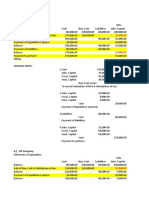

Financial Accounting June, 2009. First Year

Financial Accounting June, 2009. First Year

You might also like

- Information Technology (802) - Class 12 - Lesson 1 - Mysql CommandsDocument35 pagesInformation Technology (802) - Class 12 - Lesson 1 - Mysql CommandsSudhakar R100% (1)

- Midterm ExamDocument25 pagesMidterm Examarnel buanNo ratings yet

- Microsoft Office and OpenOfficeDocument5 pagesMicrosoft Office and OpenOfficeguysbadNo ratings yet

- Information Technology (802) - Class 12 - Lesson 3. Fundamentals of Java Programming - Part 3Document52 pagesInformation Technology (802) - Class 12 - Lesson 3. Fundamentals of Java Programming - Part 3Sudhakar RNo ratings yet

- Information Technology (802) - Class 12 - Lesson 3 - Fundamentals of Java Programming - Part 1Document31 pagesInformation Technology (802) - Class 12 - Lesson 3 - Fundamentals of Java Programming - Part 1Sudhakar RNo ratings yet

- Policy No Policy OnDocument6 pagesPolicy No Policy OnSudhakar RNo ratings yet

- Use of Raspberry Pi in Operating Systems ClassDocument6 pagesUse of Raspberry Pi in Operating Systems Classgileraz90No ratings yet

- Multinational Company&Computer EthicsDocument29 pagesMultinational Company&Computer EthicspremsonyNo ratings yet

- Operating SystemDocument20 pagesOperating SystemTony StarkNo ratings yet

- Fedora Operating SystemDocument11 pagesFedora Operating Systemarvi.sardarNo ratings yet

- QuizDocument7 pagesQuizPiyush KhandelwalNo ratings yet

- Science IXDocument5 pagesScience IXSudhakar RNo ratings yet

- CS101 Abbreviations From Lectures 1 To 81Document7 pagesCS101 Abbreviations From Lectures 1 To 81Kinza LaiqatNo ratings yet

- Computer VirusDocument15 pagesComputer VirusautomationwindowNo ratings yet

- Computer ViruesDocument19 pagesComputer ViruesMuhammad Adeel AnsariNo ratings yet

- Chapter - 001: Computer Fundamental & HistoryDocument33 pagesChapter - 001: Computer Fundamental & HistoryPRAVINITNo ratings yet

- Open Office TutorialDocument127 pagesOpen Office TutorialRudyard VonNo ratings yet

- Self - Managed Work TeamsDocument23 pagesSelf - Managed Work Teamsrak_sai15100% (2)

- Important Abbreviations - ComputersDocument2 pagesImportant Abbreviations - Computersanilnair88No ratings yet

- Plan 9 Operating SystemDocument10 pagesPlan 9 Operating SystemDipak HarkalNo ratings yet

- Unit-2 Operating SystemDocument74 pagesUnit-2 Operating SystemSaroj VarshneyNo ratings yet

- Role of Information and Communication TechnologiesDocument12 pagesRole of Information and Communication TechnologiesmathanNo ratings yet

- # All Words Fullform Related ComputerDocument8 pages# All Words Fullform Related ComputerPushpa Rani100% (1)

- Office LayoutDocument36 pagesOffice LayoutchagrapunNo ratings yet

- Virus and AntivirusDocument18 pagesVirus and AntivirusJacob CharlesNo ratings yet

- Computer VirusDocument24 pagesComputer VirusAvneet KaurNo ratings yet

- Emotional Intelligence, Staff Management Skills and Job SatisfactionDocument39 pagesEmotional Intelligence, Staff Management Skills and Job SatisfactionShania Jane MontañezNo ratings yet

- CS1010 Introduction To Computing: (Computer Software)Document65 pagesCS1010 Introduction To Computing: (Computer Software)asad shahNo ratings yet

- Parts of ComputerDocument18 pagesParts of ComputerJazzt D MerencillaNo ratings yet

- Information and Communication TechnologyDocument299 pagesInformation and Communication TechnologyKishor ShettiNo ratings yet

- Operating Systems Structures: Jerry BreecherDocument22 pagesOperating Systems Structures: Jerry Breecherbutterfily100% (1)

