Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- LTI Smart MoneyDocument26 pagesLTI Smart Moneyy6bt25096% (53)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Pay PalDocument30 pagesPay PalTarik El Fehri100% (1)

- Nonprofit Insider: What Is Your Form 990 Telling The IRS?Document2 pagesNonprofit Insider: What Is Your Form 990 Telling The IRS?UHYColumbiaMDNo ratings yet

- UHY Not-for-Profit Newsletter - August 2013Document2 pagesUHY Not-for-Profit Newsletter - August 2013UHYColumbiaMDNo ratings yet

- UHY Not-For-Profit Newsletter - August 2012Document2 pagesUHY Not-For-Profit Newsletter - August 2012UHYColumbiaMDNo ratings yet

- Nonprofit Insider: Plan Sponsors, Are You Ready For The New Regulations?Document2 pagesNonprofit Insider: Plan Sponsors, Are You Ready For The New Regulations?UHYColumbiaMDNo ratings yet

- Insider: Plan Sponsors, Are You Ready For The New Regulations?Document2 pagesInsider: Plan Sponsors, Are You Ready For The New Regulations?UHYColumbiaMDNo ratings yet

- UHY Not-For-Profit Newsletter - March 2012Document2 pagesUHY Not-For-Profit Newsletter - March 2012UHYColumbiaMDNo ratings yet

- UHY Government Contractor Newsletter - November 2011Document2 pagesUHY Government Contractor Newsletter - November 2011UHYColumbiaMD100% (1)

- UHY Not-for-Profit Newsletter - November 2011Document2 pagesUHY Not-for-Profit Newsletter - November 2011UHYColumbiaMDNo ratings yet

- UHY Government Contractor Newsletter - September 2011Document2 pagesUHY Government Contractor Newsletter - September 2011UHYColumbiaMDNo ratings yet

- UHY Not-for-Profit Newsletter - August 2011Document2 pagesUHY Not-for-Profit Newsletter - August 2011UHYColumbiaMDNo ratings yet

- UHY Financial Managment Newsletter - February 2011Document2 pagesUHY Financial Managment Newsletter - February 2011UHYColumbiaMDNo ratings yet

- UHY Government Contractor Newsletter - January 2011Document2 pagesUHY Government Contractor Newsletter - January 2011UHYColumbiaMDNo ratings yet

- UHY Construction Newsletter - February 2011Document2 pagesUHY Construction Newsletter - February 2011UHYColumbiaMDNo ratings yet

- UHY Not-for-Profit Newsletter - March 2011Document2 pagesUHY Not-for-Profit Newsletter - March 2011UHYColumbiaMDNo ratings yet

- UHY Not-for-Profit Newsletter - December 2010Document2 pagesUHY Not-for-Profit Newsletter - December 2010UHYColumbiaMDNo ratings yet

- UHY Government Contractor Newsletter - February 2011Document2 pagesUHY Government Contractor Newsletter - February 2011UHYColumbiaMDNo ratings yet

- 95 AFAR Final PreboardDocument19 pages95 AFAR Final Preboard20100723No ratings yet

- 3.G.R. No. 103092Document5 pages3.G.R. No. 103092Lord AumarNo ratings yet

- Indicadores 2023 08Document21 pagesIndicadores 2023 08Maria Fernanda TrigoNo ratings yet

- Maths Project On Home BudgetDocument10 pagesMaths Project On Home BudgetKatyayni KohliNo ratings yet

- Test Bank For Risk Management and Insurance 12th Edition James S TrieschmannDocument24 pagesTest Bank For Risk Management and Insurance 12th Edition James S TrieschmannGeorgeWangeprm100% (44)

- Advanced Financial Accounting 8th Edition Baker Test Bank Full Chapter PDFDocument67 pagesAdvanced Financial Accounting 8th Edition Baker Test Bank Full Chapter PDFsahebmostwhatgr91100% (14)

- Pangasinan State University: Housing and Human SettlementsDocument21 pagesPangasinan State University: Housing and Human SettlementsMarinelle MejiaNo ratings yet

- 3 PDFDocument4 pages3 PDFClaude WarwickNo ratings yet

- TAXABLE INCOME ReportDocument6 pagesTAXABLE INCOME ReportTrudgeOnNo ratings yet

- Organization Study On Canara BankDocument77 pagesOrganization Study On Canara Bankmokshasinchana0% (2)

- BPI02 - BPI Payroll Waiver Form (Annex A)Document1 pageBPI02 - BPI Payroll Waiver Form (Annex A)Icelle IsideraNo ratings yet

- Essays in Taxation and International Relations PDFDocument74 pagesEssays in Taxation and International Relations PDFtishamadalinaNo ratings yet

- Interview Case Study 2 - Strategic Commodity SpecialistDocument5 pagesInterview Case Study 2 - Strategic Commodity SpecialisttalytaamorimNo ratings yet

- Gov. Bruce Rauner's 2018 Statement of Economic InterestDocument11 pagesGov. Bruce Rauner's 2018 Statement of Economic InterestMitch ArmentroutNo ratings yet

- The Silicon Valley Bank Crisis British English StudentDocument8 pagesThe Silicon Valley Bank Crisis British English StudentTrang DoNo ratings yet

- The Future of EverythingDocument216 pagesThe Future of EverythingKanchai Keeratikamon100% (1)

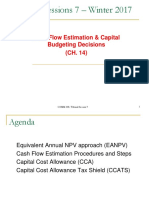

- m308 Tutorial7 Capitalbudgeting Solutions Winter17Document44 pagesm308 Tutorial7 Capitalbudgeting Solutions Winter17hyphensNo ratings yet

- Ocean Carriers Case StudyDocument7 pagesOcean Carriers Case Studyaida100% (1)

- Diversification StrategyDocument13 pagesDiversification StrategyitsmrcoolpbNo ratings yet

- Textile Policy Govt of Maharashtra 2011-2017Document31 pagesTextile Policy Govt of Maharashtra 2011-2017Pradeep AhireNo ratings yet

- Derivatives: Swap Markets and ContractsDocument19 pagesDerivatives: Swap Markets and ContractsDEVINo ratings yet

- Monetary Policy and Money Supply Process-Aminul IslamDocument89 pagesMonetary Policy and Money Supply Process-Aminul IslamHelal Uddin50% (2)

- Makerere UniversityDocument37 pagesMakerere UniversityGuerrero MetrashNo ratings yet

- TMOBILE - Soft Offer Sheet (Signed)Document1 pageTMOBILE - Soft Offer Sheet (Signed)Jarro Dela TorreNo ratings yet

- Pchome PresentationDocument38 pagesPchome Presentationecommerce zenNo ratings yet

- Full Download Test Bank For Portfolio Construction Management and Protection 5th Edition Strong PDF Full ChapterDocument35 pagesFull Download Test Bank For Portfolio Construction Management and Protection 5th Edition Strong PDF Full Chaptershaps.tortillayf3th100% (27)

- Unit 1 VocabularyDocument4 pagesUnit 1 VocabularyAlice NguyenNo ratings yet

- 1 Step - General JournalDocument27 pages1 Step - General JournalAiman qayyumNo ratings yet