(Half-Yearly) Introduction To Economics

(Half-Yearly) Introduction To Economics

You might also like

- Managing Filipino Teams by Mike GroganDocument107 pagesManaging Filipino Teams by Mike GroganglycerilkayeNo ratings yet

- Government Departments Contact Emails/Phone Numbers EtcDocument149 pagesGovernment Departments Contact Emails/Phone Numbers EtcPaul Smith0% (1)

- 2 Michel Thomas Spanish AdvancedDocument48 pages2 Michel Thomas Spanish Advancedsanjacarica100% (2)

- Software Manual: Intravision Image Processing Software 11.87.2Document159 pagesSoftware Manual: Intravision Image Processing Software 11.87.2Cristian FerchiuNo ratings yet

- 1 Scarcity, Choice & Opportunity CostDocument7 pages1 Scarcity, Choice & Opportunity Costqihui17No ratings yet

- Economics Study Yr 11Document41 pagesEconomics Study Yr 11sarahNo ratings yet

- Economics Notes HYDocument21 pagesEconomics Notes HYilu_3No ratings yet

- Economics Study Yr 11Document37 pagesEconomics Study Yr 11dgfdgNo ratings yet

- Toaz - Info CXC Economics Study Guide PRDocument31 pagesToaz - Info CXC Economics Study Guide PRRickoy Playz100% (1)

- What Is Economics About: Relative ScarcityDocument28 pagesWhat Is Economics About: Relative Scarcitykevin9797No ratings yet

- Principles of Economics 1Document36 pagesPrinciples of Economics 1reda gadNo ratings yet

- Chapter 1 The Central Problem of Economics and Economic SystemDocument11 pagesChapter 1 The Central Problem of Economics and Economic SystemcsanjeevanNo ratings yet

- Econ 1-Lesson 1 ModuleDocument9 pagesEcon 1-Lesson 1 ModuleArnie Jovinille Sablay RemullaNo ratings yet

- Handout 2 EconomicsDocument5 pagesHandout 2 EconomicsAllyn Jade BandialaNo ratings yet

- What Is Economics.s02Document75 pagesWhat Is Economics.s02GenNo ratings yet

- Week 1 Introduction To MicroeconomicsDocument39 pagesWeek 1 Introduction To Microeconomicstissot63No ratings yet

- Resource Utilization and EconomicsDocument5 pagesResource Utilization and EconomicsmalindaNo ratings yet

- Q3 Module 2 EconDocument45 pagesQ3 Module 2 Econashleypepito958No ratings yet

- 1.1 The Market SystemDocument36 pages1.1 The Market Systemsk001No ratings yet

- Year 11 Economics Introduction NotesDocument9 pagesYear 11 Economics Introduction Notesanon_3154664060% (1)

- Price TheoryDocument9 pagesPrice Theoryogunshinaoluwaseun337No ratings yet

- Economics Notes: 1.1 - Basic Economic Problem: Choice and The Allocation of ResourcesDocument52 pagesEconomics Notes: 1.1 - Basic Economic Problem: Choice and The Allocation of ResourcesMukmin Shukri100% (1)

- Introduction To EconomiesDocument12 pagesIntroduction To EconomiesCindy ChauNo ratings yet

- 001 The Nature and Purpose of Economic ActivityDocument6 pages001 The Nature and Purpose of Economic ActivityPratik DahalNo ratings yet

- Economics Unit 1 Notes From Sayeedh GhouseDocument50 pagesEconomics Unit 1 Notes From Sayeedh GhouseSayeedh GhouseNo ratings yet

- Economics Notes - Introduction To EconomicsDocument16 pagesEconomics Notes - Introduction To Economicskkesarwani727No ratings yet

- ECO401 - EconomicsDocument178 pagesECO401 - EconomicsMadeeeha83% (35)

- Ibcc Economics CD 01Document3 pagesIbcc Economics CD 01Raviraag RajasekharNo ratings yet

- Study Note - The Basic Economic Problem: Scarcity and ChoiceDocument5 pagesStudy Note - The Basic Economic Problem: Scarcity and ChoicePrerna GillNo ratings yet

- Introduction To EconomicsDocument12 pagesIntroduction To EconomicsBaro LeeNo ratings yet

- Central Problem of EconomicsDocument14 pagesCentral Problem of EconomicsOnella GrantNo ratings yet

