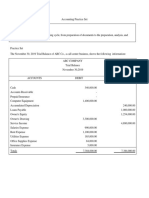

2015 09 Months Financial Report

2015 09 Months Financial Report

You might also like

- Contract of Lease With Special Power of Attorney SampleDocument3 pagesContract of Lease With Special Power of Attorney SampleRuben Luyon100% (1)

- BBMA OA MyEnglishVersion1.1Document79 pagesBBMA OA MyEnglishVersion1.1LAURENT MULLAHNo ratings yet

- 2015 Financial StatementDocument85 pages2015 Financial StatementMiftah IndiraNo ratings yet

- Demonstra??es Financeiras em Padr?es InternacionaisDocument66 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- 3Q15 Financial StatementsDocument43 pages3Q15 Financial StatementsFibriaRINo ratings yet

- Airbus Group Financial Statements 2015Document119 pagesAirbus Group Financial Statements 2015AdrianPedroviejoFernandez100% (1)

- Demonstra??es Financeiras em Padr?es InternacionaisDocument66 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- 2Q15 Financial StatementsDocument43 pages2Q15 Financial StatementsFibriaRINo ratings yet

- Financial Results & Limited Review For June 30, 2015 (Company Update)Document7 pagesFinancial Results & Limited Review For June 30, 2015 (Company Update)Shyam SunderNo ratings yet

- 3 - Sept14 PDFDocument87 pages3 - Sept14 PDFKiim Saii DhaNo ratings yet

- Consolidated2010 FinalDocument79 pagesConsolidated2010 FinalHammna AshrafNo ratings yet

- Unvr - LK Audit 2012Document79 pagesUnvr - LK Audit 2012Abiyyu AhmadNo ratings yet

- Allianz-Ţiriac Asigurări Sa Consolidated Financial Statements Year Ended 31 December 2000Document29 pagesAllianz-Ţiriac Asigurări Sa Consolidated Financial Statements Year Ended 31 December 2000Ovidiu BradatanuNo ratings yet

- Fibria Celulose S.ADocument69 pagesFibria Celulose S.AFibriaRINo ratings yet

- IfrsDocument272 pagesIfrsKisu ShuteNo ratings yet

- 25 Chart of AccountsDocument104 pages25 Chart of AccountsFiania WatungNo ratings yet

- Leucadia 2012 Q3 ReportDocument43 pagesLeucadia 2012 Q3 Reportofb1No ratings yet

- Consolidated Accounts December 31 2011 For Web (Revised) PDFDocument93 pagesConsolidated Accounts December 31 2011 For Web (Revised) PDFElegant EmeraldNo ratings yet

- MCB Consolidated For Year Ended Dec 2011Document87 pagesMCB Consolidated For Year Ended Dec 2011shoaibjeeNo ratings yet

- Shell Pakistan Limited Condensed Interim Financial Information (Unaudited) For The Half Year Ended June 30, 2011Document19 pagesShell Pakistan Limited Condensed Interim Financial Information (Unaudited) For The Half Year Ended June 30, 2011roker_m3No ratings yet

- Items That May Be Reclassified Subsequently To The Profit or LossDocument4 pagesItems That May Be Reclassified Subsequently To The Profit or LossEugene Khoo Sheng ChuanNo ratings yet

- Q4FY2013 Interim ResultsDocument13 pagesQ4FY2013 Interim ResultsrickysuNo ratings yet

- Breeze-Eastern Corporation: Securities and Exchange CommissionDocument31 pagesBreeze-Eastern Corporation: Securities and Exchange Commissionashish822No ratings yet

- 2 PDocument238 pages2 Pbillyryan1100% (3)

- Apple Inc.: Form 10-QDocument53 pagesApple Inc.: Form 10-QSeiha ChhengNo ratings yet

- Financial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Document4 pagesFinancial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderNo ratings yet

- POAL Financial Review 2013Document13 pagesPOAL Financial Review 2013George WoodNo ratings yet

