Download as pdf or txt

You might also like

- Unit 3 & Unit 4Document8 pagesUnit 3 & Unit 4Melania Arliana MeoNo ratings yet

- Farm Tools in Agricultural Crop ProductionDocument6 pagesFarm Tools in Agricultural Crop ProductionJohnLesterDeLeon67% (15)

- Presentation (Company Update)Document29 pagesPresentation (Company Update)Shyam SunderNo ratings yet

- Communication To Investors - June 2015 (Company Update)Document11 pagesCommunication To Investors - June 2015 (Company Update)Shyam SunderNo ratings yet

- Q2FY16 Investor Presentation (Company Update)Document37 pagesQ2FY16 Investor Presentation (Company Update)Shyam SunderNo ratings yet

- Fsa 2011 15 PDFDocument253 pagesFsa 2011 15 PDFalizaNo ratings yet

- 1H15 PPT - VFDocument29 pages1H15 PPT - VFClaudio Andrés De LucaNo ratings yet

- Blue Dart Express LTD.: CompanyDocument5 pagesBlue Dart Express LTD.: CompanygirishrajsNo ratings yet

- Britannia Investor PresentationDocument29 pagesBritannia Investor PresentationDaniel ChngNo ratings yet

- Investor Presentation (Company Update)Document34 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Fiscal Management Report 2016Document123 pagesFiscal Management Report 2016Ada DeranaNo ratings yet

- HCL Infosystems Limited: Q1 FY17 Investor UpdateDocument13 pagesHCL Infosystems Limited: Q1 FY17 Investor UpdateRajasekhar Reddy AnekalluNo ratings yet

- Auditors Report and Audited Financial StatementsDocument45 pagesAuditors Report and Audited Financial Statementszahir2020No ratings yet

- Investor Update (Company Update)Document27 pagesInvestor Update (Company Update)Shyam SunderNo ratings yet

- PGOLD: Investor Presentation MaterialsDocument18 pagesPGOLD: Investor Presentation MaterialsBusinessWorldNo ratings yet

- Financial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Document4 pagesFinancial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderNo ratings yet

- Financial Results With Results Press Release & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Document5 pagesFinancial Results With Results Press Release & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderNo ratings yet

- Axiata Presentation 1Q2015Document39 pagesAxiata Presentation 1Q2015Jeck Hong TanNo ratings yet

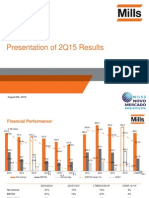

- 2Q15 Presentation of ResultsDocument30 pages2Q15 Presentation of ResultsMillsRINo ratings yet

- Financial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Document3 pagesFinancial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderNo ratings yet

- Analyst Meet Kolkata 13 August 2014Document21 pagesAnalyst Meet Kolkata 13 August 2014pv1977No ratings yet

- 1Q14 Presentation of ResultsDocument16 pages1Q14 Presentation of ResultsMillsRINo ratings yet

- Interim Report Interim ReportDocument34 pagesInterim Report Interim ReportMohammed AbdoNo ratings yet

- Acc PloDocument2 pagesAcc PloAshan MartinoNo ratings yet

- Rio Tinto Delivers First Half Underlying Earnings of 2.9 BillionDocument58 pagesRio Tinto Delivers First Half Underlying Earnings of 2.9 BillionBisto MasiloNo ratings yet

- JM Financial Consolidated Performance Q4 FY14Document29 pagesJM Financial Consolidated Performance Q4 FY14Ankita NirolaNo ratings yet

- Corporate GovernanceDocument182 pagesCorporate GovernanceBabu RaoNo ratings yet

- Earnings Update Q4FY15 (Company Update)Document45 pagesEarnings Update Q4FY15 (Company Update)Shyam SunderNo ratings yet

- ABL Half Yearly 2015Document52 pagesABL Half Yearly 2015hamzaNo ratings yet

- KPIT Technologies: IT Services Sector Outlook - NeutralDocument9 pagesKPIT Technologies: IT Services Sector Outlook - NeutralgirishrajsNo ratings yet

- KPIT 2QFY16 Outlook ReviewDocument5 pagesKPIT 2QFY16 Outlook ReviewgirishrajsNo ratings yet

- KPIT Technologies (KPISYS) : Optimistic RecoveryDocument11 pagesKPIT Technologies (KPISYS) : Optimistic RecoverygirishrajsNo ratings yet

- Kellton Tech Surges Ahead in 2014-15Document18 pagesKellton Tech Surges Ahead in 2014-15api-234474152No ratings yet

- Investors' Presentation (Company Update)Document28 pagesInvestors' Presentation (Company Update)Shyam SunderNo ratings yet

- 2015 04 Investor PresentationDocument37 pages2015 04 Investor PresentationsidNo ratings yet