- A Developing Self-Management SkillsDocument11 pagesA Developing Self-Management Skillsjjespiritu21No ratings yet

- Computer Virus and WormsDocument28 pagesComputer Virus and WormsDeepak PatraNo ratings yet

- Self Managed TeamsDocument13 pagesSelf Managed Teamsrabh21santaNo ratings yet

- VP-Finance - VP-Corporate HR - CFO - CEO - DirectorDocument3 pagesVP-Finance - VP-Corporate HR - CFO - CEO - DirectorSudhakar RNo ratings yet

- Chapter 1 Introduction To ComputerDocument44 pagesChapter 1 Introduction To ComputerHana BertianiNo ratings yet

- Cable Operating SystemDocument21 pagesCable Operating SystemBarry AllenNo ratings yet

- Open Office ImpressDocument5 pagesOpen Office Impress7A04Aditya MayankNo ratings yet

- Computer VirusDocument17 pagesComputer Virusapi-275496974No ratings yet

- Real Time Operating SystemsDocument35 pagesReal Time Operating SystemsNeerajBooraNo ratings yet

- Types of Application SoftwareDocument7 pagesTypes of Application SoftwareRakesh KurupatiNo ratings yet

- Opearting SystemDocument25 pagesOpearting SystemlovishsindhwaniNo ratings yet

- Functions of Operating SystemDocument6 pagesFunctions of Operating SystemGaurav BishtNo ratings yet

- Management SkillsDocument59 pagesManagement SkillsHmoodAlsaadounNo ratings yet

- Operating SystemDocument29 pagesOperating SystemFrancine EspinedaNo ratings yet

- Data and Information: What Is A Computer?Document6 pagesData and Information: What Is A Computer?Adnan KhanNo ratings yet

- Module 1Document39 pagesModule 1Soniya Kadam100% (1)

- SoftwareDocument37 pagesSoftwareAnjanette BautistaNo ratings yet

- Introduction To Open OfficeDocument12 pagesIntroduction To Open OfficeVithanalage WathsalaNo ratings yet

- University For Development Studies: Faculty of EducationDocument41 pagesUniversity For Development Studies: Faculty of EducationKofi AsaaseNo ratings yet

- Parts of A ComputerDocument30 pagesParts of A ComputerChangani Jagdish GNo ratings yet

- Seminar Topics: Name of The TopicDocument12 pagesSeminar Topics: Name of The TopicRahul NambiarNo ratings yet

- ICT Practical 10thDocument6 pagesICT Practical 10thAnonymous ifheT2Yhi100% (1)

- The Magic of Team WorkDocument3 pagesThe Magic of Team WorkSudhakar RNo ratings yet

- The Operating System's JobDocument30 pagesThe Operating System's JobGlyndel D DupioNo ratings yet

- Operating System NotesDocument42 pagesOperating System NotesironmanNo ratings yet

- A Colloquim Report ON: Computer VirusDocument13 pagesA Colloquim Report ON: Computer VirusRishi KalaNo ratings yet

- Computer Abbreviations For All Competitive ExamsDocument9 pagesComputer Abbreviations For All Competitive ExamsVortex 366No ratings yet

- Topic 1 Digital DevicesDocument38 pagesTopic 1 Digital DevicesEmma MakinNo ratings yet

- Computer Virus: BY Shivang BhattDocument19 pagesComputer Virus: BY Shivang BhattSunil PillaiNo ratings yet

- Introduction To Information Technology: DR Dharmendra Kumar KanchanDocument83 pagesIntroduction To Information Technology: DR Dharmendra Kumar KanchanSadhika KatiyarNo ratings yet

- Computer Virus and Antivirus TechniquesDocument37 pagesComputer Virus and Antivirus TechniquessanjuNo ratings yet

- Presentation 1Document21 pagesPresentation 1md zuber alamNo ratings yet

- Bpz2a Bpf2a Sbaml Bpc2a Bpg2aDocument10 pagesBpz2a Bpf2a Sbaml Bpc2a Bpg2aJimmyNo ratings yet

- Information Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 3Document17 pagesInformation Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 3Sudhakar R100% (2)

- Information Technology (802) - Class 12 - Employability Skills - Entrepreneurial SkillsDocument32 pagesInformation Technology (802) - Class 12 - Employability Skills - Entrepreneurial SkillsSudhakar R50% (4)

