The Bulletproof Portfolio NYC

The Bulletproof Portfolio NYC

You might also like

- Least Mastered Competencies (Grade 6)Document14 pagesLeast Mastered Competencies (Grade 6)Renge Taña91% (33)

- Portfolio Investment ReportDocument27 pagesPortfolio Investment ReportSowmya04No ratings yet

- AQR Alternative Thinking 3Q15Document12 pagesAQR Alternative Thinking 3Q15moonNo ratings yet

- Neelay Both PartsDocument5 pagesNeelay Both PartsHaute Femme AttractionNo ratings yet

- Elton-Are Investors Rational 1Document36 pagesElton-Are Investors Rational 1Abey FrancisNo ratings yet

- Comparison of Five Popular StrategiesDocument12 pagesComparison of Five Popular StrategiesNam Dang ThanhNo ratings yet

- Adaptive Asset AllocationDocument14 pagesAdaptive Asset AllocationQuasiNo ratings yet

- Security Bank - UITF Investment ReportDocument2 pagesSecurity Bank - UITF Investment ReportgwapongkabayoNo ratings yet

- First Q Uarter R Eport 2010Document16 pagesFirst Q Uarter R Eport 2010richardck20No ratings yet

- Prepared By: Bhavin Patel Piyush Radadiya: Comparatives Study of Performance of Mutual Funds Companies in IndiaDocument19 pagesPrepared By: Bhavin Patel Piyush Radadiya: Comparatives Study of Performance of Mutual Funds Companies in Indiapatel2431No ratings yet

- Full Download Running Money Professional Portfolio Management 1st Edition Stewart Solutions ManualDocument36 pagesFull Download Running Money Professional Portfolio Management 1st Edition Stewart Solutions Manualwigibsoncd3f100% (30)

- Investment and Portfolio Management Chapter 1 (AN OVERVIEW OF THE INVESTMENT PROCESS)Document28 pagesInvestment and Portfolio Management Chapter 1 (AN OVERVIEW OF THE INVESTMENT PROCESS)Star AragonNo ratings yet

- Asset Allocation and Tactical Asset AllocationDocument16 pagesAsset Allocation and Tactical Asset AllocationGabriel ManjonjoNo ratings yet

- Gary Antonacci - Momentum Success Factors (2012)Document33 pagesGary Antonacci - Momentum Success Factors (2012)johnetownsendNo ratings yet

- Fin Term PaperDocument15 pagesFin Term PaperFarjana Yasmin RumiNo ratings yet

- SBI Mutual FundsDocument17 pagesSBI Mutual FundsphaniNo ratings yet

- The Long and Short of Market Neutral Investing: Investment InsightsDocument4 pagesThe Long and Short of Market Neutral Investing: Investment Insightsmkmanish1No ratings yet

- A Sleep Well Bond Rotation Strategy With 15 Percent Annualized Return Since 2008Document4 pagesA Sleep Well Bond Rotation Strategy With 15 Percent Annualized Return Since 2008Logical InvestNo ratings yet

- Shikhar Sharma Theswedishinvestor Iag1-HmmDocument5 pagesShikhar Sharma Theswedishinvestor Iag1-HmmresourcesficNo ratings yet

- Long Term InvestingDocument8 pagesLong Term InvestingkrishchellaNo ratings yet

- Tilson Funds Annual Report 2005Document28 pagesTilson Funds Annual Report 2005josepmcdalena6542No ratings yet

- Sample ChapterDocument39 pagesSample ChapterMaxwell KozakNo ratings yet

- Bhavesh Sawant Bhuvan DalviDocument8 pagesBhavesh Sawant Bhuvan DalviBhuvan DalviNo ratings yet

- 5 Investment Books For 2021Document4 pages5 Investment Books For 2021Yassine MafraxNo ratings yet

- Security and Portfolio Management Answer.Document7 pagesSecurity and Portfolio Management Answer.ttwahirwa100% (3)

- Portfolio Management Anshu, Jagriti, Mahima, DheryaDocument15 pagesPortfolio Management Anshu, Jagriti, Mahima, DheryaMahima BhatnagarNo ratings yet

