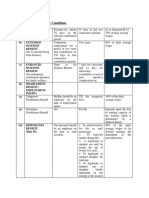

Template - Restructuring-Tax Computation-BER-Salary Tracker For FY 2015-16 - CK

Template - Restructuring-Tax Computation-BER-Salary Tracker For FY 2015-16 - CK

You might also like

- India: Shift Allowance and Compensatory Off PolicyDocument3 pagesIndia: Shift Allowance and Compensatory Off PolicySahil JunejaNo ratings yet

- India Benefits UpdatedDocument2 pagesIndia Benefits UpdatedRavi GoyalNo ratings yet

- CTC Break UpDocument100 pagesCTC Break UpnareshNo ratings yet

- 4 - Hydro Jetting and Sludge RemovalDocument18 pages4 - Hydro Jetting and Sludge RemovalPerwez21100% (2)

- The List of Components Which You Can Use For Salary BreakupDocument8 pagesThe List of Components Which You Can Use For Salary BreakupAnonymous VhqxrXNo ratings yet

- Whichever Is Lower Is Exempt From Tax. For ExampleDocument13 pagesWhichever Is Lower Is Exempt From Tax. For ExampleNasir AhmedNo ratings yet

- Insync CTC Breakup PDFDocument1 pageInsync CTC Breakup PDFSocialIndostoriesNo ratings yet

- Salary Break Up HRDocument4 pagesSalary Break Up HRnaman156No ratings yet

- What Is A Flexible Benefit Plan in A Salary Breakup? - QuoraDocument8 pagesWhat Is A Flexible Benefit Plan in A Salary Breakup? - QuoraSiNo ratings yet

- CTC - Salary Slip - The Very Basic VersionDocument2 pagesCTC - Salary Slip - The Very Basic VersionAJAY KULKARNI100% (2)

- Presented By,: Shraddha Dhatrak (01) Priyanka Ghatrat Mayuri Koli Sneha MoreDocument30 pagesPresented By,: Shraddha Dhatrak (01) Priyanka Ghatrat Mayuri Koli Sneha MoreshraddhavanjariNo ratings yet

- Salary, Net Salary, Gross Salary, Cost To Company Are They Same or Different. For Most People It IsDocument6 pagesSalary, Net Salary, Gross Salary, Cost To Company Are They Same or Different. For Most People It IsAnonymous CwxsRiwNo ratings yet

- CTC Salary CalculatorDocument1 pageCTC Salary CalculatorsavideshwalNo ratings yet

- PF Esi Calculation Sheet ExampleDocument3 pagesPF Esi Calculation Sheet ExampleRajinder KumarNo ratings yet

- Annexure II Details of AllowancesDocument4 pagesAnnexure II Details of AllowancesPravin Balasaheb GunjalNo ratings yet

- Quikchex CTC CalculatorDocument8 pagesQuikchex CTC CalculatoriamgodrajeshNo ratings yet

- Employee Benfit & ServicesDocument14 pagesEmployee Benfit & Servicesaloha123456No ratings yet

- Auto CTC Salary CalculatorDocument1 pageAuto CTC Salary CalculatorSathvika SaaraNo ratings yet

- Income Under The Head "Salaries": Shubhangi Gupta Roll No. 11 Financial Management Bhartiya Vidya BhavanDocument44 pagesIncome Under The Head "Salaries": Shubhangi Gupta Roll No. 11 Financial Management Bhartiya Vidya Bhavanhny0910No ratings yet

- Few Points To Be Kept in Mind While Doing Investment DeclarationDocument8 pagesFew Points To Be Kept in Mind While Doing Investment Declarationcool rock MohindraNo ratings yet

- Higher Pension As Per SC Decision With Calculation - Synopsis1Document13 pagesHigher Pension As Per SC Decision With Calculation - Synopsis1hariveerNo ratings yet

- Pay SlipDocument50 pagesPay SlipSushil Shrestha100% (1)

- CHRC869Document3 pagesCHRC869jvnraoNo ratings yet

- 3RD PRC Presentation-1Document25 pages3RD PRC Presentation-1sai krishna krishnaNo ratings yet

- Darshan Shetty - AnnexureDocument1 pageDarshan Shetty - Annexuredarshan shettyNo ratings yet

- Salary Calculation Yearly & Monthly Break Up of Gross SalaryDocument2 pagesSalary Calculation Yearly & Monthly Break Up of Gross Salarymoh300No ratings yet

