Download as pdf or txt

You might also like

- HW 4 - R Chapter 6 SpenceDocument7 pagesHW 4 - R Chapter 6 SpenceMorgan Spence0% (1)

- Six Research FrameworksDocument12 pagesSix Research FrameworkscoachhandNo ratings yet

- Principal-Agent Final PaperDocument74 pagesPrincipal-Agent Final Paperangelocarlorosario100% (4)

- Geoffs Private Pilot Study GuideDocument28 pagesGeoffs Private Pilot Study Guideajcd110No ratings yet

- Percipitation: Rainfall Data AnalysisDocument18 pagesPercipitation: Rainfall Data AnalysiswanradhiahNo ratings yet

- 1Document2 pages1KaeNo ratings yet

- The Nature of Accounting Theory and The Development of TheoryDocument6 pagesThe Nature of Accounting Theory and The Development of TheoryEngrAbeer Arif100% (1)

- Insider Outsider TheoryDocument21 pagesInsider Outsider TheorysukandeNo ratings yet

- Seminar Paper - CDT - Ralph HartungDocument11 pagesSeminar Paper - CDT - Ralph HartungRalph HartungNo ratings yet

- Research Tools and Techniques Assignment Farah Ashraf SP17-BBA-051Document5 pagesResearch Tools and Techniques Assignment Farah Ashraf SP17-BBA-051Farah AshrafNo ratings yet

- Combining ForecastsDocument5 pagesCombining ForecastsAlexander SanchezNo ratings yet

- Heuristics in Decision MakingDocument12 pagesHeuristics in Decision MakingAsty AstitiNo ratings yet

- Research: Business Research Research Process Approaches To ResearchDocument8 pagesResearch: Business Research Research Process Approaches To ResearchMuhammad Faiq SiddiquiNo ratings yet

- Example For Questions QM AnswersDocument5 pagesExample For Questions QM AnswersempirechocoNo ratings yet

- Research Concept PaperDocument12 pagesResearch Concept PaperATI BUDGETNo ratings yet

- Hassan Forecasting PrinciplesDocument8 pagesHassan Forecasting PrinciplesscribdzippotNo ratings yet

- Research Tools and Techniques Assignment Farah Ashraf SP17-BBA-051Document5 pagesResearch Tools and Techniques Assignment Farah Ashraf SP17-BBA-051Farah AshrafNo ratings yet

- GSLC Research MetodologyDocument4 pagesGSLC Research MetodologyIvan TrisnioNo ratings yet

- Chapter 2 TemplateDocument4 pagesChapter 2 TemplateVanna SEARTNo ratings yet

- The Role of Accounting TheoryDocument13 pagesThe Role of Accounting TheoryemmaNo ratings yet

- Concepts of e-HRM Consequences: A Categorisation, Review and SuggestionDocument17 pagesConcepts of e-HRM Consequences: A Categorisation, Review and SuggestionMd Shawfiqul IslamNo ratings yet

- 10 Experimental Learning GuideDocument5 pages10 Experimental Learning GuideDewa PutraNo ratings yet

- CH01 WithfiguresDocument18 pagesCH01 Withfiguresmrvaskez100% (1)

- The Peter Principle: A Theory of Decline: Edward P. LazearDocument24 pagesThe Peter Principle: A Theory of Decline: Edward P. LazearRoso DelimaNo ratings yet

- Solution IMT-120 3Document8 pagesSolution IMT-120 3Kishor kumar BhatiaNo ratings yet

- SLM - PDF - Unit 7Document21 pagesSLM - PDF - Unit 7RanzNo ratings yet

- Propensity Score MatchingDocument40 pagesPropensity Score MatchingMizter. A. KnightsNo ratings yet

- An Alternative Approach of Handling The Outlier: A Case With Indian NPSDocument22 pagesAn Alternative Approach of Handling The Outlier: A Case With Indian NPSSoumen SarkarNo ratings yet

- Accounting TheoryDocument5 pagesAccounting TheoryToluwalope BamideleNo ratings yet

- Theoretical Framework and Hypothesis DevelopmentDocument26 pagesTheoretical Framework and Hypothesis DevelopmenthenatabassumNo ratings yet

