Buy Electrotherm India LTD

Buy Electrotherm India LTD

You might also like

- Sun Microsystems Case PDFDocument30 pagesSun Microsystems Case PDFJasdeep SinghNo ratings yet

- Sun Microsystems Case JasdeepDocument6 pagesSun Microsystems Case JasdeepJasdeep SinghNo ratings yet

- Intuit ValuationDocument4 pagesIntuit ValuationcorvettejrwNo ratings yet

- Chapter 1: Investment Recommendation: How We Have Derived The Summed Up ValueDocument4 pagesChapter 1: Investment Recommendation: How We Have Derived The Summed Up ValueMd. Mehedi HasanNo ratings yet

- Mergers and Acquisition: Presented By, Vinay Kumar Kashyap AnanthramanDocument9 pagesMergers and Acquisition: Presented By, Vinay Kumar Kashyap AnanthramanKashyap AnantharamanNo ratings yet

- Torrent Power - Strategy Implementation: Introduction To The Indian Power IndustryDocument7 pagesTorrent Power - Strategy Implementation: Introduction To The Indian Power IndustryPriyank Acharya100% (1)

- Bhel CompititorDocument3 pagesBhel CompititorabdulrahmanjameelNo ratings yet

- Mumbai, May 5: Its Now Official. Chinese Dragon Has Posed A Serious Challenge To The IndianDocument3 pagesMumbai, May 5: Its Now Official. Chinese Dragon Has Posed A Serious Challenge To The IndianabdulrahmanjameelNo ratings yet

- IOL Chemicals & Pharmaceuticals Ltd. Company Report Card-StandaloneDocument4 pagesIOL Chemicals & Pharmaceuticals Ltd. Company Report Card-StandaloneVenkatesh VasudevanNo ratings yet

- HDFC EquityDocument6 pagesHDFC EquityDarshan ShettyNo ratings yet

- Sca POWERPLANTDocument1 pageSca POWERPLANTAbinash PattanaikNo ratings yet

- BLUE STAR LTD - Quantamental Equity Research Report-1Document1 pageBLUE STAR LTD - Quantamental Equity Research Report-1Vivek NambiarNo ratings yet

- Sterlite Technologies - Q4'10 Result Update - (23!04!2010)Document3 pagesSterlite Technologies - Q4'10 Result Update - (23!04!2010)kotler_2006No ratings yet

- Kim's Trade Summary and StatisticsDocument3 pagesKim's Trade Summary and StatisticsSiméon MorelloNo ratings yet

- America'S Top Companies: Available On The IpadDocument4 pagesAmerica'S Top Companies: Available On The IpadMichele KongNo ratings yet

- Group - 4 PPT DraftDocument15 pagesGroup - 4 PPT Draftrufus carvalhoNo ratings yet

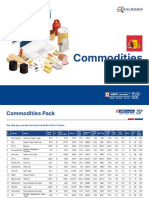

- HSL - Commodities Pack Report - 2021-202108182348310059173Document16 pagesHSL - Commodities Pack Report - 2021-202108182348310059173SHAIK AHMEDNo ratings yet

- Stock Cues: Amara Raja Batteries Ltd. Company Report Card-StandaloneDocument3 pagesStock Cues: Amara Raja Batteries Ltd. Company Report Card-StandalonekukkujiNo ratings yet

- Teaser CdNetDocument10 pagesTeaser CdNetfarhansadique29No ratings yet

- LKP Moldtek 01feb08Document2 pagesLKP Moldtek 01feb08nillchopraNo ratings yet

- Mar-19 Dec-18 Sep-18 Jun-18 Figures in Rs CroreDocument12 pagesMar-19 Dec-18 Sep-18 Jun-18 Figures in Rs Croreneha singhNo ratings yet

- Equty Analysis by Rameez Fazal Tayyeba JayanthDocument17 pagesEquty Analysis by Rameez Fazal Tayyeba JayanthtayyebaNo ratings yet

- Corporate Valuation: Tata Motors LTDDocument10 pagesCorporate Valuation: Tata Motors LTDUTKARSH PABALENo ratings yet

