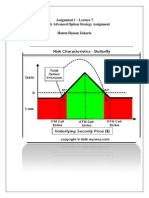

Assignment 1 - Lecture 4 Protective Call & Covered Call Probelm Hatem Hassan Zakaria

Assignment 1 - Lecture 4 Protective Call & Covered Call Probelm Hatem Hassan Zakaria

You might also like

- Chapter 7 Workout SheetDocument14 pagesChapter 7 Workout Sheetanh sy tranNo ratings yet

- Situational Leadership MANAGEMENTDocument2 pagesSituational Leadership MANAGEMENTHatem Hassan89% (9)

- SCDL - Marketing ManagementDocument20 pagesSCDL - Marketing Managementpradipta_moh100% (1)

- Fin 645 11906130 PDFDocument7 pagesFin 645 11906130 PDFPrateek SehgalNo ratings yet

- An Example of A Marketing PlanDocument8 pagesAn Example of A Marketing PlanJannie Aldrin SiahaanNo ratings yet

- Dividend Policy and Internal FinancingDocument14 pagesDividend Policy and Internal FinancingMichaela San Diego0% (1)

- Toby Crabel - Opening Range Breakout (Part1-8)Document39 pagesToby Crabel - Opening Range Breakout (Part1-8)saisonia75% (8)

- Different Option StrategiesDocument43 pagesDifferent Option StrategiessizzlingabheeNo ratings yet

- Bull Call Spread & Put SpreadDocument16 pagesBull Call Spread & Put Spreadravirana60No ratings yet

- Strategy Guide: Bull Call SpreadDocument14 pagesStrategy Guide: Bull Call SpreadworkNo ratings yet

- Ratio Back SpreadsDocument20 pagesRatio Back SpreadsOladipupo Mayowa PaulNo ratings yet

- Option Trading Strategies & Option SpreadsDocument30 pagesOption Trading Strategies & Option SpreadsPushkar GautamNo ratings yet

- Problem Set 3-Group 9Document6 pagesProblem Set 3-Group 9WristWork Entertainment100% (1)

- Margin TradingDocument11 pagesMargin TradingAvi RajNo ratings yet

- Hedging Risk With DerivativesDocument36 pagesHedging Risk With DerivativesSoumyadeep RoyNo ratings yet

- What Is The Maximum Loss or Profit With A Covered CallDocument3 pagesWhat Is The Maximum Loss or Profit With A Covered CallJonhmark AniñonNo ratings yet

- Put-Call Parity: By: Shruti Agrawal-201 Suhas Anjaria-202 Kankana Dutta-205 Aabhas Garg-207Document24 pagesPut-Call Parity: By: Shruti Agrawal-201 Suhas Anjaria-202 Kankana Dutta-205 Aabhas Garg-207Aabbhas GargNo ratings yet

- Derivatives Option StrategiesDocument45 pagesDerivatives Option Strategiesjim125No ratings yet

- Derivatives Talking PointsDocument4 pagesDerivatives Talking PointsAlice KujurNo ratings yet

- Derivatives Buy PutDocument10 pagesDerivatives Buy PutRajan kumar singhNo ratings yet

- Derivatives Buy PutDocument11 pagesDerivatives Buy PutRajan kumar singhNo ratings yet

- Butterfly + Broken Wing ButterflyDocument4 pagesButterfly + Broken Wing ButterflyMrityunjay Kumar100% (1)

- Option Strategy Builder Client PDFDocument13 pagesOption Strategy Builder Client PDFसन्तोष सिंह जादौनNo ratings yet

- 02 Market Mechanics 2Document16 pages02 Market Mechanics 2倪采萱No ratings yet

- Soln CH 20 Option IntroDocument14 pagesSoln CH 20 Option IntroSilviu TrebuianNo ratings yet

- Msc. Accounting and FinanceDocument18 pagesMsc. Accounting and FinancerytchluvNo ratings yet

- Butterfly Advanced Option Strategy AssignmentDocument3 pagesButterfly Advanced Option Strategy AssignmentHatem HassanNo ratings yet

