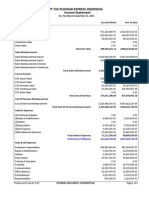

Valuation Final

Valuation Final

You might also like

- Worldcom Financials 2000 2002 ADocument5 pagesWorldcom Financials 2000 2002 AmominNo ratings yet

- Chapter16.Capital Expenditure DecisionsDocument44 pagesChapter16.Capital Expenditure DecisionsErdjol Yzeiri63% (8)

- Tutorial FIN645 PYQDocument2 pagesTutorial FIN645 PYQJuu Scully DavidNo ratings yet

- MU PLC Annual Report 2002 Financial StatementsDocument21 pagesMU PLC Annual Report 2002 Financial StatementsNurlisaAlnyNo ratings yet

- ST Aerospace Financial ReportDocument4 pagesST Aerospace Financial ReportMuhammad FirdausNo ratings yet

- Airthread Connections NidaDocument15 pagesAirthread Connections NidaNidaParveen100% (1)

- Taxation AnswerDocument13 pagesTaxation AnswerkannadhassNo ratings yet

- AirThread G015Document6 pagesAirThread G015sahildharhakim83% (6)

- Chapter 2 Payroll Accounting 2018Document53 pagesChapter 2 Payroll Accounting 2018Gabi Mihalek100% (1)

- Accounting PretestDocument4 pagesAccounting PretestseymourwardNo ratings yet

- 2010 Ibm StatementsDocument6 pages2010 Ibm StatementsElsa MersiniNo ratings yet

- Financial Statements Review Q4 2010Document17 pagesFinancial Statements Review Q4 2010sahaiakkiNo ratings yet

- Net Income Attributable To Noncontrolling Interest Net Income (Loss) Attributable To VerizonDocument9 pagesNet Income Attributable To Noncontrolling Interest Net Income (Loss) Attributable To VerizonvenkeeeeeNo ratings yet

- Financial Statements PDFDocument91 pagesFinancial Statements PDFHolmes MusclesFanNo ratings yet

- Income Taxes (Excluding The Synthetic Fuel Segment)Document8 pagesIncome Taxes (Excluding The Synthetic Fuel Segment)butterflygigglesNo ratings yet

- Q1 FY2013 InvestorsDocument28 pagesQ1 FY2013 InvestorsRajesh NaiduNo ratings yet

- Equity ValuationDocument2,424 pagesEquity ValuationMuteeb Raina0% (1)

- Macys 2011 10kDocument39 pagesMacys 2011 10kapb5223No ratings yet

- Kunci Jawaban Black and WhiteDocument18 pagesKunci Jawaban Black and WhitefebrythiodorNo ratings yet

- Result Y15 Doc4Document28 pagesResult Y15 Doc4ashokdb2kNo ratings yet

- MCB Consolidated For Year Ended Dec 2011Document87 pagesMCB Consolidated For Year Ended Dec 2011shoaibjeeNo ratings yet

- IT Return IT1 WithAnnexure 23454434Document3 pagesIT Return IT1 WithAnnexure 23454434khurramacaaNo ratings yet

- Profit&Loss May 2010Document2 pagesProfit&Loss May 2010Andre KjNo ratings yet

- Return On EquityDocument1 pageReturn On EquityNilesh KumarNo ratings yet

- Vertical Analysis For Att and VerizonDocument4 pagesVertical Analysis For Att and Verizonapi-299644289No ratings yet

- Ebitda: Change in Other Current Liabilities - (2,492)Document3 pagesEbitda: Change in Other Current Liabilities - (2,492)waldyraeNo ratings yet

- Ak Hotel Sap 4Document7 pagesAk Hotel Sap 4aniNo ratings yet

- Ford Financial StatementDocument14 pagesFord Financial Statementaegan27No ratings yet

- Citigroup Q4 2012 Financial SupplementDocument47 pagesCitigroup Q4 2012 Financial SupplementalxcnqNo ratings yet

- Performance Highlights: Sales Volume & Growth % Net Sales, Operating EBITDA & Operating EBITDA MarginDocument4 pagesPerformance Highlights: Sales Volume & Growth % Net Sales, Operating EBITDA & Operating EBITDA MarginArijit DasNo ratings yet

