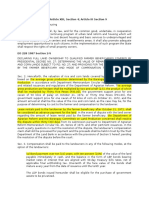

CIR Vs BOAC-Collector Vs Lara

CIR Vs BOAC-Collector Vs Lara

You might also like

- Asociacion de Agricultores V Talisay Silay MillingDocument2 pagesAsociacion de Agricultores V Talisay Silay MillingEmmanuel Ortega67% (3)

- (Template) NEW Notice of Non Response and Fault OneDocument15 pages(Template) NEW Notice of Non Response and Fault OneLexu88% (8)

- FIN300 Homework 4Document4 pagesFIN300 Homework 4John0% (2)

- 2 Limpan Investment Corporation vs. Commissioner, 17 SCRA 703Document9 pages2 Limpan Investment Corporation vs. Commissioner, 17 SCRA 703Anne Marieline BuenaventuraNo ratings yet

- CH 10 TBDocument18 pagesCH 10 TBjhaydn100% (1)

- Chapter 12 ExercisesDocument2 pagesChapter 12 ExercisesAreeba QureshiNo ratings yet

- PBC vs. CIRDocument1 pagePBC vs. CIRMarife MinorNo ratings yet

- Writ of Habeas CorpusDocument18 pagesWrit of Habeas CorpusEmmanuel Ortega100% (4)

- Project On Cash Flow StatementDocument95 pagesProject On Cash Flow Statementravikumarreddyt58% (19)

- GR No. L-18840 Kuenzle & Streiff V CirDocument7 pagesGR No. L-18840 Kuenzle & Streiff V CirRene ValentosNo ratings yet

- Vegetable Oil Corp. V Trinidad, G.R. No. 21475, March 26, 1924, 45 Phil. 822Document2 pagesVegetable Oil Corp. V Trinidad, G.R. No. 21475, March 26, 1924, 45 Phil. 822Maria Fiona Duran MerquitaNo ratings yet

- SISON V ANCHETADocument4 pagesSISON V ANCHETAMayflor BalinuyusNo ratings yet

- CIR vs. Isabela Cultural Corp.Document1 pageCIR vs. Isabela Cultural Corp.Natsu DragneelNo ratings yet

- Bagatsing Vs San Juan (Simbillo)Document3 pagesBagatsing Vs San Juan (Simbillo)Joshua Rizlan SimbilloNo ratings yet

- CIR vs. Burroghs, G.R. No. 66653, June 19, 1986Document1 pageCIR vs. Burroghs, G.R. No. 66653, June 19, 1986Oro ChamberNo ratings yet

- Cir Vs Bank of Commerce DigestDocument1 pageCir Vs Bank of Commerce DigestMimmi ShaneNo ratings yet

- CIR V StanleyDocument15 pagesCIR V StanleyPatatas SayoteNo ratings yet

- 13 Vegetable Oil Corp V TrinidadDocument2 pages13 Vegetable Oil Corp V TrinidadRocky GuzmanNo ratings yet

- Tax VAT CIR Vs GotamcoDocument3 pagesTax VAT CIR Vs GotamcoRhea Mae A. SibalaNo ratings yet

- Gutierrez V CollectorDocument3 pagesGutierrez V Collectormichee coi100% (1)

- Reinald Raven L. Guerrero Taxation Law 1 Surigao Consolidated Mining Co. vs. Collector of Internal Revenue FactsDocument1 pageReinald Raven L. Guerrero Taxation Law 1 Surigao Consolidated Mining Co. vs. Collector of Internal Revenue FactsSapere AudeNo ratings yet

- Pepsi Cola vs. City of ButuanDocument1 pagePepsi Cola vs. City of ButuanArdy Falejo FajutagNo ratings yet

- Case Digest On Taxation 1Document32 pagesCase Digest On Taxation 1Carl Vincent QuitorianoNo ratings yet

- Cir Vs Mega GeneralDocument2 pagesCir Vs Mega GeneralAiken Alagban LadinesNo ratings yet

- Batch 2 - Digested Cases in TaxationDocument20 pagesBatch 2 - Digested Cases in Taxationnikkolad100% (2)

- 136 CIR vs. Vda de PrietoDocument2 pages136 CIR vs. Vda de PrietoMiw Cortes100% (1)

- CIR v. Smith Kline / G.R. No. L-54108 / January 17, 1984Document1 pageCIR v. Smith Kline / G.R. No. L-54108 / January 17, 1984Mini U. SorianoNo ratings yet