- Study Report On Option Trading Strategies in Equity DerivativesDocument33 pagesStudy Report On Option Trading Strategies in Equity DerivativesDeepak Singh MauryaNo ratings yet

- Option StrategiesDocument33 pagesOption Strategiessurinder vermaNo ratings yet

- Jignesh Shah Dhiren Prajapati Kaustubh Parkar Akash Jadhav Deepali Jain Rahul GavaliDocument43 pagesJignesh Shah Dhiren Prajapati Kaustubh Parkar Akash Jadhav Deepali Jain Rahul GavaliDhiren Praj100% (1)

- HedgingDocument5 pagesHedgingGm EaswarNo ratings yet

- Video 12 - Bull Call Spread Strategy - UsefulDocument4 pagesVideo 12 - Bull Call Spread Strategy - Usefulshalomhanyane9No ratings yet

- Introduction To OptionsDocument9 pagesIntroduction To OptionsKumar NarayananNo ratings yet

- Intro To OptionsDocument9 pagesIntro To OptionsAntonio GenNo ratings yet

- Option and FutureDocument28 pagesOption and Futuresunil_das95No ratings yet

- Finance Questions and SolutionsDocument10 pagesFinance Questions and SolutionsEli Koech100% (1)

- Mai Thanh Hà - 22106200 - Portfolio Week 5 - Deri-T124WSB-3Document7 pagesMai Thanh Hà - 22106200 - Portfolio Week 5 - Deri-T124WSB-3Mai HàNo ratings yet

- Options CA - CS.CMA - MBA: Naveen. RohatgiDocument38 pagesOptions CA - CS.CMA - MBA: Naveen. RohatgiDivyaNo ratings yet

- Finance AssignmentDocument12 pagesFinance AssignmentYanni PoonNo ratings yet

- Options StrategiesDocument9 pagesOptions Strategiessneha496100% (1)

- 04 - 05 - Option Strategies & Payoff'sDocument66 pages04 - 05 - Option Strategies & Payoff'sMohammedAveshNagoriNo ratings yet

- Options Presentation123Document21 pagesOptions Presentation123KajalPahwaNo ratings yet

- Unit 6 Option CombinationsDocument13 pagesUnit 6 Option CombinationsFadil Ashrafi Barkati KhanNo ratings yet

- Options MSCFIÂ DECÂ 2022Document8 pagesOptions MSCFIÂ DECÂ 2022kenedy simwingaNo ratings yet

- Potm Video 3 Not-Useful Options Trading StrategiesDocument38 pagesPotm Video 3 Not-Useful Options Trading StrategiesIsIs DroneNo ratings yet

- Financial Risk Management ExercisesDocument20 pagesFinancial Risk Management ExercisesChau NguyenNo ratings yet

- Stock Option BasicsDocument62 pagesStock Option BasicsArvind DasNo ratings yet

- Long Call Condor - An Option Strategy: TH THDocument7 pagesLong Call Condor - An Option Strategy: TH THAasthaNo ratings yet

- Options Theory For Professional TradingDocument4 pagesOptions Theory For Professional TradingRaju.KonduruNo ratings yet

- Study Notes Trading StrategiesDocument16 pagesStudy Notes Trading Strategiesalok kundaliaNo ratings yet

- Chap3 Introduction To Options (Derivatives)Document30 pagesChap3 Introduction To Options (Derivatives)Jihen MejriNo ratings yet

- Derivatives - Options: Mahesh GujarDocument22 pagesDerivatives - Options: Mahesh GujarMahesh GujarNo ratings yet

- Ch11 An Introduction To Derivative SecuritiesDocument37 pagesCh11 An Introduction To Derivative SecuritiesMila AmandaNo ratings yet

- Options "The Rising Wave"Document30 pagesOptions "The Rising Wave"Neeal ParikhNo ratings yet

- Options & ModelsDocument48 pagesOptions & ModelsPraveen Kumar SinhaNo ratings yet

- Derivatives TrainingDocument83 pagesDerivatives TrainingvaibhavgdNo ratings yet

- Option Strategies PDFDocument5 pagesOption Strategies PDFdhanabal sNo ratings yet

- Put-Call Parity TheoremDocument4 pagesPut-Call Parity TheoremAmol SarafNo ratings yet

