Download as docx, pdf, or txt

You might also like

- The Aditya Birla GroupDocument4 pagesThe Aditya Birla GroupPriyanka RajputNo ratings yet

- Tata Steel - Value Chain AnalysisDocument11 pagesTata Steel - Value Chain AnalysisKiranNo ratings yet

- Tata SteelDocument41 pagesTata SteelSanjana GuptaNo ratings yet

- Project Report On Tata SteelDocument9 pagesProject Report On Tata SteelChander ShekharNo ratings yet

- Eco Analysis Tata SteelDocument79 pagesEco Analysis Tata SteelRavNeet KaUrNo ratings yet

- Tata Steel: Q1. Apply PESTLE, FIVE FORCES & SWOT Analysis On Following Tata BusinessDocument51 pagesTata Steel: Q1. Apply PESTLE, FIVE FORCES & SWOT Analysis On Following Tata BusinessAnsh AnandNo ratings yet

- Porter S Value Chain Tata SteelDocument6 pagesPorter S Value Chain Tata SteelAndreea CriclevitNo ratings yet

- 4.2 Case Study - TVSDocument4 pages4.2 Case Study - TVSRam Raj KanumuriNo ratings yet

- Intro - /bharti Airtel, Formerly Known As Bharti Tele-Ventures LimitedDocument8 pagesIntro - /bharti Airtel, Formerly Known As Bharti Tele-Ventures Limitedaminiff100% (1)

- Strategic Management ProjectDocument18 pagesStrategic Management Projectshrey khuranaNo ratings yet

- Journey of TATADocument89 pagesJourney of TATAravish419No ratings yet

- Porter'S Five Forces Model: - Barriers To EntryDocument5 pagesPorter'S Five Forces Model: - Barriers To Entryhimanshu agrawalNo ratings yet

- Tata Motors Summer Training ReportDocument98 pagesTata Motors Summer Training ReportAnsh SoniNo ratings yet

- PKDocument42 pagesPKSafeer Shibi100% (1)

- Projectonindianautomotiveindustry and Case Study of Tata MotorsDocument26 pagesProjectonindianautomotiveindustry and Case Study of Tata MotorsMukesh Manwani100% (1)

- Analysis On Financial Performance of Tata Steel and Jindal Steel & PowerDocument6 pagesAnalysis On Financial Performance of Tata Steel and Jindal Steel & PowerDeep ShahNo ratings yet

- Synopsis 00Document8 pagesSynopsis 00shalini TripathiNo ratings yet

- Recruitment Process in ACC CEMENTDocument48 pagesRecruitment Process in ACC CEMENTAmit Pasi100% (2)

- Tata Motors Strategic Plan For The FutureDocument6 pagesTata Motors Strategic Plan For The FutureItz PanggingNo ratings yet

- Aditya Birla GroupDocument7 pagesAditya Birla GroupHerdi SularkoNo ratings yet

- Tata MotorsDocument14 pagesTata MotorsADITYA GURJARNo ratings yet

- EIC Analysis Sun PharmaDocument7 pagesEIC Analysis Sun PharmaDeepakNo ratings yet

- Harshi HardDocument60 pagesHarshi HardNandeep Hêãrtrøbbér100% (2)

- Marketing Strategy of Tata MotorsDocument59 pagesMarketing Strategy of Tata MotorsVarun KhannaNo ratings yet

- Presentation of Maruti Suzuki India LTDDocument17 pagesPresentation of Maruti Suzuki India LTDRamanpreet KaurNo ratings yet

- Study of Consumer Channel Behavior For Jaypee CementDocument28 pagesStudy of Consumer Channel Behavior For Jaypee CementSachindihmNo ratings yet

- SM Project TCSDocument32 pagesSM Project TCSShivam SenNo ratings yet

- Inplant Training ReportDocument48 pagesInplant Training ReportyogeshNo ratings yet

- Employee WelfareDocument23 pagesEmployee Welfarecharu_006No ratings yet

- TI Cycles Project ReportDocument4 pagesTI Cycles Project ReportGaneshNo ratings yet

- "From A Bird's-Eye View, The 134-Year-Old Tata Group Still Looks Awesome. With 95 Operating Companies (31 ofDocument26 pages"From A Bird's-Eye View, The 134-Year-Old Tata Group Still Looks Awesome. With 95 Operating Companies (31 ofAnurag PandeyNo ratings yet

- Strategy Management at Tata SteelDocument50 pagesStrategy Management at Tata SteelMuhammad Nb100% (1)

- Tata Corus Aq ProjectDocument23 pagesTata Corus Aq ProjectKrishan Chander100% (1)

- SWOT AnalysisDocument11 pagesSWOT AnalysisKEyuRNo ratings yet

- Pest Analysis For Hindustan MotorsDocument3 pagesPest Analysis For Hindustan MotorsSachin SinghNo ratings yet

- Case Study of Tata IndicaDocument17 pagesCase Study of Tata Indicabholu43667% (3)

- Dabur IndiaDocument34 pagesDabur IndiaDerin ElsaNo ratings yet

- Global Operations of TATA GroupDocument28 pagesGlobal Operations of TATA GroupbhavanaNo ratings yet

