LB PDF

LB PDF

You might also like

- Topic - Confession Before A Police Officer and Its Various Dimensions Indian Evidence Act - Research PaperDocument8 pagesTopic - Confession Before A Police Officer and Its Various Dimensions Indian Evidence Act - Research Paperabhi guptaNo ratings yet

- Collapse of Lehman BrothersDocument8 pagesCollapse of Lehman BrothersDerick John PalapagNo ratings yet

- Case Study - Fall of Lehman BrothersDocument29 pagesCase Study - Fall of Lehman Brotherskisan_compNo ratings yet

- Lehman Brother Case StudyDocument7 pagesLehman Brother Case Studylumiradut70100% (1)

- Stakeholders: 3. Academia - Edu 4. Reports of New York Times 5. Financial Accounting Theory 7e by William R. ScottDocument5 pagesStakeholders: 3. Academia - Edu 4. Reports of New York Times 5. Financial Accounting Theory 7e by William R. ScottAnindya BasuNo ratings yet

- Chapter 11Document10 pagesChapter 11HusainiBachtiarNo ratings yet

- PX Set H Solution PDFDocument14 pagesPX Set H Solution PDFChristine Altamarino89% (9)

- Parallel Currencies in Asset Accounting: 1. Define Currencies For Leading Ledger: (OB22)Document7 pagesParallel Currencies in Asset Accounting: 1. Define Currencies For Leading Ledger: (OB22)sapeinsNo ratings yet

- Igcse Accounting Essential 2e Answers 27 PDFDocument11 pagesIgcse Accounting Essential 2e Answers 27 PDFRitu Singla.No ratings yet

- Lehman BrothersDocument12 pagesLehman BrothersNurul Artikah SariNo ratings yet

- Lessons From Lehman BrothersDocument3 pagesLessons From Lehman BrothersJanjeremy2885100% (3)

- THE LEHMAN BROTHERS CASE A Corporate Governance Failure, Not A Failure of Financial Markets - Finance - BankingDocument4 pagesTHE LEHMAN BROTHERS CASE A Corporate Governance Failure, Not A Failure of Financial Markets - Finance - BankingKumar AnandNo ratings yet

- Lehman Brother Ethical DilemmaDocument3 pagesLehman Brother Ethical DilemmaVenkatesh KamathNo ratings yet

- Case Study On Lehman Brothers by Nadine SebaiDocument5 pagesCase Study On Lehman Brothers by Nadine Sebainadine448867% (3)

- Lehman BrothersDocument25 pagesLehman BrothersKiran J50% (2)

- Literature Review On Lehman BrothersDocument6 pagesLiterature Review On Lehman Brothersea3j015d100% (1)

- Case Application 1aDocument3 pagesCase Application 1akikiNo ratings yet

- Lehman Bro Corporate Governance FailureDocument18 pagesLehman Bro Corporate Governance FailureAzhar AkhtarNo ratings yet

- Assignment 1 Final Paper (Edited)Document8 pagesAssignment 1 Final Paper (Edited)paterneNo ratings yet

- JPMorgan London WhaleDocument10 pagesJPMorgan London Whalejanedpe25000No ratings yet

- Lehman AssignmentDocument6 pagesLehman AssignmentDuaa’s CreativityNo ratings yet

- Thesis Lehman BrothersDocument7 pagesThesis Lehman Brothersjbymdenbf100% (2)

- Casestudy - Lehman Brothers and The Subprime Crisis Week 2Document2 pagesCasestudy - Lehman Brothers and The Subprime Crisis Week 2Rachita ArikrishnanNo ratings yet

- Grupp 14 Niklas Fredriksson Robin Feng Lehman Brothers BankruptcyDocument11 pagesGrupp 14 Niklas Fredriksson Robin Feng Lehman Brothers BankruptcykarunjainNo ratings yet

- Introduction of Lehman BrothersDocument11 pagesIntroduction of Lehman BrothersAnindya BasuNo ratings yet

- TABLE OF CONTENTSLehmanDocument7 pagesTABLE OF CONTENTSLehmanAlaa AboaliNo ratings yet

- Case Study Analysis Financial LeverageDocument10 pagesCase Study Analysis Financial LeverageSarah Jane OrillosaNo ratings yet

- Leahman Brothers and Repo 150Document3 pagesLeahman Brothers and Repo 150aalfo123No ratings yet