- Econ Note For A LevelDocument43 pagesEcon Note For A LevelteeheeteeheehahahaNo ratings yet

- IEF Mod 1.1Document12 pagesIEF Mod 1.1ismaielsuttu4No ratings yet

- Central Concepts of EconomicsDocument21 pagesCentral Concepts of EconomicsREHANRAJNo ratings yet

- 1.1 Introduction To EconomicsDocument10 pages1.1 Introduction To Economicsjoel collinsNo ratings yet

- Lecture1. IntroDocument25 pagesLecture1. IntroMochiiiNo ratings yet

- Ig Econ NBDocument10 pagesIg Econ NBVania AroraNo ratings yet

- Introduction To EconomicsDocument9 pagesIntroduction To EconomicsEmily ZhangNo ratings yet

- Ecs ExampackDocument103 pagesEcs ExampackCharlize RileyNo ratings yet

- Basic Economics Ideas and Resource AllocationDocument10 pagesBasic Economics Ideas and Resource AllocationWaseem AhmedNo ratings yet

- Chapter 1 Gillespie PowerpointDocument23 pagesChapter 1 Gillespie PowerpointpartlinemokhothuNo ratings yet

- Economics IGCSE - Revision Notes (39 Chapters)Document67 pagesEconomics IGCSE - Revision Notes (39 Chapters)Nhi Ngô ThảoNo ratings yet

- CHICO - Report (The Basic Economic Problem)Document18 pagesCHICO - Report (The Basic Economic Problem)Alvie ChicoNo ratings yet

- The Economic ConflictDocument6 pagesThe Economic ConflictNathiyaaNo ratings yet

- Chapter 1: The Economic Way of ThinkingDocument87 pagesChapter 1: The Economic Way of ThinkingQuinnie CervantesNo ratings yet

- Introduction To Economics. - MicroeconomicsDocument321 pagesIntroduction To Economics. - MicroeconomicsMelusi ShanziNo ratings yet

- Basic Economic Problems of The Country1Document4 pagesBasic Economic Problems of The Country1Heaven SyNo ratings yet

- Introduction To EconomicsDocument36 pagesIntroduction To EconomicsLea Guico100% (1)

- Economics - Intro - NotesDocument13 pagesEconomics - Intro - NotesAbdur RahmanNo ratings yet

- Fundamental Concepts of EconomicsDocument66 pagesFundamental Concepts of EconomicsUwuigbe UwalomwaNo ratings yet

- 6 Introduction To EconomicsDocument9 pages6 Introduction To EconomicsDeependra NigamNo ratings yet

- Unit 1-ADocument37 pagesUnit 1-Aobodyqwerty123No ratings yet

- Economics Essay On ScarcityDocument2 pagesEconomics Essay On ScarcityRayden Tan50% (4)

- Economics Chapter 1-13 NotesIGCSEDocument19 pagesEconomics Chapter 1-13 NotesIGCSEyambenari21No ratings yet

- Chap 2 M1Document9 pagesChap 2 M1science boyNo ratings yet

- Scarcity and Efficiency Refers To The Twin Themes of EconomicsDocument9 pagesScarcity and Efficiency Refers To The Twin Themes of EconomicsYuva Prakash83% (6)

- Notes On All TopicsDocument56 pagesNotes On All TopicspotpalNo ratings yet

- Management: Advance Diploma LevelDocument7 pagesManagement: Advance Diploma LevelmerusaNo ratings yet

- Slide 1Document4 pagesSlide 1Jeffrey CardonaNo ratings yet

- Basic Economic ProblemDocument4 pagesBasic Economic ProblemBrigit MartinezNo ratings yet

- Economics Cheat SheetDocument3 pagesEconomics Cheat SheetMushfiq Jahan KhanNo ratings yet

- Basic Concepts of EconomicsDocument35 pagesBasic Concepts of Economicsmahmud.anindoNo ratings yet

- Summary Of "Economics, Principles And Applications" By Mochón & Becker: UNIVERSITY SUMMARIESFrom EverandSummary Of "Economics, Principles And Applications" By Mochón & Becker: UNIVERSITY SUMMARIESNo ratings yet

- Infs1602 Assignment Part A - Final Release - cr2Document5 pagesInfs1602 Assignment Part A - Final Release - cr2Ellia ChenNo ratings yet