- Information Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 1Document18 pagesInformation Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 1Sudhakar R0% (1)

- Information Technology (802) - Class 12 - Employability Skills - Green SkillsDocument31 pagesInformation Technology (802) - Class 12 - Employability Skills - Green SkillsSudhakar R100% (2)

- Information Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 2Document18 pagesInformation Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 2Sudhakar R100% (1)

- Information Technology (802) - Class 12 - Employability Skill - Communication SkillDocument15 pagesInformation Technology (802) - Class 12 - Employability Skill - Communication SkillSudhakar R100% (1)

- Information Technology (802) - Class 12 - UNIT 4 - Work Integrated Learning IT - Part 1Document28 pagesInformation Technology (802) - Class 12 - UNIT 4 - Work Integrated Learning IT - Part 1Sudhakar R50% (2)

- Information Technology (802) - Class 12 - Lesson 3 - Fundamentals of Java Programming - Part 2Document61 pagesInformation Technology (802) - Class 12 - Lesson 3 - Fundamentals of Java Programming - Part 2Sudhakar RNo ratings yet

- Information Technology (802) - Class 12 - UNIT 4 - Work Integrated Learning IT - Session 2Document21 pagesInformation Technology (802) - Class 12 - UNIT 4 - Work Integrated Learning IT - Session 2Sudhakar RNo ratings yet

- Information Technology (802) - Class 12 - Lesson 2 - Operating WebDocument30 pagesInformation Technology (802) - Class 12 - Lesson 2 - Operating WebSudhakar R100% (1)

- Policy No Policy OnDocument8 pagesPolicy No Policy OnSudhakar RNo ratings yet

- Data Security PolicyDocument4 pagesData Security PolicySudhakar RNo ratings yet

- Science IXDocument5 pagesScience IXSudhakar RNo ratings yet

- Information Technology (802) Class 12 - Lesson 1 - Database ConceptsDocument17 pagesInformation Technology (802) Class 12 - Lesson 1 - Database ConceptsSudhakar R71% (7)

- VP-Finance - VP-Corporate HR - CFO - CEO - DirectorDocument3 pagesVP-Finance - VP-Corporate HR - CFO - CEO - DirectorSudhakar RNo ratings yet

- 4B - MedicalreimbpolicyDocument2 pages4B - MedicalreimbpolicySudhakar RNo ratings yet

- Effectiveness in Recruitment and Selection: Interviews Suffer A Number of Disadvantages ..... What Are They?Document3 pagesEffectiveness in Recruitment and Selection: Interviews Suffer A Number of Disadvantages ..... What Are They?Sudhakar RNo ratings yet

- Unit 1: Computer Fundamentals: Class XI (Theory)Document3 pagesUnit 1: Computer Fundamentals: Class XI (Theory)Sudhakar RNo ratings yet

- Policy No Policy OnDocument6 pagesPolicy No Policy OnSudhakar RNo ratings yet

- Computer Science XIIDocument3 pagesComputer Science XIISudhakar RNo ratings yet

- Policy No B 3 / M AnnexureDocument5 pagesPolicy No B 3 / M AnnexureSudhakar RNo ratings yet

- Annexure - 2Document3 pagesAnnexure - 2Sudhakar RNo ratings yet

- The Magic of Team WorkDocument3 pagesThe Magic of Team WorkSudhakar RNo ratings yet

- Mathematics (CODE NO. 041) : Course Structure Class IXDocument6 pagesMathematics (CODE NO. 041) : Course Structure Class IXSudhakar RNo ratings yet

- This Is Two-Year Syllabus For Classes IX and X: The Overall Aims of The Course AreDocument18 pagesThis Is Two-Year Syllabus For Classes IX and X: The Overall Aims of The Course AreSudhakar RNo ratings yet

- Social Science IXDocument10 pagesSocial Science IXSudhakar RNo ratings yet

- Chapter 2 Accounting For PartnershipsDocument102 pagesChapter 2 Accounting For PartnershipsVon Lloyd Ledesma Loren100% (1)

- Chapter 9 Financial Instruments: Learning ObjectivesDocument41 pagesChapter 9 Financial Instruments: Learning Objectivessamuel_dwumfourNo ratings yet