- Acc205 Ca3Document18 pagesAcc205 Ca3Sabab ZamanNo ratings yet

- ValueResearchFundcard RelianceGrowth 2010dec30Document6 pagesValueResearchFundcard RelianceGrowth 2010dec30Maulik DoshiNo ratings yet

- Final Project For Marketing PuneetDocument21 pagesFinal Project For Marketing PuneetSankalp KayathNo ratings yet

- 9e Maruti Suzuki FMDocument2 pages9e Maruti Suzuki FMDedhia Vatsal hiteshNo ratings yet

- Long Term SIP Picks Jan 23Document15 pagesLong Term SIP Picks Jan 23sbvaNo ratings yet

- MOIL 07feb20 Kotak PCG 00210 PDFDocument6 pagesMOIL 07feb20 Kotak PCG 00210 PDFdarshanmadeNo ratings yet

- SynopsisDocument1 pageSynopsisntkmistryNo ratings yet

- Reliance Relative ValuationDocument15 pagesReliance Relative ValuationHEM BANSALNo ratings yet

- Corp FinDocument32 pagesCorp FinsivagabbiNo ratings yet

- Amara Raja Batteries LTD: 1Q FY11 ResultsDocument5 pagesAmara Raja Batteries LTD: 1Q FY11 ResultsveguruprasadNo ratings yet

- Project GlassDocument4 pagesProject GlassAbhishek ChaturvediNo ratings yet

- Hindustan Aeronautics LTD.: BY Gurnoor Singh MBA-2CDocument18 pagesHindustan Aeronautics LTD.: BY Gurnoor Singh MBA-2CHIMANSHU RAWATNo ratings yet

- Standalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Document8 pagesStandalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Group 5A - STERLITE, THOOTHUKUDIDocument18 pagesGroup 5A - STERLITE, THOOTHUKUDIJoseph KuncheriaNo ratings yet

- To Find Out The Market Potential of Renovation & Modernization and Life Extension in Power PlantsDocument19 pagesTo Find Out The Market Potential of Renovation & Modernization and Life Extension in Power PlantsPiyushSahuNo ratings yet

- Kim's Trade Summary and StatisticsDocument13 pagesKim's Trade Summary and StatisticsSiméon MorelloNo ratings yet

- ValueResearchFundcard CanaraRobecoEquityTaxSaver 2010dec27Document6 pagesValueResearchFundcard CanaraRobecoEquityTaxSaver 2010dec27Prakash SainiNo ratings yet

- Watchlist - 28 Nov WeekDocument8 pagesWatchlist - 28 Nov WeekGohanNo ratings yet

- Fundamental Analysis of ACCDocument10 pagesFundamental Analysis of ACCmandeep_hs7698100% (2)

- 09b Valuation2Document8 pages09b Valuation2david AbotsitseNo ratings yet

- CTBCM - Opertunities and ChallengesDocument5 pagesCTBCM - Opertunities and ChallengesMuhammad afzaalNo ratings yet

- ValueResearchFundcard PrincipalPersonalTaxSaver 2010nov09Document6 pagesValueResearchFundcard PrincipalPersonalTaxSaver 2010nov09ksrygNo ratings yet

- Kim's Trade Summary and StatisticsDocument4 pagesKim's Trade Summary and StatisticsSiméon MorelloNo ratings yet

- Generation 0Document1 pageGeneration 0Nathalia BalderamaNo ratings yet

- Equity Portfolio SGDocument208 pagesEquity Portfolio SGdharmendra_kanthariaNo ratings yet

- Coal Lignite Gas Liquid Diesel: Central Electricity Authority Go&Dwing Operation Performance Monitoring DivisionDocument2 pagesCoal Lignite Gas Liquid Diesel: Central Electricity Authority Go&Dwing Operation Performance Monitoring DivisionData CentrumNo ratings yet

- Fundcard: Franklin India Smaller Companies FundDocument4 pagesFundcard: Franklin India Smaller Companies FundChiman RaoNo ratings yet

