Download as pdf or txt

You might also like

- Case Notes EcoPakDocument8 pagesCase Notes EcoPakGajan SelvaNo ratings yet

- Linklaters Schwab ReportDocument81 pagesLinklaters Schwab Reportkiting28No ratings yet

- Chapter 01Document5 pagesChapter 01Alima Toon Noor Ridita 1612638630No ratings yet

- Test Bank Chapter 9Document10 pagesTest Bank Chapter 9Rebecca StephanieNo ratings yet

- 3-3 Franking AccountDocument1 page3-3 Franking Accountoddsey0713No ratings yet

- Does FBT Apply?: Div 13 ExclusionsDocument1 pageDoes FBT Apply?: Div 13 Exclusionsoddsey0713No ratings yet

- 4-3 Part IVA General AntiAvoidanceDocument1 page4-3 Part IVA General AntiAvoidanceoddsey0713No ratings yet

- 1-8 GST - GST Payable or ITC AvalDocument2 pages1-8 GST - GST Payable or ITC Avaloddsey0713No ratings yet

- 2-3 Capital AllowancesDocument1 page2-3 Capital Allowancesoddsey0713No ratings yet

- Ratio Analysis Is Very Useful Tool of Management AccountingDocument13 pagesRatio Analysis Is Very Useful Tool of Management AccountingSonal PorwalNo ratings yet

- Adjustments at The End of An Accounting PeriodDocument18 pagesAdjustments at The End of An Accounting PeriodTevabless Suoived SpotlightbabeNo ratings yet

- Module 2Document12 pagesModule 2zoyaNo ratings yet

- CPA TAX Notes - Module 1Document4 pagesCPA TAX Notes - Module 1wumel01No ratings yet

- Capital Budgeting Decision - SBSDocument43 pagesCapital Budgeting Decision - SBSSahil SherasiyaNo ratings yet

- Income Taxes (IAS 12)Document15 pagesIncome Taxes (IAS 12)Mahir RahmanNo ratings yet

- FRM NotesDocument13 pagesFRM NotesNeeraj LowanshiNo ratings yet

- CBIDocument39 pagesCBIVMRONo ratings yet

- Types of Financial RisksDocument5 pagesTypes of Financial RisksShaharyar QayumNo ratings yet

- Calculating Capital Gains TaxDocument5 pagesCalculating Capital Gains TaxAsif A. MemonNo ratings yet

- Start Your BusinessDocument8 pagesStart Your BusinessIqbal MOUSSANo ratings yet

- cREATIVE ACCOUNTINGDocument12 pagescREATIVE ACCOUNTINGAshraful Jaygirdar0% (1)

- Smieliauskas 6e - Solutions Manual - Chapter 02Document14 pagesSmieliauskas 6e - Solutions Manual - Chapter 02scribdteaNo ratings yet

- Section A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Document24 pagesSection A: Multiple Choice Questions - Single Option: This Section Has 70 Questions Worth 1 Mark Each (Total of 70 Marks)Kenny HoNo ratings yet

- What Is A Profit and Loss (P&L) Statement - InvestopediaDocument16 pagesWhat Is A Profit and Loss (P&L) Statement - InvestopediaFrancisco Del PuertoNo ratings yet

- Taxation Module1Document55 pagesTaxation Module1Techbotix AppsNo ratings yet

- Actuarial Glossary PDFDocument18 pagesActuarial Glossary PDFmiguelNo ratings yet

- Colgate-Financial-Model-Solved-Wallstreetmojo ComDocument34 pagesColgate-Financial-Model-Solved-Wallstreetmojo Comapi-300740104No ratings yet

- Cash Flow Forecasting in Construction Finance 3Document7 pagesCash Flow Forecasting in Construction Finance 3GeorgeNo ratings yet

- CMA P3 Finance 4Document23 pagesCMA P3 Finance 4Hamza Lutaf UllahNo ratings yet

- AC2091 ZB Final For UoLDocument16 pagesAC2091 ZB Final For UoLkikiNo ratings yet

- Insurance AccountingDocument16 pagesInsurance Accountingssp2000No ratings yet

- 04 Working Capital Management and Corporate GovernanceDocument26 pages04 Working Capital Management and Corporate GovernanceKrutika NandanNo ratings yet

- Part 3 - Understanding Financial Statements and ReportsDocument7 pagesPart 3 - Understanding Financial Statements and ReportsJeanrey AlcantaraNo ratings yet

- Smieliauskas 6e - Solutions Manual - Chapter 03Document12 pagesSmieliauskas 6e - Solutions Manual - Chapter 03scribdtea100% (1)

- Analysis Beyond Consensus: The New Abc of ResearchDocument5 pagesAnalysis Beyond Consensus: The New Abc of Researchanupbhansali2004No ratings yet

