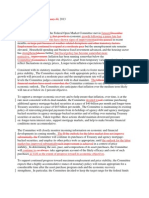

December 17, 2014 Compared With October 29, 2014 Jeremie Cohen-Setton

December 17, 2014 Compared With October 29, 2014 Jeremie Cohen-Setton

You might also like

- NIBM - Risk MGMTDocument5 pagesNIBM - Risk MGMTNB SouthNo ratings yet

- MBS Basics: Nomura Fixed Income ResearchDocument31 pagesMBS Basics: Nomura Fixed Income ResearchanuragNo ratings yet

- Cryptocurrency Scams 2022 V8Document18 pagesCryptocurrency Scams 2022 V8CBS 11 News100% (4)

- FOMC Redline MarchDocument2 pagesFOMC Redline MarchZerohedgeNo ratings yet

- Fed TalkDocument2 pagesFed TalkTelegraphUKNo ratings yet

- Fomc StatmentDocument1 pageFomc Statmentapi-280585983No ratings yet

- Oct FOMC RedlineDocument2 pagesOct FOMC RedlineZerohedgeNo ratings yet

- FOMC Word For Word Changes. 05.01.13Document2 pagesFOMC Word For Word Changes. 05.01.13Pensford FinancialNo ratings yet

- Fed SideDocument1 pageFed Sideannawitkowski88No ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEandrewbloggerNo ratings yet

- FOMC Word For Word Changes 03.20.13Document2 pagesFOMC Word For Word Changes 03.20.13Pensford FinancialNo ratings yet

- Fed Side by Side 20120125Document3 pagesFed Side by Side 20120125andrewbloggerNo ratings yet

- FOMC Rate Decision 04.25.12Document1 pageFOMC Rate Decision 04.25.12Pensford FinancialNo ratings yet

- FOMC Side by Side 11022011Document2 pagesFOMC Side by Side 11022011andrewbloggerNo ratings yet

- Press Release: For Release at 2:00 P.M. EDTDocument2 pagesPress Release: For Release at 2:00 P.M. EDTTREND_7425No ratings yet

- Fed 09212011Document2 pagesFed 09212011andrewbloggerNo ratings yet

- 2010-09-21 - Fed Side by Side StatementsDocument2 pages2010-09-21 - Fed Side by Side Statementsglerner133926No ratings yet

- Fomc Pres Conf 20141217Document23 pagesFomc Pres Conf 20141217JoseLastNo ratings yet

- SidebysidefedDocument1 pageSidebysidefedandrewbloggerNo ratings yet

- January - March FOMC Statement ComparisonDocument1 pageJanuary - March FOMC Statement Comparisonshawn2207No ratings yet

- FOMC RedLineDocument2 pagesFOMC RedLineEduardo VinanteNo ratings yet

- Sidebyside 08092011Document1 pageSidebyside 08092011andrewbloggerNo ratings yet

- Fed Statements Side by SideDocument1 pageFed Statements Side by SideTaylor CottamNo ratings yet

- Yellen TestimonyDocument7 pagesYellen TestimonyZerohedgeNo ratings yet

- Federal Reserve Issues FOMC Statement: ShareDocument2 pagesFederal Reserve Issues FOMC Statement: ShareTREND_7425No ratings yet

- SystemDocument8 pagesSystempathanfor786No ratings yet

- FOMC0810Document2 pagesFOMC0810arborjimbNo ratings yet

- US Fed FOMC Press Conference 18 September 2013 No TaperDocument26 pagesUS Fed FOMC Press Conference 18 September 2013 No TaperJhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- 2018.01.31 FED Press ReleaseDocument2 pages2018.01.31 FED Press ReleaseTREND_7425No ratings yet

- Fomc Septiembre 2015Document2 pagesFomc Septiembre 2015cocoNo ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEarborjimbNo ratings yet

- Fomc Pres Conf 20240501Document4 pagesFomc Pres Conf 20240501gustavo.kahilNo ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEarborjimbNo ratings yet

- FOMCstatementDocument2 pagesFOMCstatementCBNo ratings yet

- Transcript of Chairman Bernanke's Press Conference April 25, 2012Document23 pagesTranscript of Chairman Bernanke's Press Conference April 25, 2012CoolidgeLowNo ratings yet

- Transcript of Chair Powell's Press Conference Opening Statement March 20, 2024Document4 pagesTranscript of Chair Powell's Press Conference Opening Statement March 20, 2024andre.torresNo ratings yet