- Porfolio Rebalancing ReportDocument3 pagesPorfolio Rebalancing ReportAayushi ChandwaniNo ratings yet

- IndustryDocument20 pagesIndustry121prashantNo ratings yet

- ValueResearchFundcard HDFCEquity 2012jul30Document6 pagesValueResearchFundcard HDFCEquity 2012jul30Rachit GoyalNo ratings yet

- ValueResearchFundcard RelianceTaxSaver 2010dec24Document6 pagesValueResearchFundcard RelianceTaxSaver 2010dec24Kumar DeepanshuNo ratings yet

- Top Superstocks of IndiaDocument17 pagesTop Superstocks of IndiaSantoshJammiNo ratings yet

- Indiab Power Adani Power NTPC Reliance Power JSW Energy Tata PowerDocument4 pagesIndiab Power Adani Power NTPC Reliance Power JSW Energy Tata Power1987geoNo ratings yet

- Microsoft ValuationDocument4 pagesMicrosoft ValuationcorvettejrwNo ratings yet

- Jindal Steels & Power LimitedDocument10 pagesJindal Steels & Power LimitedHIMANSHU RAWATNo ratings yet

- ValueResearchFundcard BirlaSunLifeFrontlineEquity 2011apr20Document6 pagesValueResearchFundcard BirlaSunLifeFrontlineEquity 2011apr20Venkatesh VijayakumarNo ratings yet

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- The Brain PDFDocument20 pagesThe Brain PDFDesiree Pescasio DimasuayNo ratings yet

- General Ledger Interview Questions in R12Document9 pagesGeneral Ledger Interview Questions in R12jeedNo ratings yet

- 1 - Chapter 11 - PresentationDocument140 pages1 - Chapter 11 - Presentationyass.methniNo ratings yet

- Talent ManagementDocument6 pagesTalent Managementmovys musicNo ratings yet

- VACANCIES ANNOUNCEMENT STAMICO TPB DMI MNMA MUCE TICD TIB 7 December 2018Document9 pagesVACANCIES ANNOUNCEMENT STAMICO TPB DMI MNMA MUCE TICD TIB 7 December 2018Zegera MgendiNo ratings yet

- HR Consultancy ContractDocument3 pagesHR Consultancy ContractMominaQureshiNo ratings yet

- ACADEMIC WRITING SKILLS - Part 2Document5 pagesACADEMIC WRITING SKILLS - Part 2MWENDA MOSESNo ratings yet

- Dcitionary Errors and SolutionsDocument2 pagesDcitionary Errors and SolutionsGaurav MathurNo ratings yet

- Carbocation - Wikipedia, The Free EncyclopediaDocument5 pagesCarbocation - Wikipedia, The Free EncyclopediaBenni WewokNo ratings yet

- ANC Guidelines - 18 July 2022 - Final-3 (6942)Document238 pagesANC Guidelines - 18 July 2022 - Final-3 (6942)Sara YehiaNo ratings yet

- 1SDA066561R1 A3n 400 TMF 400 4000 3p F FDocument3 pages1SDA066561R1 A3n 400 TMF 400 4000 3p F FJessika duperly rueda vasquezNo ratings yet

- Thank You For The Broken HeartDocument76 pagesThank You For The Broken Heartkaito_shinigamiNo ratings yet

- Tai Wai Maintenance Center: Planning, Design, and ConstructionDocument7 pagesTai Wai Maintenance Center: Planning, Design, and ConstructionSomesh SiddharthNo ratings yet

- Chemistry Project Project-2Document21 pagesChemistry Project Project-2Jijin SajeevNo ratings yet

- Slice Account Statement - May '22Document5 pagesSlice Account Statement - May '22Anil kumar kamathNo ratings yet

- Creating A Windows 10 Boot Drive Is Easy Peasy. Here's How: Use Microsoft's Media Creation ToolDocument9 pagesCreating A Windows 10 Boot Drive Is Easy Peasy. Here's How: Use Microsoft's Media Creation TooljayaramanrathnamNo ratings yet

- Method Statement For Survey WorksDocument13 pagesMethod Statement For Survey WorksSagun Almario100% (1)