- Presentation On Unit Linked Insurance Plan: Shri D.K.Mondal, Asst. Secretary (Marketing) Central Office, MumbaiDocument42 pagesPresentation On Unit Linked Insurance Plan: Shri D.K.Mondal, Asst. Secretary (Marketing) Central Office, Mumbaijamesbond786No ratings yet

- Summary - Lectures PDFDocument57 pagesSummary - Lectures PDFYafeah Diokno100% (1)

- Risk Management Guide For Small To Medium BusinessesDocument10 pagesRisk Management Guide For Small To Medium BusinessesroldoguidoNo ratings yet

- Tax Book 2016-17 - Version 1.0a USB PDFDocument372 pagesTax Book 2016-17 - Version 1.0a USB PDFemc2_mcv100% (2)

- TABL2751 2016-2 Tutorial Program FinalDocument25 pagesTABL2751 2016-2 Tutorial Program FinalAnna ChenNo ratings yet

- FAC1501 Learning Unit 4 PDFDocument29 pagesFAC1501 Learning Unit 4 PDFMasixole BokweNo ratings yet

- SMA QuizDocument76 pagesSMA QuizQuỳnh ChâuNo ratings yet

- Tax Function Effectiveness Best Practice ChecklistDocument2 pagesTax Function Effectiveness Best Practice ChecklistGbengaNo ratings yet

- Ratio Analysis - A2-Level-Level-Revision, Business-Studies, Accounting-Finance-Marketing, Ratio-Analysis - Revision WorldDocument5 pagesRatio Analysis - A2-Level-Level-Revision, Business-Studies, Accounting-Finance-Marketing, Ratio-Analysis - Revision WorldFarzan SajwaniNo ratings yet

- Short Intro To M&ADocument103 pagesShort Intro To M&AShivangi MaheshwariNo ratings yet

- Colgate Financial Model UnsolvedDocument31 pagesColgate Financial Model UnsolvedZainab HashmiNo ratings yet

- Academy Course NotesDocument208 pagesAcademy Course NotesPhebin PhilipNo ratings yet

- AC2091 Financial Reporting: Session 4Document40 pagesAC2091 Financial Reporting: Session 4NadiaIssabellaNo ratings yet

- Code of Ethics Part C Professional Accountants in Business 1 Jan 2011Document11 pagesCode of Ethics Part C Professional Accountants in Business 1 Jan 2011James De Torres CarilloNo ratings yet

- Financial Model - Colgate Palmolive (Solved) : Prepared by Dheeraj Vaidya, CFA, FRMDocument27 pagesFinancial Model - Colgate Palmolive (Solved) : Prepared by Dheeraj Vaidya, CFA, FRMMehmet Isbilen100% (1)

- SBL Guide PDFDocument14 pagesSBL Guide PDFAbin AntonyNo ratings yet

- Fp&a Questions v2Document11 pagesFp&a Questions v2wokif64246No ratings yet

- Morning Session Q&ADocument50 pagesMorning Session Q&AGANESH MENONNo ratings yet

- Tax AdministrationDocument93 pagesTax AdministrationRobin LiuNo ratings yet

- CH 12 NotesDocument23 pagesCH 12 NotesBec barronNo ratings yet

- Framework For Business Analysis and Valuation Using Financial StatementsDocument18 pagesFramework For Business Analysis and Valuation Using Financial StatementsFarhat987No ratings yet

- Chapter Two SolutionsDocument9 pagesChapter Two Solutionsapi-3705855No ratings yet

- Income Tax Calculator in ExcelDocument2 pagesIncome Tax Calculator in Excelkirang gandhi50% (2)

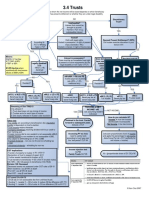

- 3-4 TrustsDocument1 page3-4 Trustsoddsey0713No ratings yet

- 1-8 GST - GST Payable or ITC AvalDocument2 pages1-8 GST - GST Payable or ITC Avaloddsey0713No ratings yet

- Does FBT Apply?: Div 13 ExclusionsDocument1 pageDoes FBT Apply?: Div 13 Exclusionsoddsey0713No ratings yet

- 3-3 Company LossesDocument1 page3-3 Company Lossesoddsey0713No ratings yet

- 3-3 Franking AccountDocument1 page3-3 Franking Accountoddsey0713No ratings yet

- 2-3 Capital AllowancesDocument1 page2-3 Capital Allowancesoddsey0713No ratings yet

- 4-3 Part IVA General AntiAvoidanceDocument1 page4-3 Part IVA General AntiAvoidanceoddsey0713No ratings yet

