Download as pdf or txt

You might also like

- Attachment Disturbances in Adults Treatment For Comprehensive Repair (Etc.) (Z-Library)Document477 pagesAttachment Disturbances in Adults Treatment For Comprehensive Repair (Etc.) (Z-Library)fa ab100% (8)

- Tutorial 5 and 6Document5 pagesTutorial 5 and 6Ahmad HaikalNo ratings yet

- Calculus BC For DummiesDocument12 pagesCalculus BC For DummiesJoon KoNo ratings yet

- The Rules of Wealth NotesDocument20 pagesThe Rules of Wealth NotesWill Matcham100% (2)

- 6592 - A1 QuestionsDocument14 pages6592 - A1 QuestionsYuhan KENo ratings yet

- Establish Kinder Garden School - Develope Project ManagerDocument25 pagesEstablish Kinder Garden School - Develope Project ManagerVõ Thúy Trân0% (1)

- Econ 335 Wooldridge CH 7Document22 pagesEcon 335 Wooldridge CH 7minhly12104No ratings yet

- Lecture 19: InteractionsDocument4 pagesLecture 19: InteractionsSNo ratings yet

- 2 - Model Linear Jamak Dan OLSDocument11 pages2 - Model Linear Jamak Dan OLSTabahRizkiNo ratings yet

- Transportation ProblemDocument4 pagesTransportation ProblemericNo ratings yet

- Clifford S AlgebraDocument90 pagesClifford S AlgebraJorgeGrajalesRivera100% (1)

- SVM ExampleDocument10 pagesSVM ExampleYash AgarwalNo ratings yet

- 04 Violation of Assumptions AllDocument24 pages04 Violation of Assumptions AllFasiko AsmaroNo ratings yet

- 2. Given Information:: 3. Calculate εDocument9 pages2. Given Information:: 3. Calculate εveyeda7265No ratings yet

- 1 Use and Interpretation of Dummy VariablesDocument5 pages1 Use and Interpretation of Dummy Variablesshivani singhNo ratings yet

- Suggested Solutions: Problem Set 5: β = (X X) X YDocument7 pagesSuggested Solutions: Problem Set 5: β = (X X) X YqiucumberNo ratings yet

- Lecturenotes PerceptronDocument7 pagesLecturenotes PerceptronKundan MahasethNo ratings yet

- Lecture 1, Part 3: Training A Classifier: Roger GrosseDocument11 pagesLecture 1, Part 3: Training A Classifier: Roger GrosseShamil shihab pkNo ratings yet

- 03 - Mich - Solutions To Problem Set 1 - Ao319Document13 pages03 - Mich - Solutions To Problem Set 1 - Ao319albertwing1010No ratings yet

- EC212: Introduction To Econometrics Multiple Regression: Estimation (Wooldridge, Ch. 3)Document76 pagesEC212: Introduction To Econometrics Multiple Regression: Estimation (Wooldridge, Ch. 3)SHUMING ZHUNo ratings yet

- Section05 SolutionsDocument9 pagesSection05 Solutionsebi1234No ratings yet

- Semester 1Document44 pagesSemester 1Tom DavisNo ratings yet

- Violation of (Weak) Exogeneity AssumptionDocument34 pagesViolation of (Weak) Exogeneity AssumptionKaushiki SenguptaNo ratings yet

- Solutions Problem Set 1Document7 pagesSolutions Problem Set 1sanketjaiswalNo ratings yet

- Regression Analysis: Ordinary Least SquaresDocument12 pagesRegression Analysis: Ordinary Least Squaresmpc.9315970No ratings yet

- Wooldridge 6e Ch09 SSMDocument8 pagesWooldridge 6e Ch09 SSMJakob ThoriusNo ratings yet

- Continuidad Problemas SelectosDocument4 pagesContinuidad Problemas SelectosFlorentino HMNo ratings yet

- Mult RegressionDocument28 pagesMult Regressioniabureid7460No ratings yet

- Definition: A Vector-Argument, Real Valued Function G (X) Is Strictly Convex IffDocument2 pagesDefinition: A Vector-Argument, Real Valued Function G (X) Is Strictly Convex IffnakinhoNo ratings yet

- ReaderDocument2 pagesReadercrazyaznraver13No ratings yet

- GMAT Mock 35 SolDocument11 pagesGMAT Mock 35 SolSrikanth Chowdary DareNo ratings yet