- FedDocument4 pagesFedandre.torresNo ratings yet

- Federal Reserve Issues FOMC Statement: ShareDocument1 pageFederal Reserve Issues FOMC Statement: ShareTREND_7425No ratings yet

- Fomc Pres Conf 20231101Document26 pagesFomc Pres Conf 20231101Quynh Le Thi NhuNo ratings yet

- Fomc Pres Conf 20130918Document7 pagesFomc Pres Conf 20130918helmuthNo ratings yet

- Monetary 20240501 A 1Document4 pagesMonetary 20240501 A 1gustavo.kahilNo ratings yet

- FOMCpresconf 20230920Document4 pagesFOMCpresconf 20230920KHAIRULNo ratings yet

- Fed Statement June 2009Document2 pagesFed Statement June 2009andrewbloggerNo ratings yet

- FOMCpresconf 20210922Document26 pagesFOMCpresconf 20210922marcoNo ratings yet

- PowellDocument4 pagesPowellandre.torresNo ratings yet

- Comptabilité Tle G3 Et G2Document24 pagesComptabilité Tle G3 Et G2albertvalk2.0No ratings yet

- 2018.09.26 FED Press ReleaseDocument1 page2018.09.26 FED Press ReleaseTREND_7425No ratings yet

- Fed Redline FebruaryDocument2 pagesFed Redline FebruaryPradeep SolankiNo ratings yet

- Yellen HHDocument7 pagesYellen HHZerohedgeNo ratings yet

- Press ReleaseDocument2 pagesPress Releaseapi-26018528No ratings yet

- Conférence de Presse BCE JanvierDocument2 pagesConférence de Presse BCE JanvierToroloNo ratings yet

- FOMCpresconf20240501Document26 pagesFOMCpresconf20240501David SimõesNo ratings yet

- Monetary 20230614 A 1Document4 pagesMonetary 20230614 A 1Jhony SmithYTNo ratings yet

- FOMCpresconf 20230503Document25 pagesFOMCpresconf 20230503Edi SaputraNo ratings yet

- Fomc Statements - Side-By-sideDocument2 pagesFomc Statements - Side-By-sideurbanovNo ratings yet

- Fomc Pres Conf 20230614Document26 pagesFomc Pres Conf 20230614LAKHAN TRIVEDINo ratings yet

- FOMCpresconf 20230614Document5 pagesFOMCpresconf 20230614Jhony SmithYTNo ratings yet

- resconfDocument4 pagesresconfgothurded24No ratings yet

- Monetary 20230201 A 1Document4 pagesMonetary 20230201 A 1tamhid nahianNo ratings yet

- Federal Reserve: Unconventional Monetary Policy Options: Marc LabonteDocument37 pagesFederal Reserve: Unconventional Monetary Policy Options: Marc Labonterichardck61No ratings yet

- Monetary Policy Summary: Publication Date: 3 August 2017Document3 pagesMonetary Policy Summary: Publication Date: 3 August 2017TraderNo ratings yet

- Jerome Powell's Written TestimonyDocument5 pagesJerome Powell's Written TestimonyTim MooreNo ratings yet

- Summer Training ReportDocument76 pagesSummer Training ReportRibhanshu RajNo ratings yet

- Intro To Mathematical Finance Part I: Lecture 1: 1.1: The One-Period Binomial ModelDocument21 pagesIntro To Mathematical Finance Part I: Lecture 1: 1.1: The One-Period Binomial ModelSoham KumarNo ratings yet

- Bonds PayableDocument52 pagesBonds PayableJohn Charles Andaya100% (2)

- Account Statement 4000Document1 pageAccount Statement 4000ebmk oeibNo ratings yet

- Cmd. 00427991823303 Cmd. 00427991823303 Cmd. 00427991823303 Cmd. 00427991823303Document1 pageCmd. 00427991823303 Cmd. 00427991823303 Cmd. 00427991823303 Cmd. 00427991823303irfanNo ratings yet

- Wichita Old Town Warren Theatre LLC Term LoanDocument2 pagesWichita Old Town Warren Theatre LLC Term LoanBob WeeksNo ratings yet

- What Is International TradeDocument2 pagesWhat Is International Tradeeknath2000No ratings yet

- BRMDocument69 pagesBRMpatesweetu1No ratings yet

- Scam 1992 - A Web Series On Harshad Mehta ScamDocument2 pagesScam 1992 - A Web Series On Harshad Mehta ScamAavish GuptaNo ratings yet

- Negotiable Instrument (Discharge of Instrument)Document15 pagesNegotiable Instrument (Discharge of Instrument)Sara Andrea Santiago100% (1)