- Comparative Analysis of Investment Alternatives: Personal Financial PlanningDocument12 pagesComparative Analysis of Investment Alternatives: Personal Financial Planningwish_coolalok8995No ratings yet

- Spam Unit 1-5Document84 pagesSpam Unit 1-5kaipulla1234567No ratings yet

- MF0010 Set1 Q1& 2Document5 pagesMF0010 Set1 Q1& 2s_konarNo ratings yet

- Q2 2015 KAM Conference Call 07-07-15 FINALDocument18 pagesQ2 2015 KAM Conference Call 07-07-15 FINALCanadianValueNo ratings yet

- Empower July 2011Document74 pagesEmpower July 2011Priyanka AroraNo ratings yet

- Mutaul Fund PresentationDocument28 pagesMutaul Fund PresentationAshwani MittalNo ratings yet

- The Little BookDocument7 pagesThe Little BookGaurav ChhibbaNo ratings yet

- Master in Business Administration - Semester 3 MF0010 - Security Analysis and Portfolio Management - 4 Credits Assignment Set-1 (60 Marks)Document11 pagesMaster in Business Administration - Semester 3 MF0010 - Security Analysis and Portfolio Management - 4 Credits Assignment Set-1 (60 Marks)Sumit ChhuganiNo ratings yet

- IDFC Emergin Businesses NFODocument5 pagesIDFC Emergin Businesses NFOfinancialbondingNo ratings yet

- Assignment Sample 1Document30 pagesAssignment Sample 1Sujäń ShähíNo ratings yet

- Dollar Cost Averaging vs. Lump Sum Investing: Benjamin FelixDocument17 pagesDollar Cost Averaging vs. Lump Sum Investing: Benjamin FelixCláudioNo ratings yet

- Investment Triangle - Three Compromising ObjectivesDocument23 pagesInvestment Triangle - Three Compromising ObjectivesmakkasssNo ratings yet

- Lecture 6 ScriptDocument3 pagesLecture 6 ScriptAshish MalhotraNo ratings yet

- Risk and Return AnalysisDocument38 pagesRisk and Return AnalysisAshwini Pawar100% (1)

- Anish Tawakley, Rajat Chandak, and The Elite Team of Managers at The Icici Prudential Mutal FundDocument3 pagesAnish Tawakley, Rajat Chandak, and The Elite Team of Managers at The Icici Prudential Mutal FundRadhika AgrawalNo ratings yet

- Steven Romick September 30, 2010Document13 pagesSteven Romick September 30, 2010eric695No ratings yet

- ChapterDocument90 pagesChapterRavi SharmaNo ratings yet

- Case For High Conviction InvestingDocument2 pagesCase For High Conviction Investingkenneth1195No ratings yet

- DAY 3 Mutual Fund Presentation ShrutiDocument20 pagesDAY 3 Mutual Fund Presentation ShrutiArushi GuptaNo ratings yet

- Portfolio ManagementDocument9 pagesPortfolio ManagementAvinaw KumarNo ratings yet

- Value or Growth Stocks Which Is BetterDocument4 pagesValue or Growth Stocks Which Is BetterCalvin YeohNo ratings yet

- R. Driehaus, Unconventional Wisdom in The Investment ProcessDocument6 pagesR. Driehaus, Unconventional Wisdom in The Investment Processbagelboy2No ratings yet

- Doshi Gama Fund April 2013Document2 pagesDoshi Gama Fund April 2013ados1984No ratings yet

- Mark Yusko Q2 LetterDocument47 pagesMark Yusko Q2 LetterValueWalkNo ratings yet

- Cia - 3a PDFDocument8 pagesCia - 3a PDFAyush SarawagiNo ratings yet

- Mi Bill Eigen Mid Year Outlook1Document6 pagesMi Bill Eigen Mid Year Outlook1nievinnyNo ratings yet

- 10 Rules For Successful Long-Term InvestingDocument8 pages10 Rules For Successful Long-Term InvestingPGM5HNo ratings yet