- CIR v. Acesite Hotel CorporationDocument2 pagesCIR v. Acesite Hotel CorporationJemima FalinchaoNo ratings yet

- Hilado vs. CIRDocument1 pageHilado vs. CIRAlan GultiaNo ratings yet

- 17 Republic Vs de La RamaDocument3 pages17 Republic Vs de La RamaLara YuloNo ratings yet

- 29 CIR v. CADocument2 pages29 CIR v. CARem SerranoNo ratings yet

- Case Digest - Doctrines in TaxationDocument3 pagesCase Digest - Doctrines in TaxationBryne Angelo BrillantesNo ratings yet

- James V USDocument4 pagesJames V USKTNo ratings yet

- (TAX) Matalin Coconut vs. Municipal Council of MalabangDocument1 page(TAX) Matalin Coconut vs. Municipal Council of Malabangthornapple25100% (1)

- Bagatsing v. San Juan DigestDocument1 pageBagatsing v. San Juan DigestBruno GalwatNo ratings yet

- CIR Vs CA & CastanedaDocument1 pageCIR Vs CA & CastanedaArmstrong BosantogNo ratings yet

- Collector v. LaraDocument2 pagesCollector v. LaraJaypoll DiazNo ratings yet

- Melecio Domingo vs. Lorenzo Garlitos, G.R. No. L-18994, June 29, 1963Document2 pagesMelecio Domingo vs. Lorenzo Garlitos, G.R. No. L-18994, June 29, 1963Bal Nikko Joville - RocamoraNo ratings yet

- Punsalan Vs Municipal Board of ManilaDocument3 pagesPunsalan Vs Municipal Board of ManilaGayFleur Cabatit RamosNo ratings yet

- Ramoso Vs CADocument2 pagesRamoso Vs CARegine Joy MagaboNo ratings yet

- Consolidated Mines, Inc Vs Cta and CirDocument3 pagesConsolidated Mines, Inc Vs Cta and CirKirs Tie100% (3)

- Republic vs. Salud v. HizonDocument2 pagesRepublic vs. Salud v. HizonGyelamagne EstradaNo ratings yet

- Churchill V ConcepcionDocument2 pagesChurchill V ConcepcionKent A. AlonzoNo ratings yet

- Cir v. John Gotamco - SonsDocument2 pagesCir v. John Gotamco - SonsLEIGH TARITZ GANANCIALNo ratings yet

- Taxation 1 Case Analysis 3Document5 pagesTaxation 1 Case Analysis 3PJ OrtizNo ratings yet

- CIR vs. Metro StarDocument1 pageCIR vs. Metro StarRodney SantiagoNo ratings yet

- CIR Vs MarubeniDocument2 pagesCIR Vs MarubeniJocelyn MagbanuaNo ratings yet

- Panasonic Communications Imaging Corporation of The Philippines vs. Commissioner of Internal Revenue, 612 SCRA 18, February 08, 2010Document2 pagesPanasonic Communications Imaging Corporation of The Philippines vs. Commissioner of Internal Revenue, 612 SCRA 18, February 08, 2010idolbondoc100% (1)

- City of Baguio v. Fortunato de Leon GR L-24756Document1 pageCity of Baguio v. Fortunato de Leon GR L-24756Charles Roger RayaNo ratings yet

- Phil. Acetylene Co. Inc. VS Cir, GR No L-19707, Aug 17, 1967Document11 pagesPhil. Acetylene Co. Inc. VS Cir, GR No L-19707, Aug 17, 1967KidMonkey2299No ratings yet

- Kuenzle v. CIRDocument2 pagesKuenzle v. CIRTippy Dos Santos100% (2)

- Gutierrez Vs CollectorDocument2 pagesGutierrez Vs CollectorBenedict AlvarezNo ratings yet

- Us VS LudeyDocument2 pagesUs VS LudeyA Paula Cruz FranciscoNo ratings yet

- Case No. 3 Tax Case DigestDocument3 pagesCase No. 3 Tax Case Digestkc lovessNo ratings yet

- Pepsi v. TanauanDocument2 pagesPepsi v. TanauanKhian JamerNo ratings yet

- COMPAÑIA GENERAL DE TABACOS DE FILIPINAS Vs ManilaDocument2 pagesCOMPAÑIA GENERAL DE TABACOS DE FILIPINAS Vs ManilaLau NunezNo ratings yet