- Earth Science: Safety Precautions Before, During, and After Volcanic EruptionDocument33 pagesEarth Science: Safety Precautions Before, During, and After Volcanic Eruptionrhalf tagaduarNo ratings yet

- OPNAV Correspondence Writing GuideDocument38 pagesOPNAV Correspondence Writing Guideroger_roland_1No ratings yet

- SBQ On Globalization in SingaporeDocument4 pagesSBQ On Globalization in SingaporeMegan NgNo ratings yet

- Hsu Early Printing Egypt Vol1Document198 pagesHsu Early Printing Egypt Vol1dln2510No ratings yet

- VaricoceleDocument4 pagesVaricoceleRahajeng Ainiken PutririmasariNo ratings yet

- Lec 1-Vapor Liquid Equilibrium-Part 1Document30 pagesLec 1-Vapor Liquid Equilibrium-Part 1DianaNo ratings yet

- KimDocument104 pagesKimBayby SiZzle'zNo ratings yet

- Foreign Debt, Balance of Payments, and The Economic Crisis of The Philippines in 1983-84Document26 pagesForeign Debt, Balance of Payments, and The Economic Crisis of The Philippines in 1983-84Cielo GriñoNo ratings yet

- Welcome To Presentation On Discharge of SuretyDocument18 pagesWelcome To Presentation On Discharge of SuretyAmit Gurav94% (16)

- The Cumulative Frequency Graph Shows The Amount of Time in Minutes, 200 Students Spend Waiting For Their Train On A Particular MorningDocument8 pagesThe Cumulative Frequency Graph Shows The Amount of Time in Minutes, 200 Students Spend Waiting For Their Train On A Particular MorningJonathanNo ratings yet

- How To Upgrade TP-Link Pharos DevicesDocument5 pagesHow To Upgrade TP-Link Pharos DevicesGina LópezNo ratings yet

- Mathey Wireline UnitsDocument1 pageMathey Wireline UnitsTri CahyadiNo ratings yet

- Concrete Canvas Data SheetDocument1 pageConcrete Canvas Data SheetSeasonNo ratings yet

Download as pdf or txt

You might also like

- Sun Microsystems Case PDFDocument30 pagesSun Microsystems Case PDFJasdeep SinghNo ratings yet

- Sun Microsystems Case JasdeepDocument6 pagesSun Microsystems Case JasdeepJasdeep SinghNo ratings yet

- Intuit ValuationDocument4 pagesIntuit ValuationcorvettejrwNo ratings yet

- Chapter 1: Investment Recommendation: How We Have Derived The Summed Up ValueDocument4 pagesChapter 1: Investment Recommendation: How We Have Derived The Summed Up ValueMd. Mehedi HasanNo ratings yet

- Mergers and Acquisition: Presented By, Vinay Kumar Kashyap AnanthramanDocument9 pagesMergers and Acquisition: Presented By, Vinay Kumar Kashyap AnanthramanKashyap AnantharamanNo ratings yet

- Torrent Power - Strategy Implementation: Introduction To The Indian Power IndustryDocument7 pagesTorrent Power - Strategy Implementation: Introduction To The Indian Power IndustryPriyank Acharya100% (1)

- Bhel CompititorDocument3 pagesBhel CompititorabdulrahmanjameelNo ratings yet

- Mumbai, May 5: Its Now Official. Chinese Dragon Has Posed A Serious Challenge To The IndianDocument3 pagesMumbai, May 5: Its Now Official. Chinese Dragon Has Posed A Serious Challenge To The IndianabdulrahmanjameelNo ratings yet

- IOL Chemicals & Pharmaceuticals Ltd. Company Report Card-StandaloneDocument4 pagesIOL Chemicals & Pharmaceuticals Ltd. Company Report Card-StandaloneVenkatesh VasudevanNo ratings yet

- HDFC EquityDocument6 pagesHDFC EquityDarshan ShettyNo ratings yet

- Sca POWERPLANTDocument1 pageSca POWERPLANTAbinash PattanaikNo ratings yet

- BLUE STAR LTD - Quantamental Equity Research Report-1Document1 pageBLUE STAR LTD - Quantamental Equity Research Report-1Vivek NambiarNo ratings yet