- Telus 40042789 2023 03 25Document10 pagesTelus 40042789 2023 03 25Harold KumarNo ratings yet

- Soa300822Document1 pageSoa300822Sandy SavitraNo ratings yet

- Understanding Investment - Class 6 PDFDocument4 pagesUnderstanding Investment - Class 6 PDFDebabrattaNo ratings yet

- Cash and CequizDocument5 pagesCash and CequizMaria Emarla Grace CanozaNo ratings yet

- Rip-Off by The Federal Reserve (Revised)Document13 pagesRip-Off by The Federal Reserve (Revised)Oldereb100% (2)

- Financial InstrumentsDocument93 pagesFinancial InstrumentsLuisa Janelle BoquirenNo ratings yet

- BUDGET AT A GLANCE Full PDFDocument440 pagesBUDGET AT A GLANCE Full PDFTamilnadu KaatumanarkovilNo ratings yet

- Account Statement As of 05-06-2020 12:14:26 GMT +0530Document9 pagesAccount Statement As of 05-06-2020 12:14:26 GMT +0530Arun VeeraniNo ratings yet

- Discounted Cash Flow Valuation PDFDocument130 pagesDiscounted Cash Flow Valuation PDFayca_No ratings yet

- Sap Fi/Co: Transaction CodesDocument51 pagesSap Fi/Co: Transaction CodesReddaveni NagarajuNo ratings yet

- 158 634353431366610342 New Test 2Document14 pages158 634353431366610342 New Test 2Mara Shaira SiegaNo ratings yet

- Basic Finance Prelim Q1Document5 pagesBasic Finance Prelim Q1Michelle EsperalNo ratings yet

- NGN ArbitrageDocument4 pagesNGN Arbitragewraje01No ratings yet

- Cottco H1 2016 ResultsDocument2 pagesCottco H1 2016 ResultsaddyNo ratings yet

- Character, Ability, Margin, Purpose, Amount, Repayment, Insurance/Security or FiveDocument7 pagesCharacter, Ability, Margin, Purpose, Amount, Repayment, Insurance/Security or FiveRuohui ChenNo ratings yet

- PGBP NotesDocument24 pagesPGBP NotesYogesh Aggarwal100% (2)

- Americandownload b2 Extra Tasks and KeyDocument12 pagesAmericandownload b2 Extra Tasks and Keyangelos1apostolidisNo ratings yet

Download as docx, pdf, or txt

You might also like

- NIBM - Risk MGMTDocument5 pagesNIBM - Risk MGMTNB SouthNo ratings yet

- MBS Basics: Nomura Fixed Income ResearchDocument31 pagesMBS Basics: Nomura Fixed Income ResearchanuragNo ratings yet

- Cryptocurrency Scams 2022 V8Document18 pagesCryptocurrency Scams 2022 V8CBS 11 News100% (4)

- FOMC Redline MarchDocument2 pagesFOMC Redline MarchZerohedgeNo ratings yet

- Fed TalkDocument2 pagesFed TalkTelegraphUKNo ratings yet

- Fomc StatmentDocument1 pageFomc Statmentapi-280585983No ratings yet

- Oct FOMC RedlineDocument2 pagesOct FOMC RedlineZerohedgeNo ratings yet

- FOMC Word For Word Changes. 05.01.13Document2 pagesFOMC Word For Word Changes. 05.01.13Pensford FinancialNo ratings yet

- Fed SideDocument1 pageFed Sideannawitkowski88No ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEandrewbloggerNo ratings yet

- FOMC Word For Word Changes 03.20.13Document2 pagesFOMC Word For Word Changes 03.20.13Pensford FinancialNo ratings yet

- Fed Side by Side 20120125Document3 pagesFed Side by Side 20120125andrewbloggerNo ratings yet

- FOMC Rate Decision 04.25.12Document1 pageFOMC Rate Decision 04.25.12Pensford FinancialNo ratings yet

- FOMC Side by Side 11022011Document2 pagesFOMC Side by Side 11022011andrewbloggerNo ratings yet

- Press Release: For Release at 2:00 P.M. EDTDocument2 pagesPress Release: For Release at 2:00 P.M. EDTTREND_7425No ratings yet

- Fed 09212011Document2 pagesFed 09212011andrewbloggerNo ratings yet

- 2010-09-21 - Fed Side by Side StatementsDocument2 pages2010-09-21 - Fed Side by Side Statementsglerner133926No ratings yet

- Fomc Pres Conf 20141217Document23 pagesFomc Pres Conf 20141217JoseLastNo ratings yet

