Download as doc, pdf, or txt

You might also like

- MAS - Agamata Chapter 3 Answer KeyDocument5 pagesMAS - Agamata Chapter 3 Answer Keymagoimoi100% (3)

- Project Report On Sanitary Napkin Manufacturing Unit (Biodegradable) Cap: 12 Lac No / Day (Miscellaneous Products)Document10 pagesProject Report On Sanitary Napkin Manufacturing Unit (Biodegradable) Cap: 12 Lac No / Day (Miscellaneous Products)Sachin SharmaNo ratings yet

- Seagate QuestionsDocument2 pagesSeagate QuestionsCoolminded Coolminded50% (2)

- Level 3 Costing & MA Text Update June 2021pdfDocument125 pagesLevel 3 Costing & MA Text Update June 2021pdfAmi KayNo ratings yet

- MECN430 Homework 3 Winter 2020 - RCGDocument5 pagesMECN430 Homework 3 Winter 2020 - RCGRamon GondimNo ratings yet

- GRC FinMan Capital Budgeting ModuleDocument10 pagesGRC FinMan Capital Budgeting ModuleJasmine FiguraNo ratings yet

- Basic Capital BudgetingDocument42 pagesBasic Capital BudgetingMay Abia100% (2)

- BUAD 839 ASSIGNMENT (Group F)Document4 pagesBUAD 839 ASSIGNMENT (Group F)Yemi Jonathan OlusholaNo ratings yet

- Tata Corus Deal-Where Did They Go Wrong?: Case StudyDocument10 pagesTata Corus Deal-Where Did They Go Wrong?: Case StudyMalika BajpaiNo ratings yet

- Business and Investment Opportunities For BambooDocument37 pagesBusiness and Investment Opportunities For Bamboolenvf100% (2)

- Capital Budgeting: Financial ManagementDocument22 pagesCapital Budgeting: Financial ManagementKaRin MerRoNo ratings yet

- Unit 2 Capital Budgeting Technique ProblemsDocument39 pagesUnit 2 Capital Budgeting Technique ProblemsAshok Kumar100% (1)

- Presentation Capital Budgeting 1464200210 160310Document37 pagesPresentation Capital Budgeting 1464200210 160310Esha ThawalNo ratings yet

- Chapter 6Document52 pagesChapter 6Bhi-ehm GajusanNo ratings yet

- Fcma, Fpa, Ma (Economics), BSC Dubai, United Arab Emirates: Presentation byDocument42 pagesFcma, Fpa, Ma (Economics), BSC Dubai, United Arab Emirates: Presentation byAhmad Tariq Bhatti100% (1)

- 5, 6 & 7 Capital BudgetingDocument42 pages5, 6 & 7 Capital BudgetingNaman AgarwalNo ratings yet

- Profitability Alternative Investment and ReplacementDocument24 pagesProfitability Alternative Investment and ReplacementSakthi S100% (1)

- Summary of Capital Budgeting Techniques GitmanDocument12 pagesSummary of Capital Budgeting Techniques GitmanHarold Dela FuenteNo ratings yet

- Feasibility StudyDocument8 pagesFeasibility StudymuhaNo ratings yet

- 6 - Basic Methods For Making Economy StudiesDocument25 pages6 - Basic Methods For Making Economy StudiesChu KathNo ratings yet

- Corporate Finance (Lecture-3)Document72 pagesCorporate Finance (Lecture-3)meahearun nesa mouNo ratings yet

- MODULE 8 Capital BudgetingDocument9 pagesMODULE 8 Capital BudgetingLumingNo ratings yet

- 254 Chapter 10Document23 pages254 Chapter 10Zidan ZaifNo ratings yet

- Project Appraisal - Investment Appraisal - 2023Document40 pagesProject Appraisal - Investment Appraisal - 2023ThaboNo ratings yet

- L1R32 Annotated CalculatorDocument33 pagesL1R32 Annotated CalculatorAlex PaulNo ratings yet

- Capital Budgeting Lesson NewDocument44 pagesCapital Budgeting Lesson NewLea MachadoNo ratings yet

- Net Present Value MethodDocument9 pagesNet Present Value MethodRain Roslan100% (2)

- Concept of Capital Budgeting: Capital Budgeting Is A Process of Planning That Is Used To AscertainDocument11 pagesConcept of Capital Budgeting: Capital Budgeting Is A Process of Planning That Is Used To AscertainLeena SachdevaNo ratings yet

- Capital Budgeting MethodsDocument13 pagesCapital Budgeting MethodsAmit SinghNo ratings yet