- Lehman On The Brink of BankruptcyDocument19 pagesLehman On The Brink of Bankruptcyed_nycNo ratings yet

- Ex-Lehman CEO Richard Fuld's Testimony About Repo 105Document8 pagesEx-Lehman CEO Richard Fuld's Testimony About Repo 105DealBookNo ratings yet

- BolDocument1 pageBolAnindya BasuNo ratings yet

- How Lehman Brothers Used Repo 105 To Manipulate Their Financial SDocument14 pagesHow Lehman Brothers Used Repo 105 To Manipulate Their Financial Sarath reyesNo ratings yet

- Lehman Brothers - Analysis of FailureDocument25 pagesLehman Brothers - Analysis of FailureArif AhmedNo ratings yet

- 001 2014 3A V1 LehmanBrothers A REVADocument23 pages001 2014 3A V1 LehmanBrothers A REVAErica JoannaNo ratings yet

- Management - Lehman Brothers (Bakrie University)Document13 pagesManagement - Lehman Brothers (Bakrie University)kikiNo ratings yet

- Lehman BrothersDocument4 pagesLehman BrothersHenri De sloovereNo ratings yet

- Activities - Session 3Document2 pagesActivities - Session 3danssoNo ratings yet

- The Lehman Brothers Bankruptcy A - OverviewDocument25 pagesThe Lehman Brothers Bankruptcy A - OverviewDiniNo ratings yet

- Derivative & Risk MGTDocument4 pagesDerivative & Risk MGTKansaanah Tierong JaphethNo ratings yet

- Capital Can't Be MeasuredDocument5 pagesCapital Can't Be MeasureddocscriberNo ratings yet

- 12 Sym 13Document23 pages12 Sym 13Dania Sekar WuryandariNo ratings yet

- BMAN33000 Lehman Brothers Case PackDocument9 pagesBMAN33000 Lehman Brothers Case Packpouria11No ratings yet

- Business Social ResponsibilityDocument2 pagesBusiness Social ResponsibilityOlajideAbatanNo ratings yet

- L B: T B F ?: Ehman Rothers OO Ig To AILDocument12 pagesL B: T B F ?: Ehman Rothers OO Ig To AILShiven PriyadarshiNo ratings yet

- Lehman Brothers BankruptcyDocument8 pagesLehman Brothers BankruptcyOmar EshanNo ratings yet

- Pamantasan NG Cabuyao: Lehman Brothers: The CollapsedDocument12 pagesPamantasan NG Cabuyao: Lehman Brothers: The CollapsedJeth Vigilla NangcaNo ratings yet

- FM Momin AssignmentDocument6 pagesFM Momin AssignmentAfreen SarwarNo ratings yet

- Lehmanbrothers Casestudy2 120224103739 Phpapp01Document33 pagesLehmanbrothers Casestudy2 120224103739 Phpapp01Michael SextonNo ratings yet

- Professional Accountant PortfolioDocument14 pagesProfessional Accountant PortfolioLame JoelNo ratings yet

- 2008 Fin CrisisDocument10 pages2008 Fin CrisisAlok PalNo ratings yet

- Assignemnt 1 - Baring and Lehman Brother's BankDocument7 pagesAssignemnt 1 - Baring and Lehman Brother's BankBrow SimonNo ratings yet

- Trust Markets GovDocument10 pagesTrust Markets GovwhitestoneoeilNo ratings yet

- The Lehman Brothers A Story of Corporate Greed and CollapseDocument8 pagesThe Lehman Brothers A Story of Corporate Greed and CollapseAirooh SenNo ratings yet

- Analysis - ShubhamDocument26 pagesAnalysis - ShubhamShubham GoenkaNo ratings yet

- ACCG847 Case Study Report - Group 2Document15 pagesACCG847 Case Study Report - Group 2melissatabanagNo ratings yet

- Lehman Brothers Case StudyDocument7 pagesLehman Brothers Case Studyali goharNo ratings yet

- A Case Study Entitled: The Collapse of Lehman BrothersDocument10 pagesA Case Study Entitled: The Collapse of Lehman BrothersRoby IbeNo ratings yet

- Lehman BrothersDocument14 pagesLehman Brotherssumitkjham100% (1)

- Corporate Governance Failures: The Role of Institutional Investors in the Global Financial CrisisFrom EverandCorporate Governance Failures: The Role of Institutional Investors in the Global Financial CrisisRating: 1 out of 5 stars1/5 (1)