- Role of Asset Allocation in Portfolio ManagementDocument10 pagesRole of Asset Allocation in Portfolio ManagementAbhijeet PatilNo ratings yet

- Advancement in Portfolio Construction: P/E RatioDocument7 pagesAdvancement in Portfolio Construction: P/E RatioAyush SarawagiNo ratings yet

- Executive Summary: TH NDDocument20 pagesExecutive Summary: TH NDRocky MahmudNo ratings yet

- Background of The Investor: Ketki Prabhat Roll No:44Document4 pagesBackground of The Investor: Ketki Prabhat Roll No:44Santosh KardakNo ratings yet

- Advisorkhoj Mirae Asset Mutual Fund ArticleDocument6 pagesAdvisorkhoj Mirae Asset Mutual Fund ArticleSowmya GuptaNo ratings yet

- Portfolio Management - Part 2: Portfolio Management, #2From EverandPortfolio Management - Part 2: Portfolio Management, #2Rating: 5 out of 5 stars5/5 (9)

- Timing the Markets: Unemotional Approaches to Making Buy & Sell Decisions in MarketsFrom EverandTiming the Markets: Unemotional Approaches to Making Buy & Sell Decisions in MarketsNo ratings yet

- Accounting For Managers: S. No. Questions 1Document5 pagesAccounting For Managers: S. No. Questions 1shilpa mishraNo ratings yet

- Teacher Newsletter TemplateDocument1 pageTeacher Newsletter TemplateHart LJNo ratings yet

- Unit 14 - Unemployment and Fiscal Policy - 1.0Document41 pagesUnit 14 - Unemployment and Fiscal Policy - 1.0Georgius Yeremia CandraNo ratings yet

- Schedule CDocument273 pagesSchedule CAzi PaybarahNo ratings yet

- Pengkarya Muda - Aliah BiDocument7 pagesPengkarya Muda - Aliah BiNORHASLIZA BINTI MOHAMAD MoeNo ratings yet

- Shaping The Way We Teach English:: Successful Practices Around The WorldDocument5 pagesShaping The Way We Teach English:: Successful Practices Around The WorldCristina DiaconuNo ratings yet

- Russian General Speaks Out On UFOsDocument7 pagesRussian General Speaks Out On UFOsochaerryNo ratings yet

- Not in His Image (15th Anniversary Edition) - Preface and IntroDocument17 pagesNot in His Image (15th Anniversary Edition) - Preface and IntroChelsea Green PublishingNo ratings yet

- GIS Based Analysis On Walkability of Commercial Streets at Continuing Growth Stages - EditedDocument11 pagesGIS Based Analysis On Walkability of Commercial Streets at Continuing Growth Stages - EditedemmanuelNo ratings yet

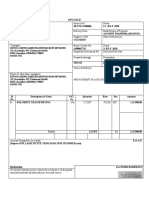

- Invoice: Qrt. No - : Cc-15, Civil Township Rourkela, Dist - (Sundargarh (Odisha) - 769012 GSTIN - 21ACWFS2234G1Z4Document2 pagesInvoice: Qrt. No - : Cc-15, Civil Township Rourkela, Dist - (Sundargarh (Odisha) - 769012 GSTIN - 21ACWFS2234G1Z4PUNYASHLOK PANDANo ratings yet

- Manual Mycom InglêsDocument158 pagesManual Mycom InglêsJorge Palinkas100% (1)

- Human Resource Management PrelimsDocument2 pagesHuman Resource Management PrelimsLei PalumponNo ratings yet

- Intro To ForsciDocument16 pagesIntro To ForsciChloe MaciasNo ratings yet

- Trial in AbsentiaDocument12 pagesTrial in AbsentiaNahid hossainNo ratings yet

- History of The Stanford Watershed Model PDFDocument3 pagesHistory of The Stanford Watershed Model PDFchindy adsariaNo ratings yet

- Past Simple Weekend.m4aDocument7 pagesPast Simple Weekend.m4aCarmen Victoria Niño RamosNo ratings yet