- Ultratech CementDocument65 pagesUltratech CementSonam Borana0% (1)

- Strategic Management Project On Tata SteelDocument18 pagesStrategic Management Project On Tata SteelRonak GosaliaNo ratings yet

- Birlasoft ProjectDocument41 pagesBirlasoft Projectashkash19No ratings yet

- Activity Based CostingDocument4 pagesActivity Based CostingSivalakshmi MavillaNo ratings yet

- 8 P's of AirtelDocument10 pages8 P's of Airtelrajat_singlaNo ratings yet

- AshrulDocument58 pagesAshrulNilabjo Kanti Paul100% (2)

- Strategic Profile of L&T GroupDocument7 pagesStrategic Profile of L&T Groupyash brahmbhattNo ratings yet

- Case Study On TATA SteelDocument26 pagesCase Study On TATA SteelKaustubh ShindeNo ratings yet

- Swot Analysis of ItcDocument14 pagesSwot Analysis of Itcsamarth agarwalNo ratings yet

- TCS BibliographyDocument4 pagesTCS BibliographyShreya TrehanNo ratings yet

- Bharti Airtel Limited HRMDocument47 pagesBharti Airtel Limited HRMAkshay Kumbhare50% (12)

- Tata SteelDocument32 pagesTata SteelAngad KalraNo ratings yet

- TataSteel Project AbstractDocument1 pageTataSteel Project Abstractdeepthisnl100% (1)

- Swot Gail IndiaDocument3 pagesSwot Gail IndiaTanish GuptaNo ratings yet

- The Cryptms Group-V3 (1) 2Document16 pagesThe Cryptms Group-V3 (1) 2Kavita BaeetNo ratings yet

- What Are Some Examples of HR Events at A B-School College FestDocument1 pageWhat Are Some Examples of HR Events at A B-School College Festgorika chawlaNo ratings yet

- Tata GroupDocument58 pagesTata GroupSaurabh G100% (1)

- Tata Steel Final Report 1Document116 pagesTata Steel Final Report 1Manu Srivastav50% (2)

- Titan Case StudyDocument19 pagesTitan Case StudyRohitSharmaNo ratings yet

- It’S Business, It’S Personal: From Setting a Vision to Delivering It Through Organizational ExcellenceFrom EverandIt’S Business, It’S Personal: From Setting a Vision to Delivering It Through Organizational ExcellenceNo ratings yet

- SBA-Module 6Document6 pagesSBA-Module 6Patricia ReyesNo ratings yet

- Aaron de Smet, Et Al.-Performance and HealthDocument12 pagesAaron de Smet, Et Al.-Performance and HealthboonikutzaNo ratings yet

- Parts of SpeechDocument6 pagesParts of SpeechArunKumarNo ratings yet

- Hindi Thesis ListDocument2 pagesHindi Thesis ListArunKumarNo ratings yet

- Finance Major and Minor Project ListDocument5 pagesFinance Major and Minor Project ListArunKumarNo ratings yet

- Vivekananda Institute of Professional Studies Ggsip UniversityDocument1 pageVivekananda Institute of Professional Studies Ggsip UniversityArunKumarNo ratings yet

- AIMA Finance Project ListDocument1 pageAIMA Finance Project ListArunKumarNo ratings yet

- Front Page FormatDocument7 pagesFront Page FormatArunKumarNo ratings yet

- Ciment Industry Project ListDocument4 pagesCiment Industry Project ListArunKumarNo ratings yet

- AcknowledgmentDocument65 pagesAcknowledgmentArunKumarNo ratings yet

- Political Science Dissertation ListDocument3 pagesPolitical Science Dissertation ListArunKumarNo ratings yet

- QuestionnaireDocument3 pagesQuestionnaireArunKumarNo ratings yet

- Aastha Jain (Resume)Document5 pagesAastha Jain (Resume)ArunKumarNo ratings yet

- Guidelines For Writing Synopsis For PH.D Thesis: PurposeDocument8 pagesGuidelines For Writing Synopsis For PH.D Thesis: PurposeArunKumarNo ratings yet

- Observation and ResultDocument17 pagesObservation and ResultArunKumarNo ratings yet

- 0-Intial Pages Nandita ThesisDocument25 pages0-Intial Pages Nandita ThesisArunKumarNo ratings yet

- E-Mail: Nareshmayal425: Career ObjectiveDocument2 pagesE-Mail: Nareshmayal425: Career ObjectiveArunKumarNo ratings yet

- Detail No.1 1/7/2016 To 2/7/2016 Detail No.4 5/7/2016Document5 pagesDetail No.1 1/7/2016 To 2/7/2016 Detail No.4 5/7/2016ArunKumarNo ratings yet

- Memorandum of Understanding Between Ramjas College Students Union and DB GroupDocument2 pagesMemorandum of Understanding Between Ramjas College Students Union and DB GroupArunKumarNo ratings yet

- Certificate: Cash Management SystemDocument6 pagesCertificate: Cash Management SystemArunKumarNo ratings yet