- Solution QUIZ Partnership LiquidationDocument6 pagesSolution QUIZ Partnership Liquidationchezyl cadinongNo ratings yet

- Mmem28 Corporate Finance - s8 Uts DMMX Equity AnalysisDocument7 pagesMmem28 Corporate Finance - s8 Uts DMMX Equity AnalysisIsmiyar CahyaniNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument35 pagesFinancial Statement Analysis: K R Subramanyam John J Wildchristina dwi setiaNo ratings yet

- Daftar Akun PT Niko ElektronikDocument4 pagesDaftar Akun PT Niko ElektronikYulitaNo ratings yet

- Revenue From Contracts With CustomersDocument4 pagesRevenue From Contracts With Customersmy miNo ratings yet

- Chapter-16 - Simple Interest PDFDocument6 pagesChapter-16 - Simple Interest PDFdeepaksaini140% (1)

- PartnershipDocument10 pagesPartnershipJasmine Marie Ng Cheong50% (2)

- Rachel's Baking Delights: Business PlanDocument21 pagesRachel's Baking Delights: Business PlanRachel Flores SanchezNo ratings yet

- Epo Financial Statements 2013 V 16Document40 pagesEpo Financial Statements 2013 V 16Appie KoekangeNo ratings yet

- Managerial Accounting Term Paper Sta. Lucia Land, Inc.Document23 pagesManagerial Accounting Term Paper Sta. Lucia Land, Inc.Joan BasayNo ratings yet

- Elimination of Unrealized Profit On Intercompany Sales of InventoryDocument102 pagesElimination of Unrealized Profit On Intercompany Sales of InventorySia DLSLNo ratings yet

- Acc CIA2Document22 pagesAcc CIA2Aleena Clare ThomasNo ratings yet

- JSW Energy: Horizontal Analysis Vertical AnalysisDocument15 pagesJSW Energy: Horizontal Analysis Vertical Analysissuyash gargNo ratings yet

- JPIA Current LiabilitiesDocument7 pagesJPIA Current LiabilitiesKimboy Elizalde PanaguitonNo ratings yet

- UNIT (24) 2.08 CONSOLIDATED bALANCE SHEET PROBLEMDocument4 pagesUNIT (24) 2.08 CONSOLIDATED bALANCE SHEET PROBLEMAaryan K MNo ratings yet

- CORRECTION Egypt Dairy Sector Note 31 Oct 2017Document18 pagesCORRECTION Egypt Dairy Sector Note 31 Oct 2017Ahmed Ali HefnawyNo ratings yet

- AY2020-21 132 B CompressedDocument306 pagesAY2020-21 132 B CompressedJitendra UdawantNo ratings yet

- Strategic Profit ModelDocument2 pagesStrategic Profit Modelth3hackerssquadNo ratings yet

- Sapm Unit - 3Document36 pagesSapm Unit - 3Alavudeen Shajahan100% (3)

- A Project Report On Ratio Analysis at The Gadag Co-Operative Textile Mill LTDDocument67 pagesA Project Report On Ratio Analysis at The Gadag Co-Operative Textile Mill LTDBabasab Patil (Karrisatte)No ratings yet

- CE On Quasi-ReorganizationDocument1 pageCE On Quasi-ReorganizationalyssaNo ratings yet

- Takeawaycom NV Annual Report 2016 PDFDocument126 pagesTakeawaycom NV Annual Report 2016 PDFSXC948No ratings yet

- Consolidated Balance Sheet Equity and Liabilities Shareholders' FundsDocument17 pagesConsolidated Balance Sheet Equity and Liabilities Shareholders' FundsGaurav SharmaNo ratings yet

- Financial Reporting Final Mock: Barcelona Madrid Non-Current AssetsDocument7 pagesFinancial Reporting Final Mock: Barcelona Madrid Non-Current AssetsMuhammad AsadNo ratings yet

- Accounting AdjustmentDocument6 pagesAccounting AdjustmentIzzat AzriNo ratings yet

- MBA Intership Report On Liquidity Management Process of The City Bank Ltd-LibreDocument84 pagesMBA Intership Report On Liquidity Management Process of The City Bank Ltd-LibreGultekin Binte AzadNo ratings yet

- The Accounting EquationDocument24 pagesThe Accounting EquationShaina CalingNo ratings yet