- Babst Vs CA PDFDocument17 pagesBabst Vs CA PDFJustin YañezNo ratings yet

- Installation, Operation and Maintenance Manual: Rotoclone LVNDocument23 pagesInstallation, Operation and Maintenance Manual: Rotoclone LVNbertan dağıstanlıNo ratings yet

- HCI634K - Technical Data SheetDocument8 pagesHCI634K - Technical Data SheetQuynhNo ratings yet

- British Baker Top Bakery Trends 2023Document15 pagesBritish Baker Top Bakery Trends 2023kiagus artaNo ratings yet

- Mindanao Geothermal v. CIRDocument22 pagesMindanao Geothermal v. CIRMarchini Sandro Cañizares KongNo ratings yet

- Data Sheets Ecc I On AdoraDocument23 pagesData Sheets Ecc I On AdoraAlanAvtoNo ratings yet

- Ferdinando Carulli - Op 121, 24 Pieces - 4. Anglaise in A MajorDocument2 pagesFerdinando Carulli - Op 121, 24 Pieces - 4. Anglaise in A MajorOniscoidNo ratings yet

- Study of Blood Groups and Rhesus Factor in Beta Thalassemia Patients Undergoing Blood TransfusionsDocument6 pagesStudy of Blood Groups and Rhesus Factor in Beta Thalassemia Patients Undergoing Blood TransfusionsOpenaccess Research paperNo ratings yet

- Asfwa Report2008 PDFDocument4 pagesAsfwa Report2008 PDFMesfin DerbewNo ratings yet

- Product Data Sheet Ingenuity Core LRDocument16 pagesProduct Data Sheet Ingenuity Core LRCeoĐứcTrườngNo ratings yet

- Informative Essays TopicsDocument9 pagesInformative Essays Topicsb725c62j100% (2)

- UnpublishedDocument7 pagesUnpublishedScribd Government DocsNo ratings yet

- Chinas Legal Strategy To Cope With US Export ContDocument9 pagesChinas Legal Strategy To Cope With US Export Contb19fd0013No ratings yet

Download as docx, pdf, or txt

You might also like

- Least Mastered Competencies (Grade 6)Document14 pagesLeast Mastered Competencies (Grade 6)Renge Taña91% (33)

- Portfolio Investment ReportDocument27 pagesPortfolio Investment ReportSowmya04No ratings yet

- AQR Alternative Thinking 3Q15Document12 pagesAQR Alternative Thinking 3Q15moonNo ratings yet

- Neelay Both PartsDocument5 pagesNeelay Both PartsHaute Femme AttractionNo ratings yet

- Elton-Are Investors Rational 1Document36 pagesElton-Are Investors Rational 1Abey FrancisNo ratings yet

- Comparison of Five Popular StrategiesDocument12 pagesComparison of Five Popular StrategiesNam Dang ThanhNo ratings yet

- Adaptive Asset AllocationDocument14 pagesAdaptive Asset AllocationQuasiNo ratings yet

- Security Bank - UITF Investment ReportDocument2 pagesSecurity Bank - UITF Investment ReportgwapongkabayoNo ratings yet

- First Q Uarter R Eport 2010Document16 pagesFirst Q Uarter R Eport 2010richardck20No ratings yet

- Prepared By: Bhavin Patel Piyush Radadiya: Comparatives Study of Performance of Mutual Funds Companies in IndiaDocument19 pagesPrepared By: Bhavin Patel Piyush Radadiya: Comparatives Study of Performance of Mutual Funds Companies in Indiapatel2431No ratings yet

- Full Download Running Money Professional Portfolio Management 1st Edition Stewart Solutions ManualDocument36 pagesFull Download Running Money Professional Portfolio Management 1st Edition Stewart Solutions Manualwigibsoncd3f100% (30)

- Investment and Portfolio Management Chapter 1 (AN OVERVIEW OF THE INVESTMENT PROCESS)Document28 pagesInvestment and Portfolio Management Chapter 1 (AN OVERVIEW OF THE INVESTMENT PROCESS)Star AragonNo ratings yet

