Download as pdf or txt

You might also like

- Engineering EconomyDocument16 pagesEngineering EconomyHazel Marie Ignacio PeraltaNo ratings yet

- Temple CPU Appeal - Scanned Docs - USPS Disclosures No 1-6, Bates StampedDocument546 pagesTemple CPU Appeal - Scanned Docs - USPS Disclosures No 1-6, Bates StampedBrent MartinNo ratings yet

- Katy Freeway Corridor Flood Control StudyDocument31 pagesKaty Freeway Corridor Flood Control Studycityhallblog100% (8)

- Route 3 Reports - PC - MILER WebDocument3 pagesRoute 3 Reports - PC - MILER WebLemon GundersonNo ratings yet

- Route 1 Reports - PC - MILER Web Palwinder Jul-SepDocument3 pagesRoute 1 Reports - PC - MILER Web Palwinder Jul-SepLemon GundersonNo ratings yet

- 2009 NetTaxBefFrz CertifiedDocument2 pages2009 NetTaxBefFrz CertifiedwhundleyNo ratings yet

- Route 2 Reports - PC - MILER Web JasvinderDocument3 pagesRoute 2 Reports - PC - MILER Web JasvinderLemon GundersonNo ratings yet

- Route 3 Reports - PC - MILER WebDocument2 pagesRoute 3 Reports - PC - MILER WebLemon GundersonNo ratings yet

- Altos Research Real-Time Housing Report - November 2010Document6 pagesAltos Research Real-Time Housing Report - November 2010Altos ResearchNo ratings yet

- SM014 Elemental Costing DatabaseDocument41 pagesSM014 Elemental Costing DatabasewanfaroukNo ratings yet

- MultiFamily July2007Document1 pageMultiFamily July2007teamtingNo ratings yet

- 2011 Assessment For Commerical PropertiesDocument1 page2011 Assessment For Commerical PropertiesmdebonisNo ratings yet

- Comparison of Incomes and Rents, Rent-Stabilized vs. Market-Rate RentalsDocument3 pagesComparison of Incomes and Rents, Rent-Stabilized vs. Market-Rate RentalsBrad LanderNo ratings yet

- Prin Borough SalesDocument2 pagesPrin Borough SalesPlanet PrincetonNo ratings yet

- 2011 Assessment For Residential PropertiesDocument1 page2011 Assessment For Residential PropertiesmdebonisNo ratings yet

- Vancouver Real Estate Stats Package - August2010Document7 pagesVancouver Real Estate Stats Package - August2010BenAmzalegNo ratings yet

- 2012 Assessments ResidentialDocument2 pages2012 Assessments ResidentialmdebonisNo ratings yet

- DCMetroStats 1Q2011Document1 pageDCMetroStats 1Q2011Anonymous Feglbx5No ratings yet

- Staff Report Information Only: Date: To: From: Wards: Reference NumberDocument14 pagesStaff Report Information Only: Date: To: From: Wards: Reference NumberAdam BuchananNo ratings yet

- 11-Oct 10-Sep 9-Aug 8-Jul 7-Jun 6-May 10-Sep 10-May Median % Change Bergen CountyDocument4 pages11-Oct 10-Sep 9-Aug 8-Jul 7-Jun 6-May 10-Sep 10-May Median % Change Bergen CountytakebackbergenfieldNo ratings yet

- Courtesy of Jim Duncan - Nest Realty Group, Charlottesville, Virginia 434-242-7140Document6 pagesCourtesy of Jim Duncan - Nest Realty Group, Charlottesville, Virginia 434-242-7140api-25884944No ratings yet

- REBGV Stats Package October 2010Document7 pagesREBGV Stats Package October 2010Mike StewartNo ratings yet

- REBGV Stats Package October 2009Document7 pagesREBGV Stats Package October 2009eyalpevznerNo ratings yet

