Download as xls, pdf, or txt

You might also like

- Excel Mass Balance CVD NalaysaiDocument31 pagesExcel Mass Balance CVD NalaysaiLuqmanhakim XavNo ratings yet

- Stoichiometry Worksheet6-1Document6 pagesStoichiometry Worksheet6-1Von AmoresNo ratings yet

- 1B-FNDC003 BOM12 2S2021 EA07: Adjusting Entries: End of QuizDocument9 pages1B-FNDC003 BOM12 2S2021 EA07: Adjusting Entries: End of QuizNina Donato100% (1)

- Past Final Papers 1Document21 pagesPast Final Papers 1Luqmanhakim XavNo ratings yet

- Strain and Deflection of A Circular Plate - Lab ReportDocument4 pagesStrain and Deflection of A Circular Plate - Lab ReportRoshane NanayakkaraNo ratings yet

- Husserl, Edmund - The Idea of PhenomenologyDocument75 pagesHusserl, Edmund - The Idea of PhenomenologyFelipeMgr100% (7)

- 10 Full Questions Till Closing Account BSSE (2A)Document33 pages10 Full Questions Till Closing Account BSSE (2A)Should Should100% (2)

- Financial Statement ExamDocument2 pagesFinancial Statement ExamTam TamNo ratings yet

- Ch01 McGuiganDocument31 pagesCh01 McGuiganJonathan WatersNo ratings yet

- What Is Management Science?: Management Science (MS) Known To Some As Quantitative Analysis (QA)Document8 pagesWhat Is Management Science?: Management Science (MS) Known To Some As Quantitative Analysis (QA)Mhelren De La PeñaNo ratings yet

- Depreciation Rate Bakery IndustryDocument2 pagesDepreciation Rate Bakery IndustryPhuong Ho100% (1)

- FINC 304 Managerial EconomicsDocument21 pagesFINC 304 Managerial EconomicsJephthah BansahNo ratings yet

- CFAS REVIEWER 1st Sem Depratmental ExamDocument16 pagesCFAS REVIEWER 1st Sem Depratmental ExamRhona Mae DonguinesNo ratings yet

- TOS Common Exam 2S1819Document24 pagesTOS Common Exam 2S1819Mary Anne ManaoisNo ratings yet

- Week1 AUD1201-IA & Entitys CNTRL EnvironmentDocument44 pagesWeek1 AUD1201-IA & Entitys CNTRL EnvironmentHeidee SabidoNo ratings yet

- rev-mat-2-IA Print PDFDocument31 pagesrev-mat-2-IA Print PDFAyaka FujiharaNo ratings yet

- FM - Cost of CapitalDocument26 pagesFM - Cost of CapitalMaxine SantosNo ratings yet

- IRR - 5th NFJPIA CUPDocument6 pagesIRR - 5th NFJPIA CUPJanna CaducioNo ratings yet

- Ac101 ch3Document21 pagesAc101 ch3Alex ChewNo ratings yet

- Case Problem 1 Forecasting SalesDocument3 pagesCase Problem 1 Forecasting SalesSomething ChicNo ratings yet

- Baysas Problems Partnership OperationsDocument3 pagesBaysas Problems Partnership OperationsHoney MuliNo ratings yet

- Chapter1-4 Answers Cfa BookDocument35 pagesChapter1-4 Answers Cfa BookSaeym Segovia100% (1)

- Review For Quiz 3 Part 2Document18 pagesReview For Quiz 3 Part 2Mariah ValizadoNo ratings yet

- Chapter 1 - EthicsDocument7 pagesChapter 1 - EthicsEzekylah AlbaNo ratings yet

- Human Relations and Morale in Business OrganizationDocument9 pagesHuman Relations and Morale in Business OrganizationRonajane Bael100% (1)

- Basic Accounting Test Questions1Document4 pagesBasic Accounting Test Questions1Ervin CabangalNo ratings yet

- Journal-Entry AssignmentsDocument2 pagesJournal-Entry AssignmentsRieven BaracinasNo ratings yet