- Overtime AllowanceDocument3 pagesOvertime AllowanceKumudha Devi100% (1)

- Benefits & Contributory Conditions: (I) (A) Sickness BenefitDocument4 pagesBenefits & Contributory Conditions: (I) (A) Sickness BenefitKunwar Sa Amit SinghNo ratings yet

- Salary Structure: Please Put The Gross Salry in Red Column in Any Slab, U Will Find StructureDocument6 pagesSalary Structure: Please Put The Gross Salry in Red Column in Any Slab, U Will Find StructureSagar ShindeNo ratings yet

- Compensation Rules and Salary Design GuidelinesDocument6 pagesCompensation Rules and Salary Design GuidelinesDivya NatarajanNo ratings yet

- Family Pension SchemeDocument15 pagesFamily Pension SchemeJitu Choudhary100% (1)

- Salary StructureDocument4 pagesSalary StructureniranjanaNo ratings yet

- LDocument7 pagesLaman anandNo ratings yet

- DGM Annexure B Know Your Pay ComponentsDocument3 pagesDGM Annexure B Know Your Pay ComponentsaakritishellNo ratings yet

- Allowances Under Income Tax Act1961Document12 pagesAllowances Under Income Tax Act1961Sahil14JNo ratings yet

- EPF CalenderDocument1 pageEPF CalenderAmitav TalukdarNo ratings yet

- National Pension Scheme (NPS) Guidelines FY 2019-20Document21 pagesNational Pension Scheme (NPS) Guidelines FY 2019-20harrishNo ratings yet

- Salary Slip Format in PDF All PDFDocument3 pagesSalary Slip Format in PDF All PDFRajeev GunasekaranNo ratings yet

- SubhashDocument1 pageSubhashsubhash221103No ratings yet

- Salary Break UpDocument17 pagesSalary Break UpRam Surya Prakash DommetiNo ratings yet

- Provident Fund (PF)Document13 pagesProvident Fund (PF)chandub6No ratings yet

- Novartis NPS Employee Awareness Presentation PDFDocument33 pagesNovartis NPS Employee Awareness Presentation PDFMohan CNo ratings yet

- Salary AdministrationDocument17 pagesSalary AdministrationMae Ann GonzalesNo ratings yet

- EPF Provident Fund CalculatorDocument6 pagesEPF Provident Fund CalculatorUtkal SolankiNo ratings yet

- Tata Consultancy Layer FormatDocument21 pagesTata Consultancy Layer FormatChinnu SalimathNo ratings yet

- Salary Breakup Calculator ExcelDocument2 pagesSalary Breakup Calculator ExcelAnup RawatNo ratings yet

- NPS PPT - HDFC BankDocument17 pagesNPS PPT - HDFC BankPankaj Kothari100% (1)

- Sallary AllowanceDocument15 pagesSallary AllowanceKeval PatelNo ratings yet

- CCS LTC RULES PPT 20210617141434Document28 pagesCCS LTC RULES PPT 20210617141434Kumar KumarNo ratings yet

- Employees' State Insurance Corporation E-Pehchan Card: Insured Person: Insurance No.: Date of RegistrationDocument3 pagesEmployees' State Insurance Corporation E-Pehchan Card: Insured Person: Insurance No.: Date of RegistrationGoutam HotaNo ratings yet

- CTS Marriage Loan PolicyDocument5 pagesCTS Marriage Loan PolicyshaannivasNo ratings yet

- New Incentive Structure - Sales TeamDocument2 pagesNew Incentive Structure - Sales TeamvishnuindianNo ratings yet

- Pension CalculationDocument1 pagePension Calculationulmilu15No ratings yet

- Salary Break Up - DamanDocument16 pagesSalary Break Up - Damanvirag_shahsNo ratings yet

- Appointment Salary BreakupDocument1 pageAppointment Salary BreakupPhani KumarNo ratings yet

- Compliance Manual F.Y. 2020 21 A.Y.2021 22 PDFDocument52 pagesCompliance Manual F.Y. 2020 21 A.Y.2021 22 PDFTHERMAL TECH ENGINEERINGNo ratings yet

- Salary Tax CalculatorDocument7 pagesSalary Tax Calculatorbecito6195No ratings yet

- Maulana Azad National Urdu University: CircularDocument4 pagesMaulana Azad National Urdu University: CircularDebasish BiswalNo ratings yet