- Tax Ii CasesDocument4 pagesTax Ii CasesBae Irene100% (2)

- Request of Atty. ZialcitaDocument2 pagesRequest of Atty. ZialcitaAngelo Castillo100% (1)

- 10 - CIR V Mega General Merchandising Corp and CTADocument2 pages10 - CIR V Mega General Merchandising Corp and CTAkenken320No ratings yet

- CIR vs. Placer DomeDocument4 pagesCIR vs. Placer DomeAngelo Castillo100% (1)

- Nazareno - LVM CONSTRUCTION CORPORATIONDocument3 pagesNazareno - LVM CONSTRUCTION CORPORATIONNoel Christopher G. BellezaNo ratings yet

- TAX DigestDocument18 pagesTAX DigestBerna BadongenNo ratings yet

- 2 Tax Case DigestDocument11 pages2 Tax Case DigestLean Manuel Paragas0% (1)

- American Express International v. CIR CTA Case No. 6099 (April 19, 2002)Document2 pagesAmerican Express International v. CIR CTA Case No. 6099 (April 19, 2002)Francis Xavier Sinon100% (1)

- Week 5Document15 pagesWeek 5Richelle GraceNo ratings yet

- Digest TaxDocument10 pagesDigest TaxDominic EmbodoNo ratings yet

- Income TaxDocument24 pagesIncome TaxJozele DalupangNo ratings yet

- Invencion Case To Webb CaseDocument44 pagesInvencion Case To Webb CaseEmmanuel OrtegaNo ratings yet

- Philippine Constitution Article XIII, Section 4 Article III Section 9Document28 pagesPhilippine Constitution Article XIII, Section 4 Article III Section 9Emmanuel OrtegaNo ratings yet

- Agrarian Law Midterm ReviewerDocument41 pagesAgrarian Law Midterm ReviewerEmmanuel Ortega100% (3)

- Dissenting Opinion of Justice Puno DigestDocument6 pagesDissenting Opinion of Justice Puno DigestEmmanuel OrtegaNo ratings yet

- Media DigestsDocument4 pagesMedia DigestsEmmanuel OrtegaNo ratings yet

- GMA V PabrigaDocument3 pagesGMA V PabrigaEmmanuel Ortega100% (1)

- Agrarian Week2Document23 pagesAgrarian Week2Emmanuel OrtegaNo ratings yet

- Mactan Electic DigestDocument21 pagesMactan Electic DigestEmmanuel OrtegaNo ratings yet

- Salinas V NLRCDocument2 pagesSalinas V NLRCEmmanuel OrtegaNo ratings yet

- Conference of Maritime Agencies V POEADocument1 pageConference of Maritime Agencies V POEAEmmanuel Ortega100% (2)

- RUPA Vs CADocument4 pagesRUPA Vs CAEmmanuel OrtegaNo ratings yet

- Francisco V NLRCDocument3 pagesFrancisco V NLRCEmmanuel OrtegaNo ratings yet

- DGT - Duncan Vs Glaxo WellcomeDocument3 pagesDGT - Duncan Vs Glaxo WellcomeEmmanuel OrtegaNo ratings yet

- PAL V NLRCDocument2 pagesPAL V NLRCEmmanuel Ortega100% (2)

- Manuel V NC ConstructionDocument2 pagesManuel V NC ConstructionEmmanuel OrtegaNo ratings yet

- DGT - Yrasuegui Vs NLRCDocument6 pagesDGT - Yrasuegui Vs NLRCEmmanuel OrtegaNo ratings yet

- Serrano Vs Gallant Maritime Services DigestDocument6 pagesSerrano Vs Gallant Maritime Services DigestEmmanuel OrtegaNo ratings yet

- Avon Cosmetics V LunaDocument2 pagesAvon Cosmetics V LunaEmmanuel OrtegaNo ratings yet

- Arco Metal Products Co V SAMARM-NAFLUDocument1 pageArco Metal Products Co V SAMARM-NAFLUEmmanuel OrtegaNo ratings yet

- Calalang Vs Williams DigestDocument3 pagesCalalang Vs Williams DigestEmmanuel OrtegaNo ratings yet

- Air Marine v. Balatbat DigestDocument2 pagesAir Marine v. Balatbat DigestEmmanuel OrtegaNo ratings yet

- LABOR - Norkis Trading Vs GniloDocument4 pagesLABOR - Norkis Trading Vs GniloEmmanuel Ortega100% (1)