- Industrial and Managerial Economics Assignment-1Document18 pagesIndustrial and Managerial Economics Assignment-1Kunal RawatNo ratings yet

- Mixing Other Methods With Simulation IsDocument7 pagesMixing Other Methods With Simulation IsAli MejbriNo ratings yet

- Reading For The Pay Moocs: (Neil Conway and Andrew Eriksen-Brown 2016)Document10 pagesReading For The Pay Moocs: (Neil Conway and Andrew Eriksen-Brown 2016)Anees AhmedNo ratings yet

- WKo Hyq 87 U Ps IWH975 C WODocument17 pagesWKo Hyq 87 U Ps IWH975 C WOakhilsharmac1140No ratings yet

- Methodology of EconomicsDocument14 pagesMethodology of EconomicspraveenNo ratings yet

- 1st MidtermDocument9 pages1st MidtermMD Hafizul Islam HafizNo ratings yet

- Methods in Business ResearchDocument66 pagesMethods in Business ResearchosamaNo ratings yet

- Demand ForecastingDocument17 pagesDemand ForecastingPoonam SatapathyNo ratings yet

- Name: Bamidele Toluwalope CelestinaDocument8 pagesName: Bamidele Toluwalope CelestinaToluwalope BamideleNo ratings yet

- Andrew Gelman - The Problem With P-Values - AddendumDocument3 pagesAndrew Gelman - The Problem With P-Values - AddendumLoki OdinsonNo ratings yet

- Cultivating Your Judgement SkillsDocument14 pagesCultivating Your Judgement SkillsmystearicaNo ratings yet

- My Report Balance Theory2023Document26 pagesMy Report Balance Theory2023Judy Ann FunitNo ratings yet

- BFA715 Workshop 1 Solutions and DiscussionDocument24 pagesBFA715 Workshop 1 Solutions and Discussionyizhi liuNo ratings yet

- 56 - Organizational Behaviour-Pearson Education Limited (2020)Document5 pages56 - Organizational Behaviour-Pearson Education Limited (2020)mozam haqNo ratings yet

- Daniels Cap 1Document19 pagesDaniels Cap 1Samuel AraújoNo ratings yet

- What Is The Significance of Research in Social and Business Sciences?Document7 pagesWhat Is The Significance of Research in Social and Business Sciences?sid007.earth6327No ratings yet

- I) Define Research. How Does Research Facilitate Decision Making. I) Explain The Emerging Trends in Business ResearchDocument15 pagesI) Define Research. How Does Research Facilitate Decision Making. I) Explain The Emerging Trends in Business ResearchRahul MoreNo ratings yet

- Psy 3711 First Midterm QuestionsDocument14 pagesPsy 3711 First Midterm QuestionsShiv PatelNo ratings yet

- 452 Chapter 06Document38 pages452 Chapter 06Joshua IgbuhayNo ratings yet

- Cap 1 - P1Document5 pagesCap 1 - P1OSMAR JOSHUA VALENZUELA MENDOZANo ratings yet

- Topic 1: Introduction To Principles of Experimental Design: 1. 1. PurposeDocument16 pagesTopic 1: Introduction To Principles of Experimental Design: 1. 1. PurposeSagarias AlbusNo ratings yet

- Book Summary HR AnalyticsDocument25 pagesBook Summary HR AnalyticsMerleNo ratings yet

- CP 206Document390 pagesCP 206kegnataNo ratings yet

- Problem.: Unit of AnalysisDocument36 pagesProblem.: Unit of Analysisso urdip50% (2)

- IOPS 311 Assignment 1Document8 pagesIOPS 311 Assignment 1Dylan BanksNo ratings yet

- Psychologist, 39Document4 pagesPsychologist, 39kevinNo ratings yet

- Systems Thinking Strategy: The New Way to Understand Your Business and Drive PerformanceFrom EverandSystems Thinking Strategy: The New Way to Understand Your Business and Drive PerformanceNo ratings yet

- Digital Project Practice: Managing Innovation and ChangeFrom EverandDigital Project Practice: Managing Innovation and ChangeNo ratings yet

- Metaheuristics Algorithms for Medical Applications: Methods and ApplicationsFrom EverandMetaheuristics Algorithms for Medical Applications: Methods and ApplicationsNo ratings yet