- Sterlite Technologies - Q4'10 Result Update - (23!04!2010)Document3 pagesSterlite Technologies - Q4'10 Result Update - (23!04!2010)kotler_2006No ratings yet

- Kim's Trade Summary and StatisticsDocument3 pagesKim's Trade Summary and StatisticsSiméon MorelloNo ratings yet

- America'S Top Companies: Available On The IpadDocument4 pagesAmerica'S Top Companies: Available On The IpadMichele KongNo ratings yet

- Group - 4 PPT DraftDocument15 pagesGroup - 4 PPT Draftrufus carvalhoNo ratings yet

- HSL - Commodities Pack Report - 2021-202108182348310059173Document16 pagesHSL - Commodities Pack Report - 2021-202108182348310059173SHAIK AHMEDNo ratings yet

- Stock Cues: Amara Raja Batteries Ltd. Company Report Card-StandaloneDocument3 pagesStock Cues: Amara Raja Batteries Ltd. Company Report Card-StandalonekukkujiNo ratings yet

- Teaser CdNetDocument10 pagesTeaser CdNetfarhansadique29No ratings yet

- LKP Moldtek 01feb08Document2 pagesLKP Moldtek 01feb08nillchopraNo ratings yet

- Mar-19 Dec-18 Sep-18 Jun-18 Figures in Rs CroreDocument12 pagesMar-19 Dec-18 Sep-18 Jun-18 Figures in Rs Croreneha singhNo ratings yet

- Equty Analysis by Rameez Fazal Tayyeba JayanthDocument17 pagesEquty Analysis by Rameez Fazal Tayyeba JayanthtayyebaNo ratings yet

- Corporate Valuation: Tata Motors LTDDocument10 pagesCorporate Valuation: Tata Motors LTDUTKARSH PABALENo ratings yet

- Acc205 Ca3Document18 pagesAcc205 Ca3Sabab ZamanNo ratings yet

- ValueResearchFundcard RelianceGrowth 2010dec30Document6 pagesValueResearchFundcard RelianceGrowth 2010dec30Maulik DoshiNo ratings yet

- Final Project For Marketing PuneetDocument21 pagesFinal Project For Marketing PuneetSankalp KayathNo ratings yet

- 9e Maruti Suzuki FMDocument2 pages9e Maruti Suzuki FMDedhia Vatsal hiteshNo ratings yet

- Long Term SIP Picks Jan 23Document15 pagesLong Term SIP Picks Jan 23sbvaNo ratings yet

- MOIL 07feb20 Kotak PCG 00210 PDFDocument6 pagesMOIL 07feb20 Kotak PCG 00210 PDFdarshanmadeNo ratings yet

- SynopsisDocument1 pageSynopsisntkmistryNo ratings yet

- Reliance Relative ValuationDocument15 pagesReliance Relative ValuationHEM BANSALNo ratings yet

- Corp FinDocument32 pagesCorp FinsivagabbiNo ratings yet

- Amara Raja Batteries LTD: 1Q FY11 ResultsDocument5 pagesAmara Raja Batteries LTD: 1Q FY11 ResultsveguruprasadNo ratings yet

- Project GlassDocument4 pagesProject GlassAbhishek ChaturvediNo ratings yet

- Hindustan Aeronautics LTD.: BY Gurnoor Singh MBA-2CDocument18 pagesHindustan Aeronautics LTD.: BY Gurnoor Singh MBA-2CHIMANSHU RAWATNo ratings yet

- Standalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Document8 pagesStandalone & Consolidated Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Group 5A - STERLITE, THOOTHUKUDIDocument18 pagesGroup 5A - STERLITE, THOOTHUKUDIJoseph KuncheriaNo ratings yet

- To Find Out The Market Potential of Renovation & Modernization and Life Extension in Power PlantsDocument19 pagesTo Find Out The Market Potential of Renovation & Modernization and Life Extension in Power PlantsPiyushSahuNo ratings yet