- Asset Allocation and Tactical Asset AllocationDocument16 pagesAsset Allocation and Tactical Asset AllocationGabriel ManjonjoNo ratings yet

- Gary Antonacci - Momentum Success Factors (2012)Document33 pagesGary Antonacci - Momentum Success Factors (2012)johnetownsendNo ratings yet

- Fin Term PaperDocument15 pagesFin Term PaperFarjana Yasmin RumiNo ratings yet

- SBI Mutual FundsDocument17 pagesSBI Mutual FundsphaniNo ratings yet

- The Long and Short of Market Neutral Investing: Investment InsightsDocument4 pagesThe Long and Short of Market Neutral Investing: Investment Insightsmkmanish1No ratings yet

- A Sleep Well Bond Rotation Strategy With 15 Percent Annualized Return Since 2008Document4 pagesA Sleep Well Bond Rotation Strategy With 15 Percent Annualized Return Since 2008Logical InvestNo ratings yet

- Shikhar Sharma Theswedishinvestor Iag1-HmmDocument5 pagesShikhar Sharma Theswedishinvestor Iag1-HmmresourcesficNo ratings yet

- Long Term InvestingDocument8 pagesLong Term InvestingkrishchellaNo ratings yet

- Tilson Funds Annual Report 2005Document28 pagesTilson Funds Annual Report 2005josepmcdalena6542No ratings yet

- Sample ChapterDocument39 pagesSample ChapterMaxwell KozakNo ratings yet

- Bhavesh Sawant Bhuvan DalviDocument8 pagesBhavesh Sawant Bhuvan DalviBhuvan DalviNo ratings yet

- 5 Investment Books For 2021Document4 pages5 Investment Books For 2021Yassine MafraxNo ratings yet

- Security and Portfolio Management Answer.Document7 pagesSecurity and Portfolio Management Answer.ttwahirwa100% (3)

- Portfolio Management Anshu, Jagriti, Mahima, DheryaDocument15 pagesPortfolio Management Anshu, Jagriti, Mahima, DheryaMahima BhatnagarNo ratings yet

- Comparative Analysis of Investment Alternatives: Personal Financial PlanningDocument12 pagesComparative Analysis of Investment Alternatives: Personal Financial Planningwish_coolalok8995No ratings yet

- Spam Unit 1-5Document84 pagesSpam Unit 1-5kaipulla1234567No ratings yet

- MF0010 Set1 Q1& 2Document5 pagesMF0010 Set1 Q1& 2s_konarNo ratings yet

- Q2 2015 KAM Conference Call 07-07-15 FINALDocument18 pagesQ2 2015 KAM Conference Call 07-07-15 FINALCanadianValueNo ratings yet

- Empower July 2011Document74 pagesEmpower July 2011Priyanka AroraNo ratings yet

- Mutaul Fund PresentationDocument28 pagesMutaul Fund PresentationAshwani MittalNo ratings yet

- The Little BookDocument7 pagesThe Little BookGaurav ChhibbaNo ratings yet

- Master in Business Administration - Semester 3 MF0010 - Security Analysis and Portfolio Management - 4 Credits Assignment Set-1 (60 Marks)Document11 pagesMaster in Business Administration - Semester 3 MF0010 - Security Analysis and Portfolio Management - 4 Credits Assignment Set-1 (60 Marks)Sumit ChhuganiNo ratings yet

- IDFC Emergin Businesses NFODocument5 pagesIDFC Emergin Businesses NFOfinancialbondingNo ratings yet

- Assignment Sample 1Document30 pagesAssignment Sample 1Sujäń ShähíNo ratings yet

- Dollar Cost Averaging vs. Lump Sum Investing: Benjamin FelixDocument17 pagesDollar Cost Averaging vs. Lump Sum Investing: Benjamin FelixCláudioNo ratings yet

- Investment Triangle - Three Compromising ObjectivesDocument23 pagesInvestment Triangle - Three Compromising ObjectivesmakkasssNo ratings yet