- Central Bank Employees Vs BSP DigestDocument6 pagesCentral Bank Employees Vs BSP DigestEmmanuel Ortega100% (2)

- Traveno Vs Bobongan DigestDocument1 pageTraveno Vs Bobongan DigestEmmanuel Ortega100% (2)

- Conference of Maritime Agencies, Inc. vs. POEA-DIGESTDocument1 pageConference of Maritime Agencies, Inc. vs. POEA-DIGESTinvictusincNo ratings yet

- PLDT Vs Abucay DigestDocument2 pagesPLDT Vs Abucay DigestEmmanuel Ortega100% (1)

- Case Study On Vnacs: PrashantDocument5 pagesCase Study On Vnacs: PrashantPrashant BagdiaNo ratings yet

- B Stock PricesDocument7 pagesB Stock PricesJenny PabualanNo ratings yet

- GF Difference Between Private and Public Company Structure Under The Corporations ActDocument3 pagesGF Difference Between Private and Public Company Structure Under The Corporations ActUbai M-pireNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicySumit PandeyNo ratings yet

- Time Period Hayden (Net) S&P 500 MSCI World (ACWI)Document13 pagesTime Period Hayden (Net) S&P 500 MSCI World (ACWI)Andy HuffNo ratings yet

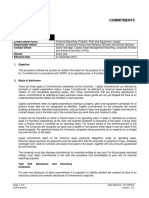

- Definition of CommitmentDocument2 pagesDefinition of CommitmentcrissiekamNo ratings yet

- Principles of Shariah Governing Islamic Investment FundsDocument8 pagesPrinciples of Shariah Governing Islamic Investment Fundsrizwansurti1No ratings yet

- Chapter Four: Incentive PayDocument14 pagesChapter Four: Incentive PayAyesha AfrinNo ratings yet

- 12 Dunayer Distressed M&a Techniques MA05Document6 pages12 Dunayer Distressed M&a Techniques MA05sawilson1No ratings yet

- R&P RULES - GENERAL PRINCIPLES (Revised 08 - 2010Document106 pagesR&P RULES - GENERAL PRINCIPLES (Revised 08 - 2010kunalNo ratings yet

- Paycheck Protection Program Increase Act of 2020 Section-By-Section - FINALDocument2 pagesPaycheck Protection Program Increase Act of 2020 Section-By-Section - FINALFox News50% (4)

- 190 Capitol Subd. v. Negros Occ.Document1 page190 Capitol Subd. v. Negros Occ.Rem SerranoNo ratings yet

- Mindanao Savings and Loan Asso., vs. Edward Willkom (GOJAR)Document2 pagesMindanao Savings and Loan Asso., vs. Edward Willkom (GOJAR)Krizzia GojarNo ratings yet

- Financial Statements and Ratio Analysis: ChapterDocument25 pagesFinancial Statements and Ratio Analysis: Chapterkarim67% (3)

- PHD Research Bureau PHD Chamber of Commerce and IndustryDocument33 pagesPHD Research Bureau PHD Chamber of Commerce and IndustrySUNIL PUJARINo ratings yet

- MEDINA - Homework 1 (Midterm) No. 8Document3 pagesMEDINA - Homework 1 (Midterm) No. 8Von Andrei MedinaNo ratings yet

- Income Tax, Defined:: "The Hardest Thing in The World To Understand Is The Income Tax."Document12 pagesIncome Tax, Defined:: "The Hardest Thing in The World To Understand Is The Income Tax."Ron RamosNo ratings yet

- D.Y. Patil Institute of Master of Computer Applications and ManagementDocument3 pagesD.Y. Patil Institute of Master of Computer Applications and ManagementpltNo ratings yet

- Chap 004Document24 pagesChap 004Hiep LuuNo ratings yet

- HDFC Deposit FormDocument4 pagesHDFC Deposit FormnaguficoNo ratings yet

- ICICI Bank - Click To Pay PDFDocument1 pageICICI Bank - Click To Pay PDFSuzanne WilsonNo ratings yet

- Screenshot 2020-03-18 at 11.13.01 AM PDFDocument2 pagesScreenshot 2020-03-18 at 11.13.01 AM PDFKartik MathukiyaNo ratings yet

- Fredun PharmaDocument37 pagesFredun PharmaBandaru NarendrababuNo ratings yet

- AFAR-01 PartnershipDocument6 pagesAFAR-01 PartnershipRamainne Ronquillo0% (1)