- Myer AR10 Financial ReportDocument50 pagesMyer AR10 Financial ReportMitchell HughesNo ratings yet

- FY2014 - HHI - English FS (Separate) - FIN - 1Document88 pagesFY2014 - HHI - English FS (Separate) - FIN - 1airlanggaputraNo ratings yet

- Demonstra??es Financeiras em Padr?es InternacionaisDocument81 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- CSS Financial Report Web 10-11Document20 pagesCSS Financial Report Web 10-11LIFECommsNo ratings yet

- Ar 11 pt03Document112 pagesAr 11 pt03Muneeb ShahidNo ratings yet

- Cash Flow StatementDocument1 pageCash Flow StatementGENIUS1507No ratings yet

- Announces Q2 Results & Auditors' Report For The Quarter Ended September 30, 2015 (Result)Document4 pagesAnnounces Q2 Results & Auditors' Report For The Quarter Ended September 30, 2015 (Result)Shyam SunderNo ratings yet

- Financial Results & Limited Review Report For June 30, 2015 (Standalone) (Company Update)Document3 pagesFinancial Results & Limited Review Report For June 30, 2015 (Standalone) (Company Update)Shyam SunderNo ratings yet

- Glosario de FinanzasDocument9 pagesGlosario de FinanzasRaúl VargasNo ratings yet

- Airbus Annual ReportDocument201 pagesAirbus Annual ReportfsdfsdfsNo ratings yet

- HBS Investment Limited 2015Document32 pagesHBS Investment Limited 2015Areej FatimaNo ratings yet

- 3Q16 Financial StatementsDocument46 pages3Q16 Financial StatementsFibriaRINo ratings yet

- Cognizant+Technologies+9!30!11+Form+10 Q+ +as+filedDocument55 pagesCognizant+Technologies+9!30!11+Form+10 Q+ +as+filedKalpesh PatilNo ratings yet

- Entah LerDocument62 pagesEntah LerNor Azizuddin Abdul MananNo ratings yet

- FordMotorCompany 10Q 20110805Document102 pagesFordMotorCompany 10Q 20110805Lee LoganNo ratings yet

- JFC 2011 Audited FSDocument82 pagesJFC 2011 Audited FSRegla MarieNo ratings yet

- Bida - Tech Company Statement of Financial Position: As of December 31, Assets 2020 Current AssetsDocument42 pagesBida - Tech Company Statement of Financial Position: As of December 31, Assets 2020 Current AssetsTrisha Mae Mendoza MacalinoNo ratings yet

- Juhayna-Annual Report 2014Document20 pagesJuhayna-Annual Report 2014Wasseem Atalla100% (1)

- Demonstra??es Financeiras em Padr?es InternacionaisDocument62 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- 1Q16 Financial StatementsDocument40 pages1Q16 Financial StatementsFibriaRINo ratings yet

- Demonstra??es Financeiras em Padr?es InternacionaisDocument65 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- DemonstraDocument74 pagesDemonstraFibriaRINo ratings yet

- 1Q15 Financial StatementsDocument42 pages1Q15 Financial StatementsFibriaRINo ratings yet

- MFRS 101 - Ig - 042015Document24 pagesMFRS 101 - Ig - 042015Prasen RajNo ratings yet

- Statement of Financial Position AssetsDocument5 pagesStatement of Financial Position AssetsNindasurnilaPramestiCahyaniNo ratings yet

- Financial Results & Limited Review For Sept 30, 2014 (Standalone) (Result)Document4 pagesFinancial Results & Limited Review For Sept 30, 2014 (Standalone) (Result)Shyam SunderNo ratings yet

- A Wholly Owned Subsidiary of Megaworld CorporationDocument4 pagesA Wholly Owned Subsidiary of Megaworld CorporationAngelo LabiosNo ratings yet

- IDEAL RICE INDUSTRIES AccountsDocument89 pagesIDEAL RICE INDUSTRIES Accountsahmed.zjcNo ratings yet