- FinTech Rising: Navigating the maze of US & EU regulationsFrom EverandFinTech Rising: Navigating the maze of US & EU regulationsRating: 5 out of 5 stars5/5 (1)

- Summary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionFrom EverandSummary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionNo ratings yet

- PEOPLE v. ELY POLICARPIO Y NATIVIDADDocument8 pagesPEOPLE v. ELY POLICARPIO Y NATIVIDADFaustina del RosarioNo ratings yet

- Madness in Buenos AiresDocument340 pagesMadness in Buenos AiresLaura VanadiaNo ratings yet

- 22 Riddles To Learn EnglishDocument25 pages22 Riddles To Learn EnglishXurxo LubimanNo ratings yet

- Axxess IPdevices Install ManualDocument230 pagesAxxess IPdevices Install ManualJorge CabreraNo ratings yet

- Sicangu Eyapaha - Volume 11, Issue 13Document16 pagesSicangu Eyapaha - Volume 11, Issue 13Ojinjintka NewsNo ratings yet

- Motor Accident ClaimsDocument8 pagesMotor Accident ClaimsHarshitha.S PhysicsNo ratings yet

- Legal System of Sri Lanka 2015Document22 pagesLegal System of Sri Lanka 2015Riyas100% (1)

- A Butterfly Smile: Author: Mathangi Subramanian Illustrator: Lavanya NaiduDocument22 pagesA Butterfly Smile: Author: Mathangi Subramanian Illustrator: Lavanya NaiduNeyda EspínNo ratings yet

- Print VP GoelDocument4 pagesPrint VP GoelGopsNo ratings yet

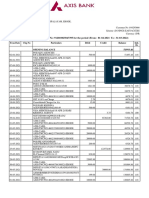

- Statement of Axis Account No:912010025047395 For The Period (From: 01-04-2021 To: 31-03-2022)Document5 pagesStatement of Axis Account No:912010025047395 For The Period (From: 01-04-2021 To: 31-03-2022)Naghul MxNo ratings yet

- Genil vs. RiveraDocument2 pagesGenil vs. RiveraElaine HonradeNo ratings yet

- Chapter 15 Corporation-Share CapitalDocument58 pagesChapter 15 Corporation-Share CapitalLe Ann Rhine MayantongNo ratings yet

- Unibis Leaflet EnglishDocument6 pagesUnibis Leaflet EnglishShna KawaNo ratings yet

- School Planning Team Composition: Chairman: Co-Chairman: MembersDocument6 pagesSchool Planning Team Composition: Chairman: Co-Chairman: MembersCarmina Nadora DuldulaoNo ratings yet

- Veritas Backup Exec Migration AssistantDocument21 pagesVeritas Backup Exec Migration AssistantArunMuraliNo ratings yet

- Name Vocabulary: Unit 4 - Grammar and VocabularyDocument4 pagesName Vocabulary: Unit 4 - Grammar and VocabularyCarolina Cachaldora RodriguezNo ratings yet

- Assignment Eco S 1005 - Bouchra MrabetiDocument6 pagesAssignment Eco S 1005 - Bouchra MrabetiBouchra MrabetiNo ratings yet

- VISTA LAND AND LIFESCAPES INC FinalDocument9 pagesVISTA LAND AND LIFESCAPES INC Finalmarie crisNo ratings yet

- Bedand Breakfast SchemeDocument14 pagesBedand Breakfast SchemeJasmeet DhamijaNo ratings yet

- Divine Alloys & Power Co.-R-23042012Document3 pagesDivine Alloys & Power Co.-R-23042012Dhirendra SinghNo ratings yet

- Robert Down The Right PathDocument18 pagesRobert Down The Right PathNicole JusticeNo ratings yet

- Cakravartinship of Buddha MaitreyaDocument12 pagesCakravartinship of Buddha MaitreyaudayNo ratings yet

- Kennedy 1987Document30 pagesKennedy 1987Merlot Papin100% (1)

- Double Lives - Stephen Koch (Resenha)Document6 pagesDouble Lives - Stephen Koch (Resenha)Paulo Bento0% (1)

- TTTNitzavim 71Document3 pagesTTTNitzavim 71Mark GreenspanNo ratings yet

- Acclaimed and Outspoken Writers of TurkeyDocument4 pagesAcclaimed and Outspoken Writers of TurkeyRabeea AsifNo ratings yet