Download as pdf or txt

You might also like

- Information Technology (802) - Class 12 - Lesson 1 - Mysql CommandsDocument35 pagesInformation Technology (802) - Class 12 - Lesson 1 - Mysql CommandsSudhakar R100% (1)

- Midterm ExamDocument25 pagesMidterm Examarnel buanNo ratings yet

- Microsoft Office and OpenOfficeDocument5 pagesMicrosoft Office and OpenOfficeguysbadNo ratings yet

- Information Technology (802) - Class 12 - Lesson 3. Fundamentals of Java Programming - Part 3Document52 pagesInformation Technology (802) - Class 12 - Lesson 3. Fundamentals of Java Programming - Part 3Sudhakar RNo ratings yet

- Information Technology (802) - Class 12 - Lesson 3 - Fundamentals of Java Programming - Part 1Document31 pagesInformation Technology (802) - Class 12 - Lesson 3 - Fundamentals of Java Programming - Part 1Sudhakar RNo ratings yet

- Policy No Policy OnDocument6 pagesPolicy No Policy OnSudhakar RNo ratings yet

- Use of Raspberry Pi in Operating Systems ClassDocument6 pagesUse of Raspberry Pi in Operating Systems Classgileraz90No ratings yet

- Multinational Company&Computer EthicsDocument29 pagesMultinational Company&Computer EthicspremsonyNo ratings yet

- Operating SystemDocument20 pagesOperating SystemTony StarkNo ratings yet

- Fedora Operating SystemDocument11 pagesFedora Operating Systemarvi.sardarNo ratings yet

- QuizDocument7 pagesQuizPiyush KhandelwalNo ratings yet

- Science IXDocument5 pagesScience IXSudhakar RNo ratings yet

- CS101 Abbreviations From Lectures 1 To 81Document7 pagesCS101 Abbreviations From Lectures 1 To 81Kinza LaiqatNo ratings yet

- Computer VirusDocument15 pagesComputer VirusautomationwindowNo ratings yet

- Computer ViruesDocument19 pagesComputer ViruesMuhammad Adeel AnsariNo ratings yet

- Chapter - 001: Computer Fundamental & HistoryDocument33 pagesChapter - 001: Computer Fundamental & HistoryPRAVINITNo ratings yet

- Open Office TutorialDocument127 pagesOpen Office TutorialRudyard VonNo ratings yet

- Self - Managed Work TeamsDocument23 pagesSelf - Managed Work Teamsrak_sai15100% (2)

- Important Abbreviations - ComputersDocument2 pagesImportant Abbreviations - Computersanilnair88No ratings yet

- Plan 9 Operating SystemDocument10 pagesPlan 9 Operating SystemDipak HarkalNo ratings yet

- Unit-2 Operating SystemDocument74 pagesUnit-2 Operating SystemSaroj VarshneyNo ratings yet

- Role of Information and Communication TechnologiesDocument12 pagesRole of Information and Communication TechnologiesmathanNo ratings yet

- # All Words Fullform Related ComputerDocument8 pages# All Words Fullform Related ComputerPushpa Rani100% (1)

- Office LayoutDocument36 pagesOffice LayoutchagrapunNo ratings yet

- Virus and AntivirusDocument18 pagesVirus and AntivirusJacob CharlesNo ratings yet

- Computer VirusDocument24 pagesComputer VirusAvneet KaurNo ratings yet

- Emotional Intelligence, Staff Management Skills and Job SatisfactionDocument39 pagesEmotional Intelligence, Staff Management Skills and Job SatisfactionShania Jane MontañezNo ratings yet

- CS1010 Introduction To Computing: (Computer Software)Document65 pagesCS1010 Introduction To Computing: (Computer Software)asad shahNo ratings yet

- Parts of ComputerDocument18 pagesParts of ComputerJazzt D MerencillaNo ratings yet

- Information and Communication TechnologyDocument299 pagesInformation and Communication TechnologyKishor ShettiNo ratings yet

- Operating Systems Structures: Jerry BreecherDocument22 pagesOperating Systems Structures: Jerry Breecherbutterfily100% (1)

- A Developing Self-Management SkillsDocument11 pagesA Developing Self-Management Skillsjjespiritu21No ratings yet