- 4 CHAPTER FOUR ProjectDocument43 pages4 CHAPTER FOUR ProjectOfgaha Alemu100% (1)

- Collection SayingsDocument2 pagesCollection SayingsLessia MiliutenkoNo ratings yet

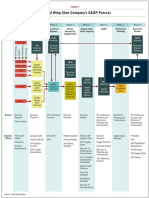

- The Red Wing Shoe Company's S&OP Process: Phase 1 Phase 3 Phase 5 Phase 7Document1 pageThe Red Wing Shoe Company's S&OP Process: Phase 1 Phase 3 Phase 5 Phase 7Uchenna 'Bonex' OgbonnaNo ratings yet

- OM Narrative ReportDocument9 pagesOM Narrative ReportJinx Cyrus RodilloNo ratings yet

- Forecasting & Methods: CE G545 Airport Planning and DesignDocument23 pagesForecasting & Methods: CE G545 Airport Planning and DesignNavik BhandariNo ratings yet

- Book 29Document29 pagesBook 29dinbhatt86% (7)

- NZ USAR Awareness Team Leaders FOG (Print)Document49 pagesNZ USAR Awareness Team Leaders FOG (Print)Shane Briggs100% (2)

- Lecture 12Document33 pagesLecture 12Anamul HaqueNo ratings yet

- 062 Event Based Rainfall-Runoff Simulation Using Hec-Hms Model (2014) (JaybDocument92 pages062 Event Based Rainfall-Runoff Simulation Using Hec-Hms Model (2014) (JaybczartripsNo ratings yet

- Instrumen FaaDocument11 pagesInstrumen FaaditoalmaNo ratings yet

- Daily Prediction of Solar Power GenerationDocument6 pagesDaily Prediction of Solar Power GenerationKávilAvano 44No ratings yet

- Mysterious Australia Newsletter - June 2011Document25 pagesMysterious Australia Newsletter - June 2011Rex and Heather GilroyNo ratings yet

- Cheat SheetDocument5 pagesCheat SheetMNo ratings yet

- Weather Prediction Based On LSTM Model Implemented AWS Machine Learning PlatformDocument10 pagesWeather Prediction Based On LSTM Model Implemented AWS Machine Learning PlatformIJRASETPublications100% (1)

- LOCG-GEN-Guideline-006 Rev 0 - Lift-Off Transportation + Inshore Mating of TopsidesDocument26 pagesLOCG-GEN-Guideline-006 Rev 0 - Lift-Off Transportation + Inshore Mating of TopsidesTomkel VoonNo ratings yet

- PT34 18Document3 pagesPT34 18Ashley DeanNo ratings yet

- WatervizDocument1 pageWatervizConsortium of Universities for the Advancement of Hydrologic Science, Inc.No ratings yet

- BibliographyDocument6 pagesBibliographyrlensch100% (1)

- CH 2 - Frequency Analysis and ForecastingDocument31 pagesCH 2 - Frequency Analysis and ForecastingYaregal Geremew100% (1)

- Apuntes de Ingles - VerbosDocument9 pagesApuntes de Ingles - VerbosJuan Francisco ValeroNo ratings yet

- TR Prep Package Brochure CAEDocument44 pagesTR Prep Package Brochure CAEpintua_1No ratings yet

- Fastclass Test01bDocument5 pagesFastclass Test01bSebastian2007No ratings yet

- Air Pollution Prediction Using Long Short-Term Memory (LSTM) and Deep Autoencoder (DAE) ModelsDocument17 pagesAir Pollution Prediction Using Long Short-Term Memory (LSTM) and Deep Autoencoder (DAE) ModelsChardin Hoyos CordovaNo ratings yet

- Introduction To Wildland Fire Behavior Calculations390RMDocument115 pagesIntroduction To Wildland Fire Behavior Calculations390RMFG Summer100% (1)

- The Tea Industry and A Review of Its Price ModelliDocument17 pagesThe Tea Industry and A Review of Its Price ModelliashishNo ratings yet

- Methods of Demand ForecastingDocument4 pagesMethods of Demand ForecastingSreya PrakashNo ratings yet