- Working Capital Management SscEDocument38 pagesWorking Capital Management SscEKinNo ratings yet

Download as docx, pdf, or txt

You might also like

- Asociacion de Agricultores V Talisay Silay MillingDocument2 pagesAsociacion de Agricultores V Talisay Silay MillingEmmanuel Ortega67% (3)

- (Template) NEW Notice of Non Response and Fault OneDocument15 pages(Template) NEW Notice of Non Response and Fault OneLexu88% (8)

- FIN300 Homework 4Document4 pagesFIN300 Homework 4John0% (2)

- 2 Limpan Investment Corporation vs. Commissioner, 17 SCRA 703Document9 pages2 Limpan Investment Corporation vs. Commissioner, 17 SCRA 703Anne Marieline BuenaventuraNo ratings yet

- CH 10 TBDocument18 pagesCH 10 TBjhaydn100% (1)

- Chapter 12 ExercisesDocument2 pagesChapter 12 ExercisesAreeba QureshiNo ratings yet

- PBC vs. CIRDocument1 pagePBC vs. CIRMarife MinorNo ratings yet

- Writ of Habeas CorpusDocument18 pagesWrit of Habeas CorpusEmmanuel Ortega100% (4)

- Project On Cash Flow StatementDocument95 pagesProject On Cash Flow Statementravikumarreddyt58% (19)

- GR No. L-18840 Kuenzle & Streiff V CirDocument7 pagesGR No. L-18840 Kuenzle & Streiff V CirRene ValentosNo ratings yet

- Vegetable Oil Corp. V Trinidad, G.R. No. 21475, March 26, 1924, 45 Phil. 822Document2 pagesVegetable Oil Corp. V Trinidad, G.R. No. 21475, March 26, 1924, 45 Phil. 822Maria Fiona Duran MerquitaNo ratings yet

- SISON V ANCHETADocument4 pagesSISON V ANCHETAMayflor BalinuyusNo ratings yet

- CIR vs. Isabela Cultural Corp.Document1 pageCIR vs. Isabela Cultural Corp.Natsu DragneelNo ratings yet

- Bagatsing Vs San Juan (Simbillo)Document3 pagesBagatsing Vs San Juan (Simbillo)Joshua Rizlan SimbilloNo ratings yet

- CIR vs. Burroghs, G.R. No. 66653, June 19, 1986Document1 pageCIR vs. Burroghs, G.R. No. 66653, June 19, 1986Oro ChamberNo ratings yet

- Cir Vs Bank of Commerce DigestDocument1 pageCir Vs Bank of Commerce DigestMimmi ShaneNo ratings yet

- CIR V StanleyDocument15 pagesCIR V StanleyPatatas SayoteNo ratings yet

- 13 Vegetable Oil Corp V TrinidadDocument2 pages13 Vegetable Oil Corp V TrinidadRocky GuzmanNo ratings yet

- Tax VAT CIR Vs GotamcoDocument3 pagesTax VAT CIR Vs GotamcoRhea Mae A. SibalaNo ratings yet

- Gutierrez V CollectorDocument3 pagesGutierrez V Collectormichee coi100% (1)

- Reinald Raven L. Guerrero Taxation Law 1 Surigao Consolidated Mining Co. vs. Collector of Internal Revenue FactsDocument1 pageReinald Raven L. Guerrero Taxation Law 1 Surigao Consolidated Mining Co. vs. Collector of Internal Revenue FactsSapere AudeNo ratings yet

- Pepsi Cola vs. City of ButuanDocument1 pagePepsi Cola vs. City of ButuanArdy Falejo FajutagNo ratings yet

- Case Digest On Taxation 1Document32 pagesCase Digest On Taxation 1Carl Vincent QuitorianoNo ratings yet

- Cir Vs Mega GeneralDocument2 pagesCir Vs Mega GeneralAiken Alagban LadinesNo ratings yet

- Batch 2 - Digested Cases in TaxationDocument20 pagesBatch 2 - Digested Cases in Taxationnikkolad100% (2)

- 136 CIR vs. Vda de PrietoDocument2 pages136 CIR vs. Vda de PrietoMiw Cortes100% (1)

- CIR v. Smith Kline / G.R. No. L-54108 / January 17, 1984Document1 pageCIR v. Smith Kline / G.R. No. L-54108 / January 17, 1984Mini U. SorianoNo ratings yet