- Direct Tax Code: Capital Gains Tax On Sale of Residential PropertyDocument5 pagesDirect Tax Code: Capital Gains Tax On Sale of Residential Propertykarthikeyan.mohandossNo ratings yet

- Salaries PresentationDocument21 pagesSalaries PresentationDipika PandaNo ratings yet

- Compensation Analysis of Manufacturing IndustriesDocument14 pagesCompensation Analysis of Manufacturing IndustriesSankar Rajan100% (13)

- GSB Samaj Foundation - List of Goud Saraswat Brahmin SurnamesDocument2 pagesGSB Samaj Foundation - List of Goud Saraswat Brahmin SurnamesShree Vishnu ShastriNo ratings yet

- Cut List Cheat SheetDocument1 pageCut List Cheat SheetmeredithNo ratings yet

- CV Examples Uk StudentDocument8 pagesCV Examples Uk Studente7648d37100% (1)

- Pumba Cap 3 2022Document15 pagesPumba Cap 3 2022adityakamble070103No ratings yet

- Cable Incendio 2X18 Awg S/P: UL1424FPLRDocument1 pageCable Incendio 2X18 Awg S/P: UL1424FPLR04143510504gallucciNo ratings yet

- Study On Vehicle Loan Disbursement ProceDocument11 pagesStudy On Vehicle Loan Disbursement ProceRuby PrajapatiNo ratings yet

- Irene RAYOS-OMBAC, Complainant, Orlando A. RAYOS, RespondentDocument5 pagesIrene RAYOS-OMBAC, Complainant, Orlando A. RAYOS, RespondentGraceNo ratings yet

- Display CAT PDFDocument2 pagesDisplay CAT PDFAndres130No ratings yet

- SIM7000 Series - AT Command Manual - V1.01Document163 pagesSIM7000 Series - AT Command Manual - V1.01Bill CheimarasNo ratings yet

- A Profect Report On Star Claytech Pvt. LTDDocument44 pagesA Profect Report On Star Claytech Pvt. LTDraj danichaNo ratings yet

- MatchmakerDocument43 pagesMatchmakerMatthew MckayNo ratings yet

- XrayDocument9 pagesXraySohail AhmedNo ratings yet

- Funda ExamDocument115 pagesFunda ExamKate Onniel RimandoNo ratings yet

- Code of Practice For Power System ProtectionDocument3 pagesCode of Practice For Power System ProtectionVinit JhingronNo ratings yet

- AnswersDocument24 pagesAnswersDeul ErNo ratings yet

- Mazlan's Lecture MNE - Fire Fighting SystemDocument34 pagesMazlan's Lecture MNE - Fire Fighting SystemTuan JalaiNo ratings yet

- Dqs259 Assignment 2_question [Mar-Aug 2024]Document12 pagesDqs259 Assignment 2_question [Mar-Aug 2024]CrackedCoreNo ratings yet

- ICC Air 2009 CL387 - SrpskiDocument2 pagesICC Air 2009 CL387 - SrpskiZoran DimitrijevicNo ratings yet

- Zxy 110 DatasheetDocument2 pagesZxy 110 DatasheetitembolehNo ratings yet

- Profile: NR Technoserve Pvt. Ltd. 2016 - PresentDocument2 pagesProfile: NR Technoserve Pvt. Ltd. 2016 - PresentSuvam MohapatraNo ratings yet

- How A GPU Works: Kayvon Fatahalian 15-462 (Fall 2011)Document87 pagesHow A GPU Works: Kayvon Fatahalian 15-462 (Fall 2011)Michaele ErmiasNo ratings yet

- Student Mentor RolesDocument5 pagesStudent Mentor RolesAravind MohanNo ratings yet

- Bathroom Items Any RFQDocument8 pagesBathroom Items Any RFQarqsarqsNo ratings yet

- Temidayo Cybercrime ReportDocument13 pagesTemidayo Cybercrime ReportMAYOWA ADEBAYONo ratings yet

- PointersDocument147 pagesPointersSoumya VijoyNo ratings yet

- M Cecconi 2023 Intensive Care FundamentalsDocument278 pagesM Cecconi 2023 Intensive Care FundamentalsGustavo ParedesNo ratings yet

- Connorm Edid6507-Assign 2Document27 pagesConnorm Edid6507-Assign 2api-399872156No ratings yet