- SidebysidefedDocument1 pageSidebysidefedandrewbloggerNo ratings yet

- January - March FOMC Statement ComparisonDocument1 pageJanuary - March FOMC Statement Comparisonshawn2207No ratings yet

- FOMC RedLineDocument2 pagesFOMC RedLineEduardo VinanteNo ratings yet

- Sidebyside 08092011Document1 pageSidebyside 08092011andrewbloggerNo ratings yet

- Fed Statements Side by SideDocument1 pageFed Statements Side by SideTaylor CottamNo ratings yet

- Yellen TestimonyDocument7 pagesYellen TestimonyZerohedgeNo ratings yet

- Federal Reserve Issues FOMC Statement: ShareDocument2 pagesFederal Reserve Issues FOMC Statement: ShareTREND_7425No ratings yet

- SystemDocument8 pagesSystempathanfor786No ratings yet

- FOMC0810Document2 pagesFOMC0810arborjimbNo ratings yet

- US Fed FOMC Press Conference 18 September 2013 No TaperDocument26 pagesUS Fed FOMC Press Conference 18 September 2013 No TaperJhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- 2018.01.31 FED Press ReleaseDocument2 pages2018.01.31 FED Press ReleaseTREND_7425No ratings yet

- Fomc Septiembre 2015Document2 pagesFomc Septiembre 2015cocoNo ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEarborjimbNo ratings yet

- Fomc Pres Conf 20240501Document4 pagesFomc Pres Conf 20240501gustavo.kahilNo ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEarborjimbNo ratings yet

- FOMCstatementDocument2 pagesFOMCstatementCBNo ratings yet

- Transcript of Chairman Bernanke's Press Conference April 25, 2012Document23 pagesTranscript of Chairman Bernanke's Press Conference April 25, 2012CoolidgeLowNo ratings yet

- Transcript of Chair Powell's Press Conference Opening Statement March 20, 2024Document4 pagesTranscript of Chair Powell's Press Conference Opening Statement March 20, 2024andre.torresNo ratings yet

- FedDocument4 pagesFedandre.torresNo ratings yet

- Federal Reserve Issues FOMC Statement: ShareDocument1 pageFederal Reserve Issues FOMC Statement: ShareTREND_7425No ratings yet

- Fomc Pres Conf 20231101Document26 pagesFomc Pres Conf 20231101Quynh Le Thi NhuNo ratings yet

- Fomc Pres Conf 20130918Document7 pagesFomc Pres Conf 20130918helmuthNo ratings yet

- Monetary 20240501 A 1Document4 pagesMonetary 20240501 A 1gustavo.kahilNo ratings yet

- FOMCpresconf 20230920Document4 pagesFOMCpresconf 20230920KHAIRULNo ratings yet

- Fed Statement June 2009Document2 pagesFed Statement June 2009andrewbloggerNo ratings yet

- FOMCpresconf 20210922Document26 pagesFOMCpresconf 20210922marcoNo ratings yet

- PowellDocument4 pagesPowellandre.torresNo ratings yet

- Comptabilité Tle G3 Et G2Document24 pagesComptabilité Tle G3 Et G2albertvalk2.0No ratings yet

- 2018.09.26 FED Press ReleaseDocument1 page2018.09.26 FED Press ReleaseTREND_7425No ratings yet

- Fed Redline FebruaryDocument2 pagesFed Redline FebruaryPradeep SolankiNo ratings yet

- Yellen HHDocument7 pagesYellen HHZerohedgeNo ratings yet

- Press ReleaseDocument2 pagesPress Releaseapi-26018528No ratings yet

- Conférence de Presse BCE JanvierDocument2 pagesConférence de Presse BCE JanvierToroloNo ratings yet

- FOMCpresconf20240501Document26 pagesFOMCpresconf20240501David SimõesNo ratings yet

- Monetary 20230614 A 1Document4 pagesMonetary 20230614 A 1Jhony SmithYTNo ratings yet

- FOMCpresconf 20230503Document25 pagesFOMCpresconf 20230503Edi SaputraNo ratings yet

- Fomc Statements - Side-By-sideDocument2 pagesFomc Statements - Side-By-sideurbanovNo ratings yet

- Fomc Pres Conf 20230614Document26 pagesFomc Pres Conf 20230614LAKHAN TRIVEDINo ratings yet

- FOMCpresconf 20230614Document5 pagesFOMCpresconf 20230614Jhony SmithYTNo ratings yet