- DominosPizzaInc Q2-2013Document28 pagesDominosPizzaInc Q2-2013nitin2khNo ratings yet

- YTB 062015 NotesDocument13 pagesYTB 062015 Notesnickong53No ratings yet

- Mills Estruturas e Serviços de Engenharia S.ADocument61 pagesMills Estruturas e Serviços de Engenharia S.AMillsRINo ratings yet

- IFRS For SMEsDocument10 pagesIFRS For SMEsJhemmilyn RiveraNo ratings yet

- A2Z Annual Report 2018Document216 pagesA2Z Annual Report 2018Siddharth ShekharNo ratings yet

- 2017 - 10 - FEV India - Presentation PDFDocument21 pages2017 - 10 - FEV India - Presentation PDFSiddharth ShekharNo ratings yet

- Asha Annual Report - 2015-2016Document134 pagesAsha Annual Report - 2015-2016Siddharth ShekharNo ratings yet

- AOLAnnualReport2016 17Document180 pagesAOLAnnualReport2016 17Siddharth ShekharNo ratings yet

- Annualreport16 17Document215 pagesAnnualreport16 17Siddharth ShekharNo ratings yet

- Annual Report 2015 16Document188 pagesAnnual Report 2015 16Siddharth ShekharNo ratings yet

- Anant Raj Limited321Document12 pagesAnant Raj Limited321Siddharth ShekharNo ratings yet

- Smartlink Annual Report 2015-16-25june2016 1Document84 pagesSmartlink Annual Report 2015-16-25june2016 1Siddharth ShekharNo ratings yet

- 3SB300 0aa11Document3 pages3SB300 0aa11Siddharth ShekharNo ratings yet

- Arihant Superstructures Limited: February 23, 2010 For Equity Shareholders of The Company OnlyDocument176 pagesArihant Superstructures Limited: February 23, 2010 For Equity Shareholders of The Company OnlySiddharth ShekharNo ratings yet

- MSL Annual Report 2015 16Document133 pagesMSL Annual Report 2015 16Siddharth ShekharNo ratings yet

- Manaksia Aluminium Co LTD 2015 16Document68 pagesManaksia Aluminium Co LTD 2015 16Siddharth ShekharNo ratings yet

- AnnualDocument122 pagesAnnualSiddharth ShekharNo ratings yet

- Rain Industries Limited - 40th Annual Report - 2014Document171 pagesRain Industries Limited - 40th Annual Report - 2014Siddharth ShekharNo ratings yet

- Annual Report - Ram Minerals and Chemicals LimitedDocument32 pagesAnnual Report - Ram Minerals and Chemicals LimitedSiddharth ShekharNo ratings yet

- Annual Report For The Year 2016-17Document89 pagesAnnual Report For The Year 2016-17Siddharth ShekharNo ratings yet

- Impact of Foreign Aid On Saving in NigeriaDocument80 pagesImpact of Foreign Aid On Saving in NigeriaTreasured PrinceNo ratings yet

- Essel Propack LTDDocument8 pagesEssel Propack LTDmaheshNo ratings yet

- ABC CompanyDocument11 pagesABC CompanyA DiolataNo ratings yet

- ΠΡΟΚΗΡΥΞΗ ΕΣΠΑ ΝΕΕΣ ΜΜΕ ΑΔΑ - ΨΩΓΚΗ-ΕΥΦDocument235 pagesΠΡΟΚΗΡΥΞΗ ΕΣΠΑ ΝΕΕΣ ΜΜΕ ΑΔΑ - ΨΩΓΚΗ-ΕΥΦaloukeriNo ratings yet

- Business Finance LAS.Q1.WEEK5Document5 pagesBusiness Finance LAS.Q1.WEEK5Jeisha Mae RicoNo ratings yet

- Universityof St. La Salle: REPORT: Quarrying and Mining Waste Management / Sanitation / Pollution ControlDocument40 pagesUniversityof St. La Salle: REPORT: Quarrying and Mining Waste Management / Sanitation / Pollution ControlXirkul TupasNo ratings yet