- Lecture 6 ScriptDocument3 pagesLecture 6 ScriptAshish MalhotraNo ratings yet

- Risk and Return AnalysisDocument38 pagesRisk and Return AnalysisAshwini Pawar100% (1)

- Anish Tawakley, Rajat Chandak, and The Elite Team of Managers at The Icici Prudential Mutal FundDocument3 pagesAnish Tawakley, Rajat Chandak, and The Elite Team of Managers at The Icici Prudential Mutal FundRadhika AgrawalNo ratings yet

- Steven Romick September 30, 2010Document13 pagesSteven Romick September 30, 2010eric695No ratings yet

- ChapterDocument90 pagesChapterRavi SharmaNo ratings yet

- Case For High Conviction InvestingDocument2 pagesCase For High Conviction Investingkenneth1195No ratings yet

- DAY 3 Mutual Fund Presentation ShrutiDocument20 pagesDAY 3 Mutual Fund Presentation ShrutiArushi GuptaNo ratings yet

- Portfolio ManagementDocument9 pagesPortfolio ManagementAvinaw KumarNo ratings yet

- Value or Growth Stocks Which Is BetterDocument4 pagesValue or Growth Stocks Which Is BetterCalvin YeohNo ratings yet

- R. Driehaus, Unconventional Wisdom in The Investment ProcessDocument6 pagesR. Driehaus, Unconventional Wisdom in The Investment Processbagelboy2No ratings yet

- Doshi Gama Fund April 2013Document2 pagesDoshi Gama Fund April 2013ados1984No ratings yet

- Mark Yusko Q2 LetterDocument47 pagesMark Yusko Q2 LetterValueWalkNo ratings yet

- Cia - 3a PDFDocument8 pagesCia - 3a PDFAyush SarawagiNo ratings yet

- Mi Bill Eigen Mid Year Outlook1Document6 pagesMi Bill Eigen Mid Year Outlook1nievinnyNo ratings yet

- 10 Rules For Successful Long-Term InvestingDocument8 pages10 Rules For Successful Long-Term InvestingPGM5HNo ratings yet

- Role of Asset Allocation in Portfolio ManagementDocument10 pagesRole of Asset Allocation in Portfolio ManagementAbhijeet PatilNo ratings yet

- Advancement in Portfolio Construction: P/E RatioDocument7 pagesAdvancement in Portfolio Construction: P/E RatioAyush SarawagiNo ratings yet

- Executive Summary: TH NDDocument20 pagesExecutive Summary: TH NDRocky MahmudNo ratings yet

- Background of The Investor: Ketki Prabhat Roll No:44Document4 pagesBackground of The Investor: Ketki Prabhat Roll No:44Santosh KardakNo ratings yet

- Advisorkhoj Mirae Asset Mutual Fund ArticleDocument6 pagesAdvisorkhoj Mirae Asset Mutual Fund ArticleSowmya GuptaNo ratings yet

- Portfolio Management - Part 2: Portfolio Management, #2From EverandPortfolio Management - Part 2: Portfolio Management, #2Rating: 5 out of 5 stars5/5 (9)

- Timing the Markets: Unemotional Approaches to Making Buy & Sell Decisions in MarketsFrom EverandTiming the Markets: Unemotional Approaches to Making Buy & Sell Decisions in MarketsNo ratings yet

- Accounting For Managers: S. No. Questions 1Document5 pagesAccounting For Managers: S. No. Questions 1shilpa mishraNo ratings yet

- Teacher Newsletter TemplateDocument1 pageTeacher Newsletter TemplateHart LJNo ratings yet

- Unit 14 - Unemployment and Fiscal Policy - 1.0Document41 pagesUnit 14 - Unemployment and Fiscal Policy - 1.0Georgius Yeremia CandraNo ratings yet

- Schedule CDocument273 pagesSchedule CAzi PaybarahNo ratings yet

- Pengkarya Muda - Aliah BiDocument7 pagesPengkarya Muda - Aliah BiNORHASLIZA BINTI MOHAMAD MoeNo ratings yet