- Environment Court in India: Success and ChallengesDocument1 pageEnvironment Court in India: Success and ChallengesArunKumarNo ratings yet

- Binding Cover PageDocument1 pageBinding Cover PageArunKumarNo ratings yet

- A Comparative Clinical Study of Ushna Manda As Pathya Ahara Kalpana and Yogic Procedures in Management of Sthaulya W.S.R. ObesityDocument2 pagesA Comparative Clinical Study of Ushna Manda As Pathya Ahara Kalpana and Yogic Procedures in Management of Sthaulya W.S.R. ObesityArunKumarNo ratings yet

- MAN 4720 Exam 2 ReviewDocument2 pagesMAN 4720 Exam 2 ReviewSergey GarberNo ratings yet

- Mint Delhi 17-04-2024Document16 pagesMint Delhi 17-04-2024Gourab ChakrabortyNo ratings yet

- Walmart Supply ChainDocument15 pagesWalmart Supply ChainShashank Shukla100% (1)

- Unit 2 Marketing ManagementDocument34 pagesUnit 2 Marketing ManagementMuhammed Althaf h sNo ratings yet

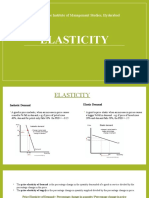

- Elasticity: Narsee Monjee Institute of Management Studies, HyderabadDocument5 pagesElasticity: Narsee Monjee Institute of Management Studies, HyderabadAishwaryaNo ratings yet

- ST439 - Chapter 1: Financial Derivatives, Binomial ModelsDocument27 pagesST439 - Chapter 1: Financial Derivatives, Binomial ModelslowchangsongNo ratings yet

- Elective 1Document2 pagesElective 1Cedie Gonzaga Alba100% (1)

- Commercial Cleaning Rates PDFDocument4 pagesCommercial Cleaning Rates PDFErnest0% (1)

- 2.3 Fra and Swap ExercisesDocument5 pages2.3 Fra and Swap ExercisesrandomcuriNo ratings yet

- Buy Used 2020 Maruti Dzire VXI MANUAL in Lucknow - CARS24Document1 pageBuy Used 2020 Maruti Dzire VXI MANUAL in Lucknow - CARS24Shivam KumarNo ratings yet

- Rajshree Sen PDFDocument18 pagesRajshree Sen PDFarpit85No ratings yet

- Macroeconomics Mankiw Chapter 3Document68 pagesMacroeconomics Mankiw Chapter 3SajidahPutri0% (1)

- Brand Preference of SoapDocument38 pagesBrand Preference of Soapsunithascribd45% (11)

- Segmentation, Targeting, and PositioningDocument50 pagesSegmentation, Targeting, and PositioningPrathibani PoornikaNo ratings yet

- Macro Answer - ChaDocument7 pagesMacro Answer - Chashann hein htetNo ratings yet

- Ca. Prabin Raj Kafle: Summary of Custom Act, 2064 & Custom Rules, 2064Document77 pagesCa. Prabin Raj Kafle: Summary of Custom Act, 2064 & Custom Rules, 2064Amrit NeupaneNo ratings yet

- Case Study On Letter of CreditDocument4 pagesCase Study On Letter of Creditfarhanahmed010% (1)

- Denim Present and Future of Bangladesh (For Selim)Document12 pagesDenim Present and Future of Bangladesh (For Selim)shohagh12133% (3)

- CH 10Document4 pagesCH 10vivienNo ratings yet

- RTD Tea - IndonesiaDocument9 pagesRTD Tea - IndonesiaRachitaRattanNo ratings yet

- Account Receivable ManagementDocument41 pagesAccount Receivable ManagementUtkarsh Joshi100% (2)

- Corporate Evaluation - VazirDocument73 pagesCorporate Evaluation - VazirSathishPerlaNo ratings yet

- Nifty Technical and Fundamental Research UpdateDocument5 pagesNifty Technical and Fundamental Research UpdateDrSreejithKBNo ratings yet

- FCF G NPV RG RDocument3 pagesFCF G NPV RG RJared TanNo ratings yet

- Standard Costing: Setting Standards and Analyzing VariancesDocument60 pagesStandard Costing: Setting Standards and Analyzing VariancesJenika AtanacioNo ratings yet

- Restaurant MirchiDocument32 pagesRestaurant MirchiDavidChenNo ratings yet

- Intermediate Microeconomics: Vivekananda Mukherjee Department of Economics, Jadavpur UniversityDocument8 pagesIntermediate Microeconomics: Vivekananda Mukherjee Department of Economics, Jadavpur UniversityYukta Modernite RajNo ratings yet

- 5.E - Conv07 - Paper - Lurie - Actuarial Methods in Health Insurance PricingDocument23 pages5.E - Conv07 - Paper - Lurie - Actuarial Methods in Health Insurance PricingJeezNo ratings yet

- Tax Evasion Practices in Philippine Estate TaxDocument68 pagesTax Evasion Practices in Philippine Estate Taxepra83% (6)

- NissanDocument2 pagesNissanRia Fasyah FatmawatiNo ratings yet