- Brokerage Transactions Stock MarketDocument17 pagesBrokerage Transactions Stock MarketMohsin SadaqatNo ratings yet

- Chapter 15 Exchange Traded Options Money and Capitals Market AFW1300/AFF1300Document5 pagesChapter 15 Exchange Traded Options Money and Capitals Market AFW1300/AFF1300Meng YeeNo ratings yet

- MGMT149 HW1Document5 pagesMGMT149 HW1Lin Lin KanokkornNo ratings yet

- Call OptionDocument1 pageCall OptionMustafa BhaiNo ratings yet

- Options Trading For Beginners: Tips, Formulas and Strategies For Traders to Make Money with OptionsFrom EverandOptions Trading For Beginners: Tips, Formulas and Strategies For Traders to Make Money with OptionsNo ratings yet

- OPTIONS TRADING: Mastering the Art of Options Trading for Financial Success (2023 Guide for Beginners)From EverandOPTIONS TRADING: Mastering the Art of Options Trading for Financial Success (2023 Guide for Beginners)No ratings yet

- Assignment 1 Chapter 8Document4 pagesAssignment 1 Chapter 8Hatem HassanNo ratings yet

- Credit Risk Management in BanksDocument31 pagesCredit Risk Management in BanksHatem HassanNo ratings yet

- Hatem Hassan Zakaria - Juhayna Co. Credit AnalysisDocument49 pagesHatem Hassan Zakaria - Juhayna Co. Credit AnalysisHatem Hassan100% (3)

- Assignment 1 Chapter 1Document9 pagesAssignment 1 Chapter 1Hatem HassanNo ratings yet

- Butterfly Advanced Option Strategy AssignmentDocument3 pagesButterfly Advanced Option Strategy AssignmentHatem HassanNo ratings yet

- Al Andalous PharmaceuticalsDocument17 pagesAl Andalous PharmaceuticalsHatem HassanNo ratings yet

- Thirlwall BOP EquilibriumDocument1 pageThirlwall BOP EquilibriumHatem HassanNo ratings yet

- Bop AnalysisDocument13 pagesBop AnalysisHatem HassanNo ratings yet

- Table: 19: Country:Eg Yp T B Al Ance of PaymentsDocument2 pagesTable: 19: Country:Eg Yp T B Al Ance of PaymentsHatem HassanNo ratings yet

- The Contexts of International BusinessDocument8 pagesThe Contexts of International BusinessHatem HassanNo ratings yet

- Sean Bing-Xuan NG Aqil 4057076 1945105348Document12 pagesSean Bing-Xuan NG Aqil 4057076 1945105348wong ming shengNo ratings yet

- IM 1 - Ronishka MaharjanDocument8 pagesIM 1 - Ronishka MaharjanRoni MaharjanNo ratings yet

- Vacera Investments Beverage Marketing PlanDocument2 pagesVacera Investments Beverage Marketing PlanOdoi DerekNo ratings yet

- Chapter 18 - Managing Marketing in The Global EconomyDocument48 pagesChapter 18 - Managing Marketing in The Global EconomyArman100% (2)

- Service Marketing MixDocument9 pagesService Marketing MixBashi Taizya100% (1)

- Anil PalaDocument4 pagesAnil Palageetha raniNo ratings yet

- Globalización? Análisis de Su Marketing-Mix Internacional: Mango: ¿Un Caso de Estrategia y Política deDocument15 pagesGlobalización? Análisis de Su Marketing-Mix Internacional: Mango: ¿Un Caso de Estrategia y Política demichxel psNo ratings yet

- Introduction To Economics - Class NotesDocument33 pagesIntroduction To Economics - Class NotesEliot PrimoNo ratings yet

- Cycle Agarbatti: Everyone Has A Reason To PrayDocument4 pagesCycle Agarbatti: Everyone Has A Reason To PrayRS10031986No ratings yet

- Mid Term RevisionDocument9 pagesMid Term RevisionRabie HarounNo ratings yet

- How To Prepare Economy? Exam Microeconomics Macroecono Mics Indian EconomyDocument8 pagesHow To Prepare Economy? Exam Microeconomics Macroecono Mics Indian EconomyAchuth GangadharanNo ratings yet