- NC Update 7-29Document18 pagesNC Update 7-29LandGuyNo ratings yet

- 2008 Domestic Water SurveyDocument1 page2008 Domestic Water SurveyCaroline Nordahl BrosioNo ratings yet

- Roads Elemental CostingDocument47 pagesRoads Elemental Costingsarathirv6100% (2)

- Greater Vancouver Dec 2010Document7 pagesGreater Vancouver Dec 2010urbaniak_bcNo ratings yet

- 01560-Designated Statestable7-7-06-JT 4Document5 pages01560-Designated Statestable7-7-06-JT 4losangelesNo ratings yet

- Oct 21 StatsDocument1 pageOct 21 StatsMatt PollockNo ratings yet

- Pleasanton Real Estate - Ruby Hill, Pleasanton Market Report, AprilDocument4 pagesPleasanton Real Estate - Ruby Hill, Pleasanton Market Report, AprillauramonroevaNo ratings yet

- Batman V SupermanDocument2 pagesBatman V SupermanGaby CamposNo ratings yet

- Operations Management-II Case - Megacard CorporationDocument7 pagesOperations Management-II Case - Megacard CorporationDikshma PaulNo ratings yet

- Ham North Key Suburbs Recent Sold Report August 2021 Ver.Document99 pagesHam North Key Suburbs Recent Sold Report August 2021 Ver.Jack TanNo ratings yet

- K 12 EducationDocument15 pagesK 12 EducationWTOL DIGITAL100% (1)

- Market Report-Week Ending August 7, 2010 New ListingsDocument4 pagesMarket Report-Week Ending August 7, 2010 New ListingsMelissa ConklingNo ratings yet

- Capital RiesgoDocument11 pagesCapital Riesgodarlang_zambrano5702No ratings yet

- Adding Charts To Your Dashboard AfterDocument231 pagesAdding Charts To Your Dashboard Afterhassan1989No ratings yet

- Calculo de Indirectos PS y FSR Enero 2019 UATDocument5 pagesCalculo de Indirectos PS y FSR Enero 2019 UATOdalis SernaNo ratings yet

- REBGV Stats Package March 2010Document6 pagesREBGV Stats Package March 2010BenAmzalegNo ratings yet

- News Release: Home Sales Activity Strong Through Olympic PeriodDocument7 pagesNews Release: Home Sales Activity Strong Through Olympic PeriodBenAmzalegNo ratings yet

- Weekly Market Report - Week Ending 8-14-2010Document4 pagesWeekly Market Report - Week Ending 8-14-2010Melissa ConklingNo ratings yet

- Every Stock Pick Shown Here - None Hidden: 2004 Through 2016 Average Gain For All PicksDocument14 pagesEvery Stock Pick Shown Here - None Hidden: 2004 Through 2016 Average Gain For All PicksYagnesh Patel100% (1)

- Cambrain 090109Document2 pagesCambrain 090109Annie LangNo ratings yet

- 2010 Department of State Foreign Service Salary TablesDocument40 pages2010 Department of State Foreign Service Salary TablesResumeBearNo ratings yet

- Rockcats Consultant ReportDocument33 pagesRockcats Consultant ReportkevinhfdNo ratings yet

- Source: Newspaper Association of America (Estimates) (Estimates) (Estimates)Document6 pagesSource: Newspaper Association of America (Estimates) (Estimates) (Estimates)eugene.s.lin298No ratings yet

- TM Budget Presentation 2015Document34 pagesTM Budget Presentation 2015jxmackNo ratings yet

- Route 6 Reports - PC - MILER WebDocument1 pageRoute 6 Reports - PC - MILER WebLemon GundersonNo ratings yet

- Ford Fact Sheet - Economic FootprintDocument6 pagesFord Fact Sheet - Economic FootprintFord Motor Company100% (30)

- Net ProviderDocument2 pagesNet ProvideribtiNo ratings yet

- Cache Valley Plaza AnalysisDocument10 pagesCache Valley Plaza AnalysisvobhoNo ratings yet