- resconfDocument4 pagesresconfgothurded24No ratings yet

- Monetary 20230201 A 1Document4 pagesMonetary 20230201 A 1tamhid nahianNo ratings yet

- Federal Reserve: Unconventional Monetary Policy Options: Marc LabonteDocument37 pagesFederal Reserve: Unconventional Monetary Policy Options: Marc Labonterichardck61No ratings yet

- Monetary Policy Summary: Publication Date: 3 August 2017Document3 pagesMonetary Policy Summary: Publication Date: 3 August 2017TraderNo ratings yet

- Jerome Powell's Written TestimonyDocument5 pagesJerome Powell's Written TestimonyTim MooreNo ratings yet

- Summer Training ReportDocument76 pagesSummer Training ReportRibhanshu RajNo ratings yet

- Intro To Mathematical Finance Part I: Lecture 1: 1.1: The One-Period Binomial ModelDocument21 pagesIntro To Mathematical Finance Part I: Lecture 1: 1.1: The One-Period Binomial ModelSoham KumarNo ratings yet

- Bonds PayableDocument52 pagesBonds PayableJohn Charles Andaya100% (2)

- Account Statement 4000Document1 pageAccount Statement 4000ebmk oeibNo ratings yet

- Cmd. 00427991823303 Cmd. 00427991823303 Cmd. 00427991823303 Cmd. 00427991823303Document1 pageCmd. 00427991823303 Cmd. 00427991823303 Cmd. 00427991823303 Cmd. 00427991823303irfanNo ratings yet

- Wichita Old Town Warren Theatre LLC Term LoanDocument2 pagesWichita Old Town Warren Theatre LLC Term LoanBob WeeksNo ratings yet

- What Is International TradeDocument2 pagesWhat Is International Tradeeknath2000No ratings yet

- BRMDocument69 pagesBRMpatesweetu1No ratings yet

- Scam 1992 - A Web Series On Harshad Mehta ScamDocument2 pagesScam 1992 - A Web Series On Harshad Mehta ScamAavish GuptaNo ratings yet

- Negotiable Instrument (Discharge of Instrument)Document15 pagesNegotiable Instrument (Discharge of Instrument)Sara Andrea Santiago100% (1)

- Telus 40042789 2023 03 25Document10 pagesTelus 40042789 2023 03 25Harold KumarNo ratings yet

- Soa300822Document1 pageSoa300822Sandy SavitraNo ratings yet

- Understanding Investment - Class 6 PDFDocument4 pagesUnderstanding Investment - Class 6 PDFDebabrattaNo ratings yet

- Cash and CequizDocument5 pagesCash and CequizMaria Emarla Grace CanozaNo ratings yet

- Rip-Off by The Federal Reserve (Revised)Document13 pagesRip-Off by The Federal Reserve (Revised)Oldereb100% (2)

- Financial InstrumentsDocument93 pagesFinancial InstrumentsLuisa Janelle BoquirenNo ratings yet

- BUDGET AT A GLANCE Full PDFDocument440 pagesBUDGET AT A GLANCE Full PDFTamilnadu KaatumanarkovilNo ratings yet

- Account Statement As of 05-06-2020 12:14:26 GMT +0530Document9 pagesAccount Statement As of 05-06-2020 12:14:26 GMT +0530Arun VeeraniNo ratings yet

- Discounted Cash Flow Valuation PDFDocument130 pagesDiscounted Cash Flow Valuation PDFayca_No ratings yet

- Sap Fi/Co: Transaction CodesDocument51 pagesSap Fi/Co: Transaction CodesReddaveni NagarajuNo ratings yet

- 158 634353431366610342 New Test 2Document14 pages158 634353431366610342 New Test 2Mara Shaira SiegaNo ratings yet

- Basic Finance Prelim Q1Document5 pagesBasic Finance Prelim Q1Michelle EsperalNo ratings yet

- NGN ArbitrageDocument4 pagesNGN Arbitragewraje01No ratings yet

- Cottco H1 2016 ResultsDocument2 pagesCottco H1 2016 ResultsaddyNo ratings yet

- Character, Ability, Margin, Purpose, Amount, Repayment, Insurance/Security or FiveDocument7 pagesCharacter, Ability, Margin, Purpose, Amount, Repayment, Insurance/Security or FiveRuohui ChenNo ratings yet

- PGBP NotesDocument24 pagesPGBP NotesYogesh Aggarwal100% (2)

- Americandownload b2 Extra Tasks and KeyDocument12 pagesAmericandownload b2 Extra Tasks and Keyangelos1apostolidisNo ratings yet