- Financial MarketDocument12 pagesFinancial Marketharshrajak822No ratings yet

- Reflection Paper On EconomicsDocument15 pagesReflection Paper On EconomicsRexan Dagreat Casas67% (3)

- 0205 ReposedDocument45 pages0205 ReposedLameuneNo ratings yet

- Full Analysis of Candlestick PatternsDocument67 pagesFull Analysis of Candlestick PatternsIm CupidNo ratings yet

- Jayoti Vidyapeeth Women'S University, Jaipur: Through ACT No. 17 of 2008 As Per UGC ACT 1956 NAAC Accredited UniversityDocument9 pagesJayoti Vidyapeeth Women'S University, Jaipur: Through ACT No. 17 of 2008 As Per UGC ACT 1956 NAAC Accredited UniversityDunichand chorenNo ratings yet

- Naga Neeraj Korada - ResumeDocument2 pagesNaga Neeraj Korada - ResumeHimungshu KashyapaNo ratings yet

- Chapter 3Document70 pagesChapter 3Ruben GeorgyantsNo ratings yet

- The Marketing PlanDocument23 pagesThe Marketing Planvincent gabriel cuyucaNo ratings yet

- Primary and Secondary MarketsDocument25 pagesPrimary and Secondary Marketssureh_mite_nitkyahoo50% (2)

- Venture Capital Method of Valuation2171 PDFDocument23 pagesVenture Capital Method of Valuation2171 PDFumaj25No ratings yet

- Advertising in b2bDocument22 pagesAdvertising in b2bAbhinav AggarwalNo ratings yet

- Difference Between Stock and Supply:-: Is WillingDocument13 pagesDifference Between Stock and Supply:-: Is WillingMustafa ShaikhNo ratings yet

- Engineering Economy NotebookDocument2 pagesEngineering Economy NotebookMadelo, Allysa Mae, M.No ratings yet

- Synopsis On A Study On DerivativesDocument5 pagesSynopsis On A Study On Derivativesarjunmba119624No ratings yet

- Week 5 Exercises 16 55Document4 pagesWeek 5 Exercises 16 55KNVS Siva KumarNo ratings yet

Download as docx, pdf, or txt

You might also like

- Chapter 7 Workout SheetDocument14 pagesChapter 7 Workout Sheetanh sy tranNo ratings yet

- Situational Leadership MANAGEMENTDocument2 pagesSituational Leadership MANAGEMENTHatem Hassan89% (9)

- SCDL - Marketing ManagementDocument20 pagesSCDL - Marketing Managementpradipta_moh100% (1)

- Fin 645 11906130 PDFDocument7 pagesFin 645 11906130 PDFPrateek SehgalNo ratings yet

- An Example of A Marketing PlanDocument8 pagesAn Example of A Marketing PlanJannie Aldrin SiahaanNo ratings yet

- Dividend Policy and Internal FinancingDocument14 pagesDividend Policy and Internal FinancingMichaela San Diego0% (1)

- Toby Crabel - Opening Range Breakout (Part1-8)Document39 pagesToby Crabel - Opening Range Breakout (Part1-8)saisonia75% (8)

- Different Option StrategiesDocument43 pagesDifferent Option StrategiessizzlingabheeNo ratings yet

- Bull Call Spread & Put SpreadDocument16 pagesBull Call Spread & Put Spreadravirana60No ratings yet

- Strategy Guide: Bull Call SpreadDocument14 pagesStrategy Guide: Bull Call SpreadworkNo ratings yet

- Ratio Back SpreadsDocument20 pagesRatio Back SpreadsOladipupo Mayowa PaulNo ratings yet

- Option Trading Strategies & Option SpreadsDocument30 pagesOption Trading Strategies & Option SpreadsPushkar GautamNo ratings yet

- Problem Set 3-Group 9Document6 pagesProblem Set 3-Group 9WristWork Entertainment100% (1)

- Margin TradingDocument11 pagesMargin TradingAvi RajNo ratings yet

- Hedging Risk With DerivativesDocument36 pagesHedging Risk With DerivativesSoumyadeep RoyNo ratings yet