- CIR v. Acesite Hotel CorporationDocument2 pagesCIR v. Acesite Hotel CorporationJemima FalinchaoNo ratings yet

- Hilado vs. CIRDocument1 pageHilado vs. CIRAlan GultiaNo ratings yet

- 17 Republic Vs de La RamaDocument3 pages17 Republic Vs de La RamaLara YuloNo ratings yet

- 29 CIR v. CADocument2 pages29 CIR v. CARem SerranoNo ratings yet

- Case Digest - Doctrines in TaxationDocument3 pagesCase Digest - Doctrines in TaxationBryne Angelo BrillantesNo ratings yet

- James V USDocument4 pagesJames V USKTNo ratings yet

- (TAX) Matalin Coconut vs. Municipal Council of MalabangDocument1 page(TAX) Matalin Coconut vs. Municipal Council of Malabangthornapple25100% (1)

- Bagatsing v. San Juan DigestDocument1 pageBagatsing v. San Juan DigestBruno GalwatNo ratings yet

- CIR Vs CA & CastanedaDocument1 pageCIR Vs CA & CastanedaArmstrong BosantogNo ratings yet

- Collector v. LaraDocument2 pagesCollector v. LaraJaypoll DiazNo ratings yet

- Melecio Domingo vs. Lorenzo Garlitos, G.R. No. L-18994, June 29, 1963Document2 pagesMelecio Domingo vs. Lorenzo Garlitos, G.R. No. L-18994, June 29, 1963Bal Nikko Joville - RocamoraNo ratings yet

- Punsalan Vs Municipal Board of ManilaDocument3 pagesPunsalan Vs Municipal Board of ManilaGayFleur Cabatit RamosNo ratings yet

- Ramoso Vs CADocument2 pagesRamoso Vs CARegine Joy MagaboNo ratings yet

- Consolidated Mines, Inc Vs Cta and CirDocument3 pagesConsolidated Mines, Inc Vs Cta and CirKirs Tie100% (3)

- Republic vs. Salud v. HizonDocument2 pagesRepublic vs. Salud v. HizonGyelamagne EstradaNo ratings yet

- Churchill V ConcepcionDocument2 pagesChurchill V ConcepcionKent A. AlonzoNo ratings yet

- Cir v. John Gotamco - SonsDocument2 pagesCir v. John Gotamco - SonsLEIGH TARITZ GANANCIALNo ratings yet

- Taxation 1 Case Analysis 3Document5 pagesTaxation 1 Case Analysis 3PJ OrtizNo ratings yet

- CIR vs. Metro StarDocument1 pageCIR vs. Metro StarRodney SantiagoNo ratings yet

- CIR Vs MarubeniDocument2 pagesCIR Vs MarubeniJocelyn MagbanuaNo ratings yet

- Panasonic Communications Imaging Corporation of The Philippines vs. Commissioner of Internal Revenue, 612 SCRA 18, February 08, 2010Document2 pagesPanasonic Communications Imaging Corporation of The Philippines vs. Commissioner of Internal Revenue, 612 SCRA 18, February 08, 2010idolbondoc100% (1)

- City of Baguio v. Fortunato de Leon GR L-24756Document1 pageCity of Baguio v. Fortunato de Leon GR L-24756Charles Roger RayaNo ratings yet

- Phil. Acetylene Co. Inc. VS Cir, GR No L-19707, Aug 17, 1967Document11 pagesPhil. Acetylene Co. Inc. VS Cir, GR No L-19707, Aug 17, 1967KidMonkey2299No ratings yet

- Kuenzle v. CIRDocument2 pagesKuenzle v. CIRTippy Dos Santos100% (2)

- Gutierrez Vs CollectorDocument2 pagesGutierrez Vs CollectorBenedict AlvarezNo ratings yet

- Us VS LudeyDocument2 pagesUs VS LudeyA Paula Cruz FranciscoNo ratings yet

- Case No. 3 Tax Case DigestDocument3 pagesCase No. 3 Tax Case Digestkc lovessNo ratings yet

- Pepsi v. TanauanDocument2 pagesPepsi v. TanauanKhian JamerNo ratings yet

- COMPAÑIA GENERAL DE TABACOS DE FILIPINAS Vs ManilaDocument2 pagesCOMPAÑIA GENERAL DE TABACOS DE FILIPINAS Vs ManilaLau NunezNo ratings yet

- Tax Ii CasesDocument4 pagesTax Ii CasesBae Irene100% (2)