- Example SDN BHDDocument9 pagesExample SDN BHDputery_perakNo ratings yet

- Statement Date No. of MonthsDocument6 pagesStatement Date No. of MonthscallvkNo ratings yet

- Financial Statements of Sealed Air Corporation Selected Income Statement DataDocument6 pagesFinancial Statements of Sealed Air Corporation Selected Income Statement DataRonny RoyNo ratings yet

- Financial Statement Fy 14 Q 3Document46 pagesFinancial Statement Fy 14 Q 3crtc2688No ratings yet

- Ar 2005 Financial Statements p55 eDocument3 pagesAr 2005 Financial Statements p55 esalehin1969No ratings yet

- Accounting Clinic IDocument40 pagesAccounting Clinic IRitesh Batra100% (1)

- SMRT Corporation LTD: Unaudited Financial Statements For The Second Quarter and Half-Year Ended 30 September 2011Document18 pagesSMRT Corporation LTD: Unaudited Financial Statements For The Second Quarter and Half-Year Ended 30 September 2011nicholasyeoNo ratings yet

- "Part-I B: Return of Total Income/Statement of Final Taxation Under The Income Tax Ordinance, 2001 (For Company) IT-1Document6 pages"Part-I B: Return of Total Income/Statement of Final Taxation Under The Income Tax Ordinance, 2001 (For Company) IT-1hina08855No ratings yet

- EddffDocument72 pagesEddfftatapanmindaNo ratings yet

- Boeing: I. Market InformationDocument21 pagesBoeing: I. Market InformationMohamed Ali SalemNo ratings yet

- Myer AR10 Financial ReportDocument50 pagesMyer AR10 Financial ReportMitchell HughesNo ratings yet

- Income Statement: Quarterly Financials For Toyota Motor Corporation ADSDocument7 pagesIncome Statement: Quarterly Financials For Toyota Motor Corporation ADSneenakm22No ratings yet

- Cost Accounting EVADocument6 pagesCost Accounting EVANikhil KasatNo ratings yet

- Delta CaseDocument5 pagesDelta Caseday9dreamerNo ratings yet

- Dr. Reddy's 2009Document3 pagesDr. Reddy's 2009Narasimhan SrinivasanNo ratings yet

- Condensed Consolidated Statements of IncomeDocument7 pagesCondensed Consolidated Statements of IncomevenkeeeeeNo ratings yet

- Business Activities and Financial StatementsDocument23 pagesBusiness Activities and Financial StatementsUsha RadhakrishnanNo ratings yet

- Income Statement Year Ended June 30 ($000) 1995 1994 1993 RevenuesDocument5 pagesIncome Statement Year Ended June 30 ($000) 1995 1994 1993 Revenuesthe master magicNo ratings yet

- Financial Status Sesa Goa 2011-12Document13 pagesFinancial Status Sesa Goa 2011-12Roshankumar S PimpalkarNo ratings yet

- Statement of Profit or LossDocument4 pagesStatement of Profit or LossShamierul IkhwanNo ratings yet

- Review Note 09 10Document18 pagesReview Note 09 10Amit VaghelaNo ratings yet

- Boeing: I. Market InformationDocument20 pagesBoeing: I. Market InformationJames ParkNo ratings yet

- FordMotorCompany 10Q 20110805Document102 pagesFordMotorCompany 10Q 20110805Lee LoganNo ratings yet

- Heineken 2010Document9 pagesHeineken 2010emericamikeNo ratings yet

- Financial Analysis of BioconDocument12 pagesFinancial Analysis of BioconNipun KothariNo ratings yet

- Statement of Cash FlowsDocument7 pagesStatement of Cash FlowsratihNo ratings yet

- 04 Pfizer AnalysisDocument5 pages04 Pfizer AnalysisKapil AgarwalNo ratings yet

- 2012 Annual Financial ReportDocument76 pages2012 Annual Financial ReportNguyễn Tiến HưngNo ratings yet

- SouthwestDocument15 pagesSouthwestBb DianaNo ratings yet

- FY11 - Investor PresentationDocument11 pagesFY11 - Investor Presentationcooladi$No ratings yet