- KickStart 19Document2 pagesKickStart 19Venu GopalNo ratings yet

- Berlin BlocadeDocument2 pagesBerlin BlocadeRitik TyagiNo ratings yet

![Dqs259 Assignment 2_question [Mar-Aug 2024]](https://imgv2-2-f.scribdassets.com/img/document/747277161/149x198/98cbcf6efd/1719923930?v=1)

Download as xlsx, pdf, or txt

You might also like

- India: Shift Allowance and Compensatory Off PolicyDocument3 pagesIndia: Shift Allowance and Compensatory Off PolicySahil JunejaNo ratings yet

- India Benefits UpdatedDocument2 pagesIndia Benefits UpdatedRavi GoyalNo ratings yet

- CTC Break UpDocument100 pagesCTC Break UpnareshNo ratings yet

- 4 - Hydro Jetting and Sludge RemovalDocument18 pages4 - Hydro Jetting and Sludge RemovalPerwez21100% (2)

- The List of Components Which You Can Use For Salary BreakupDocument8 pagesThe List of Components Which You Can Use For Salary BreakupAnonymous VhqxrXNo ratings yet

- Whichever Is Lower Is Exempt From Tax. For ExampleDocument13 pagesWhichever Is Lower Is Exempt From Tax. For ExampleNasir AhmedNo ratings yet

- Insync CTC Breakup PDFDocument1 pageInsync CTC Breakup PDFSocialIndostoriesNo ratings yet

- Salary Break Up HRDocument4 pagesSalary Break Up HRnaman156No ratings yet

- What Is A Flexible Benefit Plan in A Salary Breakup? - QuoraDocument8 pagesWhat Is A Flexible Benefit Plan in A Salary Breakup? - QuoraSiNo ratings yet

- CTC - Salary Slip - The Very Basic VersionDocument2 pagesCTC - Salary Slip - The Very Basic VersionAJAY KULKARNI100% (2)

- Presented By,: Shraddha Dhatrak (01) Priyanka Ghatrat Mayuri Koli Sneha MoreDocument30 pagesPresented By,: Shraddha Dhatrak (01) Priyanka Ghatrat Mayuri Koli Sneha MoreshraddhavanjariNo ratings yet

- Salary, Net Salary, Gross Salary, Cost To Company Are They Same or Different. For Most People It IsDocument6 pagesSalary, Net Salary, Gross Salary, Cost To Company Are They Same or Different. For Most People It IsAnonymous CwxsRiwNo ratings yet

- CTC Salary CalculatorDocument1 pageCTC Salary CalculatorsavideshwalNo ratings yet

- PF Esi Calculation Sheet ExampleDocument3 pagesPF Esi Calculation Sheet ExampleRajinder KumarNo ratings yet

- Annexure II Details of AllowancesDocument4 pagesAnnexure II Details of AllowancesPravin Balasaheb GunjalNo ratings yet

- Quikchex CTC CalculatorDocument8 pagesQuikchex CTC CalculatoriamgodrajeshNo ratings yet

- Employee Benfit & ServicesDocument14 pagesEmployee Benfit & Servicesaloha123456No ratings yet

- Auto CTC Salary CalculatorDocument1 pageAuto CTC Salary CalculatorSathvika SaaraNo ratings yet

- Income Under The Head "Salaries": Shubhangi Gupta Roll No. 11 Financial Management Bhartiya Vidya BhavanDocument44 pagesIncome Under The Head "Salaries": Shubhangi Gupta Roll No. 11 Financial Management Bhartiya Vidya Bhavanhny0910No ratings yet

- Few Points To Be Kept in Mind While Doing Investment DeclarationDocument8 pagesFew Points To Be Kept in Mind While Doing Investment Declarationcool rock MohindraNo ratings yet

- Higher Pension As Per SC Decision With Calculation - Synopsis1Document13 pagesHigher Pension As Per SC Decision With Calculation - Synopsis1hariveerNo ratings yet

- Pay SlipDocument50 pagesPay SlipSushil Shrestha100% (1)

- CHRC869Document3 pagesCHRC869jvnraoNo ratings yet

- 3RD PRC Presentation-1Document25 pages3RD PRC Presentation-1sai krishna krishnaNo ratings yet

- Darshan Shetty - AnnexureDocument1 pageDarshan Shetty - Annexuredarshan shettyNo ratings yet

- Salary Calculation Yearly & Monthly Break Up of Gross SalaryDocument2 pagesSalary Calculation Yearly & Monthly Break Up of Gross Salarymoh300No ratings yet