- Article 1767Document5 pagesArticle 1767Trisha Mae BahandeNo ratings yet

- Project Report ON: "A Study of Comparative Analyis of Kotak Mahindra Bank With Its Competitor'S"Document63 pagesProject Report ON: "A Study of Comparative Analyis of Kotak Mahindra Bank With Its Competitor'S"Nitesh AgrawalNo ratings yet

- Emea Consumer Discretionary Travel and LeisureDocument10 pagesEmea Consumer Discretionary Travel and LeisureThomas DldesNo ratings yet

- Factory OverheadDocument21 pagesFactory OverheadJuvi CruzNo ratings yet

- Invoice: Please DO NOT PAY. You Will Be Charged The Amount Due Through Your Selected Method of PaymentDocument2 pagesInvoice: Please DO NOT PAY. You Will Be Charged The Amount Due Through Your Selected Method of PaymentStav KamilNo ratings yet

- Itr-1 Sahaj Individual Income Tax Return: Acknowledgement Number: Assessment Year: 2018-19Document6 pagesItr-1 Sahaj Individual Income Tax Return: Acknowledgement Number: Assessment Year: 2018-19ritesh shrivastavNo ratings yet

- Freddie Mac and Fannie Mae: An Exit Strategy For The Taxpayer, Cato Briefing Paper No. 106Document8 pagesFreddie Mac and Fannie Mae: An Exit Strategy For The Taxpayer, Cato Briefing Paper No. 106Cato Institute100% (1)

- Ch01 Understanding Investments & Ch02 Investment AlternativesDocument44 pagesCh01 Understanding Investments & Ch02 Investment AlternativesCikini MentengNo ratings yet

- Apar IndustriesDocument16 pagesApar Industriesh_o_mNo ratings yet

- Explain The Relationship Between Financial Management and Other Disciplines Finance and EconomicsDocument14 pagesExplain The Relationship Between Financial Management and Other Disciplines Finance and EconomicsajeshNo ratings yet

- Financial Analysis Question Paper, Answers and Examiners CommentsDocument23 pagesFinancial Analysis Question Paper, Answers and Examiners CommentsPauline AdrinedaNo ratings yet

- Periodic and Perpetual 2Document20 pagesPeriodic and Perpetual 2Edmond De Guerto100% (1)

- IffatZehra - 2972 - 15876 - 1 - Chapter 2 Job Order CostingDocument63 pagesIffatZehra - 2972 - 15876 - 1 - Chapter 2 Job Order CostingSabeeh Mustafa ZubairiNo ratings yet

- Module 5 - Current Liabilities - Part 1Document51 pagesModule 5 - Current Liabilities - Part 1Joshua CabinasNo ratings yet

- Month - To - Month Rent AgreementDocument3 pagesMonth - To - Month Rent AgreementTony Garcia100% (1)

- Sakthi KVB ProjectDocument84 pagesSakthi KVB ProjectNaresh KumarNo ratings yet

- UPSC IAS Pre LAST 5 Year Papers General StudiesDocument96 pagesUPSC IAS Pre LAST 5 Year Papers General StudiesSundeep MalikNo ratings yet

- WEF Digital Assets Distributed Ledger Technology 2021Document100 pagesWEF Digital Assets Distributed Ledger Technology 2021Stelian IanaNo ratings yet

- Amul, The Mother Brand of India's Largest Food Products OrganizationDocument8 pagesAmul, The Mother Brand of India's Largest Food Products OrganizationJuan CollinsNo ratings yet

- Rosal - Nakpil V IAC - 1450Document2 pagesRosal - Nakpil V IAC - 1450Ergel Mae Encarnacion RosalNo ratings yet

- Universal S1 With CertificationDocument8 pagesUniversal S1 With CertificationDanica Ella PaneloNo ratings yet

- Comparison 6657 and 9700Document12 pagesComparison 6657 and 9700monchievalera100% (1)

