Distributive Justice in Firms

Distributive Justice in Firms

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- World Politics Interests Interactions Institutions 3rd Edition Frieden Test BankDocument16 pagesWorld Politics Interests Interactions Institutions 3rd Edition Frieden Test Bankthuygladys5x0100% (21)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Price Action Trading StrategyDocument8 pagesPrice Action Trading Strategyamirhosein tohidli100% (7)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- SubsidiesDocument50 pagesSubsidiesAkash SidharthNo ratings yet

- Learn Swing TradingDocument38 pagesLearn Swing TradingKamal Baitha100% (2)

- Variance Analysis WorksheetDocument8 pagesVariance Analysis WorksheetLeigh018No ratings yet

- ECO211 Chapter 4Document158 pagesECO211 Chapter 4Adam ZafryNo ratings yet

- APT 3083 Week 01 WickhamDocument59 pagesAPT 3083 Week 01 WickhamDeslin Phang100% (1)

- The Correlation Between Game Theory and International Trade PDFDocument8 pagesThe Correlation Between Game Theory and International Trade PDFAriel MontNo ratings yet

- Eco. Difficult MCQs 03 To 09Document24 pagesEco. Difficult MCQs 03 To 09iYaasir100% (2)

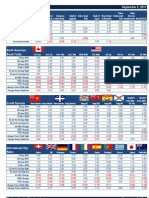

- Markets For The Week Ending September 2, 2011: Monetary PolicyDocument8 pagesMarkets For The Week Ending September 2, 2011: Monetary PolicymwarywodaNo ratings yet

- Discounted Cash Flow Model: Leesb@hanyang - Ac.krDocument2 pagesDiscounted Cash Flow Model: Leesb@hanyang - Ac.krw_fibNo ratings yet

- Revolutionary DemocracyDocument35 pagesRevolutionary Democracymatts292003574100% (2)

- International Exchange Rate Systems: EC10008, Modern World EconomyDocument26 pagesInternational Exchange Rate Systems: EC10008, Modern World EconomysimbsiNo ratings yet

- Balance of Payments - Mba Law.2023Document70 pagesBalance of Payments - Mba Law.2023Sachin KandloorNo ratings yet

- Conway, D. Consequences of Migration and Remittances For Mexican Transnational CommunitiesDocument20 pagesConway, D. Consequences of Migration and Remittances For Mexican Transnational CommunitiesMario MacíasNo ratings yet

- Managerial Aptitud Assignment2Document4 pagesManagerial Aptitud Assignment2najla fedawiNo ratings yet

- Chapter 1 - Economy and His Domain (Paper Format PDFDocument34 pagesChapter 1 - Economy and His Domain (Paper Format PDFseradjsamah37No ratings yet

- Sources and Destination of FDI & FIIDocument12 pagesSources and Destination of FDI & FIIAnith LukNo ratings yet

- PGP Retirement Planning UnlockedDocument9 pagesPGP Retirement Planning UnlockedBharathi 3280No ratings yet

- Edgeworth Box Diagram: An IntroductionDocument11 pagesEdgeworth Box Diagram: An IntroductionAbigail V100% (1)

- MMBDocument81 pagesMMBfakebakNo ratings yet

- Notes VarianceDocument37 pagesNotes Variancezms240No ratings yet

- ECONOMICS Question Paper Kerala Plus Two Second Term Half Yearly Christmas Exam Dec 2019Document8 pagesECONOMICS Question Paper Kerala Plus Two Second Term Half Yearly Christmas Exam Dec 2019ananya anuNo ratings yet

- Test Bank For Launching New Ventures An Entrepreneurial Approach 6th Edition AllenDocument9 pagesTest Bank For Launching New Ventures An Entrepreneurial Approach 6th Edition AllenTammy Wright100% (30)

- 4 Term Structure Theory of Interest RateDocument2 pages4 Term Structure Theory of Interest RateHusnul IradatiNo ratings yet

- Pakistan - Enigma of Taxation (Chapter VIII)Document6 pagesPakistan - Enigma of Taxation (Chapter VIII)Zaid NaveedNo ratings yet

- Bba 302Document8 pagesBba 302rohanNo ratings yet

- KQ Booklet PDFDocument36 pagesKQ Booklet PDFAshita Naik100% (1)

- Format of Final Report Marketing ManagementDocument2 pagesFormat of Final Report Marketing ManagementAmanullah AfzalNo ratings yet