- Marine Machinery, Equipment & Supplies Wholesale Revenues World Summary: Market Values & Financials by CountryFrom EverandMarine Machinery, Equipment & Supplies Wholesale Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Motor Vehicle & Motor Vehicle Parts & Supplies Agent Revenues World Summary: Market Values & Financials by CountryFrom EverandMotor Vehicle & Motor Vehicle Parts & Supplies Agent Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Motorcycle, Boat & Motor Vehicle Dealer Revenues World Summary: Market Values & Financials by CountryFrom EverandMotorcycle, Boat & Motor Vehicle Dealer Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- ChapterDocument42 pagesChapterdhillonjatt499No ratings yet

- Ch23 Answer KeyDocument32 pagesCh23 Answer KeyWed CornelNo ratings yet

- Grade 8 EMS Classic Ed GuideDocument41 pagesGrade 8 EMS Classic Ed GuideMartyn Van ZylNo ratings yet

- Read The Following Hypothetical Text and Answer The Given QuestionsDocument12 pagesRead The Following Hypothetical Text and Answer The Given QuestionsRoshan KardaNo ratings yet

- Establishment of RestaurantDocument2 pagesEstablishment of RestaurantDeepak JinaNo ratings yet

- Vietnam CBCR Rules - Circular No. TT41 - 2017Document14 pagesVietnam CBCR Rules - Circular No. TT41 - 2017Paula Aurora MendozaNo ratings yet

- CH 11Document48 pagesCH 11Pham Khanh Duy (K16HL)No ratings yet

- Entrepreneurship LAS 5 Q4 Week 5 6Document10 pagesEntrepreneurship LAS 5 Q4 Week 5 6Desiree Jane SaleraNo ratings yet

- Creative Accounting: A Fraudulent Practice Leading To Corporate CollapsesDocument15 pagesCreative Accounting: A Fraudulent Practice Leading To Corporate CollapsesF_Community100% (1)

- ENT600 Blueprint Format PDFDocument22 pagesENT600 Blueprint Format PDFMuhd Shoffi50% (2)

- Toaz - Info Sap HR PCR Time MGT PRDocument14 pagesToaz - Info Sap HR PCR Time MGT PRNavya HoneyNo ratings yet

- SIDCO Application For Allotment OldDocument7 pagesSIDCO Application For Allotment OldnagsankarNo ratings yet

- Master BudgetDocument6 pagesMaster BudgetPia LustreNo ratings yet

- Multiple Member Managed Operating Agreement Long FormDocument12 pagesMultiple Member Managed Operating Agreement Long Formjesusalbertogalvez100% (4)

- Financial Accounting 4th Edition. Chapter 1 SummaryDocument13 pagesFinancial Accounting 4th Edition. Chapter 1 SummaryJoey TrompNo ratings yet

- Financial Accounting - 1 PDFDocument73 pagesFinancial Accounting - 1 PDFSudhanva RajNo ratings yet

- CH - 03financial Statement Analysis Solution Manual CH - 03Document63 pagesCH - 03financial Statement Analysis Solution Manual CH - 03OktarinaNo ratings yet

- Sesi 2Document23 pagesSesi 2smpurnolietaniaNo ratings yet

- CLOTHING ALLOWANCE Payroll Form 7 Cy 2018 Guagua EastDocument144 pagesCLOTHING ALLOWANCE Payroll Form 7 Cy 2018 Guagua EastKinn GarciaNo ratings yet

- 1 BCforFS (W09)Document8 pages1 BCforFS (W09)mtaashi7115No ratings yet

- Ma Project FMCG-: Marico, Itc, Colgate, Unilever, Yili, PepsicoDocument12 pagesMa Project FMCG-: Marico, Itc, Colgate, Unilever, Yili, PepsicoJasneet BaidNo ratings yet

- 2005 - Dec - QUS CAT T3Document10 pages2005 - Dec - QUS CAT T3asad19No ratings yet

- Chapter-8 (House Property)Document40 pagesChapter-8 (House Property)BoRO TriAngLENo ratings yet

- 721 Decision CanorecoDocument45 pages721 Decision CanorecoHjktdmhmNo ratings yet

- PMDC Annual Report 2016-2017Document56 pagesPMDC Annual Report 2016-2017Ali Zain-ul-Abideen ChowhanNo ratings yet