- Principles of Accounting Midterm Exam - Sum 2022Document7 pagesPrinciples of Accounting Midterm Exam - Sum 2022Yến Hoàng HảiNo ratings yet

- DONE-Chapter 6 CompleteDocument3 pagesDONE-Chapter 6 CompleteDaphne De LeonNo ratings yet

- Republic Act No. 8293, Known As The "Intellectual Property Code of The Philippines", As Amended by Republic Act No. 10372 The Law On PatentsDocument9 pagesRepublic Act No. 8293, Known As The "Intellectual Property Code of The Philippines", As Amended by Republic Act No. 10372 The Law On PatentsPotato CommissionerNo ratings yet

- Final Term Assignment 2 On Financial Accounting and Reporting - Partnership OperationsDocument2 pagesFinal Term Assignment 2 On Financial Accounting and Reporting - Partnership OperationsAnne AlagNo ratings yet

- Chapter 2Document5 pagesChapter 2Sundaramani SaranNo ratings yet

- Summary Enhancing Qualitative CharacteristicsDocument3 pagesSummary Enhancing Qualitative CharacteristicsCahyani PrastutiNo ratings yet

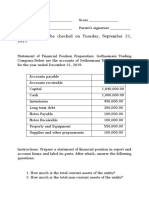

- Answer This To Be Checked On Tuesday, September 21, 2021Document2 pagesAnswer This To Be Checked On Tuesday, September 21, 2021Teresa Mae OrquiaNo ratings yet

- Welfare Effects of Perfect CompetitionDocument7 pagesWelfare Effects of Perfect CompetitionBoi NonoNo ratings yet

- Socio Economic AspectDocument3 pagesSocio Economic Aspect버니 모지코No ratings yet

- Background of The StudyDocument3 pagesBackground of The StudyRaman KapoorNo ratings yet

- Feasibility 11 13Document17 pagesFeasibility 11 13Eniam SotnasNo ratings yet

- Promissory NotesDocument7 pagesPromissory NotesJasper MenesesNo ratings yet

- We Have Studied The Different Ethical Principles in Our Search For The Morality of Human Acts. These Are The FollowingDocument3 pagesWe Have Studied The Different Ethical Principles in Our Search For The Morality of Human Acts. These Are The FollowingRosemarie CruzNo ratings yet

- Accountancy Quizbowl GuidelinesDocument4 pagesAccountancy Quizbowl GuidelinesMaria Kem EumagueNo ratings yet

- Module 1 Em3210Document13 pagesModule 1 Em3210Claire GigerNo ratings yet

- Service Rate 3 Minutes/call or 10 Calls/30 minutes/CSR Utilization (U) Demand Rate/ ( (Service Rate) (Number of Servers) )Document8 pagesService Rate 3 Minutes/call or 10 Calls/30 minutes/CSR Utilization (U) Demand Rate/ ( (Service Rate) (Number of Servers) )Nilisha DeshbhratarNo ratings yet

- FDNACCT - Quiz #1 - Set B - Answer KeyDocument4 pagesFDNACCT - Quiz #1 - Set B - Answer KeyIchi HasukiNo ratings yet

- Assignment - Intangible AssetDocument5 pagesAssignment - Intangible AssetJane DizonNo ratings yet

- Statistical TreatmentDocument9 pagesStatistical TreatmentCiv NortubNo ratings yet

- Quantitative Techniques ReviewerDocument3 pagesQuantitative Techniques ReviewerAstronomy SpacefieldNo ratings yet

- CHAPTER 1, 2, 3 and 4Document33 pagesCHAPTER 1, 2, 3 and 4Jobelle MalabananNo ratings yet

- FSA Group Assignment - Analysis of Caltex CompanyDocument22 pagesFSA Group Assignment - Analysis of Caltex CompanyĐạt Thành100% (1)

- Cindy Lota - Activity No. 3 - Statement of Financial PositionDocument6 pagesCindy Lota - Activity No. 3 - Statement of Financial PositionCindy LotaNo ratings yet

- I. Introduction To Managerial EconomicsDocument5 pagesI. Introduction To Managerial EconomicsJerico ManaloNo ratings yet