- A Grade SampleDocument25 pagesA Grade SampleTharindu PereraNo ratings yet

- Kingfisher Airlines LTD.: Result UpdateDocument4 pagesKingfisher Airlines LTD.: Result UpdateSagar KavdeNo ratings yet

- Investor Presentation: Q4FY15 UpdateDocument34 pagesInvestor Presentation: Q4FY15 UpdateAditya NagpalNo ratings yet

- File 28052013214151 PDFDocument45 pagesFile 28052013214151 PDFraheja_ashishNo ratings yet

- V-Guard Industries: CMP: INR523 TP: INR650 BuyDocument10 pagesV-Guard Industries: CMP: INR523 TP: INR650 BuySmriti SrivastavaNo ratings yet

- Investor Update (Company Update)Document16 pagesInvestor Update (Company Update)Shyam SunderNo ratings yet

- Infosys (INFTEC) : Solid Beat Spoiled by Soft GuidanceDocument11 pagesInfosys (INFTEC) : Solid Beat Spoiled by Soft GuidanceumaganNo ratings yet

- Announces Q2 Results & Auditors' Report For The Quarter Ended September 30, 2015 (Result)Document4 pagesAnnounces Q2 Results & Auditors' Report For The Quarter Ended September 30, 2015 (Result)Shyam SunderNo ratings yet

- Investor Presentation (Company Update)Document22 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- PI Industries DolatCap 141111Document6 pagesPI Industries DolatCap 141111equityanalystinvestorNo ratings yet

- The Framework Will Be As Under:: Profit Parameters Larse N& L&T Toubr o 2015 2014 Ebdita 12342 .76Document2 pagesThe Framework Will Be As Under:: Profit Parameters Larse N& L&T Toubr o 2015 2014 Ebdita 12342 .76Purna ChoudharyNo ratings yet

- Tata El Xs I LimitedDocument6 pagesTata El Xs I LimitedAyush JainNo ratings yet

- Announces Consolidated Q1 Results & Results Press Release (Result)Document7 pagesAnnounces Consolidated Q1 Results & Results Press Release (Result)Shyam SunderNo ratings yet

- CCT Ar-2015Document184 pagesCCT Ar-2015Sassy TanNo ratings yet

- Financial Results & Limited Review For March 31, 2015 (Result)Document5 pagesFinancial Results & Limited Review For March 31, 2015 (Result)Shyam SunderNo ratings yet

- 3q2015 CemproDocument16 pages3q2015 Cemproapi-307565920No ratings yet

- 1Q15 Presentation of ResultsDocument20 pages1Q15 Presentation of ResultsMillsRINo ratings yet

- Press Meet Q4 FY12Document30 pagesPress Meet Q4 FY12Chintan KotadiaNo ratings yet

- Result Presentation For March 31, 2016 (Result)Document11 pagesResult Presentation For March 31, 2016 (Result)Shyam SunderNo ratings yet

- Investor Presentation: Q2FY13 & H1FY13 UpdateDocument18 pagesInvestor Presentation: Q2FY13 & H1FY13 UpdategirishdrjNo ratings yet

- Financial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Document3 pagesFinancial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderNo ratings yet

- Financial Results & Limited Review Report For June 30, 2015 (Standalone) (Company Update)Document3 pagesFinancial Results & Limited Review Report For June 30, 2015 (Standalone) (Company Update)Shyam SunderNo ratings yet

- BRF - Deutsche Paris Jun15Document30 pagesBRF - Deutsche Paris Jun15PedroShawNo ratings yet

- Abridged 2014Document1 pageAbridged 2014Jashveer SeetahulNo ratings yet

- Guide to Management Accounting CCC (Cash Conversion Cycle) for Managers 2020 EditionFrom EverandGuide to Management Accounting CCC (Cash Conversion Cycle) for Managers 2020 EditionNo ratings yet

- Guide to Management Accounting CCC (Cash Conversion Cycle) for ManagersFrom EverandGuide to Management Accounting CCC (Cash Conversion Cycle) for ManagersNo ratings yet

- Guide to Management Accounting CCC for managers 2020 EditionFrom EverandGuide to Management Accounting CCC for managers 2020 EditionNo ratings yet

- PDF Processed With Cutepdf Evaluation EditionDocument3 pagesPDF Processed With Cutepdf Evaluation EditionShyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For June 30, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For June 30, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results For September 30, 2016 (Result)Document3 pagesStandalone Financial Results For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results For March 31, 2016 (Result)Document11 pagesStandalone Financial Results For March 31, 2016 (Result)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For September 30, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For September 30, 2016 (Result)Shyam SunderNo ratings yet

- Investor Presentation For December 31, 2016 (Company Update)Document27 pagesInvestor Presentation For December 31, 2016 (Company Update)Shyam SunderNo ratings yet