- Request of Atty. ZialcitaDocument2 pagesRequest of Atty. ZialcitaAngelo Castillo100% (1)

- 10 - CIR V Mega General Merchandising Corp and CTADocument2 pages10 - CIR V Mega General Merchandising Corp and CTAkenken320No ratings yet

- CIR vs. Placer DomeDocument4 pagesCIR vs. Placer DomeAngelo Castillo100% (1)

- Nazareno - LVM CONSTRUCTION CORPORATIONDocument3 pagesNazareno - LVM CONSTRUCTION CORPORATIONNoel Christopher G. BellezaNo ratings yet

- TAX DigestDocument18 pagesTAX DigestBerna BadongenNo ratings yet

- 2 Tax Case DigestDocument11 pages2 Tax Case DigestLean Manuel Paragas0% (1)

- American Express International v. CIR CTA Case No. 6099 (April 19, 2002)Document2 pagesAmerican Express International v. CIR CTA Case No. 6099 (April 19, 2002)Francis Xavier Sinon100% (1)

- Week 5Document15 pagesWeek 5Richelle GraceNo ratings yet

- Digest TaxDocument10 pagesDigest TaxDominic EmbodoNo ratings yet

- Income TaxDocument24 pagesIncome TaxJozele DalupangNo ratings yet

- Invencion Case To Webb CaseDocument44 pagesInvencion Case To Webb CaseEmmanuel OrtegaNo ratings yet

- Philippine Constitution Article XIII, Section 4 Article III Section 9Document28 pagesPhilippine Constitution Article XIII, Section 4 Article III Section 9Emmanuel OrtegaNo ratings yet

- Agrarian Law Midterm ReviewerDocument41 pagesAgrarian Law Midterm ReviewerEmmanuel Ortega100% (3)

- Dissenting Opinion of Justice Puno DigestDocument6 pagesDissenting Opinion of Justice Puno DigestEmmanuel OrtegaNo ratings yet

- Media DigestsDocument4 pagesMedia DigestsEmmanuel OrtegaNo ratings yet

- GMA V PabrigaDocument3 pagesGMA V PabrigaEmmanuel Ortega100% (1)

- Agrarian Week2Document23 pagesAgrarian Week2Emmanuel OrtegaNo ratings yet

- Mactan Electic DigestDocument21 pagesMactan Electic DigestEmmanuel OrtegaNo ratings yet

- Salinas V NLRCDocument2 pagesSalinas V NLRCEmmanuel OrtegaNo ratings yet

- Conference of Maritime Agencies V POEADocument1 pageConference of Maritime Agencies V POEAEmmanuel Ortega100% (2)

- RUPA Vs CADocument4 pagesRUPA Vs CAEmmanuel OrtegaNo ratings yet

- Francisco V NLRCDocument3 pagesFrancisco V NLRCEmmanuel OrtegaNo ratings yet

- DGT - Duncan Vs Glaxo WellcomeDocument3 pagesDGT - Duncan Vs Glaxo WellcomeEmmanuel OrtegaNo ratings yet

- PAL V NLRCDocument2 pagesPAL V NLRCEmmanuel Ortega100% (2)

- Manuel V NC ConstructionDocument2 pagesManuel V NC ConstructionEmmanuel OrtegaNo ratings yet

- DGT - Yrasuegui Vs NLRCDocument6 pagesDGT - Yrasuegui Vs NLRCEmmanuel OrtegaNo ratings yet

- Serrano Vs Gallant Maritime Services DigestDocument6 pagesSerrano Vs Gallant Maritime Services DigestEmmanuel OrtegaNo ratings yet

- Avon Cosmetics V LunaDocument2 pagesAvon Cosmetics V LunaEmmanuel OrtegaNo ratings yet

- Arco Metal Products Co V SAMARM-NAFLUDocument1 pageArco Metal Products Co V SAMARM-NAFLUEmmanuel OrtegaNo ratings yet

- Calalang Vs Williams DigestDocument3 pagesCalalang Vs Williams DigestEmmanuel OrtegaNo ratings yet

- Air Marine v. Balatbat DigestDocument2 pagesAir Marine v. Balatbat DigestEmmanuel OrtegaNo ratings yet

- LABOR - Norkis Trading Vs GniloDocument4 pagesLABOR - Norkis Trading Vs GniloEmmanuel Ortega100% (1)