Download as pdf or txt

You might also like

- Topic - Confession Before A Police Officer and Its Various Dimensions Indian Evidence Act - Research PaperDocument8 pagesTopic - Confession Before A Police Officer and Its Various Dimensions Indian Evidence Act - Research Paperabhi guptaNo ratings yet

- Collapse of Lehman BrothersDocument8 pagesCollapse of Lehman BrothersDerick John PalapagNo ratings yet

- Case Study - Fall of Lehman BrothersDocument29 pagesCase Study - Fall of Lehman Brotherskisan_compNo ratings yet

- Lehman Brother Case StudyDocument7 pagesLehman Brother Case Studylumiradut70100% (1)

- Stakeholders: 3. Academia - Edu 4. Reports of New York Times 5. Financial Accounting Theory 7e by William R. ScottDocument5 pagesStakeholders: 3. Academia - Edu 4. Reports of New York Times 5. Financial Accounting Theory 7e by William R. ScottAnindya BasuNo ratings yet

- Chapter 11Document10 pagesChapter 11HusainiBachtiarNo ratings yet

- PX Set H Solution PDFDocument14 pagesPX Set H Solution PDFChristine Altamarino89% (9)

- Parallel Currencies in Asset Accounting: 1. Define Currencies For Leading Ledger: (OB22)Document7 pagesParallel Currencies in Asset Accounting: 1. Define Currencies For Leading Ledger: (OB22)sapeinsNo ratings yet

- Igcse Accounting Essential 2e Answers 27 PDFDocument11 pagesIgcse Accounting Essential 2e Answers 27 PDFRitu Singla.No ratings yet

- Lehman BrothersDocument12 pagesLehman BrothersNurul Artikah SariNo ratings yet

- Lessons From Lehman BrothersDocument3 pagesLessons From Lehman BrothersJanjeremy2885100% (3)

- THE LEHMAN BROTHERS CASE A Corporate Governance Failure, Not A Failure of Financial Markets - Finance - BankingDocument4 pagesTHE LEHMAN BROTHERS CASE A Corporate Governance Failure, Not A Failure of Financial Markets - Finance - BankingKumar AnandNo ratings yet

- Lehman Brother Ethical DilemmaDocument3 pagesLehman Brother Ethical DilemmaVenkatesh KamathNo ratings yet

- Case Study On Lehman Brothers by Nadine SebaiDocument5 pagesCase Study On Lehman Brothers by Nadine Sebainadine448867% (3)

- Lehman BrothersDocument25 pagesLehman BrothersKiran J50% (2)

- Literature Review On Lehman BrothersDocument6 pagesLiterature Review On Lehman Brothersea3j015d100% (1)

- Case Application 1aDocument3 pagesCase Application 1akikiNo ratings yet

- Lehman Bro Corporate Governance FailureDocument18 pagesLehman Bro Corporate Governance FailureAzhar AkhtarNo ratings yet

- Assignment 1 Final Paper (Edited)Document8 pagesAssignment 1 Final Paper (Edited)paterneNo ratings yet

- JPMorgan London WhaleDocument10 pagesJPMorgan London Whalejanedpe25000No ratings yet

- Lehman AssignmentDocument6 pagesLehman AssignmentDuaa’s CreativityNo ratings yet

- Thesis Lehman BrothersDocument7 pagesThesis Lehman Brothersjbymdenbf100% (2)

- Casestudy - Lehman Brothers and The Subprime Crisis Week 2Document2 pagesCasestudy - Lehman Brothers and The Subprime Crisis Week 2Rachita ArikrishnanNo ratings yet

- Grupp 14 Niklas Fredriksson Robin Feng Lehman Brothers BankruptcyDocument11 pagesGrupp 14 Niklas Fredriksson Robin Feng Lehman Brothers BankruptcykarunjainNo ratings yet

- Introduction of Lehman BrothersDocument11 pagesIntroduction of Lehman BrothersAnindya BasuNo ratings yet

- TABLE OF CONTENTSLehmanDocument7 pagesTABLE OF CONTENTSLehmanAlaa AboaliNo ratings yet

- Case Study Analysis Financial LeverageDocument10 pagesCase Study Analysis Financial LeverageSarah Jane OrillosaNo ratings yet

- Leahman Brothers and Repo 150Document3 pagesLeahman Brothers and Repo 150aalfo123No ratings yet