- Computer Virus and WormsDocument28 pagesComputer Virus and WormsDeepak PatraNo ratings yet

- Self Managed TeamsDocument13 pagesSelf Managed Teamsrabh21santaNo ratings yet

- VP-Finance - VP-Corporate HR - CFO - CEO - DirectorDocument3 pagesVP-Finance - VP-Corporate HR - CFO - CEO - DirectorSudhakar RNo ratings yet

- Chapter 1 Introduction To ComputerDocument44 pagesChapter 1 Introduction To ComputerHana BertianiNo ratings yet

- Cable Operating SystemDocument21 pagesCable Operating SystemBarry AllenNo ratings yet

- Open Office ImpressDocument5 pagesOpen Office Impress7A04Aditya MayankNo ratings yet

- Computer VirusDocument17 pagesComputer Virusapi-275496974No ratings yet

- Real Time Operating SystemsDocument35 pagesReal Time Operating SystemsNeerajBooraNo ratings yet

- Types of Application SoftwareDocument7 pagesTypes of Application SoftwareRakesh KurupatiNo ratings yet

- Opearting SystemDocument25 pagesOpearting SystemlovishsindhwaniNo ratings yet

- Functions of Operating SystemDocument6 pagesFunctions of Operating SystemGaurav BishtNo ratings yet

- Management SkillsDocument59 pagesManagement SkillsHmoodAlsaadounNo ratings yet

- Operating SystemDocument29 pagesOperating SystemFrancine EspinedaNo ratings yet

- Data and Information: What Is A Computer?Document6 pagesData and Information: What Is A Computer?Adnan KhanNo ratings yet

- Module 1Document39 pagesModule 1Soniya Kadam100% (1)

- SoftwareDocument37 pagesSoftwareAnjanette BautistaNo ratings yet

- Introduction To Open OfficeDocument12 pagesIntroduction To Open OfficeVithanalage WathsalaNo ratings yet

- University For Development Studies: Faculty of EducationDocument41 pagesUniversity For Development Studies: Faculty of EducationKofi AsaaseNo ratings yet

- Parts of A ComputerDocument30 pagesParts of A ComputerChangani Jagdish GNo ratings yet

- Seminar Topics: Name of The TopicDocument12 pagesSeminar Topics: Name of The TopicRahul NambiarNo ratings yet

- ICT Practical 10thDocument6 pagesICT Practical 10thAnonymous ifheT2Yhi100% (1)

- The Magic of Team WorkDocument3 pagesThe Magic of Team WorkSudhakar RNo ratings yet

- The Operating System's JobDocument30 pagesThe Operating System's JobGlyndel D DupioNo ratings yet

- Operating System NotesDocument42 pagesOperating System NotesironmanNo ratings yet

- A Colloquim Report ON: Computer VirusDocument13 pagesA Colloquim Report ON: Computer VirusRishi KalaNo ratings yet

- Computer Abbreviations For All Competitive ExamsDocument9 pagesComputer Abbreviations For All Competitive ExamsVortex 366No ratings yet

- Topic 1 Digital DevicesDocument38 pagesTopic 1 Digital DevicesEmma MakinNo ratings yet

- Computer Virus: BY Shivang BhattDocument19 pagesComputer Virus: BY Shivang BhattSunil PillaiNo ratings yet

- Introduction To Information Technology: DR Dharmendra Kumar KanchanDocument83 pagesIntroduction To Information Technology: DR Dharmendra Kumar KanchanSadhika KatiyarNo ratings yet

- Computer Virus and Antivirus TechniquesDocument37 pagesComputer Virus and Antivirus TechniquessanjuNo ratings yet

- Presentation 1Document21 pagesPresentation 1md zuber alamNo ratings yet

- Bpz2a Bpf2a Sbaml Bpc2a Bpg2aDocument10 pagesBpz2a Bpf2a Sbaml Bpc2a Bpg2aJimmyNo ratings yet

- Information Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 3Document17 pagesInformation Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 3Sudhakar R100% (2)

- Information Technology (802) - Class 12 - Employability Skills - Entrepreneurial SkillsDocument32 pagesInformation Technology (802) - Class 12 - Employability Skills - Entrepreneurial SkillsSudhakar R50% (4)

- Information Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 1Document18 pagesInformation Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 1Sudhakar R0% (1)