- Central Bank Employees Vs BSP DigestDocument6 pagesCentral Bank Employees Vs BSP DigestEmmanuel Ortega100% (2)

- Traveno Vs Bobongan DigestDocument1 pageTraveno Vs Bobongan DigestEmmanuel Ortega100% (2)

- Conference of Maritime Agencies, Inc. vs. POEA-DIGESTDocument1 pageConference of Maritime Agencies, Inc. vs. POEA-DIGESTinvictusincNo ratings yet

- PLDT Vs Abucay DigestDocument2 pagesPLDT Vs Abucay DigestEmmanuel Ortega100% (1)

- Case Study On Vnacs: PrashantDocument5 pagesCase Study On Vnacs: PrashantPrashant BagdiaNo ratings yet

- B Stock PricesDocument7 pagesB Stock PricesJenny PabualanNo ratings yet

- GF Difference Between Private and Public Company Structure Under The Corporations ActDocument3 pagesGF Difference Between Private and Public Company Structure Under The Corporations ActUbai M-pireNo ratings yet

- Dividend PolicyDocument8 pagesDividend PolicySumit PandeyNo ratings yet

- Time Period Hayden (Net) S&P 500 MSCI World (ACWI)Document13 pagesTime Period Hayden (Net) S&P 500 MSCI World (ACWI)Andy HuffNo ratings yet

- Definition of CommitmentDocument2 pagesDefinition of CommitmentcrissiekamNo ratings yet

- Principles of Shariah Governing Islamic Investment FundsDocument8 pagesPrinciples of Shariah Governing Islamic Investment Fundsrizwansurti1No ratings yet

- Chapter Four: Incentive PayDocument14 pagesChapter Four: Incentive PayAyesha AfrinNo ratings yet

- 12 Dunayer Distressed M&a Techniques MA05Document6 pages12 Dunayer Distressed M&a Techniques MA05sawilson1No ratings yet

- R&P RULES - GENERAL PRINCIPLES (Revised 08 - 2010Document106 pagesR&P RULES - GENERAL PRINCIPLES (Revised 08 - 2010kunalNo ratings yet

- Paycheck Protection Program Increase Act of 2020 Section-By-Section - FINALDocument2 pagesPaycheck Protection Program Increase Act of 2020 Section-By-Section - FINALFox News50% (4)

- 190 Capitol Subd. v. Negros Occ.Document1 page190 Capitol Subd. v. Negros Occ.Rem SerranoNo ratings yet

- Mindanao Savings and Loan Asso., vs. Edward Willkom (GOJAR)Document2 pagesMindanao Savings and Loan Asso., vs. Edward Willkom (GOJAR)Krizzia GojarNo ratings yet

- Financial Statements and Ratio Analysis: ChapterDocument25 pagesFinancial Statements and Ratio Analysis: Chapterkarim67% (3)

- PHD Research Bureau PHD Chamber of Commerce and IndustryDocument33 pagesPHD Research Bureau PHD Chamber of Commerce and IndustrySUNIL PUJARINo ratings yet

- MEDINA - Homework 1 (Midterm) No. 8Document3 pagesMEDINA - Homework 1 (Midterm) No. 8Von Andrei MedinaNo ratings yet

- Income Tax, Defined:: "The Hardest Thing in The World To Understand Is The Income Tax."Document12 pagesIncome Tax, Defined:: "The Hardest Thing in The World To Understand Is The Income Tax."Ron RamosNo ratings yet

- D.Y. Patil Institute of Master of Computer Applications and ManagementDocument3 pagesD.Y. Patil Institute of Master of Computer Applications and ManagementpltNo ratings yet

- Chap 004Document24 pagesChap 004Hiep LuuNo ratings yet

- HDFC Deposit FormDocument4 pagesHDFC Deposit FormnaguficoNo ratings yet

- ICICI Bank - Click To Pay PDFDocument1 pageICICI Bank - Click To Pay PDFSuzanne WilsonNo ratings yet

- Screenshot 2020-03-18 at 11.13.01 AM PDFDocument2 pagesScreenshot 2020-03-18 at 11.13.01 AM PDFKartik MathukiyaNo ratings yet

- Fredun PharmaDocument37 pagesFredun PharmaBandaru NarendrababuNo ratings yet

- AFAR-01 PartnershipDocument6 pagesAFAR-01 PartnershipRamainne Ronquillo0% (1)

- Working Capital Management SscEDocument38 pagesWorking Capital Management SscEKinNo ratings yet