- Cache Valley Plaza AnalysisDocument10 pagesCache Valley Plaza AnalysisvobhoNo ratings yet

- W05-V04 - Print TitleDocument7 pagesW05-V04 - Print TitleHaider AliNo ratings yet

- Shannon Grants 2019Document1 pageShannon Grants 2019Patrick JohnsonNo ratings yet

- Attach - 2024 Year Over Year Breakdowns and GraphsDocument15 pagesAttach - 2024 Year Over Year Breakdowns and GraphsTom SummerNo ratings yet

- Top 100 CPA Firms - With RankingDocument4 pagesTop 100 CPA Firms - With RankingSajal MittalNo ratings yet

- 28 Jan 81.95Document1 page28 Jan 81.95SushilNo ratings yet

- Kanban Change Leadership: Creating a Culture of Continuous ImprovementFrom EverandKanban Change Leadership: Creating a Culture of Continuous ImprovementNo ratings yet

- Space Electronic Reconnaissance: Localization Theories and MethodsFrom EverandSpace Electronic Reconnaissance: Localization Theories and MethodsNo ratings yet

- Kkraish Khraish West Dallas PlanDocument6 pagesKkraish Khraish West Dallas PlancityhallblogNo ratings yet

- Topletz LTTR PDFDocument1 pageTopletz LTTR PDFJim SchutzeNo ratings yet

- Toll Road Supporters and OpponentsDocument5 pagesToll Road Supporters and OpponentssdallasesqNo ratings yet

- Letter From Delta To Dallas City HallDocument9 pagesLetter From Delta To Dallas City HallRobert WilonskyNo ratings yet

- Unofficial Copy - Travis Co. District Clerk Velva L. PriceDocument18 pagesUnofficial Copy - Travis Co. District Clerk Velva L. PricecityhallblogNo ratings yet

- Trinity Lakes BriefingDocument99 pagesTrinity Lakes BriefingcityhallblogNo ratings yet

- Wallace Flyer Re MilesDocument1 pageWallace Flyer Re MilescityhallblogNo ratings yet

- Amended Judgment - Carlos MedranoDocument5 pagesAmended Judgment - Carlos MedranocityhallblogNo ratings yet

- Council Memo - 14.08.25 - CM Griggs' $3.84m Budget AmendmentDocument5 pagesCouncil Memo - 14.08.25 - CM Griggs' $3.84m Budget AmendmentcityhallblogNo ratings yet

- 2013 DPFP Performance MemoDocument2 pages2013 DPFP Performance MemocityhallblogNo ratings yet

- Scott Griggs Memo To Mayor Rawlings and City CouncilDocument2 pagesScott Griggs Memo To Mayor Rawlings and City Councilwfaachannel8No ratings yet

- Jim's Car Wash Police ReportsDocument35 pagesJim's Car Wash Police ReportscityhallblogNo ratings yet

- Trinity River Corridor Project Expenditure Report: 1998 Bond ProgramDocument2 pagesTrinity River Corridor Project Expenditure Report: 1998 Bond ProgramcityhallblogNo ratings yet

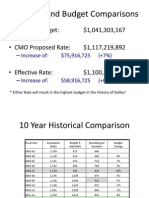

- Kleinman Effective Rate ProposalDocument5 pagesKleinman Effective Rate ProposalcityhallblogNo ratings yet

- City Design Studio Jefferson BLVD 2014-01-13Document14 pagesCity Design Studio Jefferson BLVD 2014-01-13rappletonNo ratings yet

- 2013-2015 Council CommitteesDocument3 pages2013-2015 Council CommitteescityhallblogNo ratings yet

- Introduction To Market FailureDocument3 pagesIntroduction To Market FailureJennifer Baquial Comia100% (1)

- ProfileDocument4 pagesProfileGreen Sustain EnergyNo ratings yet

- Welcome To ACT14: Conceptual Framework and Accounting Standards (CFAS)Document38 pagesWelcome To ACT14: Conceptual Framework and Accounting Standards (CFAS)Jashi SiñelNo ratings yet