- ProjectDocument10 pagesProjectKrishnaNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Worldcom Financials 2000 2002 ADocument5 pagesWorldcom Financials 2000 2002 AmominNo ratings yet

- Chapter16.Capital Expenditure DecisionsDocument44 pagesChapter16.Capital Expenditure DecisionsErdjol Yzeiri63% (8)

- Tutorial FIN645 PYQDocument2 pagesTutorial FIN645 PYQJuu Scully DavidNo ratings yet

- MU PLC Annual Report 2002 Financial StatementsDocument21 pagesMU PLC Annual Report 2002 Financial StatementsNurlisaAlnyNo ratings yet

- ST Aerospace Financial ReportDocument4 pagesST Aerospace Financial ReportMuhammad FirdausNo ratings yet

- Airthread Connections NidaDocument15 pagesAirthread Connections NidaNidaParveen100% (1)

- Taxation AnswerDocument13 pagesTaxation AnswerkannadhassNo ratings yet

- AirThread G015Document6 pagesAirThread G015sahildharhakim83% (6)

- Chapter 2 Payroll Accounting 2018Document53 pagesChapter 2 Payroll Accounting 2018Gabi Mihalek100% (1)

- Accounting PretestDocument4 pagesAccounting PretestseymourwardNo ratings yet

- 2010 Ibm StatementsDocument6 pages2010 Ibm StatementsElsa MersiniNo ratings yet

- Financial Statements Review Q4 2010Document17 pagesFinancial Statements Review Q4 2010sahaiakkiNo ratings yet

- Net Income Attributable To Noncontrolling Interest Net Income (Loss) Attributable To VerizonDocument9 pagesNet Income Attributable To Noncontrolling Interest Net Income (Loss) Attributable To VerizonvenkeeeeeNo ratings yet

- Financial Statements PDFDocument91 pagesFinancial Statements PDFHolmes MusclesFanNo ratings yet

- Income Taxes (Excluding The Synthetic Fuel Segment)Document8 pagesIncome Taxes (Excluding The Synthetic Fuel Segment)butterflygigglesNo ratings yet

- Q1 FY2013 InvestorsDocument28 pagesQ1 FY2013 InvestorsRajesh NaiduNo ratings yet

- Equity ValuationDocument2,424 pagesEquity ValuationMuteeb Raina0% (1)

- Macys 2011 10kDocument39 pagesMacys 2011 10kapb5223No ratings yet

- Kunci Jawaban Black and WhiteDocument18 pagesKunci Jawaban Black and WhitefebrythiodorNo ratings yet

- Result Y15 Doc4Document28 pagesResult Y15 Doc4ashokdb2kNo ratings yet

- MCB Consolidated For Year Ended Dec 2011Document87 pagesMCB Consolidated For Year Ended Dec 2011shoaibjeeNo ratings yet

- IT Return IT1 WithAnnexure 23454434Document3 pagesIT Return IT1 WithAnnexure 23454434khurramacaaNo ratings yet

- Profit&Loss May 2010Document2 pagesProfit&Loss May 2010Andre KjNo ratings yet

- Return On EquityDocument1 pageReturn On EquityNilesh KumarNo ratings yet

- Vertical Analysis For Att and VerizonDocument4 pagesVertical Analysis For Att and Verizonapi-299644289No ratings yet

- Ebitda: Change in Other Current Liabilities - (2,492)Document3 pagesEbitda: Change in Other Current Liabilities - (2,492)waldyraeNo ratings yet

- Ak Hotel Sap 4Document7 pagesAk Hotel Sap 4aniNo ratings yet

- Ford Financial StatementDocument14 pagesFord Financial Statementaegan27No ratings yet

- Citigroup Q4 2012 Financial SupplementDocument47 pagesCitigroup Q4 2012 Financial SupplementalxcnqNo ratings yet

- Performance Highlights: Sales Volume & Growth % Net Sales, Operating EBITDA & Operating EBITDA MarginDocument4 pagesPerformance Highlights: Sales Volume & Growth % Net Sales, Operating EBITDA & Operating EBITDA MarginArijit DasNo ratings yet