- Environment UncertaintyDocument7 pagesEnvironment UncertaintyNailaAns0% (1)

Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- World Politics Interests Interactions Institutions 3rd Edition Frieden Test BankDocument16 pagesWorld Politics Interests Interactions Institutions 3rd Edition Frieden Test Bankthuygladys5x0100% (21)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Price Action Trading StrategyDocument8 pagesPrice Action Trading Strategyamirhosein tohidli100% (7)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- SubsidiesDocument50 pagesSubsidiesAkash SidharthNo ratings yet

- Learn Swing TradingDocument38 pagesLearn Swing TradingKamal Baitha100% (2)

- Variance Analysis WorksheetDocument8 pagesVariance Analysis WorksheetLeigh018No ratings yet

- ECO211 Chapter 4Document158 pagesECO211 Chapter 4Adam ZafryNo ratings yet

- APT 3083 Week 01 WickhamDocument59 pagesAPT 3083 Week 01 WickhamDeslin Phang100% (1)

- The Correlation Between Game Theory and International Trade PDFDocument8 pagesThe Correlation Between Game Theory and International Trade PDFAriel MontNo ratings yet

- Eco. Difficult MCQs 03 To 09Document24 pagesEco. Difficult MCQs 03 To 09iYaasir100% (2)

- Markets For The Week Ending September 2, 2011: Monetary PolicyDocument8 pagesMarkets For The Week Ending September 2, 2011: Monetary PolicymwarywodaNo ratings yet

- Discounted Cash Flow Model: Leesb@hanyang - Ac.krDocument2 pagesDiscounted Cash Flow Model: Leesb@hanyang - Ac.krw_fibNo ratings yet

- Revolutionary DemocracyDocument35 pagesRevolutionary Democracymatts292003574100% (2)

- International Exchange Rate Systems: EC10008, Modern World EconomyDocument26 pagesInternational Exchange Rate Systems: EC10008, Modern World EconomysimbsiNo ratings yet

- Balance of Payments - Mba Law.2023Document70 pagesBalance of Payments - Mba Law.2023Sachin KandloorNo ratings yet

- Conway, D. Consequences of Migration and Remittances For Mexican Transnational CommunitiesDocument20 pagesConway, D. Consequences of Migration and Remittances For Mexican Transnational CommunitiesMario MacíasNo ratings yet

- Managerial Aptitud Assignment2Document4 pagesManagerial Aptitud Assignment2najla fedawiNo ratings yet

- Chapter 1 - Economy and His Domain (Paper Format PDFDocument34 pagesChapter 1 - Economy and His Domain (Paper Format PDFseradjsamah37No ratings yet

- Sources and Destination of FDI & FIIDocument12 pagesSources and Destination of FDI & FIIAnith LukNo ratings yet

- PGP Retirement Planning UnlockedDocument9 pagesPGP Retirement Planning UnlockedBharathi 3280No ratings yet

- Edgeworth Box Diagram: An IntroductionDocument11 pagesEdgeworth Box Diagram: An IntroductionAbigail V100% (1)

- MMBDocument81 pagesMMBfakebakNo ratings yet

- Notes VarianceDocument37 pagesNotes Variancezms240No ratings yet

- ECONOMICS Question Paper Kerala Plus Two Second Term Half Yearly Christmas Exam Dec 2019Document8 pagesECONOMICS Question Paper Kerala Plus Two Second Term Half Yearly Christmas Exam Dec 2019ananya anuNo ratings yet

- Test Bank For Launching New Ventures An Entrepreneurial Approach 6th Edition AllenDocument9 pagesTest Bank For Launching New Ventures An Entrepreneurial Approach 6th Edition AllenTammy Wright100% (30)

- 4 Term Structure Theory of Interest RateDocument2 pages4 Term Structure Theory of Interest RateHusnul IradatiNo ratings yet

- Pakistan - Enigma of Taxation (Chapter VIII)Document6 pagesPakistan - Enigma of Taxation (Chapter VIII)Zaid NaveedNo ratings yet

- Bba 302Document8 pagesBba 302rohanNo ratings yet

- KQ Booklet PDFDocument36 pagesKQ Booklet PDFAshita Naik100% (1)

- Format of Final Report Marketing ManagementDocument2 pagesFormat of Final Report Marketing ManagementAmanullah AfzalNo ratings yet

- Environment UncertaintyDocument7 pagesEnvironment UncertaintyNailaAns0% (1)