- Carrefour InternetDocument25 pagesCarrefour InternetJuan PabloNo ratings yet

- P P P P P P MRS MRS: 2020-2021 Term 1 ECON2011A/B Problem Set 2Document3 pagesP P P P P P MRS MRS: 2020-2021 Term 1 ECON2011A/B Problem Set 2Helen ToNo ratings yet

- Advertising Techniques - 13 Most Common Techniques Used by The AdvertisersDocument3 pagesAdvertising Techniques - 13 Most Common Techniques Used by The AdvertisersjrenceNo ratings yet

- Requested Products - Van SchaikDocument3 pagesRequested Products - Van Schaik6lackzamokuhleNo ratings yet

- Business Plan TemplateDocument14 pagesBusiness Plan TemplateMei HuaNo ratings yet

- Diversification, Venturing and Corporate Restructuring For National and International BusinessDocument12 pagesDiversification, Venturing and Corporate Restructuring For National and International BusinessShubh GuptaNo ratings yet

- How To Generate Leads in InstagramDocument3 pagesHow To Generate Leads in InstagramWeiss SolutionsNo ratings yet

- CopaDocument6 pagesCopasivasivasapNo ratings yet

- 10B Olstein AnniversaryDocument21 pages10B Olstein AnniversaryMatt EbrahimiNo ratings yet

- Test1 ReviewDocument8 pagesTest1 Reviewghsoub777No ratings yet

- Ajanta Shoes Company LTDDocument3 pagesAjanta Shoes Company LTDGautam SoniNo ratings yet

- Student Answer:: - 703637150 Multiplechoice 15 True 0 - 703637150 Multiplechoice 15Document15 pagesStudent Answer:: - 703637150 Multiplechoice 15 True 0 - 703637150 Multiplechoice 15YukiNo ratings yet

- Introduction To : Amway & Its Supply ChainDocument16 pagesIntroduction To : Amway & Its Supply Chainn2oh1No ratings yet

- Hill PPT 12e ch03Document30 pagesHill PPT 12e ch03raywelNo ratings yet

- Chapter FiveDocument49 pagesChapter FiveLoai AbusaifNo ratings yet

- The Six Key Components of A Business Strategy IncludeDocument6 pagesThe Six Key Components of A Business Strategy IncludeFoysal Ahmed AfnanNo ratings yet

- Accounting Adjustments 1Document71 pagesAccounting Adjustments 1vukicevic.ivan5No ratings yet

- Implementing An Automated Inventory Management System For Small and Medium-Sized EnterprisesDocument7 pagesImplementing An Automated Inventory Management System For Small and Medium-Sized EnterprisesKoraima Gomez RojasNo ratings yet

- Britannia BourbonDocument12 pagesBritannia BourbonDebmalya De100% (1)

- Amul Brand AuditDocument25 pagesAmul Brand AuditRoopeshkumar YadavNo ratings yet

- FIN 425 Nur Nabi SirDocument7 pagesFIN 425 Nur Nabi SirSumaiya AfrinNo ratings yet

- Option Pricing in VBADocument5 pagesOption Pricing in VBArndompersonNo ratings yet

- Impact Analysis of Market Structure On Supply of Goods in The Market.Document21 pagesImpact Analysis of Market Structure On Supply of Goods in The Market.Vritika ChanjotraNo ratings yet

- Submitted By: Sumit Mudgil: Course: Digital Business Innovation Project: Hamleys'SDocument7 pagesSubmitted By: Sumit Mudgil: Course: Digital Business Innovation Project: Hamleys'SSumitNo ratings yet

- Quiz 1 Final ExamDocument6 pagesQuiz 1 Final ExamNica Jane MacapinigNo ratings yet

- SLWebb DissertationDocument167 pagesSLWebb DissertationAbhay ParasharNo ratings yet