- Kim's Trade Summary and StatisticsDocument13 pagesKim's Trade Summary and StatisticsSiméon MorelloNo ratings yet

- ValueResearchFundcard CanaraRobecoEquityTaxSaver 2010dec27Document6 pagesValueResearchFundcard CanaraRobecoEquityTaxSaver 2010dec27Prakash SainiNo ratings yet

- Watchlist - 28 Nov WeekDocument8 pagesWatchlist - 28 Nov WeekGohanNo ratings yet

- Fundamental Analysis of ACCDocument10 pagesFundamental Analysis of ACCmandeep_hs7698100% (2)

- 09b Valuation2Document8 pages09b Valuation2david AbotsitseNo ratings yet

- CTBCM - Opertunities and ChallengesDocument5 pagesCTBCM - Opertunities and ChallengesMuhammad afzaalNo ratings yet

- ValueResearchFundcard PrincipalPersonalTaxSaver 2010nov09Document6 pagesValueResearchFundcard PrincipalPersonalTaxSaver 2010nov09ksrygNo ratings yet

- Kim's Trade Summary and StatisticsDocument4 pagesKim's Trade Summary and StatisticsSiméon MorelloNo ratings yet

- Generation 0Document1 pageGeneration 0Nathalia BalderamaNo ratings yet

- Equity Portfolio SGDocument208 pagesEquity Portfolio SGdharmendra_kanthariaNo ratings yet

- Coal Lignite Gas Liquid Diesel: Central Electricity Authority Go&Dwing Operation Performance Monitoring DivisionDocument2 pagesCoal Lignite Gas Liquid Diesel: Central Electricity Authority Go&Dwing Operation Performance Monitoring DivisionData CentrumNo ratings yet

- Fundcard: Franklin India Smaller Companies FundDocument4 pagesFundcard: Franklin India Smaller Companies FundChiman RaoNo ratings yet

- Porfolio Rebalancing ReportDocument3 pagesPorfolio Rebalancing ReportAayushi ChandwaniNo ratings yet

- IndustryDocument20 pagesIndustry121prashantNo ratings yet

- ValueResearchFundcard HDFCEquity 2012jul30Document6 pagesValueResearchFundcard HDFCEquity 2012jul30Rachit GoyalNo ratings yet

- ValueResearchFundcard RelianceTaxSaver 2010dec24Document6 pagesValueResearchFundcard RelianceTaxSaver 2010dec24Kumar DeepanshuNo ratings yet

- Top Superstocks of IndiaDocument17 pagesTop Superstocks of IndiaSantoshJammiNo ratings yet

- Indiab Power Adani Power NTPC Reliance Power JSW Energy Tata PowerDocument4 pagesIndiab Power Adani Power NTPC Reliance Power JSW Energy Tata Power1987geoNo ratings yet

- Microsoft ValuationDocument4 pagesMicrosoft ValuationcorvettejrwNo ratings yet

- Jindal Steels & Power LimitedDocument10 pagesJindal Steels & Power LimitedHIMANSHU RAWATNo ratings yet

- ValueResearchFundcard BirlaSunLifeFrontlineEquity 2011apr20Document6 pagesValueResearchFundcard BirlaSunLifeFrontlineEquity 2011apr20Venkatesh VijayakumarNo ratings yet

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- The Brain PDFDocument20 pagesThe Brain PDFDesiree Pescasio DimasuayNo ratings yet

- General Ledger Interview Questions in R12Document9 pagesGeneral Ledger Interview Questions in R12jeedNo ratings yet

- 1 - Chapter 11 - PresentationDocument140 pages1 - Chapter 11 - Presentationyass.methniNo ratings yet

- Talent ManagementDocument6 pagesTalent Managementmovys musicNo ratings yet

- VACANCIES ANNOUNCEMENT STAMICO TPB DMI MNMA MUCE TICD TIB 7 December 2018Document9 pagesVACANCIES ANNOUNCEMENT STAMICO TPB DMI MNMA MUCE TICD TIB 7 December 2018Zegera MgendiNo ratings yet

