Download as pdf or txt

You might also like

- Strategic Analysis of ARCELOR MITTAL STEELDocument29 pagesStrategic Analysis of ARCELOR MITTAL STEELharsh_desai2429100% (1)

- Chapter 1 Study TestDocument3 pagesChapter 1 Study TestChethan KumarNo ratings yet

- Regulatory Framework AssignmentDocument3 pagesRegulatory Framework AssignmentMahima SharmaNo ratings yet

- Arcelor MittalDocument20 pagesArcelor MittalRuchi Madiya50% (2)

- HUL GSK AcquisitionDocument7 pagesHUL GSK AcquisitionTirtha Das100% (1)

- Group03 - SectionA - M&A - Project - P&G Acquisition GilletteDocument7 pagesGroup03 - SectionA - M&A - Project - P&G Acquisition Gillettesili coreNo ratings yet

- Jet Etihad Deal On Merger and AcquisitionsDocument22 pagesJet Etihad Deal On Merger and AcquisitionsTushar GargNo ratings yet

- Pidilite Industries Company AnalysisDocument7 pagesPidilite Industries Company Analysisdhruv_mavani0% (1)

- Mergers and AcquisitionDocument71 pagesMergers and AcquisitionAnonymous k2ZXzsNo ratings yet

- Islamic Directorate of The Philippines v. CADocument2 pagesIslamic Directorate of The Philippines v. CAGedan TanNo ratings yet

- Accounts Receivable 2Document10 pagesAccounts Receivable 2jade rotiaNo ratings yet

- Merger of Mittal and Arcelor PDFDocument41 pagesMerger of Mittal and Arcelor PDFANCHAL SINGH0% (1)

- Arcelor Mittal MergerDocument26 pagesArcelor Mittal MergerPuja AgarwalNo ratings yet

- Arcelor Mittal (Final)Document31 pagesArcelor Mittal (Final)manansolankiNo ratings yet

- Arcelor Mittal Post Merger Marketing IntegrationDocument7 pagesArcelor Mittal Post Merger Marketing IntegrationAkhil BangiaNo ratings yet

- Mergers and Acquisition 3Document55 pagesMergers and Acquisition 3Vivek SinghNo ratings yet

- CC !CC! C"#: Download The Original AttachmentDocument36 pagesCC !CC! C"#: Download The Original Attachmentsomanath_cool0% (1)

- Surabhi Chouhan M. Sriraman Manas Agarwal Ujjval Jain Arpit Bansal Vignesh K. Ritu RanjanDocument27 pagesSurabhi Chouhan M. Sriraman Manas Agarwal Ujjval Jain Arpit Bansal Vignesh K. Ritu RanjanUjjval YadavNo ratings yet

- Merger of Tata Steel and CorusDocument24 pagesMerger of Tata Steel and Coruspratik tanna100% (17)

- A Project On Merger and Acquisition of Vodafone and HutchDocument7 pagesA Project On Merger and Acquisition of Vodafone and HutchiamsourabhcNo ratings yet

- Mergers and Acquisitions in India 2006-2010Document32 pagesMergers and Acquisitions in India 2006-2010Rajat Kataria100% (12)

- ABRYDocument25 pagesABRYAlaura AshleyNo ratings yet

- Tata - Corus - Merger ReportDocument18 pagesTata - Corus - Merger Reportsanil_p100% (2)

- A Case Study of Tata and Corus MergerDocument14 pagesA Case Study of Tata and Corus Mergershalvi vaidya100% (1)

- Arcelor Mittal+ReportDocument13 pagesArcelor Mittal+ReportSrikanth DL0% (1)

- Hostile TakeDocument4 pagesHostile TakeAyushJainNo ratings yet

- UltraTech Cements and Jaiprakash AssociatesDocument8 pagesUltraTech Cements and Jaiprakash AssociatesanushaNo ratings yet

- Hostile & Defensive Takeover StrategiesDocument26 pagesHostile & Defensive Takeover StrategiesShobhit Bhatnagar100% (2)

- Ccea Approves Selling 51% Stake in HPCL To OngcDocument1 pageCcea Approves Selling 51% Stake in HPCL To OngcNisseem KrishnaNo ratings yet

- Hul - GSK Acquisition: A Brief About The EventDocument2 pagesHul - GSK Acquisition: A Brief About The EventTestNo ratings yet

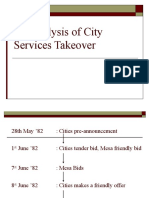

- CitiesService Takeover CaseDocument20 pagesCitiesService Takeover CasesushilkhannaNo ratings yet