- Shaping The Way We Teach English:: Successful Practices Around The WorldDocument5 pagesShaping The Way We Teach English:: Successful Practices Around The WorldCristina DiaconuNo ratings yet

- Russian General Speaks Out On UFOsDocument7 pagesRussian General Speaks Out On UFOsochaerryNo ratings yet

- Not in His Image (15th Anniversary Edition) - Preface and IntroDocument17 pagesNot in His Image (15th Anniversary Edition) - Preface and IntroChelsea Green PublishingNo ratings yet

- GIS Based Analysis On Walkability of Commercial Streets at Continuing Growth Stages - EditedDocument11 pagesGIS Based Analysis On Walkability of Commercial Streets at Continuing Growth Stages - EditedemmanuelNo ratings yet

- Invoice: Qrt. No - : Cc-15, Civil Township Rourkela, Dist - (Sundargarh (Odisha) - 769012 GSTIN - 21ACWFS2234G1Z4Document2 pagesInvoice: Qrt. No - : Cc-15, Civil Township Rourkela, Dist - (Sundargarh (Odisha) - 769012 GSTIN - 21ACWFS2234G1Z4PUNYASHLOK PANDANo ratings yet

- Manual Mycom InglêsDocument158 pagesManual Mycom InglêsJorge Palinkas100% (1)

- Human Resource Management PrelimsDocument2 pagesHuman Resource Management PrelimsLei PalumponNo ratings yet

- Intro To ForsciDocument16 pagesIntro To ForsciChloe MaciasNo ratings yet

- Trial in AbsentiaDocument12 pagesTrial in AbsentiaNahid hossainNo ratings yet

- History of The Stanford Watershed Model PDFDocument3 pagesHistory of The Stanford Watershed Model PDFchindy adsariaNo ratings yet

- Past Simple Weekend.m4aDocument7 pagesPast Simple Weekend.m4aCarmen Victoria Niño RamosNo ratings yet

- Babst Vs CA PDFDocument17 pagesBabst Vs CA PDFJustin YañezNo ratings yet

- Installation, Operation and Maintenance Manual: Rotoclone LVNDocument23 pagesInstallation, Operation and Maintenance Manual: Rotoclone LVNbertan dağıstanlıNo ratings yet

- HCI634K - Technical Data SheetDocument8 pagesHCI634K - Technical Data SheetQuynhNo ratings yet

- British Baker Top Bakery Trends 2023Document15 pagesBritish Baker Top Bakery Trends 2023kiagus artaNo ratings yet

- Mindanao Geothermal v. CIRDocument22 pagesMindanao Geothermal v. CIRMarchini Sandro Cañizares KongNo ratings yet

- Data Sheets Ecc I On AdoraDocument23 pagesData Sheets Ecc I On AdoraAlanAvtoNo ratings yet

- Ferdinando Carulli - Op 121, 24 Pieces - 4. Anglaise in A MajorDocument2 pagesFerdinando Carulli - Op 121, 24 Pieces - 4. Anglaise in A MajorOniscoidNo ratings yet

- Study of Blood Groups and Rhesus Factor in Beta Thalassemia Patients Undergoing Blood TransfusionsDocument6 pagesStudy of Blood Groups and Rhesus Factor in Beta Thalassemia Patients Undergoing Blood TransfusionsOpenaccess Research paperNo ratings yet

- Asfwa Report2008 PDFDocument4 pagesAsfwa Report2008 PDFMesfin DerbewNo ratings yet

- Product Data Sheet Ingenuity Core LRDocument16 pagesProduct Data Sheet Ingenuity Core LRCeoĐứcTrườngNo ratings yet

- Informative Essays TopicsDocument9 pagesInformative Essays Topicsb725c62j100% (2)

- UnpublishedDocument7 pagesUnpublishedScribd Government DocsNo ratings yet

- Chinas Legal Strategy To Cope With US Export ContDocument9 pagesChinas Legal Strategy To Cope With US Export Contb19fd0013No ratings yet