- Example SDN BHDDocument9 pagesExample SDN BHDputery_perakNo ratings yet

- Statement Date No. of MonthsDocument6 pagesStatement Date No. of MonthscallvkNo ratings yet

- Financial Statements of Sealed Air Corporation Selected Income Statement DataDocument6 pagesFinancial Statements of Sealed Air Corporation Selected Income Statement DataRonny RoyNo ratings yet

- Financial Statement Fy 14 Q 3Document46 pagesFinancial Statement Fy 14 Q 3crtc2688No ratings yet

- Ar 2005 Financial Statements p55 eDocument3 pagesAr 2005 Financial Statements p55 esalehin1969No ratings yet

- Accounting Clinic IDocument40 pagesAccounting Clinic IRitesh Batra100% (1)

- SMRT Corporation LTD: Unaudited Financial Statements For The Second Quarter and Half-Year Ended 30 September 2011Document18 pagesSMRT Corporation LTD: Unaudited Financial Statements For The Second Quarter and Half-Year Ended 30 September 2011nicholasyeoNo ratings yet

- "Part-I B: Return of Total Income/Statement of Final Taxation Under The Income Tax Ordinance, 2001 (For Company) IT-1Document6 pages"Part-I B: Return of Total Income/Statement of Final Taxation Under The Income Tax Ordinance, 2001 (For Company) IT-1hina08855No ratings yet

- EddffDocument72 pagesEddfftatapanmindaNo ratings yet

- Boeing: I. Market InformationDocument21 pagesBoeing: I. Market InformationMohamed Ali SalemNo ratings yet

- Myer AR10 Financial ReportDocument50 pagesMyer AR10 Financial ReportMitchell HughesNo ratings yet

- Income Statement: Quarterly Financials For Toyota Motor Corporation ADSDocument7 pagesIncome Statement: Quarterly Financials For Toyota Motor Corporation ADSneenakm22No ratings yet

- Cost Accounting EVADocument6 pagesCost Accounting EVANikhil KasatNo ratings yet

- Delta CaseDocument5 pagesDelta Caseday9dreamerNo ratings yet

- Dr. Reddy's 2009Document3 pagesDr. Reddy's 2009Narasimhan SrinivasanNo ratings yet

- Condensed Consolidated Statements of IncomeDocument7 pagesCondensed Consolidated Statements of IncomevenkeeeeeNo ratings yet

- Business Activities and Financial StatementsDocument23 pagesBusiness Activities and Financial StatementsUsha RadhakrishnanNo ratings yet

- Income Statement Year Ended June 30 ($000) 1995 1994 1993 RevenuesDocument5 pagesIncome Statement Year Ended June 30 ($000) 1995 1994 1993 Revenuesthe master magicNo ratings yet

- Financial Status Sesa Goa 2011-12Document13 pagesFinancial Status Sesa Goa 2011-12Roshankumar S PimpalkarNo ratings yet

- Statement of Profit or LossDocument4 pagesStatement of Profit or LossShamierul IkhwanNo ratings yet

- Review Note 09 10Document18 pagesReview Note 09 10Amit VaghelaNo ratings yet

- Boeing: I. Market InformationDocument20 pagesBoeing: I. Market InformationJames ParkNo ratings yet

- FordMotorCompany 10Q 20110805Document102 pagesFordMotorCompany 10Q 20110805Lee LoganNo ratings yet

- Heineken 2010Document9 pagesHeineken 2010emericamikeNo ratings yet

- Financial Analysis of BioconDocument12 pagesFinancial Analysis of BioconNipun KothariNo ratings yet

- Statement of Cash FlowsDocument7 pagesStatement of Cash FlowsratihNo ratings yet

- 04 Pfizer AnalysisDocument5 pages04 Pfizer AnalysisKapil AgarwalNo ratings yet

- 2012 Annual Financial ReportDocument76 pages2012 Annual Financial ReportNguyễn Tiến HưngNo ratings yet

- SouthwestDocument15 pagesSouthwestBb DianaNo ratings yet

- FY11 - Investor PresentationDocument11 pagesFY11 - Investor Presentationcooladi$No ratings yet