Download as pdf or txt

You might also like

- Contract of Lease With Special Power of Attorney SampleDocument3 pagesContract of Lease With Special Power of Attorney SampleRuben Luyon100% (1)

- BBMA OA MyEnglishVersion1.1Document79 pagesBBMA OA MyEnglishVersion1.1LAURENT MULLAHNo ratings yet

- 2015 Financial StatementDocument85 pages2015 Financial StatementMiftah IndiraNo ratings yet

- Demonstra??es Financeiras em Padr?es InternacionaisDocument66 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- 3Q15 Financial StatementsDocument43 pages3Q15 Financial StatementsFibriaRINo ratings yet

- Airbus Group Financial Statements 2015Document119 pagesAirbus Group Financial Statements 2015AdrianPedroviejoFernandez100% (1)

- Demonstra??es Financeiras em Padr?es InternacionaisDocument66 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- 2Q15 Financial StatementsDocument43 pages2Q15 Financial StatementsFibriaRINo ratings yet

- Financial Results & Limited Review For June 30, 2015 (Company Update)Document7 pagesFinancial Results & Limited Review For June 30, 2015 (Company Update)Shyam SunderNo ratings yet

- 3 - Sept14 PDFDocument87 pages3 - Sept14 PDFKiim Saii DhaNo ratings yet

- Consolidated2010 FinalDocument79 pagesConsolidated2010 FinalHammna AshrafNo ratings yet

- Unvr - LK Audit 2012Document79 pagesUnvr - LK Audit 2012Abiyyu AhmadNo ratings yet

- Allianz-Ţiriac Asigurări Sa Consolidated Financial Statements Year Ended 31 December 2000Document29 pagesAllianz-Ţiriac Asigurări Sa Consolidated Financial Statements Year Ended 31 December 2000Ovidiu BradatanuNo ratings yet

- Fibria Celulose S.ADocument69 pagesFibria Celulose S.AFibriaRINo ratings yet

- IfrsDocument272 pagesIfrsKisu ShuteNo ratings yet

- 25 Chart of AccountsDocument104 pages25 Chart of AccountsFiania WatungNo ratings yet

- Leucadia 2012 Q3 ReportDocument43 pagesLeucadia 2012 Q3 Reportofb1No ratings yet

- Consolidated Accounts December 31 2011 For Web (Revised) PDFDocument93 pagesConsolidated Accounts December 31 2011 For Web (Revised) PDFElegant EmeraldNo ratings yet

- MCB Consolidated For Year Ended Dec 2011Document87 pagesMCB Consolidated For Year Ended Dec 2011shoaibjeeNo ratings yet

- Shell Pakistan Limited Condensed Interim Financial Information (Unaudited) For The Half Year Ended June 30, 2011Document19 pagesShell Pakistan Limited Condensed Interim Financial Information (Unaudited) For The Half Year Ended June 30, 2011roker_m3No ratings yet

- Items That May Be Reclassified Subsequently To The Profit or LossDocument4 pagesItems That May Be Reclassified Subsequently To The Profit or LossEugene Khoo Sheng ChuanNo ratings yet

- Q4FY2013 Interim ResultsDocument13 pagesQ4FY2013 Interim ResultsrickysuNo ratings yet

- Breeze-Eastern Corporation: Securities and Exchange CommissionDocument31 pagesBreeze-Eastern Corporation: Securities and Exchange Commissionashish822No ratings yet

- 2 PDocument238 pages2 Pbillyryan1100% (3)

- Apple Inc.: Form 10-QDocument53 pagesApple Inc.: Form 10-QSeiha ChhengNo ratings yet

- Financial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Document4 pagesFinancial Results & Limited Review Report For Sept 30, 2015 (Standalone) (Result)Shyam SunderNo ratings yet

- POAL Financial Review 2013Document13 pagesPOAL Financial Review 2013George WoodNo ratings yet

- Myer AR10 Financial ReportDocument50 pagesMyer AR10 Financial ReportMitchell HughesNo ratings yet