- HR Consultancy ContractDocument3 pagesHR Consultancy ContractMominaQureshiNo ratings yet

- ACADEMIC WRITING SKILLS - Part 2Document5 pagesACADEMIC WRITING SKILLS - Part 2MWENDA MOSESNo ratings yet

- Dcitionary Errors and SolutionsDocument2 pagesDcitionary Errors and SolutionsGaurav MathurNo ratings yet

- Carbocation - Wikipedia, The Free EncyclopediaDocument5 pagesCarbocation - Wikipedia, The Free EncyclopediaBenni WewokNo ratings yet

- ANC Guidelines - 18 July 2022 - Final-3 (6942)Document238 pagesANC Guidelines - 18 July 2022 - Final-3 (6942)Sara YehiaNo ratings yet

- 1SDA066561R1 A3n 400 TMF 400 4000 3p F FDocument3 pages1SDA066561R1 A3n 400 TMF 400 4000 3p F FJessika duperly rueda vasquezNo ratings yet

- Thank You For The Broken HeartDocument76 pagesThank You For The Broken Heartkaito_shinigamiNo ratings yet

- Tai Wai Maintenance Center: Planning, Design, and ConstructionDocument7 pagesTai Wai Maintenance Center: Planning, Design, and ConstructionSomesh SiddharthNo ratings yet

- Chemistry Project Project-2Document21 pagesChemistry Project Project-2Jijin SajeevNo ratings yet

- Slice Account Statement - May '22Document5 pagesSlice Account Statement - May '22Anil kumar kamathNo ratings yet

- Creating A Windows 10 Boot Drive Is Easy Peasy. Here's How: Use Microsoft's Media Creation ToolDocument9 pagesCreating A Windows 10 Boot Drive Is Easy Peasy. Here's How: Use Microsoft's Media Creation TooljayaramanrathnamNo ratings yet

- Method Statement For Survey WorksDocument13 pagesMethod Statement For Survey WorksSagun Almario100% (1)

- Earth Science: Safety Precautions Before, During, and After Volcanic EruptionDocument33 pagesEarth Science: Safety Precautions Before, During, and After Volcanic Eruptionrhalf tagaduarNo ratings yet

- OPNAV Correspondence Writing GuideDocument38 pagesOPNAV Correspondence Writing Guideroger_roland_1No ratings yet

- SBQ On Globalization in SingaporeDocument4 pagesSBQ On Globalization in SingaporeMegan NgNo ratings yet

- Hsu Early Printing Egypt Vol1Document198 pagesHsu Early Printing Egypt Vol1dln2510No ratings yet

- VaricoceleDocument4 pagesVaricoceleRahajeng Ainiken PutririmasariNo ratings yet

- Lec 1-Vapor Liquid Equilibrium-Part 1Document30 pagesLec 1-Vapor Liquid Equilibrium-Part 1DianaNo ratings yet

- KimDocument104 pagesKimBayby SiZzle'zNo ratings yet

- Foreign Debt, Balance of Payments, and The Economic Crisis of The Philippines in 1983-84Document26 pagesForeign Debt, Balance of Payments, and The Economic Crisis of The Philippines in 1983-84Cielo GriñoNo ratings yet

- Welcome To Presentation On Discharge of SuretyDocument18 pagesWelcome To Presentation On Discharge of SuretyAmit Gurav94% (16)

- The Cumulative Frequency Graph Shows The Amount of Time in Minutes, 200 Students Spend Waiting For Their Train On A Particular MorningDocument8 pagesThe Cumulative Frequency Graph Shows The Amount of Time in Minutes, 200 Students Spend Waiting For Their Train On A Particular MorningJonathanNo ratings yet

- How To Upgrade TP-Link Pharos DevicesDocument5 pagesHow To Upgrade TP-Link Pharos DevicesGina LópezNo ratings yet

- Mathey Wireline UnitsDocument1 pageMathey Wireline UnitsTri CahyadiNo ratings yet

- Concrete Canvas Data SheetDocument1 pageConcrete Canvas Data SheetSeasonNo ratings yet