- What Is The Maximum Loss or Profit With A Covered CallDocument3 pagesWhat Is The Maximum Loss or Profit With A Covered CallJonhmark AniñonNo ratings yet

- Put-Call Parity: By: Shruti Agrawal-201 Suhas Anjaria-202 Kankana Dutta-205 Aabhas Garg-207Document24 pagesPut-Call Parity: By: Shruti Agrawal-201 Suhas Anjaria-202 Kankana Dutta-205 Aabhas Garg-207Aabbhas GargNo ratings yet

- Derivatives Option StrategiesDocument45 pagesDerivatives Option Strategiesjim125No ratings yet

- Derivatives Talking PointsDocument4 pagesDerivatives Talking PointsAlice KujurNo ratings yet

- Derivatives Buy PutDocument10 pagesDerivatives Buy PutRajan kumar singhNo ratings yet

- Derivatives Buy PutDocument11 pagesDerivatives Buy PutRajan kumar singhNo ratings yet

- Butterfly + Broken Wing ButterflyDocument4 pagesButterfly + Broken Wing ButterflyMrityunjay Kumar100% (1)

- Option Strategy Builder Client PDFDocument13 pagesOption Strategy Builder Client PDFसन्तोष सिंह जादौनNo ratings yet

- 02 Market Mechanics 2Document16 pages02 Market Mechanics 2倪采萱No ratings yet

- Soln CH 20 Option IntroDocument14 pagesSoln CH 20 Option IntroSilviu TrebuianNo ratings yet

- Msc. Accounting and FinanceDocument18 pagesMsc. Accounting and FinancerytchluvNo ratings yet

- Butterfly Advanced Option Strategy AssignmentDocument3 pagesButterfly Advanced Option Strategy AssignmentHatem HassanNo ratings yet

- Study Report On Option Trading Strategies in Equity DerivativesDocument33 pagesStudy Report On Option Trading Strategies in Equity DerivativesDeepak Singh MauryaNo ratings yet

- Option StrategiesDocument33 pagesOption Strategiessurinder vermaNo ratings yet

- Jignesh Shah Dhiren Prajapati Kaustubh Parkar Akash Jadhav Deepali Jain Rahul GavaliDocument43 pagesJignesh Shah Dhiren Prajapati Kaustubh Parkar Akash Jadhav Deepali Jain Rahul GavaliDhiren Praj100% (1)

- HedgingDocument5 pagesHedgingGm EaswarNo ratings yet

- Video 12 - Bull Call Spread Strategy - UsefulDocument4 pagesVideo 12 - Bull Call Spread Strategy - Usefulshalomhanyane9No ratings yet

- Introduction To OptionsDocument9 pagesIntroduction To OptionsKumar NarayananNo ratings yet

- Intro To OptionsDocument9 pagesIntro To OptionsAntonio GenNo ratings yet

- Option and FutureDocument28 pagesOption and Futuresunil_das95No ratings yet

- Finance Questions and SolutionsDocument10 pagesFinance Questions and SolutionsEli Koech100% (1)

- Mai Thanh Hà - 22106200 - Portfolio Week 5 - Deri-T124WSB-3Document7 pagesMai Thanh Hà - 22106200 - Portfolio Week 5 - Deri-T124WSB-3Mai HàNo ratings yet

- Options CA - CS.CMA - MBA: Naveen. RohatgiDocument38 pagesOptions CA - CS.CMA - MBA: Naveen. RohatgiDivyaNo ratings yet

- Finance AssignmentDocument12 pagesFinance AssignmentYanni PoonNo ratings yet

- Options StrategiesDocument9 pagesOptions Strategiessneha496100% (1)

- 04 - 05 - Option Strategies & Payoff'sDocument66 pages04 - 05 - Option Strategies & Payoff'sMohammedAveshNagoriNo ratings yet

- Options Presentation123Document21 pagesOptions Presentation123KajalPahwaNo ratings yet

- Unit 6 Option CombinationsDocument13 pagesUnit 6 Option CombinationsFadil Ashrafi Barkati KhanNo ratings yet