- Fins1613 FormulasDocument7 pagesFins1613 FormulasEllia ChenNo ratings yet

- Skills: HSC Course Outcomes Content 11.1 Identify Data Sources ToDocument4 pagesSkills: HSC Course Outcomes Content 11.1 Identify Data Sources ToEllia ChenNo ratings yet

- Definitions: 1. Production of MaterialsDocument1 pageDefinitions: 1. Production of MaterialsEllia ChenNo ratings yet

- Suvigya: Details Furnished by You WereDocument1 pageSuvigya: Details Furnished by You WereMKMK JilaniNo ratings yet

- Lyrics - More Than AbleDocument2 pagesLyrics - More Than AbleZarita CarranzaNo ratings yet

- Word Form KeyDocument2 pagesWord Form KeyHoang Quynh AnhNo ratings yet

- 2021 WA2 Science (Physics) 3E ModifiedDocument13 pages2021 WA2 Science (Physics) 3E ModifiedfinNo ratings yet

- Davis Michael 1A Resume 1Document1 pageDavis Michael 1A Resume 1Alyssa HowellNo ratings yet

- Palanca vs. CADocument16 pagesPalanca vs. CASherwin Anoba CabutijaNo ratings yet

- Jersey Documentation 1.0.3 User GuideDocument35 pagesJersey Documentation 1.0.3 User Guidenaresh921No ratings yet

- Problem StatementDocument15 pagesProblem Statementcabamaro100% (3)

- The RC Oscillator CircuitDocument6 pagesThe RC Oscillator CircuitNishanthi BheemanNo ratings yet

- Angela SolikovaDocument10 pagesAngela SolikovaGirisha PathakNo ratings yet

- Experimental and CFD Resistance Calculation of A Small Fast CatamaranDocument7 pagesExperimental and CFD Resistance Calculation of A Small Fast CatamaranChandra SibaraniNo ratings yet

- Enfermedades Emergentes y Embarazo - EID - November 2006 - Volume CompletoDocument187 pagesEnfermedades Emergentes y Embarazo - EID - November 2006 - Volume CompletoRuth Vargas GonzalesNo ratings yet

- The Impact of Different Political Beliefs On The Family Relationship of College-StudentsDocument16 pagesThe Impact of Different Political Beliefs On The Family Relationship of College-Studentshue sandovalNo ratings yet

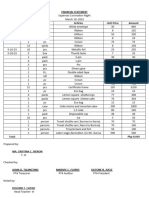

- Financial Statement Coronation NightDocument8 pagesFinancial Statement Coronation NightRuel Gapuz ManzanoNo ratings yet

- Learning Competency (Essential Competency) : Let's Recall (Review)Document6 pagesLearning Competency (Essential Competency) : Let's Recall (Review)Heidee BasasNo ratings yet

- Duration: 90 Days.: Fico Training ProgramDocument15 pagesDuration: 90 Days.: Fico Training ProgramMohammed Nawaz ShariffNo ratings yet

- Global Guidelines For The Prevention of Surgical Site Infection: An IntroductionDocument8 pagesGlobal Guidelines For The Prevention of Surgical Site Infection: An IntroductionJNUHospital NABHNo ratings yet

- ED6008Document4 pagesED6008VolvoxdjNo ratings yet

- PestelDocument2 pagesPestelSruthi DNo ratings yet

- UIL Calculator Applications Study ListDocument7 pagesUIL Calculator Applications Study ListRocket FireNo ratings yet

- Party Facility: Atty. Serrano LTD Lecture - July 12 Jzel EndozoDocument7 pagesParty Facility: Atty. Serrano LTD Lecture - July 12 Jzel EndozoJVLNo ratings yet

- CPD and Contracted PelvisDocument53 pagesCPD and Contracted Pelvismaxim tomuNo ratings yet

- RA 020 Risk Assessment - Risk Assessment - Installation of Cables in Ducts & TrenchesDocument11 pagesRA 020 Risk Assessment - Risk Assessment - Installation of Cables in Ducts & Trenchesthomson100% (2)

- English - Fine - Tune Your English 2019Document3 pagesEnglish - Fine - Tune Your English 2019NishaNo ratings yet

- LoB Player Guide Pyram KingDocument15 pagesLoB Player Guide Pyram KingRonaldo SilveiraNo ratings yet