- Overtime AllowanceDocument3 pagesOvertime AllowanceKumudha Devi100% (1)

- Benefits & Contributory Conditions: (I) (A) Sickness BenefitDocument4 pagesBenefits & Contributory Conditions: (I) (A) Sickness BenefitKunwar Sa Amit SinghNo ratings yet

- Salary Structure: Please Put The Gross Salry in Red Column in Any Slab, U Will Find StructureDocument6 pagesSalary Structure: Please Put The Gross Salry in Red Column in Any Slab, U Will Find StructureSagar ShindeNo ratings yet

- Compensation Rules and Salary Design GuidelinesDocument6 pagesCompensation Rules and Salary Design GuidelinesDivya NatarajanNo ratings yet

- Family Pension SchemeDocument15 pagesFamily Pension SchemeJitu Choudhary100% (1)

- Salary StructureDocument4 pagesSalary StructureniranjanaNo ratings yet

- LDocument7 pagesLaman anandNo ratings yet

- DGM Annexure B Know Your Pay ComponentsDocument3 pagesDGM Annexure B Know Your Pay ComponentsaakritishellNo ratings yet

- Allowances Under Income Tax Act1961Document12 pagesAllowances Under Income Tax Act1961Sahil14JNo ratings yet

- EPF CalenderDocument1 pageEPF CalenderAmitav TalukdarNo ratings yet

- National Pension Scheme (NPS) Guidelines FY 2019-20Document21 pagesNational Pension Scheme (NPS) Guidelines FY 2019-20harrishNo ratings yet

- Salary Slip Format in PDF All PDFDocument3 pagesSalary Slip Format in PDF All PDFRajeev GunasekaranNo ratings yet

- SubhashDocument1 pageSubhashsubhash221103No ratings yet

- Salary Break UpDocument17 pagesSalary Break UpRam Surya Prakash DommetiNo ratings yet

- Provident Fund (PF)Document13 pagesProvident Fund (PF)chandub6No ratings yet

- Novartis NPS Employee Awareness Presentation PDFDocument33 pagesNovartis NPS Employee Awareness Presentation PDFMohan CNo ratings yet

- Salary AdministrationDocument17 pagesSalary AdministrationMae Ann GonzalesNo ratings yet

- EPF Provident Fund CalculatorDocument6 pagesEPF Provident Fund CalculatorUtkal SolankiNo ratings yet

- Tata Consultancy Layer FormatDocument21 pagesTata Consultancy Layer FormatChinnu SalimathNo ratings yet

- Salary Breakup Calculator ExcelDocument2 pagesSalary Breakup Calculator ExcelAnup RawatNo ratings yet

- NPS PPT - HDFC BankDocument17 pagesNPS PPT - HDFC BankPankaj Kothari100% (1)

- Sallary AllowanceDocument15 pagesSallary AllowanceKeval PatelNo ratings yet

- CCS LTC RULES PPT 20210617141434Document28 pagesCCS LTC RULES PPT 20210617141434Kumar KumarNo ratings yet

- Employees' State Insurance Corporation E-Pehchan Card: Insured Person: Insurance No.: Date of RegistrationDocument3 pagesEmployees' State Insurance Corporation E-Pehchan Card: Insured Person: Insurance No.: Date of RegistrationGoutam HotaNo ratings yet

- CTS Marriage Loan PolicyDocument5 pagesCTS Marriage Loan PolicyshaannivasNo ratings yet

- New Incentive Structure - Sales TeamDocument2 pagesNew Incentive Structure - Sales TeamvishnuindianNo ratings yet

- Pension CalculationDocument1 pagePension Calculationulmilu15No ratings yet

- Salary Break Up - DamanDocument16 pagesSalary Break Up - Damanvirag_shahsNo ratings yet

- Appointment Salary BreakupDocument1 pageAppointment Salary BreakupPhani KumarNo ratings yet

- Compliance Manual F.Y. 2020 21 A.Y.2021 22 PDFDocument52 pagesCompliance Manual F.Y. 2020 21 A.Y.2021 22 PDFTHERMAL TECH ENGINEERINGNo ratings yet

- Salary Tax CalculatorDocument7 pagesSalary Tax Calculatorbecito6195No ratings yet

- Maulana Azad National Urdu University: CircularDocument4 pagesMaulana Azad National Urdu University: CircularDebasish BiswalNo ratings yet

