEthics of Tax AvoidanceRashmi SharmaNo ratings yet

- Zakon o Potvrdjivanju ZajmaDocument41 pagesZakon o Potvrdjivanju ZajmaSlavoljub AleksicNo ratings yet

- Assgn-I Marketing Mix Zara and H&MDocument40 pagesAssgn-I Marketing Mix Zara and H&Mzayana kadeeja100% (1)

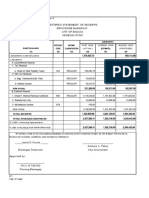

- Past Year Current Year Budget Year (Actual) (Proposed)Document16 pagesPast Year Current Year Budget Year (Actual) (Proposed)Saphire DonsolNo ratings yet

- Minimum Alternate Tax: Prepared by - Dhaval Girishkumar TrivediDocument21 pagesMinimum Alternate Tax: Prepared by - Dhaval Girishkumar TrivediSmit NareshNo ratings yet

- Chapter 9 BusinessDocument26 pagesChapter 9 BusinessAnamta RizwanNo ratings yet

- Section 54ED, Income Tax Act, 1961 2015: Explanation.-For The Purposes of This Sub SectionDocument2 pagesSection 54ED, Income Tax Act, 1961 2015: Explanation.-For The Purposes of This Sub SectionSushil GuptaNo ratings yet

- PBCom v. CIR DigestDocument1 pagePBCom v. CIR DigestRonnie Garcia Del RosarioNo ratings yet

- Siya - BCH 17 216 (Project)Document42 pagesSiya - BCH 17 216 (Project)ManthanNo ratings yet

- Net 57,000 Date (5.II.e)Document11 pagesNet 57,000 Date (5.II.e)Kyree VladeNo ratings yet

- Secial Terms and Conditions of RFQ 1.0 CommunicationDocument14 pagesSecial Terms and Conditions of RFQ 1.0 CommunicationKarandeep SinghNo ratings yet

- Worst Fracking RegsDocument6 pagesWorst Fracking RegsJames "Chip" NorthrupNo ratings yet

- Receipt - 25-10-2021 (1.)Document2 pagesReceipt - 25-10-2021 (1.)Lim LikweeNo ratings yet

- Financial Planning F-FIBA306Document261 pagesFinancial Planning F-FIBA306Cornelius NarteyNo ratings yet

- An Enquiry Into The Effect of GST On Real Estate Sector of IndiaDocument5 pagesAn Enquiry Into The Effect of GST On Real Estate Sector of IndiaEditor IJTSRDNo ratings yet

- Obillos, Jr. vs. Cir - 139 Scra 436Document4 pagesObillos, Jr. vs. Cir - 139 Scra 436Ygh E SargeNo ratings yet

- EY Budget Flash 2021Document12 pagesEY Budget Flash 2021Anam IqbalNo ratings yet

- Government Spending, Public Debt and Economic Growth in KenyaDocument12 pagesGovernment Spending, Public Debt and Economic Growth in KenyaResearch ParkNo ratings yet

- Doing Business in The Philippines (Why The Philippines?)Document14 pagesDoing Business in The Philippines (Why The Philippines?)Lianna RodriguezNo ratings yet

- DTC Agreement Between United Kingdom and Gambia, TheDocument36 pagesDTC Agreement Between United Kingdom and Gambia, TheOECD: Organisation for Economic Co-operation and DevelopmentNo ratings yet

- IE MergedDocument173 pagesIE MergedOm PrakashNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Nishkarsh SinghNo ratings yet

- Drilon v. Lim, GR. No. 112497, August 4, 1994Document1 pageDrilon v. Lim, GR. No. 112497, August 4, 1994Pio Guieb AguilarNo ratings yet

- Agreement To Demolish/Remove and Reconstruct Improvement (Adri)Document4 pagesAgreement To Demolish/Remove and Reconstruct Improvement (Adri)PANGINOON LOVENo ratings yet

- Tax 05 Final Taxes Part 1Document5 pagesTax 05 Final Taxes Part 1Panda CocoNo ratings yet

- Amount Chargeable (In Words) E. & O.EDocument1 pageAmount Chargeable (In Words) E. & O.EManish JaiswalNo ratings yet

- BMBEs (RA 9178), IRRDocument5 pagesBMBEs (RA 9178), IRRtagabantayNo ratings yet

- RMC No. 44-2021 RevisedDocument2 pagesRMC No. 44-2021 RevisedDessere Ann AnchetaNo ratings yet

- Compilation of Band 9 Essays For Ielts Writing Task 2Document20 pagesCompilation of Band 9 Essays For Ielts Writing Task 2tim man100% (1)