- Lehman On The Brink of BankruptcyDocument19 pagesLehman On The Brink of Bankruptcyed_nycNo ratings yet

- Ex-Lehman CEO Richard Fuld's Testimony About Repo 105Document8 pagesEx-Lehman CEO Richard Fuld's Testimony About Repo 105DealBookNo ratings yet

- BolDocument1 pageBolAnindya BasuNo ratings yet

- How Lehman Brothers Used Repo 105 To Manipulate Their Financial SDocument14 pagesHow Lehman Brothers Used Repo 105 To Manipulate Their Financial Sarath reyesNo ratings yet

- Lehman Brothers - Analysis of FailureDocument25 pagesLehman Brothers - Analysis of FailureArif AhmedNo ratings yet

- 001 2014 3A V1 LehmanBrothers A REVADocument23 pages001 2014 3A V1 LehmanBrothers A REVAErica JoannaNo ratings yet

- Management - Lehman Brothers (Bakrie University)Document13 pagesManagement - Lehman Brothers (Bakrie University)kikiNo ratings yet

- Lehman BrothersDocument4 pagesLehman BrothersHenri De sloovereNo ratings yet

- Activities - Session 3Document2 pagesActivities - Session 3danssoNo ratings yet

- The Lehman Brothers Bankruptcy A - OverviewDocument25 pagesThe Lehman Brothers Bankruptcy A - OverviewDiniNo ratings yet

- Derivative & Risk MGTDocument4 pagesDerivative & Risk MGTKansaanah Tierong JaphethNo ratings yet

- Capital Can't Be MeasuredDocument5 pagesCapital Can't Be MeasureddocscriberNo ratings yet

- 12 Sym 13Document23 pages12 Sym 13Dania Sekar WuryandariNo ratings yet

- BMAN33000 Lehman Brothers Case PackDocument9 pagesBMAN33000 Lehman Brothers Case Packpouria11No ratings yet

- Business Social ResponsibilityDocument2 pagesBusiness Social ResponsibilityOlajideAbatanNo ratings yet

- L B: T B F ?: Ehman Rothers OO Ig To AILDocument12 pagesL B: T B F ?: Ehman Rothers OO Ig To AILShiven PriyadarshiNo ratings yet

- Lehman Brothers BankruptcyDocument8 pagesLehman Brothers BankruptcyOmar EshanNo ratings yet

- Pamantasan NG Cabuyao: Lehman Brothers: The CollapsedDocument12 pagesPamantasan NG Cabuyao: Lehman Brothers: The CollapsedJeth Vigilla NangcaNo ratings yet

- FM Momin AssignmentDocument6 pagesFM Momin AssignmentAfreen SarwarNo ratings yet

- Lehmanbrothers Casestudy2 120224103739 Phpapp01Document33 pagesLehmanbrothers Casestudy2 120224103739 Phpapp01Michael SextonNo ratings yet

- Professional Accountant PortfolioDocument14 pagesProfessional Accountant PortfolioLame JoelNo ratings yet

- 2008 Fin CrisisDocument10 pages2008 Fin CrisisAlok PalNo ratings yet

- Assignemnt 1 - Baring and Lehman Brother's BankDocument7 pagesAssignemnt 1 - Baring and Lehman Brother's BankBrow SimonNo ratings yet

- Trust Markets GovDocument10 pagesTrust Markets GovwhitestoneoeilNo ratings yet

- The Lehman Brothers A Story of Corporate Greed and CollapseDocument8 pagesThe Lehman Brothers A Story of Corporate Greed and CollapseAirooh SenNo ratings yet

- Analysis - ShubhamDocument26 pagesAnalysis - ShubhamShubham GoenkaNo ratings yet

- ACCG847 Case Study Report - Group 2Document15 pagesACCG847 Case Study Report - Group 2melissatabanagNo ratings yet

- Lehman Brothers Case StudyDocument7 pagesLehman Brothers Case Studyali goharNo ratings yet

- A Case Study Entitled: The Collapse of Lehman BrothersDocument10 pagesA Case Study Entitled: The Collapse of Lehman BrothersRoby IbeNo ratings yet

- Lehman BrothersDocument14 pagesLehman Brotherssumitkjham100% (1)