- Industry AnalisysDocument63 pagesIndustry Analisyselmita ririyanaNo ratings yet

- Strategic Management FinalDocument22 pagesStrategic Management FinaladityaNo ratings yet

- Corporate Governance Issue in India 2019Document8 pagesCorporate Governance Issue in India 2019kunal fulewaleNo ratings yet

- Porter's Five Forces Analysis For Indian Oil & Gas Industry: Bargaining Power of BuyersDocument3 pagesPorter's Five Forces Analysis For Indian Oil & Gas Industry: Bargaining Power of BuyersAditya JainNo ratings yet

- Running Head: Gillette Company Case 1Document23 pagesRunning Head: Gillette Company Case 1Aneela Jabeen100% (1)

- Mergers and Acquisitions Tata CorusDocument31 pagesMergers and Acquisitions Tata Corusash_wick50% (2)

- Project Report of RILDocument53 pagesProject Report of RILeakta100% (4)

- STM Pidilite Group2 SectionBDocument41 pagesSTM Pidilite Group2 SectionBSiddharth SharmaNo ratings yet

- Corporate Governance in TATA MotorsDocument9 pagesCorporate Governance in TATA MotorsSai VasudevanNo ratings yet

- Equity Research On Paint and FMCG SectorDocument43 pagesEquity Research On Paint and FMCG SectornehagadgeNo ratings yet

- Project Report On Tata MotorsDocument24 pagesProject Report On Tata Motorsdheeraj777733% (3)

- Inbound Mergers and Acquisitions Financing, IPE, HYDERABADDocument20 pagesInbound Mergers and Acquisitions Financing, IPE, HYDERABADsushantsaahaji100% (1)

- Project On Ratio Analysis of Pidilite - 190669176Document23 pagesProject On Ratio Analysis of Pidilite - 190669176Anshu yaduNo ratings yet

- Flipkart - Walmart M&ADocument23 pagesFlipkart - Walmart M&ACHINMAY SANKHENo ratings yet

- L&T Case PDFDocument31 pagesL&T Case PDFArpit AgarwalNo ratings yet

- Tata Group Buys Jaguar Land RoverDocument17 pagesTata Group Buys Jaguar Land RoverShubh ShrivastavaNo ratings yet

- Tata Corus DealDocument39 pagesTata Corus DealdhavalkurveyNo ratings yet

- GROUP 1 Project Report Strategy MGMTDocument18 pagesGROUP 1 Project Report Strategy MGMTDiksha LathNo ratings yet

- Mergers and AcquisitionsDocument10 pagesMergers and AcquisitionsHarpreet ChawlaNo ratings yet

- ArcelorMittal SWOTDocument7 pagesArcelorMittal SWOTSanjiv KarsoliaNo ratings yet

- Case Study On Hindalco Acquire NovelisDocument13 pagesCase Study On Hindalco Acquire Novelissahilagl23_121905585No ratings yet

- Vodafone HutchDocument12 pagesVodafone Hutchkushalnadekar0% (1)

- Acquisition of Arcelor Steel by Mittal Steel: Presented by-SONUKA AGARWAL (M.B.A. Design Management)Document25 pagesAcquisition of Arcelor Steel by Mittal Steel: Presented by-SONUKA AGARWAL (M.B.A. Design Management)sonuka86% (7)

- M&A Tata Corus Merger AnalysisDocument21 pagesM&A Tata Corus Merger AnalysisPreetam Joga100% (1)

- Equity Carve OutDocument32 pagesEquity Carve OutmuditsingNo ratings yet

- FreeMove Alliance Group5Document10 pagesFreeMove Alliance Group5Annisa MoeslimNo ratings yet

- Promoters Influence On Corporate Governance: A Case Study of Tata GroupDocument9 pagesPromoters Influence On Corporate Governance: A Case Study of Tata GroupAaronNo ratings yet

- Maruti Manesar Plant Case StudyDocument6 pagesMaruti Manesar Plant Case StudyvaibhavNo ratings yet

- Case Synopsis Nestle and Alcon The Value of ListingDocument4 pagesCase Synopsis Nestle and Alcon The Value of Listingavnish kumarNo ratings yet

- Assignments of Corporate FinanceDocument20 pagesAssignments of Corporate Financenumb_sahilNo ratings yet

- 02 IFRS 3 Business CombinationDocument15 pages02 IFRS 3 Business CombinationtsionNo ratings yet