- Options MSCFIÂ DECÂ 2022Document8 pagesOptions MSCFIÂ DECÂ 2022kenedy simwingaNo ratings yet

- Potm Video 3 Not-Useful Options Trading StrategiesDocument38 pagesPotm Video 3 Not-Useful Options Trading StrategiesIsIs DroneNo ratings yet

- Financial Risk Management ExercisesDocument20 pagesFinancial Risk Management ExercisesChau NguyenNo ratings yet

- Stock Option BasicsDocument62 pagesStock Option BasicsArvind DasNo ratings yet

- Long Call Condor - An Option Strategy: TH THDocument7 pagesLong Call Condor - An Option Strategy: TH THAasthaNo ratings yet

- Options Theory For Professional TradingDocument4 pagesOptions Theory For Professional TradingRaju.KonduruNo ratings yet

- Study Notes Trading StrategiesDocument16 pagesStudy Notes Trading Strategiesalok kundaliaNo ratings yet

- Chap3 Introduction To Options (Derivatives)Document30 pagesChap3 Introduction To Options (Derivatives)Jihen MejriNo ratings yet

- Derivatives - Options: Mahesh GujarDocument22 pagesDerivatives - Options: Mahesh GujarMahesh GujarNo ratings yet

- Ch11 An Introduction To Derivative SecuritiesDocument37 pagesCh11 An Introduction To Derivative SecuritiesMila AmandaNo ratings yet

- Options "The Rising Wave"Document30 pagesOptions "The Rising Wave"Neeal ParikhNo ratings yet

- Options & ModelsDocument48 pagesOptions & ModelsPraveen Kumar SinhaNo ratings yet

- Derivatives TrainingDocument83 pagesDerivatives TrainingvaibhavgdNo ratings yet

- Option Strategies PDFDocument5 pagesOption Strategies PDFdhanabal sNo ratings yet

- Put-Call Parity TheoremDocument4 pagesPut-Call Parity TheoremAmol SarafNo ratings yet

- Brokerage Transactions Stock MarketDocument17 pagesBrokerage Transactions Stock MarketMohsin SadaqatNo ratings yet

- Chapter 15 Exchange Traded Options Money and Capitals Market AFW1300/AFF1300Document5 pagesChapter 15 Exchange Traded Options Money and Capitals Market AFW1300/AFF1300Meng YeeNo ratings yet

- MGMT149 HW1Document5 pagesMGMT149 HW1Lin Lin KanokkornNo ratings yet

- Call OptionDocument1 pageCall OptionMustafa BhaiNo ratings yet

- Options Trading For Beginners: Tips, Formulas and Strategies For Traders to Make Money with OptionsFrom EverandOptions Trading For Beginners: Tips, Formulas and Strategies For Traders to Make Money with OptionsNo ratings yet

- OPTIONS TRADING: Mastering the Art of Options Trading for Financial Success (2023 Guide for Beginners)From EverandOPTIONS TRADING: Mastering the Art of Options Trading for Financial Success (2023 Guide for Beginners)No ratings yet

- Assignment 1 Chapter 8Document4 pagesAssignment 1 Chapter 8Hatem HassanNo ratings yet

- Credit Risk Management in BanksDocument31 pagesCredit Risk Management in BanksHatem HassanNo ratings yet

- Hatem Hassan Zakaria - Juhayna Co. Credit AnalysisDocument49 pagesHatem Hassan Zakaria - Juhayna Co. Credit AnalysisHatem Hassan100% (3)

- Assignment 1 Chapter 1Document9 pagesAssignment 1 Chapter 1Hatem HassanNo ratings yet

- Butterfly Advanced Option Strategy AssignmentDocument3 pagesButterfly Advanced Option Strategy AssignmentHatem HassanNo ratings yet

- Al Andalous PharmaceuticalsDocument17 pagesAl Andalous PharmaceuticalsHatem HassanNo ratings yet

- Thirlwall BOP EquilibriumDocument1 pageThirlwall BOP EquilibriumHatem HassanNo ratings yet

- Bop AnalysisDocument13 pagesBop AnalysisHatem HassanNo ratings yet

- Table: 19: Country:Eg Yp T B Al Ance of PaymentsDocument2 pagesTable: 19: Country:Eg Yp T B Al Ance of PaymentsHatem HassanNo ratings yet