- Corporate Governance Failures: The Role of Institutional Investors in the Global Financial CrisisFrom EverandCorporate Governance Failures: The Role of Institutional Investors in the Global Financial CrisisRating: 1 out of 5 stars1/5 (1)

- FinTech Rising: Navigating the maze of US & EU regulationsFrom EverandFinTech Rising: Navigating the maze of US & EU regulationsRating: 5 out of 5 stars5/5 (1)

- Summary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionFrom EverandSummary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionNo ratings yet

- PEOPLE v. ELY POLICARPIO Y NATIVIDADDocument8 pagesPEOPLE v. ELY POLICARPIO Y NATIVIDADFaustina del RosarioNo ratings yet

- Madness in Buenos AiresDocument340 pagesMadness in Buenos AiresLaura VanadiaNo ratings yet

- 22 Riddles To Learn EnglishDocument25 pages22 Riddles To Learn EnglishXurxo LubimanNo ratings yet

- Axxess IPdevices Install ManualDocument230 pagesAxxess IPdevices Install ManualJorge CabreraNo ratings yet

- Sicangu Eyapaha - Volume 11, Issue 13Document16 pagesSicangu Eyapaha - Volume 11, Issue 13Ojinjintka NewsNo ratings yet

- Motor Accident ClaimsDocument8 pagesMotor Accident ClaimsHarshitha.S PhysicsNo ratings yet

- Legal System of Sri Lanka 2015Document22 pagesLegal System of Sri Lanka 2015Riyas100% (1)

- A Butterfly Smile: Author: Mathangi Subramanian Illustrator: Lavanya NaiduDocument22 pagesA Butterfly Smile: Author: Mathangi Subramanian Illustrator: Lavanya NaiduNeyda EspínNo ratings yet

- Print VP GoelDocument4 pagesPrint VP GoelGopsNo ratings yet

- Statement of Axis Account No:912010025047395 For The Period (From: 01-04-2021 To: 31-03-2022)Document5 pagesStatement of Axis Account No:912010025047395 For The Period (From: 01-04-2021 To: 31-03-2022)Naghul MxNo ratings yet

- Genil vs. RiveraDocument2 pagesGenil vs. RiveraElaine HonradeNo ratings yet

- Chapter 15 Corporation-Share CapitalDocument58 pagesChapter 15 Corporation-Share CapitalLe Ann Rhine MayantongNo ratings yet

- Unibis Leaflet EnglishDocument6 pagesUnibis Leaflet EnglishShna KawaNo ratings yet

- School Planning Team Composition: Chairman: Co-Chairman: MembersDocument6 pagesSchool Planning Team Composition: Chairman: Co-Chairman: MembersCarmina Nadora DuldulaoNo ratings yet

- Veritas Backup Exec Migration AssistantDocument21 pagesVeritas Backup Exec Migration AssistantArunMuraliNo ratings yet

- Name Vocabulary: Unit 4 - Grammar and VocabularyDocument4 pagesName Vocabulary: Unit 4 - Grammar and VocabularyCarolina Cachaldora RodriguezNo ratings yet

- Assignment Eco S 1005 - Bouchra MrabetiDocument6 pagesAssignment Eco S 1005 - Bouchra MrabetiBouchra MrabetiNo ratings yet

- VISTA LAND AND LIFESCAPES INC FinalDocument9 pagesVISTA LAND AND LIFESCAPES INC Finalmarie crisNo ratings yet

- Bedand Breakfast SchemeDocument14 pagesBedand Breakfast SchemeJasmeet DhamijaNo ratings yet

- Divine Alloys & Power Co.-R-23042012Document3 pagesDivine Alloys & Power Co.-R-23042012Dhirendra SinghNo ratings yet

- Robert Down The Right PathDocument18 pagesRobert Down The Right PathNicole JusticeNo ratings yet

- Cakravartinship of Buddha MaitreyaDocument12 pagesCakravartinship of Buddha MaitreyaudayNo ratings yet

- Kennedy 1987Document30 pagesKennedy 1987Merlot Papin100% (1)

- Double Lives - Stephen Koch (Resenha)Document6 pagesDouble Lives - Stephen Koch (Resenha)Paulo Bento0% (1)

- TTTNitzavim 71Document3 pagesTTTNitzavim 71Mark GreenspanNo ratings yet

- Acclaimed and Outspoken Writers of TurkeyDocument4 pagesAcclaimed and Outspoken Writers of TurkeyRabeea AsifNo ratings yet