- Linear ModelsDocument36 pagesLinear ModelsIstiaq AkbarNo ratings yet

- Week1 SolutionsDocument5 pagesWeek1 Solutionsavani.goenkaug25No ratings yet

- ECON 1630 Problem Set #2 Fall 2021: Bias VarianceDocument9 pagesECON 1630 Problem Set #2 Fall 2021: Bias VarianceMel CuiNo ratings yet

- Materi Fismat Bab 2Document33 pagesMateri Fismat Bab 2novitia latifahNo ratings yet

- Multiple Regression Analysis: I 0 1 I1 K Ik IDocument30 pagesMultiple Regression Analysis: I 0 1 I1 K Ik Iajayikayode100% (1)

- 斯坦福大学机器学习数学基础 33-40Document8 pages斯坦福大学机器学习数学基础 33-402285145156No ratings yet

- Lecture 2, Part 2: Backpropagation: Roger GrosseDocument9 pagesLecture 2, Part 2: Backpropagation: Roger GrosseDhaval PatelNo ratings yet

- EECS 16A - Note1Document18 pagesEECS 16A - Note1Ram VNo ratings yet

- PHY250 Lectures1-8 CompleteDocument48 pagesPHY250 Lectures1-8 CompleteawirogoNo ratings yet

- GMAT QUANT TOPIC 3 (Inequalities + Absolute Value) SolutionsDocument46 pagesGMAT QUANT TOPIC 3 (Inequalities + Absolute Value) SolutionsBhagath GottipatiNo ratings yet

- Convexity Examples: CE 377K Stephen D. Boyles Spring 2015Document11 pagesConvexity Examples: CE 377K Stephen D. Boyles Spring 2015hoalongkiemNo ratings yet

- Math 4310 Handout - Quotient Vector Spaces: Dan CollinsDocument5 pagesMath 4310 Handout - Quotient Vector Spaces: Dan CollinsVATSAL KEDIANo ratings yet

- CH 06Document22 pagesCH 06xpj25tpfq4No ratings yet

- Answers To Odd-Numbered Exercises For Fox, Applied Regression AnalysisDocument151 pagesAnswers To Odd-Numbered Exercises For Fox, Applied Regression AnalysisFrances YuanNo ratings yet

- Complex Analysis - K. HoustonDocument38 pagesComplex Analysis - K. HoustonWilliam Pajak100% (2)

- 2959 Complex AnalysisDocument77 pages2959 Complex AnalysisAngel DaniellaNo ratings yet

- 401 Endterm 2020Document3 pages401 Endterm 2020Anuj DiwediNo ratings yet

- 6 Rational Functions & Partial Fraction DecompositionDocument6 pages6 Rational Functions & Partial Fraction Decompositiona2hasijaNo ratings yet

- Chapter 6Document5 pagesChapter 6LALANo ratings yet

- 1 - The "Algorithm".: There Is A Typo in The Book)Document3 pages1 - The "Algorithm".: There Is A Typo in The Book)Parveen DagarNo ratings yet

- Statistical Machine Learning Solutions For Exam 2019-03-15Document5 pagesStatistical Machine Learning Solutions For Exam 2019-03-15Yu Ching LeeNo ratings yet

- Complex Analysis - HoustonDocument98 pagesComplex Analysis - HoustonPablo MartínezNo ratings yet

- KECCAK Verification 1Document10 pagesKECCAK Verification 1beyousmart95No ratings yet

- CalculusForEveryone ch27Document5 pagesCalculusForEveryone ch27kmishchuk17No ratings yet

- Mat 217 Group 7 EXACT DIFFERENTIAL EQUATIONDocument5 pagesMat 217 Group 7 EXACT DIFFERENTIAL EQUATIONOlonade TeniolaNo ratings yet

- Practice MidtermDocument4 pagesPractice MidtermArka MitraNo ratings yet

- MathReview 2Document31 pagesMathReview 2resperadoNo ratings yet

- Hw3 SolutionsDocument7 pagesHw3 Solutionsmahamd saiedNo ratings yet

- FubiniDocument5 pagesFubiniAloke ChatterjeeNo ratings yet

- Algebra IDocument694 pagesAlgebra IKristi Rogers0% (1)

- 3 - Mathematics in TeXDocument7 pages3 - Mathematics in TeXWill MatchamNo ratings yet

- System of EquationsDocument5 pagesSystem of EquationsWill MatchamNo ratings yet