- FY2014 - HHI - English FS (Separate) - FIN - 1Document88 pagesFY2014 - HHI - English FS (Separate) - FIN - 1airlanggaputraNo ratings yet

- Demonstra??es Financeiras em Padr?es InternacionaisDocument81 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- CSS Financial Report Web 10-11Document20 pagesCSS Financial Report Web 10-11LIFECommsNo ratings yet

- Ar 11 pt03Document112 pagesAr 11 pt03Muneeb ShahidNo ratings yet

- Cash Flow StatementDocument1 pageCash Flow StatementGENIUS1507No ratings yet

- Announces Q2 Results & Auditors' Report For The Quarter Ended September 30, 2015 (Result)Document4 pagesAnnounces Q2 Results & Auditors' Report For The Quarter Ended September 30, 2015 (Result)Shyam SunderNo ratings yet

- Financial Results & Limited Review Report For June 30, 2015 (Standalone) (Company Update)Document3 pagesFinancial Results & Limited Review Report For June 30, 2015 (Standalone) (Company Update)Shyam SunderNo ratings yet

- Glosario de FinanzasDocument9 pagesGlosario de FinanzasRaúl VargasNo ratings yet

- Airbus Annual ReportDocument201 pagesAirbus Annual ReportfsdfsdfsNo ratings yet

- HBS Investment Limited 2015Document32 pagesHBS Investment Limited 2015Areej FatimaNo ratings yet

- 3Q16 Financial StatementsDocument46 pages3Q16 Financial StatementsFibriaRINo ratings yet

- Cognizant+Technologies+9!30!11+Form+10 Q+ +as+filedDocument55 pagesCognizant+Technologies+9!30!11+Form+10 Q+ +as+filedKalpesh PatilNo ratings yet

- Entah LerDocument62 pagesEntah LerNor Azizuddin Abdul MananNo ratings yet

- FordMotorCompany 10Q 20110805Document102 pagesFordMotorCompany 10Q 20110805Lee LoganNo ratings yet

- JFC 2011 Audited FSDocument82 pagesJFC 2011 Audited FSRegla MarieNo ratings yet

- Bida - Tech Company Statement of Financial Position: As of December 31, Assets 2020 Current AssetsDocument42 pagesBida - Tech Company Statement of Financial Position: As of December 31, Assets 2020 Current AssetsTrisha Mae Mendoza MacalinoNo ratings yet

- Juhayna-Annual Report 2014Document20 pagesJuhayna-Annual Report 2014Wasseem Atalla100% (1)

- Demonstra??es Financeiras em Padr?es InternacionaisDocument62 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- 1Q16 Financial StatementsDocument40 pages1Q16 Financial StatementsFibriaRINo ratings yet

- Demonstra??es Financeiras em Padr?es InternacionaisDocument65 pagesDemonstra??es Financeiras em Padr?es InternacionaisFibriaRINo ratings yet

- DemonstraDocument74 pagesDemonstraFibriaRINo ratings yet

- 1Q15 Financial StatementsDocument42 pages1Q15 Financial StatementsFibriaRINo ratings yet

- MFRS 101 - Ig - 042015Document24 pagesMFRS 101 - Ig - 042015Prasen RajNo ratings yet

- Statement of Financial Position AssetsDocument5 pagesStatement of Financial Position AssetsNindasurnilaPramestiCahyaniNo ratings yet

- Financial Results & Limited Review For Sept 30, 2014 (Standalone) (Result)Document4 pagesFinancial Results & Limited Review For Sept 30, 2014 (Standalone) (Result)Shyam SunderNo ratings yet

- A Wholly Owned Subsidiary of Megaworld CorporationDocument4 pagesA Wholly Owned Subsidiary of Megaworld CorporationAngelo LabiosNo ratings yet

- IDEAL RICE INDUSTRIES AccountsDocument89 pagesIDEAL RICE INDUSTRIES Accountsahmed.zjcNo ratings yet