- Steamshovel Press Issue 04Document60 pagesSteamshovel Press Issue 04liondog1No ratings yet

Download as pdf or txt

You might also like

- Managing Filipino Teams by Mike GroganDocument107 pagesManaging Filipino Teams by Mike GroganglycerilkayeNo ratings yet

- Government Departments Contact Emails/Phone Numbers EtcDocument149 pagesGovernment Departments Contact Emails/Phone Numbers EtcPaul Smith0% (1)

- 2 Michel Thomas Spanish AdvancedDocument48 pages2 Michel Thomas Spanish Advancedsanjacarica100% (2)

- Software Manual: Intravision Image Processing Software 11.87.2Document159 pagesSoftware Manual: Intravision Image Processing Software 11.87.2Cristian FerchiuNo ratings yet

- 1 Scarcity, Choice & Opportunity CostDocument7 pages1 Scarcity, Choice & Opportunity Costqihui17No ratings yet

- Economics Study Yr 11Document41 pagesEconomics Study Yr 11sarahNo ratings yet

- Economics Notes HYDocument21 pagesEconomics Notes HYilu_3No ratings yet

- Economics Study Yr 11Document37 pagesEconomics Study Yr 11dgfdgNo ratings yet

- Toaz - Info CXC Economics Study Guide PRDocument31 pagesToaz - Info CXC Economics Study Guide PRRickoy Playz100% (1)

- What Is Economics About: Relative ScarcityDocument28 pagesWhat Is Economics About: Relative Scarcitykevin9797No ratings yet

- Principles of Economics 1Document36 pagesPrinciples of Economics 1reda gadNo ratings yet

- Chapter 1 The Central Problem of Economics and Economic SystemDocument11 pagesChapter 1 The Central Problem of Economics and Economic SystemcsanjeevanNo ratings yet

- Econ 1-Lesson 1 ModuleDocument9 pagesEcon 1-Lesson 1 ModuleArnie Jovinille Sablay RemullaNo ratings yet

- Handout 2 EconomicsDocument5 pagesHandout 2 EconomicsAllyn Jade BandialaNo ratings yet

- What Is Economics.s02Document75 pagesWhat Is Economics.s02GenNo ratings yet

- Week 1 Introduction To MicroeconomicsDocument39 pagesWeek 1 Introduction To Microeconomicstissot63No ratings yet

- Resource Utilization and EconomicsDocument5 pagesResource Utilization and EconomicsmalindaNo ratings yet

- Q3 Module 2 EconDocument45 pagesQ3 Module 2 Econashleypepito958No ratings yet

- 1.1 The Market SystemDocument36 pages1.1 The Market Systemsk001No ratings yet

- Year 11 Economics Introduction NotesDocument9 pagesYear 11 Economics Introduction Notesanon_3154664060% (1)

- Price TheoryDocument9 pagesPrice Theoryogunshinaoluwaseun337No ratings yet

- Economics Notes: 1.1 - Basic Economic Problem: Choice and The Allocation of ResourcesDocument52 pagesEconomics Notes: 1.1 - Basic Economic Problem: Choice and The Allocation of ResourcesMukmin Shukri100% (1)

- Introduction To EconomiesDocument12 pagesIntroduction To EconomiesCindy ChauNo ratings yet

- 001 The Nature and Purpose of Economic ActivityDocument6 pages001 The Nature and Purpose of Economic ActivityPratik DahalNo ratings yet

- Economics Unit 1 Notes From Sayeedh GhouseDocument50 pagesEconomics Unit 1 Notes From Sayeedh GhouseSayeedh GhouseNo ratings yet

- Economics Notes - Introduction To EconomicsDocument16 pagesEconomics Notes - Introduction To Economicskkesarwani727No ratings yet

- ECO401 - EconomicsDocument178 pagesECO401 - EconomicsMadeeeha83% (35)

- Ibcc Economics CD 01Document3 pagesIbcc Economics CD 01Raviraag RajasekharNo ratings yet

- Study Note - The Basic Economic Problem: Scarcity and ChoiceDocument5 pagesStudy Note - The Basic Economic Problem: Scarcity and ChoicePrerna GillNo ratings yet

- Introduction To EconomicsDocument12 pagesIntroduction To EconomicsBaro LeeNo ratings yet

- Central Problem of EconomicsDocument14 pagesCentral Problem of EconomicsOnella GrantNo ratings yet