- Chapter 4 (Linear Programming: Formulation and Applications)Document30 pagesChapter 4 (Linear Programming: Formulation and Applications)ripeNo ratings yet

- Cash Flows ExercicesDocument96 pagesCash Flows ExercicesAbdelmajid JamaneNo ratings yet

- Financial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreDocument16 pagesFinancial Accounting and Reporting Iii (Reviewer) : Name: Date: Professor: Section: ScoreShane TorrieNo ratings yet

- Chapter 7 - Accounting For MaterialsDocument24 pagesChapter 7 - Accounting For MaterialsTim ParasNo ratings yet

- Group 5 Case AnalyzationDocument13 pagesGroup 5 Case AnalyzationChristine DiazNo ratings yet

- Ethics in The MarketplaceDocument19 pagesEthics in The Marketplacewsnarejo100% (1)

- Qualifying Exam Review Qs Final Answers2Document30 pagesQualifying Exam Review Qs Final Answers2sunq hccnNo ratings yet

- Current Liabilities and ProvisionsDocument12 pagesCurrent Liabilities and ProvisionsRinkashizu TokimimotakuNo ratings yet

- Cash FlowDocument2 pagesCash FlowJasmine ActaNo ratings yet

- IcebreakerDocument5 pagesIcebreakerRyan MagalangNo ratings yet

- Module A Answers Feb 2014Document27 pagesModule A Answers Feb 2014maha rehmanNo ratings yet

- TUTORIAL 2 Decision AnalysisDocument11 pagesTUTORIAL 2 Decision AnalysisKayy LaNo ratings yet

- Answer CHT 3 HWDocument7 pagesAnswer CHT 3 HWscamtesterNo ratings yet

- Women: Getting On BoardDocument2 pagesWomen: Getting On BoardLuqmanhakim XavNo ratings yet

- Malaysia 2003 Terrestrial Pilot Phase2Document58 pagesMalaysia 2003 Terrestrial Pilot Phase2Luqmanhakim XavNo ratings yet

- LDP2M2 BMPDocument2 pagesLDP2M2 BMPLuqmanhakim XavNo ratings yet

- Mal 54629Document19 pagesMal 54629Luqmanhakim XavNo ratings yet

- WWW - Pmu.edu - Sa: This Thumbdrive Is Proudly Sponsored byDocument1 pageWWW - Pmu.edu - Sa: This Thumbdrive Is Proudly Sponsored byLuqmanhakim XavNo ratings yet

- Install Autocad 2016Document1 pageInstall Autocad 2016Luqmanhakim XavNo ratings yet

- Personal Inventory TemplateDocument8 pagesPersonal Inventory TemplateLuqmanhakim XavNo ratings yet

- Check Course Registered (MYCLASS) : Step 1: Step 2Document4 pagesCheck Course Registered (MYCLASS) : Step 1: Step 2Luqmanhakim XavNo ratings yet

- 50-200LCE GMP ISO Batch Type Industrial Homogenizer/mixer/emulsifier Homogenizer-Mixer-Emulsifier/32299333634.html)Document3 pages50-200LCE GMP ISO Batch Type Industrial Homogenizer/mixer/emulsifier Homogenizer-Mixer-Emulsifier/32299333634.html)Luqmanhakim XavNo ratings yet

- Solution To Solved Problems: 1.S1 Make or BuyDocument3 pagesSolution To Solved Problems: 1.S1 Make or BuyLuqmanhakim XavNo ratings yet

- Cam For Bte 3215 Heat and Mass Transfer, Semi 14/15Document1 pageCam For Bte 3215 Heat and Mass Transfer, Semi 14/15Luqmanhakim XavNo ratings yet

- Chap 002 Intro To Management ScienceDocument4 pagesChap 002 Intro To Management ScienceLuqmanhakim XavNo ratings yet

- NOOR ZATI AMANI Protein MutantDocument1 pageNOOR ZATI AMANI Protein MutantLuqmanhakim XavNo ratings yet

- Forex Survival GuideDocument22 pagesForex Survival Guidevikki2810No ratings yet