- DominosPizzaInc Q2-2013Document28 pagesDominosPizzaInc Q2-2013nitin2khNo ratings yet

- YTB 062015 NotesDocument13 pagesYTB 062015 Notesnickong53No ratings yet

- Mills Estruturas e Serviços de Engenharia S.ADocument61 pagesMills Estruturas e Serviços de Engenharia S.AMillsRINo ratings yet

- IFRS For SMEsDocument10 pagesIFRS For SMEsJhemmilyn RiveraNo ratings yet

- A2Z Annual Report 2018Document216 pagesA2Z Annual Report 2018Siddharth ShekharNo ratings yet

- 2017 - 10 - FEV India - Presentation PDFDocument21 pages2017 - 10 - FEV India - Presentation PDFSiddharth ShekharNo ratings yet

- Asha Annual Report - 2015-2016Document134 pagesAsha Annual Report - 2015-2016Siddharth ShekharNo ratings yet

- AOLAnnualReport2016 17Document180 pagesAOLAnnualReport2016 17Siddharth ShekharNo ratings yet

- Annualreport16 17Document215 pagesAnnualreport16 17Siddharth ShekharNo ratings yet

- Annual Report 2015 16Document188 pagesAnnual Report 2015 16Siddharth ShekharNo ratings yet

- Anant Raj Limited321Document12 pagesAnant Raj Limited321Siddharth ShekharNo ratings yet

- Smartlink Annual Report 2015-16-25june2016 1Document84 pagesSmartlink Annual Report 2015-16-25june2016 1Siddharth ShekharNo ratings yet

- 3SB300 0aa11Document3 pages3SB300 0aa11Siddharth ShekharNo ratings yet

- Arihant Superstructures Limited: February 23, 2010 For Equity Shareholders of The Company OnlyDocument176 pagesArihant Superstructures Limited: February 23, 2010 For Equity Shareholders of The Company OnlySiddharth ShekharNo ratings yet

- MSL Annual Report 2015 16Document133 pagesMSL Annual Report 2015 16Siddharth ShekharNo ratings yet

- Manaksia Aluminium Co LTD 2015 16Document68 pagesManaksia Aluminium Co LTD 2015 16Siddharth ShekharNo ratings yet

- AnnualDocument122 pagesAnnualSiddharth ShekharNo ratings yet

- Rain Industries Limited - 40th Annual Report - 2014Document171 pagesRain Industries Limited - 40th Annual Report - 2014Siddharth ShekharNo ratings yet

- Annual Report - Ram Minerals and Chemicals LimitedDocument32 pagesAnnual Report - Ram Minerals and Chemicals LimitedSiddharth ShekharNo ratings yet

- Annual Report For The Year 2016-17Document89 pagesAnnual Report For The Year 2016-17Siddharth ShekharNo ratings yet

- Impact of Foreign Aid On Saving in NigeriaDocument80 pagesImpact of Foreign Aid On Saving in NigeriaTreasured PrinceNo ratings yet

- Essel Propack LTDDocument8 pagesEssel Propack LTDmaheshNo ratings yet

- ABC CompanyDocument11 pagesABC CompanyA DiolataNo ratings yet

- ΠΡΟΚΗΡΥΞΗ ΕΣΠΑ ΝΕΕΣ ΜΜΕ ΑΔΑ - ΨΩΓΚΗ-ΕΥΦDocument235 pagesΠΡΟΚΗΡΥΞΗ ΕΣΠΑ ΝΕΕΣ ΜΜΕ ΑΔΑ - ΨΩΓΚΗ-ΕΥΦaloukeriNo ratings yet

- Business Finance LAS.Q1.WEEK5Document5 pagesBusiness Finance LAS.Q1.WEEK5Jeisha Mae RicoNo ratings yet

- Universityof St. La Salle: REPORT: Quarrying and Mining Waste Management / Sanitation / Pollution ControlDocument40 pagesUniversityof St. La Salle: REPORT: Quarrying and Mining Waste Management / Sanitation / Pollution ControlXirkul TupasNo ratings yet