- International MarketingDocument15 pagesInternational MarketingHursh MaheshwariNo ratings yet

- Survey AnalysisDocument23 pagesSurvey AnalysisHursh MaheshwariNo ratings yet

- Research MethodologyDocument9 pagesResearch MethodologyHursh MaheshwariNo ratings yet

- Research MethodologyDocument30 pagesResearch MethodologyHursh MaheshwariNo ratings yet

- HR Practices at ICICI BANKDocument34 pagesHR Practices at ICICI BANKHursh MaheshwariNo ratings yet

- Liquidity and Reserves Management: Strategies and Policies: Alvarez, Gladys Faith MDocument32 pagesLiquidity and Reserves Management: Strategies and Policies: Alvarez, Gladys Faith MPhieta PanchaNo ratings yet

- TerminologyDocument2 pagesTerminologyDrDrifte0% (3)

- Altman Z Score - 3Document3 pagesAltman Z Score - 3ShrutiKulkarniNo ratings yet

- 162.materials 1.SHE 001Document2 pages162.materials 1.SHE 001jpbluejnNo ratings yet

- Emkay Global Financial Services LTDDocument7 pagesEmkay Global Financial Services LTDSauvick KoleyNo ratings yet

- Chapter 6Document7 pagesChapter 6Its meh SushiNo ratings yet

- Liquidity Analysis RatiosDocument5 pagesLiquidity Analysis Ratiosyuvraj gosainNo ratings yet

- Gmail - FWD - ABI Sources - Jordanrygier@gmailDocument1 pageGmail - FWD - ABI Sources - Jordanrygier@gmailjordanrygierNo ratings yet

- Case DakaDocument7 pagesCase Dakatrisma fitrianiNo ratings yet

- Majority Rule and Protection of Minority ShareholdersDocument8 pagesMajority Rule and Protection of Minority Shareholderssajid javeed100% (1)

- TransmissionDocument2 pagesTransmissionPriyank ShahNo ratings yet

- G.R. No. L-52361 ETC-SUNSET VIEW V. CAMPOS PDFDocument7 pagesG.R. No. L-52361 ETC-SUNSET VIEW V. CAMPOS PDFLex Tamen CoercitorNo ratings yet

- MODULE 1 Summative Business FinanceDocument2 pagesMODULE 1 Summative Business Financerandy magbudhiNo ratings yet

- Suggested Answer For Corporate Laws and Secretarial Practice June 09Document23 pagesSuggested Answer For Corporate Laws and Secretarial Practice June 09tayalsirNo ratings yet

- Adv Acc Ch-4 Company Accounts SaDocument129 pagesAdv Acc Ch-4 Company Accounts SaShivaSrinivasNo ratings yet

- Quizlet PDFDocument3 pagesQuizlet PDFSaif Ali KhanNo ratings yet

- Finance TestDocument4 pagesFinance Testbhanu.chanduNo ratings yet

- 03 - Literature ReviewDocument13 pages03 - Literature Reviewshubham singhNo ratings yet

- CG of Non Listed Companies in Emerging MarketsDocument265 pagesCG of Non Listed Companies in Emerging MarketsANISANo ratings yet

- Livedoor - Japanese Corporate GovernanceDocument84 pagesLivedoor - Japanese Corporate GovernanceMulligan McMasterNo ratings yet

- Mauboussin - The Importance of ExpectationsDocument17 pagesMauboussin - The Importance of Expectationsjockxyz100% (1)

- Act 203 AnswersDocument3 pagesAct 203 AnswersShahinNo ratings yet

- Complex Group: Table of ContentDocument12 pagesComplex Group: Table of ContentRobert MunyaradziNo ratings yet

- 12 Account SP 01 PDFDocument24 pages12 Account SP 01 PDFJanvi KushwahaNo ratings yet

- Rizona Ourt of Ppeals: Plaintiffs/Appellants/Cross-Appellees, VDocument11 pagesRizona Ourt of Ppeals: Plaintiffs/Appellants/Cross-Appellees, VScribd Government DocsNo ratings yet

- GS 2008 Entire Annual ReportDocument162 pagesGS 2008 Entire Annual ReportlelaissezfaireNo ratings yet

- MBA Finance Thesis Topics List PDF: Equity Analysis of BanksDocument4 pagesMBA Finance Thesis Topics List PDF: Equity Analysis of BanksbagyaNo ratings yet

- Ratio AnalysisDocument6 pagesRatio AnalysisMilcah QuisedoNo ratings yet