- Information Technology (802) - Class 12 - Employability Skills - Green SkillsDocument31 pagesInformation Technology (802) - Class 12 - Employability Skills - Green SkillsSudhakar R100% (2)

- Information Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 2Document18 pagesInformation Technology (802) - Class 12 - Employability Skills - Unit 3 - Basic Ict Skills - IV - Session 2Sudhakar R100% (1)

- Information Technology (802) - Class 12 - Employability Skill - Communication SkillDocument15 pagesInformation Technology (802) - Class 12 - Employability Skill - Communication SkillSudhakar R100% (1)

- Information Technology (802) - Class 12 - UNIT 4 - Work Integrated Learning IT - Part 1Document28 pagesInformation Technology (802) - Class 12 - UNIT 4 - Work Integrated Learning IT - Part 1Sudhakar R50% (2)

- Information Technology (802) - Class 12 - Lesson 3 - Fundamentals of Java Programming - Part 2Document61 pagesInformation Technology (802) - Class 12 - Lesson 3 - Fundamentals of Java Programming - Part 2Sudhakar RNo ratings yet

- Information Technology (802) - Class 12 - UNIT 4 - Work Integrated Learning IT - Session 2Document21 pagesInformation Technology (802) - Class 12 - UNIT 4 - Work Integrated Learning IT - Session 2Sudhakar RNo ratings yet

- Information Technology (802) - Class 12 - Lesson 2 - Operating WebDocument30 pagesInformation Technology (802) - Class 12 - Lesson 2 - Operating WebSudhakar R100% (1)

- Policy No Policy OnDocument8 pagesPolicy No Policy OnSudhakar RNo ratings yet

- Data Security PolicyDocument4 pagesData Security PolicySudhakar RNo ratings yet

- Science IXDocument5 pagesScience IXSudhakar RNo ratings yet

- Information Technology (802) Class 12 - Lesson 1 - Database ConceptsDocument17 pagesInformation Technology (802) Class 12 - Lesson 1 - Database ConceptsSudhakar R71% (7)

- VP-Finance - VP-Corporate HR - CFO - CEO - DirectorDocument3 pagesVP-Finance - VP-Corporate HR - CFO - CEO - DirectorSudhakar RNo ratings yet

- 4B - MedicalreimbpolicyDocument2 pages4B - MedicalreimbpolicySudhakar RNo ratings yet

- Effectiveness in Recruitment and Selection: Interviews Suffer A Number of Disadvantages ..... What Are They?Document3 pagesEffectiveness in Recruitment and Selection: Interviews Suffer A Number of Disadvantages ..... What Are They?Sudhakar RNo ratings yet

- Unit 1: Computer Fundamentals: Class XI (Theory)Document3 pagesUnit 1: Computer Fundamentals: Class XI (Theory)Sudhakar RNo ratings yet

- Policy No Policy OnDocument6 pagesPolicy No Policy OnSudhakar RNo ratings yet

- Computer Science XIIDocument3 pagesComputer Science XIISudhakar RNo ratings yet

- Policy No B 3 / M AnnexureDocument5 pagesPolicy No B 3 / M AnnexureSudhakar RNo ratings yet

- Annexure - 2Document3 pagesAnnexure - 2Sudhakar RNo ratings yet

- The Magic of Team WorkDocument3 pagesThe Magic of Team WorkSudhakar RNo ratings yet

- Mathematics (CODE NO. 041) : Course Structure Class IXDocument6 pagesMathematics (CODE NO. 041) : Course Structure Class IXSudhakar RNo ratings yet

- This Is Two-Year Syllabus For Classes IX and X: The Overall Aims of The Course AreDocument18 pagesThis Is Two-Year Syllabus For Classes IX and X: The Overall Aims of The Course AreSudhakar RNo ratings yet

- Social Science IXDocument10 pagesSocial Science IXSudhakar RNo ratings yet

- Chapter 2 Accounting For PartnershipsDocument102 pagesChapter 2 Accounting For PartnershipsVon Lloyd Ledesma Loren100% (1)

- Chapter 9 Financial Instruments: Learning ObjectivesDocument41 pagesChapter 9 Financial Instruments: Learning Objectivessamuel_dwumfourNo ratings yet

- Solution QUIZ Partnership LiquidationDocument6 pagesSolution QUIZ Partnership Liquidationchezyl cadinongNo ratings yet