- Unit-3 Capital Budgeting DecisionsDocument30 pagesUnit-3 Capital Budgeting DecisionsKrishna Chandran PallippuramNo ratings yet

- Pay Back Period: What Is The Payback Period?Document18 pagesPay Back Period: What Is The Payback Period?TharinduNo ratings yet

- Recall The Flows of Funds and Decisions Important To The Financial ManagerDocument27 pagesRecall The Flows of Funds and Decisions Important To The Financial ManagerAyaz MahmoodNo ratings yet

- BF 14Document5 pagesBF 14zhairenaguila22No ratings yet

- Capital Bud ..Updated FinalDocument36 pagesCapital Bud ..Updated FinalKeyur JoshiNo ratings yet

- Capital Requirement, Raising Cost of Capital: Lecture FiveDocument32 pagesCapital Requirement, Raising Cost of Capital: Lecture FiveAbraham Temitope AkinnurojuNo ratings yet

- Payback Period-1Document12 pagesPayback Period-1OlamiNo ratings yet

- Present-Worth Analysis: Chapter Learning ObjectivesDocument30 pagesPresent-Worth Analysis: Chapter Learning ObjectivesRoman AliNo ratings yet

- Capital BudgetingDocument36 pagesCapital BudgetingDevansh DoshiNo ratings yet

- Capital Budgeting Report FinalDocument15 pagesCapital Budgeting Report FinalCezar SabladNo ratings yet

- IRR and PI - Group 5Document24 pagesIRR and PI - Group 5Pallavi BhardwajNo ratings yet

- Investment Valuation Criteria: Lecture 9thDocument49 pagesInvestment Valuation Criteria: Lecture 9thMihai StoicaNo ratings yet

- Choosing Innovation ProjectDocument25 pagesChoosing Innovation ProjectChrisha Jane LanutanNo ratings yet

- Mba Sem 2 Corporate Finance Capital BudgetingDocument17 pagesMba Sem 2 Corporate Finance Capital Budgetingekta mehtaNo ratings yet

- Capital Budgeting - Adv IssuesDocument21 pagesCapital Budgeting - Adv IssuesdixitBhavak DixitNo ratings yet

- Lecture 8Document37 pagesLecture 8Tesfaye ejetaNo ratings yet

- Financial Management: A Project On Capital BudgetingDocument20 pagesFinancial Management: A Project On Capital BudgetingHimanshi SethNo ratings yet

- Investment AppraisalDocument24 pagesInvestment AppraisalDeepankumar AthiyannanNo ratings yet

- Capital BudgetingDocument52 pagesCapital Budgetingrabitha07541No ratings yet

- Present ValueDocument8 pagesPresent ValueFarrukhsgNo ratings yet

- Ebtm3103 Slides Topic 3Document26 pagesEbtm3103 Slides Topic 3SUHAILI BINTI BOHORI STUDENTNo ratings yet

- Investment Appraisal 1Document13 pagesInvestment Appraisal 1Arslan ArifNo ratings yet

- 1.7 Financial ManagementDocument26 pages1.7 Financial ManagementEngr Mohammed UsmaniaNo ratings yet

- Methods of Project AppraisalDocument28 pagesMethods of Project AppraisalMîñåk ŞhïïNo ratings yet

- Arr 2Document5 pagesArr 2Rohit GandhiNo ratings yet

- Cfin 09Document19 pagesCfin 09Azra MuftiNo ratings yet

- Capital BudgetingDocument6 pagesCapital BudgetingRuchika AgarwalNo ratings yet

- Tute 6 PDFDocument4 pagesTute 6 PDFRony RahmanNo ratings yet

- Capital Budgeting1Document17 pagesCapital Budgeting1mohajansanjoy1975No ratings yet

- IRR NPV and PBP PDFDocument13 pagesIRR NPV and PBP PDFyared haftuNo ratings yet

- IRR, NPV and PBPDocument13 pagesIRR, NPV and PBPRajesh Shrestha100% (5)

- Investment AppraisalDocument23 pagesInvestment AppraisalHuzaifa Abdullah100% (2)

- ADocument89 pagesAJohn Carlo O. BallaresNo ratings yet

- Capital BudgetingDocument9 pagesCapital BudgetingHarshitaNo ratings yet

- Capital Budgeting, Cash Flows & Decision Making ProcessDocument47 pagesCapital Budgeting, Cash Flows & Decision Making ProcessAnifahchannie PacalnaNo ratings yet

- Chapter 4 Evaluating A Single Project Payback and BC RatioDocument13 pagesChapter 4 Evaluating A Single Project Payback and BC RatioSarah Mae WenceslaoNo ratings yet

