Retrenchment STG

Retrenchment STG

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Home Replication StrategyDocument5 pagesHome Replication StrategyChau Hoang100% (19)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- MODULE 4 Project-Quality-Management TDocument54 pagesMODULE 4 Project-Quality-Management TTewodros TadesseNo ratings yet

- Lone Pine CaféDocument3 pagesLone Pine Caféchan_han123No ratings yet

- Marketing Functions and Roles and Responsibilities of Marketing ManagerDocument19 pagesMarketing Functions and Roles and Responsibilities of Marketing ManagerFayez ShriedehNo ratings yet

- Impact: Natalia Adler, Chief of Social Policy, UNICEF NicaraguaDocument2 pagesImpact: Natalia Adler, Chief of Social Policy, UNICEF NicaraguaKundNo ratings yet

- Infolink College: Instructor: Ashenafi NDocument186 pagesInfolink College: Instructor: Ashenafi NBeka AsraNo ratings yet

- Treatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusDocument14 pagesTreatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusAnanthakumar ANo ratings yet

- Infosys JobsDocument3 pagesInfosys JobsChandan upadhyayNo ratings yet

- Muhammad Aizuddin Aizat Bin Jumhari: Contact InformationDocument4 pagesMuhammad Aizuddin Aizat Bin Jumhari: Contact InformationAndres ShaonNo ratings yet

- Christina Drumm ResumeDocument2 pagesChristina Drumm Resumeapi-272992635No ratings yet

- RBI Circular On Export Finance - 1Document21 pagesRBI Circular On Export Finance - 1Anonymous l0MTRDGu3MNo ratings yet

- Chap 007Document36 pagesChap 007Lee FeiNo ratings yet

- Patni Ar2009Document174 pagesPatni Ar2009chip_blueNo ratings yet

- BALANCE CASH HOLDING AssignDocument3 pagesBALANCE CASH HOLDING AssignJarra Abdurahman100% (2)

- Marketing Plan: 1: Define Your BusinessDocument12 pagesMarketing Plan: 1: Define Your Businessdrken3No ratings yet

- Pharma Analytics: SFE (Sales Force Effectiveness) Sales Analytics, Incentive Compensation & Reporting CapabilitiesDocument94 pagesPharma Analytics: SFE (Sales Force Effectiveness) Sales Analytics, Incentive Compensation & Reporting CapabilitiesDinesh IitmNo ratings yet

- EquityDerivatives Workbook (Version-January2020)Document80 pagesEquityDerivatives Workbook (Version-January2020)parthNo ratings yet

- Code of Ethics GhellaDocument28 pagesCode of Ethics GhellaMassimilianoTerenziNo ratings yet

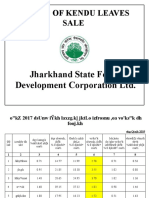

- Status of Kendu Leaves Sale: Jharkhand State Forest Development Corporation LTDDocument11 pagesStatus of Kendu Leaves Sale: Jharkhand State Forest Development Corporation LTDmdNo ratings yet

- 814001-Gabriela GeorgescuDocument86 pages814001-Gabriela GeorgescuJeremiah PacerNo ratings yet

- MA Course Outline (Revised)Document4 pagesMA Course Outline (Revised)Ali Adil0% (1)

- Quality Standards PDFDocument20 pagesQuality Standards PDFmudassarhussainNo ratings yet

- Marketing Notes PDFDocument34 pagesMarketing Notes PDFFRANCIS JOSEPHNo ratings yet

- BT India Factsheet - NewDocument2 pagesBT India Factsheet - NewsunguntNo ratings yet

- MBA HotelDocument46 pagesMBA HotelMamta RanaNo ratings yet

- Slide RMK Chapter 1 - Kelompok 5 - Maksi 43CDocument15 pagesSlide RMK Chapter 1 - Kelompok 5 - Maksi 43CJali FusNo ratings yet

- The Road To Regtech: The (Astonishing) Example of The European UnionDocument12 pagesThe Road To Regtech: The (Astonishing) Example of The European UnionDamero PalominoNo ratings yet