- Marine Machinery, Equipment & Supplies Wholesale Revenues World Summary: Market Values & Financials by CountryFrom EverandMarine Machinery, Equipment & Supplies Wholesale Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Motor Vehicle & Motor Vehicle Parts & Supplies Agent Revenues World Summary: Market Values & Financials by CountryFrom EverandMotor Vehicle & Motor Vehicle Parts & Supplies Agent Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Motorcycle, Boat & Motor Vehicle Dealer Revenues World Summary: Market Values & Financials by CountryFrom EverandMotorcycle, Boat & Motor Vehicle Dealer Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- ChapterDocument42 pagesChapterdhillonjatt499No ratings yet

- Ch23 Answer KeyDocument32 pagesCh23 Answer KeyWed CornelNo ratings yet

- Grade 8 EMS Classic Ed GuideDocument41 pagesGrade 8 EMS Classic Ed GuideMartyn Van ZylNo ratings yet

- Read The Following Hypothetical Text and Answer The Given QuestionsDocument12 pagesRead The Following Hypothetical Text and Answer The Given QuestionsRoshan KardaNo ratings yet

- Establishment of RestaurantDocument2 pagesEstablishment of RestaurantDeepak JinaNo ratings yet

- Vietnam CBCR Rules - Circular No. TT41 - 2017Document14 pagesVietnam CBCR Rules - Circular No. TT41 - 2017Paula Aurora MendozaNo ratings yet

- CH 11Document48 pagesCH 11Pham Khanh Duy (K16HL)No ratings yet

- Entrepreneurship LAS 5 Q4 Week 5 6Document10 pagesEntrepreneurship LAS 5 Q4 Week 5 6Desiree Jane SaleraNo ratings yet

- Creative Accounting: A Fraudulent Practice Leading To Corporate CollapsesDocument15 pagesCreative Accounting: A Fraudulent Practice Leading To Corporate CollapsesF_Community100% (1)

- ENT600 Blueprint Format PDFDocument22 pagesENT600 Blueprint Format PDFMuhd Shoffi50% (2)

- Toaz - Info Sap HR PCR Time MGT PRDocument14 pagesToaz - Info Sap HR PCR Time MGT PRNavya HoneyNo ratings yet

- SIDCO Application For Allotment OldDocument7 pagesSIDCO Application For Allotment OldnagsankarNo ratings yet

- Master BudgetDocument6 pagesMaster BudgetPia LustreNo ratings yet

- Multiple Member Managed Operating Agreement Long FormDocument12 pagesMultiple Member Managed Operating Agreement Long Formjesusalbertogalvez100% (4)

- Financial Accounting 4th Edition. Chapter 1 SummaryDocument13 pagesFinancial Accounting 4th Edition. Chapter 1 SummaryJoey TrompNo ratings yet

- Financial Accounting - 1 PDFDocument73 pagesFinancial Accounting - 1 PDFSudhanva RajNo ratings yet

- CH - 03financial Statement Analysis Solution Manual CH - 03Document63 pagesCH - 03financial Statement Analysis Solution Manual CH - 03OktarinaNo ratings yet

- Sesi 2Document23 pagesSesi 2smpurnolietaniaNo ratings yet

- CLOTHING ALLOWANCE Payroll Form 7 Cy 2018 Guagua EastDocument144 pagesCLOTHING ALLOWANCE Payroll Form 7 Cy 2018 Guagua EastKinn GarciaNo ratings yet

- 1 BCforFS (W09)Document8 pages1 BCforFS (W09)mtaashi7115No ratings yet

- Ma Project FMCG-: Marico, Itc, Colgate, Unilever, Yili, PepsicoDocument12 pagesMa Project FMCG-: Marico, Itc, Colgate, Unilever, Yili, PepsicoJasneet BaidNo ratings yet

- 2005 - Dec - QUS CAT T3Document10 pages2005 - Dec - QUS CAT T3asad19No ratings yet

- Chapter-8 (House Property)Document40 pagesChapter-8 (House Property)BoRO TriAngLENo ratings yet

- 721 Decision CanorecoDocument45 pages721 Decision CanorecoHjktdmhmNo ratings yet

- PMDC Annual Report 2016-2017Document56 pagesPMDC Annual Report 2016-2017Ali Zain-ul-Abideen ChowhanNo ratings yet

- ProjectDocument10 pagesProjectKrishnaNo ratings yet