- Article 1767Document5 pagesArticle 1767Trisha Mae BahandeNo ratings yet

- Project Report ON: "A Study of Comparative Analyis of Kotak Mahindra Bank With Its Competitor'S"Document63 pagesProject Report ON: "A Study of Comparative Analyis of Kotak Mahindra Bank With Its Competitor'S"Nitesh AgrawalNo ratings yet

- Emea Consumer Discretionary Travel and LeisureDocument10 pagesEmea Consumer Discretionary Travel and LeisureThomas DldesNo ratings yet

- Factory OverheadDocument21 pagesFactory OverheadJuvi CruzNo ratings yet

- Invoice: Please DO NOT PAY. You Will Be Charged The Amount Due Through Your Selected Method of PaymentDocument2 pagesInvoice: Please DO NOT PAY. You Will Be Charged The Amount Due Through Your Selected Method of PaymentStav KamilNo ratings yet

- Itr-1 Sahaj Individual Income Tax Return: Acknowledgement Number: Assessment Year: 2018-19Document6 pagesItr-1 Sahaj Individual Income Tax Return: Acknowledgement Number: Assessment Year: 2018-19ritesh shrivastavNo ratings yet

- Freddie Mac and Fannie Mae: An Exit Strategy For The Taxpayer, Cato Briefing Paper No. 106Document8 pagesFreddie Mac and Fannie Mae: An Exit Strategy For The Taxpayer, Cato Briefing Paper No. 106Cato Institute100% (1)

- Ch01 Understanding Investments & Ch02 Investment AlternativesDocument44 pagesCh01 Understanding Investments & Ch02 Investment AlternativesCikini MentengNo ratings yet

- Apar IndustriesDocument16 pagesApar Industriesh_o_mNo ratings yet

- Explain The Relationship Between Financial Management and Other Disciplines Finance and EconomicsDocument14 pagesExplain The Relationship Between Financial Management and Other Disciplines Finance and EconomicsajeshNo ratings yet

- Financial Analysis Question Paper, Answers and Examiners CommentsDocument23 pagesFinancial Analysis Question Paper, Answers and Examiners CommentsPauline AdrinedaNo ratings yet

- Periodic and Perpetual 2Document20 pagesPeriodic and Perpetual 2Edmond De Guerto100% (1)

- IffatZehra - 2972 - 15876 - 1 - Chapter 2 Job Order CostingDocument63 pagesIffatZehra - 2972 - 15876 - 1 - Chapter 2 Job Order CostingSabeeh Mustafa ZubairiNo ratings yet

- Module 5 - Current Liabilities - Part 1Document51 pagesModule 5 - Current Liabilities - Part 1Joshua CabinasNo ratings yet

- Month - To - Month Rent AgreementDocument3 pagesMonth - To - Month Rent AgreementTony Garcia100% (1)

- Sakthi KVB ProjectDocument84 pagesSakthi KVB ProjectNaresh KumarNo ratings yet

- UPSC IAS Pre LAST 5 Year Papers General StudiesDocument96 pagesUPSC IAS Pre LAST 5 Year Papers General StudiesSundeep MalikNo ratings yet

- WEF Digital Assets Distributed Ledger Technology 2021Document100 pagesWEF Digital Assets Distributed Ledger Technology 2021Stelian IanaNo ratings yet

- Amul, The Mother Brand of India's Largest Food Products OrganizationDocument8 pagesAmul, The Mother Brand of India's Largest Food Products OrganizationJuan CollinsNo ratings yet

- Rosal - Nakpil V IAC - 1450Document2 pagesRosal - Nakpil V IAC - 1450Ergel Mae Encarnacion RosalNo ratings yet

- Universal S1 With CertificationDocument8 pagesUniversal S1 With CertificationDanica Ella PaneloNo ratings yet

- Comparison 6657 and 9700Document12 pagesComparison 6657 and 9700monchievalera100% (1)