- 2007-09-29 Every Soldier Is A SensorDocument5 pages2007-09-29 Every Soldier Is A SensorDozerMayneNo ratings yet

- Tacha's ReusmeDocument2 pagesTacha's ReusmeJames HamptonNo ratings yet

- Jetblue Airways: A New BeginningDocument25 pagesJetblue Airways: A New BeginningHesty Tri BudihartiNo ratings yet

- Michigan Strategic Compliance Plan FINALDocument22 pagesMichigan Strategic Compliance Plan FINALbcap-oceanNo ratings yet

- Proces CostingDocument14 pagesProces CostingKenDedesNo ratings yet

- The Preschooler and The SchoolerDocument16 pagesThe Preschooler and The Schoolerquidditch07No ratings yet

- Chebyshev Filter: Linear Analog Electronic FiltersDocument10 pagesChebyshev Filter: Linear Analog Electronic FiltersSri Jai PriyaNo ratings yet

- Volume AdministrationDocument264 pagesVolume AdministrationeviyipyipNo ratings yet

- Planificare Calendaristică Anuală Pentru Limba Modernă 1 - Studiu Intensiv. Engleză. Clasa A Vi-ADocument6 pagesPlanificare Calendaristică Anuală Pentru Limba Modernă 1 - Studiu Intensiv. Engleză. Clasa A Vi-Acatalina marinoiuNo ratings yet

- Higher Eng Maths 9th Ed 2021 Solutions ChapterDocument17 pagesHigher Eng Maths 9th Ed 2021 Solutions ChapterAubrey JosephNo ratings yet

- Solve The Problems: (1 Marks)Document7 pagesSolve The Problems: (1 Marks)Govin RocketzNo ratings yet

- Chechk List Fokker 50Document1 pageChechk List Fokker 50Felipe PinillaNo ratings yet

- Adam Izdebski & Michael Mulryan - Environment and Society in The Long LateDocument7 pagesAdam Izdebski & Michael Mulryan - Environment and Society in The Long Latecarlos murciaNo ratings yet

- Module 5 in Eed 114: ReviewDocument6 pagesModule 5 in Eed 114: ReviewYvi BenrayNo ratings yet

- Work Inspection Checklist: Project DetailsDocument1 pageWork Inspection Checklist: Project Detailsmark lester caluzaNo ratings yet

- Earth Dams Foundation & Earth Material InvestigationDocument111 pagesEarth Dams Foundation & Earth Material Investigationmustafurade1No ratings yet

- Exercise Oracle Forms 6i TrainingDocument5 pagesExercise Oracle Forms 6i TrainingFarooq Shahid100% (1)

- Noun (Subject) + Verb + The + Superlative Adjective + Noun (Object)Document6 pagesNoun (Subject) + Verb + The + Superlative Adjective + Noun (Object)anaNo ratings yet

- Linear Programming TheoryDocument104 pagesLinear Programming Theorykostas_ntougias5453No ratings yet

- Sspc-Ab 2Document3 pagesSspc-Ab 2HafidzManafNo ratings yet

- Modeling and Simulation of Fluid Catalytic Cracking Unit: Reviews in Chemical Engineering January 2005Document38 pagesModeling and Simulation of Fluid Catalytic Cracking Unit: Reviews in Chemical Engineering January 2005Diyar AliNo ratings yet

- Resistances, Voltages and Current in CircuitsDocument21 pagesResistances, Voltages and Current in CircuitsHisyamAl-MuhammadiNo ratings yet

- Pearl Brochure SinglePageScroll A4 New Claim Final 10 05.ENDocument8 pagesPearl Brochure SinglePageScroll A4 New Claim Final 10 05.ENlassanac85No ratings yet

- Assignment Activity On Expenditure Cycles - To Be ContinuedDocument3 pagesAssignment Activity On Expenditure Cycles - To Be ContinuedRico, Jalaica B.No ratings yet

- E4nb71 PDFDocument99 pagesE4nb71 PDFtambache69100% (1)

- Problem PipingDocument79 pagesProblem PipingSiddhi MhatreNo ratings yet