- Transcript of The Investors / Analysts Con Call (Company Update)Document15 pagesTranscript of The Investors / Analysts Con Call (Company Update)Shyam SunderNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Has An Introduction That Introduces A Topic and Grabs The Reader's AttentionDocument9 pagesHas An Introduction That Introduces A Topic and Grabs The Reader's AttentionAlemar LimbingNo ratings yet

- Zenit P Series Electric Submersible Pump Data BookletDocument52 pagesZenit P Series Electric Submersible Pump Data BookletPatricia J ÁngelesNo ratings yet

- Tokomama 1Document960 pagesTokomama 1gerry zonathanNo ratings yet

- Polycrystalline Module 72X6": Chubb InsuranceDocument2 pagesPolycrystalline Module 72X6": Chubb InsuranceNatalia AndreaNo ratings yet

- Mink, Anthony James (LG)Document3 pagesMink, Anthony James (LG)James LindonNo ratings yet

- July 12, 2019 Strathmore TimesDocument20 pagesJuly 12, 2019 Strathmore TimesStrathmore TimesNo ratings yet

- Pre-Setting Manual Balancing Valves CIM 788: Technical InformationDocument7 pagesPre-Setting Manual Balancing Valves CIM 788: Technical InformationblindjaxxNo ratings yet

- Munn Inc Had The Following Intangible Account Balance at DecemberDocument1 pageMunn Inc Had The Following Intangible Account Balance at DecemberHassan JanNo ratings yet

- Ch.4 Lesson (1) EasyDocument12 pagesCh.4 Lesson (1) EasyShahd WaelNo ratings yet

- Anhedonia Preclinical, Translational, and Clinical Integration (Ch. 1)Document30 pagesAnhedonia Preclinical, Translational, and Clinical Integration (Ch. 1)strillenNo ratings yet

- Anxiety Free - Stop Worrying and - McKeown, PatrickDocument237 pagesAnxiety Free - Stop Worrying and - McKeown, PatrickLoboCamon100% (1)

- Chapter 01Document2 pagesChapter 01badunktuaNo ratings yet

- CyclamenDocument50 pagesCyclamenLAUM1No ratings yet

- Chapter 5 Connective Tissue NotesDocument3 pagesChapter 5 Connective Tissue NotesBinadi JayNo ratings yet

- Package Design GuideDocument11 pagesPackage Design Guideondoy4925No ratings yet

- P31846 Eletrificador Ultra22K Unificado REV0!1!1678975121311Document2 pagesP31846 Eletrificador Ultra22K Unificado REV0!1!1678975121311SEBASTIAN CALLEJAS GONZALEZNo ratings yet

- National Labor Relations Board v. Edward P. Tepper D/B/A Shoenberg Farms, 297 F.2d 280, 10th Cir. (1961)Document6 pagesNational Labor Relations Board v. Edward P. Tepper D/B/A Shoenberg Farms, 297 F.2d 280, 10th Cir. (1961)Scribd Government DocsNo ratings yet

- Toyota Forklift 8fbet15!20!8fbekt16 18 8fbmt15 20 Repair ManualDocument22 pagesToyota Forklift 8fbet15!20!8fbekt16 18 8fbmt15 20 Repair Manualalexhughes210188dzo100% (133)

- Band and Loop Space Maintainer: Fabrication RequirementsDocument1 pageBand and Loop Space Maintainer: Fabrication RequirementsVidhi AdilNo ratings yet

- Prahlad Patel HulDocument45 pagesPrahlad Patel Hulrichamalhotra87No ratings yet

- Conveyor ChainsDocument172 pagesConveyor Chainsmkpasha55mpNo ratings yet

- Growing in Vitro Diagnostics (IVD) Market To Set New Business Opportunities For Start Up CompanyDocument2 pagesGrowing in Vitro Diagnostics (IVD) Market To Set New Business Opportunities For Start Up CompanyPR.comNo ratings yet

- Jayson Desear: 3. What Is The Importance of Legislation in The Development and Sustenance of Special Education Programs?Document2 pagesJayson Desear: 3. What Is The Importance of Legislation in The Development and Sustenance of Special Education Programs?Jayson Desear100% (3)

- EMM-Important Questions PDFDocument26 pagesEMM-Important Questions PDFsyed abdul rahamanNo ratings yet

- Pediatric BLSDocument32 pagesPediatric BLSYuni AjahNo ratings yet

- Risk and Return AnalysisDocument22 pagesRisk and Return AnalysisRanjan Saini100% (1)

- Hospital Response To A Major Incident: Initial Considerations and Longer Term EffectsDocument5 pagesHospital Response To A Major Incident: Initial Considerations and Longer Term EffectsMinaz PatelNo ratings yet

- HB1202Document5 pagesHB1202WTVCNo ratings yet