- CompensationDocument36 pagesCompensationabdushababNo ratings yet

- Intellectual CapitalDocument2 pagesIntellectual CapitalraprapNo ratings yet

- Conjoint AnalysisDocument12 pagesConjoint AnalysisvamsibuNo ratings yet

Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Home Replication StrategyDocument5 pagesHome Replication StrategyChau Hoang100% (19)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- MODULE 4 Project-Quality-Management TDocument54 pagesMODULE 4 Project-Quality-Management TTewodros TadesseNo ratings yet

- Lone Pine CaféDocument3 pagesLone Pine Caféchan_han123No ratings yet

- Marketing Functions and Roles and Responsibilities of Marketing ManagerDocument19 pagesMarketing Functions and Roles and Responsibilities of Marketing ManagerFayez ShriedehNo ratings yet

- Impact: Natalia Adler, Chief of Social Policy, UNICEF NicaraguaDocument2 pagesImpact: Natalia Adler, Chief of Social Policy, UNICEF NicaraguaKundNo ratings yet

- Infolink College: Instructor: Ashenafi NDocument186 pagesInfolink College: Instructor: Ashenafi NBeka AsraNo ratings yet

- Treatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusDocument14 pagesTreatment of Assets Under Construction in SAP - From Creation To Settlement - SapGurusAnanthakumar ANo ratings yet

- Infosys JobsDocument3 pagesInfosys JobsChandan upadhyayNo ratings yet

- Muhammad Aizuddin Aizat Bin Jumhari: Contact InformationDocument4 pagesMuhammad Aizuddin Aizat Bin Jumhari: Contact InformationAndres ShaonNo ratings yet

- Christina Drumm ResumeDocument2 pagesChristina Drumm Resumeapi-272992635No ratings yet

- RBI Circular On Export Finance - 1Document21 pagesRBI Circular On Export Finance - 1Anonymous l0MTRDGu3MNo ratings yet

- Chap 007Document36 pagesChap 007Lee FeiNo ratings yet

- Patni Ar2009Document174 pagesPatni Ar2009chip_blueNo ratings yet

- BALANCE CASH HOLDING AssignDocument3 pagesBALANCE CASH HOLDING AssignJarra Abdurahman100% (2)

- Marketing Plan: 1: Define Your BusinessDocument12 pagesMarketing Plan: 1: Define Your Businessdrken3No ratings yet

- Pharma Analytics: SFE (Sales Force Effectiveness) Sales Analytics, Incentive Compensation & Reporting CapabilitiesDocument94 pagesPharma Analytics: SFE (Sales Force Effectiveness) Sales Analytics, Incentive Compensation & Reporting CapabilitiesDinesh IitmNo ratings yet

- EquityDerivatives Workbook (Version-January2020)Document80 pagesEquityDerivatives Workbook (Version-January2020)parthNo ratings yet

- Code of Ethics GhellaDocument28 pagesCode of Ethics GhellaMassimilianoTerenziNo ratings yet

- Status of Kendu Leaves Sale: Jharkhand State Forest Development Corporation LTDDocument11 pagesStatus of Kendu Leaves Sale: Jharkhand State Forest Development Corporation LTDmdNo ratings yet

- 814001-Gabriela GeorgescuDocument86 pages814001-Gabriela GeorgescuJeremiah PacerNo ratings yet

- MA Course Outline (Revised)Document4 pagesMA Course Outline (Revised)Ali Adil0% (1)

- Quality Standards PDFDocument20 pagesQuality Standards PDFmudassarhussainNo ratings yet

- Marketing Notes PDFDocument34 pagesMarketing Notes PDFFRANCIS JOSEPHNo ratings yet

- BT India Factsheet - NewDocument2 pagesBT India Factsheet - NewsunguntNo ratings yet

- MBA HotelDocument46 pagesMBA HotelMamta RanaNo ratings yet

- Slide RMK Chapter 1 - Kelompok 5 - Maksi 43CDocument15 pagesSlide RMK Chapter 1 - Kelompok 5 - Maksi 43CJali FusNo ratings yet

- The Road To Regtech: The (Astonishing) Example of The European UnionDocument12 pagesThe Road To Regtech: The (Astonishing) Example of The European UnionDamero PalominoNo ratings yet

- CompensationDocument36 pagesCompensationabdushababNo ratings yet

- Intellectual CapitalDocument2 pagesIntellectual CapitalraprapNo ratings yet

- Conjoint AnalysisDocument12 pagesConjoint AnalysisvamsibuNo ratings yet