- Capital Budgeting and Cost AnalysisDocument75 pagesCapital Budgeting and Cost AnalysisAkhil BatraNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Reflection DynedDocument1 pageReflection DynedmagoimoiNo ratings yet

- MAS With Answers PDFDocument13 pagesMAS With Answers PDF蔡嘉慧100% (1)

- Topics: Break-Even Analysis, Operating and Financial Leverage, and Optimal Capital StructureDocument5 pagesTopics: Break-Even Analysis, Operating and Financial Leverage, and Optimal Capital StructuremagoimoiNo ratings yet

- Single Entry (DONE!)Document8 pagesSingle Entry (DONE!)magoimoi0% (1)

- A Compilation of Financial Accounting Problems With Corresponding SolutionDocument1 pageA Compilation of Financial Accounting Problems With Corresponding SolutionmagoimoiNo ratings yet

- Cash and Accrual (DONE!)Document3 pagesCash and Accrual (DONE!)magoimoiNo ratings yet

- Notes (Done!)Document5 pagesNotes (Done!)magoimoiNo ratings yet

- Cash FlowDocument5 pagesCash FlowmagoimoiNo ratings yet

- AuditingDocument8 pagesAuditingmagoimoiNo ratings yet

- Chapter 11 Questions VarianceDocument5 pagesChapter 11 Questions VarianceBizu AlemayehuNo ratings yet

- Avalon Hill Air Baron - Strategy GuideDocument4 pagesAvalon Hill Air Baron - Strategy GuideRon Van 't VeerNo ratings yet

- Unit 7: Joint and By-Product Costing SystemDocument8 pagesUnit 7: Joint and By-Product Costing SystemCielo PulmaNo ratings yet

- Bord Na Gcon Report 2008Document48 pagesBord Na Gcon Report 2008thestorydotieNo ratings yet

- Mispriced Stocks: An OpportunityDocument12 pagesMispriced Stocks: An Opportunityarif420_999No ratings yet

- IposDocument14 pagesIposYudhister ReddyNo ratings yet

- Bukti TransferDocument1 pageBukti TransferBelajar Jangan rebahan ajaNo ratings yet

- Instruments of Trade Policy LVC ICAIDocument70 pagesInstruments of Trade Policy LVC ICAIpah studNo ratings yet

- Reactive Power Supplied by Wind Energy Converters - Cost-Benefit-AnalysisDocument10 pagesReactive Power Supplied by Wind Energy Converters - Cost-Benefit-AnalysisjandazNo ratings yet

- Kingspan TrranscriptDocument13 pagesKingspan Trranscriptdaveholohan8868No ratings yet

- ChapterIII Theory of Production and Cost.Document25 pagesChapterIII Theory of Production and Cost.VirencarpediemNo ratings yet

- Class Question CVPDocument2 pagesClass Question CVPTanuj LalchandaniNo ratings yet

- Chapter 7Document18 pagesChapter 7Raven Vargas DayritNo ratings yet

- CH 11, 13 QuestionsDocument17 pagesCH 11, 13 QuestionsNuman EratNo ratings yet

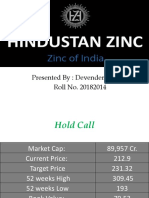

- Hindustan ZincDocument8 pagesHindustan ZincDevender SharmaNo ratings yet

- Product and Brand ManagementDocument171 pagesProduct and Brand ManagementAbhishek UpadhyayNo ratings yet

- Solved Complete Each of The Following Sentences A Your Tastes Determine TheDocument1 pageSolved Complete Each of The Following Sentences A Your Tastes Determine TheM Bilal SaleemNo ratings yet

- Cycle Time ReductionDocument5 pagesCycle Time ReductionpartygoerNo ratings yet

- G4 - Basic MicroeconDocument7 pagesG4 - Basic MicroeconannamicaellahismanaNo ratings yet

- Gold Coins: Presented By: Group EDocument21 pagesGold Coins: Presented By: Group EVairag JainNo ratings yet

- ASX - A Systematic Approach To Selling PremiumDocument4 pagesASX - A Systematic Approach To Selling PremiumPablo PaolucciNo ratings yet

- Chapter11 TestbankDocument10 pagesChapter11 TestbankKim Uyên Nguyen NgocNo ratings yet

- A Strong Brand, Dentonic Loses Its PowerDocument12 pagesA Strong Brand, Dentonic Loses Its Powermusicslave96No ratings yet

- Transcript of Philippine Star Interview With Rody DuterteDocument5 pagesTranscript of Philippine Star Interview With Rody DuterteRochelle Arayata AguilarNo ratings yet