- The Contexts of International BusinessDocument8 pagesThe Contexts of International BusinessHatem HassanNo ratings yet

- Sean Bing-Xuan NG Aqil 4057076 1945105348Document12 pagesSean Bing-Xuan NG Aqil 4057076 1945105348wong ming shengNo ratings yet

- IM 1 - Ronishka MaharjanDocument8 pagesIM 1 - Ronishka MaharjanRoni MaharjanNo ratings yet

- Vacera Investments Beverage Marketing PlanDocument2 pagesVacera Investments Beverage Marketing PlanOdoi DerekNo ratings yet

- Chapter 18 - Managing Marketing in The Global EconomyDocument48 pagesChapter 18 - Managing Marketing in The Global EconomyArman100% (2)

- Service Marketing MixDocument9 pagesService Marketing MixBashi Taizya100% (1)

- Anil PalaDocument4 pagesAnil Palageetha raniNo ratings yet

- Globalización? Análisis de Su Marketing-Mix Internacional: Mango: ¿Un Caso de Estrategia y Política deDocument15 pagesGlobalización? Análisis de Su Marketing-Mix Internacional: Mango: ¿Un Caso de Estrategia y Política demichxel psNo ratings yet

- Introduction To Economics - Class NotesDocument33 pagesIntroduction To Economics - Class NotesEliot PrimoNo ratings yet

- Cycle Agarbatti: Everyone Has A Reason To PrayDocument4 pagesCycle Agarbatti: Everyone Has A Reason To PrayRS10031986No ratings yet

- Mid Term RevisionDocument9 pagesMid Term RevisionRabie HarounNo ratings yet

- How To Prepare Economy? Exam Microeconomics Macroecono Mics Indian EconomyDocument8 pagesHow To Prepare Economy? Exam Microeconomics Macroecono Mics Indian EconomyAchuth GangadharanNo ratings yet

- Financial MarketDocument12 pagesFinancial Marketharshrajak822No ratings yet

- Reflection Paper On EconomicsDocument15 pagesReflection Paper On EconomicsRexan Dagreat Casas67% (3)

- 0205 ReposedDocument45 pages0205 ReposedLameuneNo ratings yet

- Full Analysis of Candlestick PatternsDocument67 pagesFull Analysis of Candlestick PatternsIm CupidNo ratings yet

- Jayoti Vidyapeeth Women'S University, Jaipur: Through ACT No. 17 of 2008 As Per UGC ACT 1956 NAAC Accredited UniversityDocument9 pagesJayoti Vidyapeeth Women'S University, Jaipur: Through ACT No. 17 of 2008 As Per UGC ACT 1956 NAAC Accredited UniversityDunichand chorenNo ratings yet

- Naga Neeraj Korada - ResumeDocument2 pagesNaga Neeraj Korada - ResumeHimungshu KashyapaNo ratings yet

- Chapter 3Document70 pagesChapter 3Ruben GeorgyantsNo ratings yet

- The Marketing PlanDocument23 pagesThe Marketing Planvincent gabriel cuyucaNo ratings yet

- Primary and Secondary MarketsDocument25 pagesPrimary and Secondary Marketssureh_mite_nitkyahoo50% (2)

- Venture Capital Method of Valuation2171 PDFDocument23 pagesVenture Capital Method of Valuation2171 PDFumaj25No ratings yet

- Advertising in b2bDocument22 pagesAdvertising in b2bAbhinav AggarwalNo ratings yet

- Difference Between Stock and Supply:-: Is WillingDocument13 pagesDifference Between Stock and Supply:-: Is WillingMustafa ShaikhNo ratings yet

- Engineering Economy NotebookDocument2 pagesEngineering Economy NotebookMadelo, Allysa Mae, M.No ratings yet

- Synopsis On A Study On DerivativesDocument5 pagesSynopsis On A Study On Derivativesarjunmba119624No ratings yet

- Week 5 Exercises 16 55Document4 pagesWeek 5 Exercises 16 55KNVS Siva KumarNo ratings yet