- Mmem28 Corporate Finance - s8 Uts DMMX Equity AnalysisDocument7 pagesMmem28 Corporate Finance - s8 Uts DMMX Equity AnalysisIsmiyar CahyaniNo ratings yet

- Financial Statement Analysis: K R Subramanyam John J WildDocument35 pagesFinancial Statement Analysis: K R Subramanyam John J Wildchristina dwi setiaNo ratings yet

- Daftar Akun PT Niko ElektronikDocument4 pagesDaftar Akun PT Niko ElektronikYulitaNo ratings yet

- Revenue From Contracts With CustomersDocument4 pagesRevenue From Contracts With Customersmy miNo ratings yet

- Chapter-16 - Simple Interest PDFDocument6 pagesChapter-16 - Simple Interest PDFdeepaksaini140% (1)

- PartnershipDocument10 pagesPartnershipJasmine Marie Ng Cheong50% (2)

- Rachel's Baking Delights: Business PlanDocument21 pagesRachel's Baking Delights: Business PlanRachel Flores SanchezNo ratings yet

- Epo Financial Statements 2013 V 16Document40 pagesEpo Financial Statements 2013 V 16Appie KoekangeNo ratings yet

- Managerial Accounting Term Paper Sta. Lucia Land, Inc.Document23 pagesManagerial Accounting Term Paper Sta. Lucia Land, Inc.Joan BasayNo ratings yet

- Elimination of Unrealized Profit On Intercompany Sales of InventoryDocument102 pagesElimination of Unrealized Profit On Intercompany Sales of InventorySia DLSLNo ratings yet

- Acc CIA2Document22 pagesAcc CIA2Aleena Clare ThomasNo ratings yet

- JSW Energy: Horizontal Analysis Vertical AnalysisDocument15 pagesJSW Energy: Horizontal Analysis Vertical Analysissuyash gargNo ratings yet

- JPIA Current LiabilitiesDocument7 pagesJPIA Current LiabilitiesKimboy Elizalde PanaguitonNo ratings yet

- UNIT (24) 2.08 CONSOLIDATED bALANCE SHEET PROBLEMDocument4 pagesUNIT (24) 2.08 CONSOLIDATED bALANCE SHEET PROBLEMAaryan K MNo ratings yet

- CORRECTION Egypt Dairy Sector Note 31 Oct 2017Document18 pagesCORRECTION Egypt Dairy Sector Note 31 Oct 2017Ahmed Ali HefnawyNo ratings yet

- AY2020-21 132 B CompressedDocument306 pagesAY2020-21 132 B CompressedJitendra UdawantNo ratings yet

- Strategic Profit ModelDocument2 pagesStrategic Profit Modelth3hackerssquadNo ratings yet

- Sapm Unit - 3Document36 pagesSapm Unit - 3Alavudeen Shajahan100% (3)

- A Project Report On Ratio Analysis at The Gadag Co-Operative Textile Mill LTDDocument67 pagesA Project Report On Ratio Analysis at The Gadag Co-Operative Textile Mill LTDBabasab Patil (Karrisatte)No ratings yet

- CE On Quasi-ReorganizationDocument1 pageCE On Quasi-ReorganizationalyssaNo ratings yet

- Takeawaycom NV Annual Report 2016 PDFDocument126 pagesTakeawaycom NV Annual Report 2016 PDFSXC948No ratings yet

- Consolidated Balance Sheet Equity and Liabilities Shareholders' FundsDocument17 pagesConsolidated Balance Sheet Equity and Liabilities Shareholders' FundsGaurav SharmaNo ratings yet

- Financial Reporting Final Mock: Barcelona Madrid Non-Current AssetsDocument7 pagesFinancial Reporting Final Mock: Barcelona Madrid Non-Current AssetsMuhammad AsadNo ratings yet

- Accounting AdjustmentDocument6 pagesAccounting AdjustmentIzzat AzriNo ratings yet

- MBA Intership Report On Liquidity Management Process of The City Bank Ltd-LibreDocument84 pagesMBA Intership Report On Liquidity Management Process of The City Bank Ltd-LibreGultekin Binte AzadNo ratings yet

- The Accounting EquationDocument24 pagesThe Accounting EquationShaina CalingNo ratings yet