- 2-4,5 Capital WorksDocument1 page2-4,5 Capital Worksoddsey0713No ratings yet

- Case Summaries 1 193Document54 pagesCase Summaries 1 193oddsey0713100% (1)

- T6 Chapter 5 Solutions To The Essential ActivitiesDocument12 pagesT6 Chapter 5 Solutions To The Essential Activitiesoddsey0713No ratings yet

- T7 Chapter 6 Solutions To The Essential ActivitiesDocument26 pagesT7 Chapter 6 Solutions To The Essential Activitiesoddsey0713No ratings yet

- Circular No. 902Document10 pagesCircular No. 902jc cayananNo ratings yet

- The Internal Environment: Value Creating ActivitiesDocument18 pagesThe Internal Environment: Value Creating ActivitiessarmithaNo ratings yet

- Integration SAPDocument6 pagesIntegration SAPMuhammad Afzal100% (2)

- Janina Louise Caliboso Bsa 3A: Tax Reform For Acceleration and Inclusion (TRAIN) "Document3 pagesJanina Louise Caliboso Bsa 3A: Tax Reform For Acceleration and Inclusion (TRAIN) "Ja CalibosoNo ratings yet

- The Effect of Pandemic On The Nigeria Economy: October 2020Document35 pagesThe Effect of Pandemic On The Nigeria Economy: October 2020DominicNo ratings yet

- Chapter Thirteen: Retailing and WholesalingDocument63 pagesChapter Thirteen: Retailing and WholesalingAaditya UdupaNo ratings yet

- Accounting 1 Accounting For InventoryDocument12 pagesAccounting 1 Accounting For InventoryAshraf AminNo ratings yet

- Detroit Case StudyDocument2 pagesDetroit Case Studyjohnnnnn280% (1)

- Hospitality Industry Environmental Management Systems and StrategiesDocument14 pagesHospitality Industry Environmental Management Systems and StrategiesNoshka Diane IguetNo ratings yet

- Tax Law Case BriefDocument8 pagesTax Law Case BriefDhineshNo ratings yet

- The Secret To: Japanese SuccessDocument26 pagesThe Secret To: Japanese SuccessHenryNo ratings yet

- Online Trading AssignmentDocument72 pagesOnline Trading AssignmentKr Ish NaNo ratings yet

- 1 Darna Perpetual PDFDocument1 page1 Darna Perpetual PDFZemin MorenoNo ratings yet

- BK Performance Manager Human ResourcesDocument14 pagesBK Performance Manager Human ResourcesJohn CheekanalNo ratings yet

- (Download PDF) Business and Society Ethics Sustainability and Stakeholder Management Archie B Carroll Online Ebook All Chapter PDFDocument42 pages(Download PDF) Business and Society Ethics Sustainability and Stakeholder Management Archie B Carroll Online Ebook All Chapter PDFmisty.black182100% (13)

- Class Work Chapter 5 Part ADocument2 pagesClass Work Chapter 5 Part Aaura fitrah auliya SomantriNo ratings yet

- Trading PracticesDocument2 pagesTrading PracticesRocio FernándezNo ratings yet

- Models of Financial Mathematics, MTMM.00.203Document3 pagesModels of Financial Mathematics, MTMM.00.203resufahmedNo ratings yet

- Lesson Plan Economics (Class X)Document2 pagesLesson Plan Economics (Class X)Mrs Manjula Shukla E100% (1)

- BUS 110 Project Tabs and DefinitionsDocument3 pagesBUS 110 Project Tabs and DefinitionsGopiGunigantiNo ratings yet

- Financial Report Nestlé 2019Document140 pagesFinancial Report Nestlé 2019Zulhafeez HasbollahNo ratings yet

- Shein Vi Grp2Document5 pagesShein Vi Grp2Pamela Nicole AlonzoNo ratings yet

- Financial ControllershipDocument7 pagesFinancial ControllershipKaye LaborteNo ratings yet

- Services Marketing - Question Paper Set-2 (Semester III) PDFDocument3 pagesServices Marketing - Question Paper Set-2 (Semester III) PDFVikas SinghNo ratings yet

- Zurich Kanton Tax AssessmentDocument4 pagesZurich Kanton Tax AssessmentcavalaticaNo ratings yet

- Epf Esi Salary SheetDocument115 pagesEpf Esi Salary Sheethitesh nandawaniNo ratings yet

- Chapter 5 PercentageTaxes - WithillustrationsDocument12 pagesChapter 5 PercentageTaxes - WithillustrationsCathy Marie Angela ArellanoNo ratings yet

- Mishkin EMBFM12eGE CH04Document24 pagesMishkin EMBFM12eGE CH04Omar AbouSalehNo ratings yet