- Direct Tax Code: Capital Gains Tax On Sale of Residential PropertyDocument5 pagesDirect Tax Code: Capital Gains Tax On Sale of Residential Propertykarthikeyan.mohandossNo ratings yet

- Salaries PresentationDocument21 pagesSalaries PresentationDipika PandaNo ratings yet

- Compensation Analysis of Manufacturing IndustriesDocument14 pagesCompensation Analysis of Manufacturing IndustriesSankar Rajan100% (13)

- GSB Samaj Foundation - List of Goud Saraswat Brahmin SurnamesDocument2 pagesGSB Samaj Foundation - List of Goud Saraswat Brahmin SurnamesShree Vishnu ShastriNo ratings yet

- Cut List Cheat SheetDocument1 pageCut List Cheat SheetmeredithNo ratings yet

- CV Examples Uk StudentDocument8 pagesCV Examples Uk Studente7648d37100% (1)

- Pumba Cap 3 2022Document15 pagesPumba Cap 3 2022adityakamble070103No ratings yet

- Cable Incendio 2X18 Awg S/P: UL1424FPLRDocument1 pageCable Incendio 2X18 Awg S/P: UL1424FPLR04143510504gallucciNo ratings yet

- Study On Vehicle Loan Disbursement ProceDocument11 pagesStudy On Vehicle Loan Disbursement ProceRuby PrajapatiNo ratings yet

- Irene RAYOS-OMBAC, Complainant, Orlando A. RAYOS, RespondentDocument5 pagesIrene RAYOS-OMBAC, Complainant, Orlando A. RAYOS, RespondentGraceNo ratings yet

- Display CAT PDFDocument2 pagesDisplay CAT PDFAndres130No ratings yet

- SIM7000 Series - AT Command Manual - V1.01Document163 pagesSIM7000 Series - AT Command Manual - V1.01Bill CheimarasNo ratings yet

- A Profect Report On Star Claytech Pvt. LTDDocument44 pagesA Profect Report On Star Claytech Pvt. LTDraj danichaNo ratings yet

- MatchmakerDocument43 pagesMatchmakerMatthew MckayNo ratings yet

- XrayDocument9 pagesXraySohail AhmedNo ratings yet

- Funda ExamDocument115 pagesFunda ExamKate Onniel RimandoNo ratings yet

- Code of Practice For Power System ProtectionDocument3 pagesCode of Practice For Power System ProtectionVinit JhingronNo ratings yet

- AnswersDocument24 pagesAnswersDeul ErNo ratings yet

- Mazlan's Lecture MNE - Fire Fighting SystemDocument34 pagesMazlan's Lecture MNE - Fire Fighting SystemTuan JalaiNo ratings yet

- Dqs259 Assignment 2_question [Mar-Aug 2024]Document12 pagesDqs259 Assignment 2_question [Mar-Aug 2024]CrackedCoreNo ratings yet

- ICC Air 2009 CL387 - SrpskiDocument2 pagesICC Air 2009 CL387 - SrpskiZoran DimitrijevicNo ratings yet

- Zxy 110 DatasheetDocument2 pagesZxy 110 DatasheetitembolehNo ratings yet

- Profile: NR Technoserve Pvt. Ltd. 2016 - PresentDocument2 pagesProfile: NR Technoserve Pvt. Ltd. 2016 - PresentSuvam MohapatraNo ratings yet

- How A GPU Works: Kayvon Fatahalian 15-462 (Fall 2011)Document87 pagesHow A GPU Works: Kayvon Fatahalian 15-462 (Fall 2011)Michaele ErmiasNo ratings yet

- Student Mentor RolesDocument5 pagesStudent Mentor RolesAravind MohanNo ratings yet

- Bathroom Items Any RFQDocument8 pagesBathroom Items Any RFQarqsarqsNo ratings yet

- Temidayo Cybercrime ReportDocument13 pagesTemidayo Cybercrime ReportMAYOWA ADEBAYONo ratings yet

- PointersDocument147 pagesPointersSoumya VijoyNo ratings yet

- M Cecconi 2023 Intensive Care FundamentalsDocument278 pagesM Cecconi 2023 Intensive Care FundamentalsGustavo ParedesNo ratings yet

- Connorm Edid6507-Assign 2Document27 pagesConnorm Edid6507-Assign 2api-399872156No ratings yet

- KickStart 19Document2 pagesKickStart 19Venu GopalNo ratings yet

- Berlin BlocadeDocument2 pagesBerlin BlocadeRitik TyagiNo ratings yet