- Econ Note For A LevelDocument43 pagesEcon Note For A LevelteeheeteeheehahahaNo ratings yet

- IEF Mod 1.1Document12 pagesIEF Mod 1.1ismaielsuttu4No ratings yet

- Central Concepts of EconomicsDocument21 pagesCentral Concepts of EconomicsREHANRAJNo ratings yet

- 1.1 Introduction To EconomicsDocument10 pages1.1 Introduction To Economicsjoel collinsNo ratings yet

- Lecture1. IntroDocument25 pagesLecture1. IntroMochiiiNo ratings yet

- Ig Econ NBDocument10 pagesIg Econ NBVania AroraNo ratings yet

- Introduction To EconomicsDocument9 pagesIntroduction To EconomicsEmily ZhangNo ratings yet

- Ecs ExampackDocument103 pagesEcs ExampackCharlize RileyNo ratings yet

- Basic Economics Ideas and Resource AllocationDocument10 pagesBasic Economics Ideas and Resource AllocationWaseem AhmedNo ratings yet

- Chapter 1 Gillespie PowerpointDocument23 pagesChapter 1 Gillespie PowerpointpartlinemokhothuNo ratings yet

- Economics IGCSE - Revision Notes (39 Chapters)Document67 pagesEconomics IGCSE - Revision Notes (39 Chapters)Nhi Ngô ThảoNo ratings yet

- CHICO - Report (The Basic Economic Problem)Document18 pagesCHICO - Report (The Basic Economic Problem)Alvie ChicoNo ratings yet

- The Economic ConflictDocument6 pagesThe Economic ConflictNathiyaaNo ratings yet

- Chapter 1: The Economic Way of ThinkingDocument87 pagesChapter 1: The Economic Way of ThinkingQuinnie CervantesNo ratings yet

- Introduction To Economics. - MicroeconomicsDocument321 pagesIntroduction To Economics. - MicroeconomicsMelusi ShanziNo ratings yet

- Basic Economic Problems of The Country1Document4 pagesBasic Economic Problems of The Country1Heaven SyNo ratings yet

- Introduction To EconomicsDocument36 pagesIntroduction To EconomicsLea Guico100% (1)

- Economics - Intro - NotesDocument13 pagesEconomics - Intro - NotesAbdur RahmanNo ratings yet

- Fundamental Concepts of EconomicsDocument66 pagesFundamental Concepts of EconomicsUwuigbe UwalomwaNo ratings yet

- 6 Introduction To EconomicsDocument9 pages6 Introduction To EconomicsDeependra NigamNo ratings yet

- Unit 1-ADocument37 pagesUnit 1-Aobodyqwerty123No ratings yet

- Economics Essay On ScarcityDocument2 pagesEconomics Essay On ScarcityRayden Tan50% (4)

- Economics Chapter 1-13 NotesIGCSEDocument19 pagesEconomics Chapter 1-13 NotesIGCSEyambenari21No ratings yet

- Chap 2 M1Document9 pagesChap 2 M1science boyNo ratings yet

- Scarcity and Efficiency Refers To The Twin Themes of EconomicsDocument9 pagesScarcity and Efficiency Refers To The Twin Themes of EconomicsYuva Prakash83% (6)

- Notes On All TopicsDocument56 pagesNotes On All TopicspotpalNo ratings yet

- Management: Advance Diploma LevelDocument7 pagesManagement: Advance Diploma LevelmerusaNo ratings yet

- Slide 1Document4 pagesSlide 1Jeffrey CardonaNo ratings yet

- Basic Economic ProblemDocument4 pagesBasic Economic ProblemBrigit MartinezNo ratings yet

- Economics Cheat SheetDocument3 pagesEconomics Cheat SheetMushfiq Jahan KhanNo ratings yet

- Basic Concepts of EconomicsDocument35 pagesBasic Concepts of Economicsmahmud.anindoNo ratings yet

- Summary Of "Economics, Principles And Applications" By Mochón & Becker: UNIVERSITY SUMMARIESFrom EverandSummary Of "Economics, Principles And Applications" By Mochón & Becker: UNIVERSITY SUMMARIESNo ratings yet

- Infs1602 Assignment Part A - Final Release - cr2Document5 pagesInfs1602 Assignment Part A - Final Release - cr2Ellia ChenNo ratings yet