- Linear Alegbra 1aDocument1 pageLinear Alegbra 1aWill MatchamNo ratings yet

- Butterflies and MothsDocument59 pagesButterflies and MothsReegen Tee100% (3)

- InglesDocument5 pagesInglesJessi mondragonNo ratings yet

- The Stolen Party ThesisDocument8 pagesThe Stolen Party Thesisfexschhld100% (2)

- Identifying Figures of Speech (Simile, Metaphor, and Personification)Document10 pagesIdentifying Figures of Speech (Simile, Metaphor, and Personification)khem ConstantinoNo ratings yet

- The African Essentials - Presentation - O - 2019Document34 pagesThe African Essentials - Presentation - O - 2019Fatima SilvaNo ratings yet

- C4 Tech Spec Issue 2Document5 pagesC4 Tech Spec Issue 2Дмитрий КалининNo ratings yet

- Surat Smart City S CPDocument179 pagesSurat Smart City S CPJabir AghadiNo ratings yet

- How To Cite A Research Paper in TextDocument8 pagesHow To Cite A Research Paper in Textafnkaufhczyvbc100% (1)

- English 8-Q4-M1-Grammatical SignalsDocument12 pagesEnglish 8-Q4-M1-Grammatical SignalsShekayna PalagtiwNo ratings yet

- Reactor and Regenerator System of FCCDocument67 pagesReactor and Regenerator System of FCCDai NamNo ratings yet

- MEDINA, Chandra Micole P. - Activity 6 Both A and BDocument2 pagesMEDINA, Chandra Micole P. - Activity 6 Both A and BChandra Micole MedinaNo ratings yet

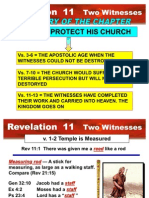

- God Will Protect His Church God Will Protect His ChurchDocument17 pagesGod Will Protect His Church God Will Protect His ChurchLaura GarciaNo ratings yet

- Collections and Recollections by Russell, George William Erskine, 1853-1919Document202 pagesCollections and Recollections by Russell, George William Erskine, 1853-1919Gutenberg.org100% (1)

- Company Profile: TML Drivelines LTD (Tata Motors, Jamshedpur)Document5 pagesCompany Profile: TML Drivelines LTD (Tata Motors, Jamshedpur)Madhav NemalikantiNo ratings yet

- The Wholly BibleDocument10 pagesThe Wholly BibleFred_Carpenter_12No ratings yet

- Cemex Holdings Philippines Annual Report 2016 PDFDocument47 pagesCemex Holdings Philippines Annual Report 2016 PDFFritz NatividadNo ratings yet

- ICH Quality Guidelines - AnuragDocument4 pagesICH Quality Guidelines - AnuragAnurag BhardwajNo ratings yet

- Lessons & Carols Service 2017Document2 pagesLessons & Carols Service 2017Essex Center UMCNo ratings yet

- Ncert Solutions Class 6 Civics Chapter 3 PDFDocument2 pagesNcert Solutions Class 6 Civics Chapter 3 PDFSabaNo ratings yet

- Conditional Sentence and Passive VoiceDocument2 pagesConditional Sentence and Passive Voicedebietamara larentikaNo ratings yet

- Project On SunsilkDocument16 pagesProject On Sunsilkiilm00282% (22)

- KS2 How Do We See ThingsDocument6 pagesKS2 How Do We See ThingsMekala WithanaNo ratings yet

- 8.b SOAL PAT B INGGRIS KELAS 8Document6 pages8.b SOAL PAT B INGGRIS KELAS 8M Adib MasykurNo ratings yet

- Reading Passage 1: Succeed in IELTS Volume 8Document16 pagesReading Passage 1: Succeed in IELTS Volume 8Huyền Kiệt thươngNo ratings yet

- Philo ExamDocument2 pagesPhilo ExamJohn Albert100% (1)

- MOA Motorcycle PolicyDocument3 pagesMOA Motorcycle Policysanyo enterprise100% (2)

- HBO Types of CommunicationsDocument14 pagesHBO Types of CommunicationsJENEVIE B. ODONNo ratings yet

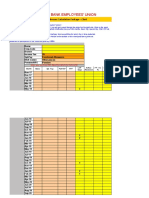

- Karur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDocument10 pagesKarur Vysya Bank Employees' Union: 11th Bipartite Arrears Calculation Package - ClerkDeepa ManianNo ratings yet