- Fins1613 FormulasDocument7 pagesFins1613 FormulasEllia ChenNo ratings yet

- Skills: HSC Course Outcomes Content 11.1 Identify Data Sources ToDocument4 pagesSkills: HSC Course Outcomes Content 11.1 Identify Data Sources ToEllia ChenNo ratings yet

- Definitions: 1. Production of MaterialsDocument1 pageDefinitions: 1. Production of MaterialsEllia ChenNo ratings yet

- Suvigya: Details Furnished by You WereDocument1 pageSuvigya: Details Furnished by You WereMKMK JilaniNo ratings yet

- Lyrics - More Than AbleDocument2 pagesLyrics - More Than AbleZarita CarranzaNo ratings yet

- Word Form KeyDocument2 pagesWord Form KeyHoang Quynh AnhNo ratings yet

- 2021 WA2 Science (Physics) 3E ModifiedDocument13 pages2021 WA2 Science (Physics) 3E ModifiedfinNo ratings yet

- Davis Michael 1A Resume 1Document1 pageDavis Michael 1A Resume 1Alyssa HowellNo ratings yet

- Palanca vs. CADocument16 pagesPalanca vs. CASherwin Anoba CabutijaNo ratings yet

- Jersey Documentation 1.0.3 User GuideDocument35 pagesJersey Documentation 1.0.3 User Guidenaresh921No ratings yet

- Problem StatementDocument15 pagesProblem Statementcabamaro100% (3)

- The RC Oscillator CircuitDocument6 pagesThe RC Oscillator CircuitNishanthi BheemanNo ratings yet

- Angela SolikovaDocument10 pagesAngela SolikovaGirisha PathakNo ratings yet

- Experimental and CFD Resistance Calculation of A Small Fast CatamaranDocument7 pagesExperimental and CFD Resistance Calculation of A Small Fast CatamaranChandra SibaraniNo ratings yet

- Enfermedades Emergentes y Embarazo - EID - November 2006 - Volume CompletoDocument187 pagesEnfermedades Emergentes y Embarazo - EID - November 2006 - Volume CompletoRuth Vargas GonzalesNo ratings yet

- The Impact of Different Political Beliefs On The Family Relationship of College-StudentsDocument16 pagesThe Impact of Different Political Beliefs On The Family Relationship of College-Studentshue sandovalNo ratings yet

- Financial Statement Coronation NightDocument8 pagesFinancial Statement Coronation NightRuel Gapuz ManzanoNo ratings yet

- Learning Competency (Essential Competency) : Let's Recall (Review)Document6 pagesLearning Competency (Essential Competency) : Let's Recall (Review)Heidee BasasNo ratings yet

- Duration: 90 Days.: Fico Training ProgramDocument15 pagesDuration: 90 Days.: Fico Training ProgramMohammed Nawaz ShariffNo ratings yet

- Global Guidelines For The Prevention of Surgical Site Infection: An IntroductionDocument8 pagesGlobal Guidelines For The Prevention of Surgical Site Infection: An IntroductionJNUHospital NABHNo ratings yet

- ED6008Document4 pagesED6008VolvoxdjNo ratings yet

- PestelDocument2 pagesPestelSruthi DNo ratings yet

- UIL Calculator Applications Study ListDocument7 pagesUIL Calculator Applications Study ListRocket FireNo ratings yet

- Party Facility: Atty. Serrano LTD Lecture - July 12 Jzel EndozoDocument7 pagesParty Facility: Atty. Serrano LTD Lecture - July 12 Jzel EndozoJVLNo ratings yet

- CPD and Contracted PelvisDocument53 pagesCPD and Contracted Pelvismaxim tomuNo ratings yet

- RA 020 Risk Assessment - Risk Assessment - Installation of Cables in Ducts & TrenchesDocument11 pagesRA 020 Risk Assessment - Risk Assessment - Installation of Cables in Ducts & Trenchesthomson100% (2)

- English - Fine - Tune Your English 2019Document3 pagesEnglish - Fine - Tune Your English 2019NishaNo ratings yet

- LoB Player Guide Pyram KingDocument15 pagesLoB Player Guide Pyram KingRonaldo SilveiraNo ratings yet

- Steamshovel Press Issue 04Document60 pagesSteamshovel Press Issue 04liondog1No ratings yet