Principal / Immediate Employer: Esic Revenue Manual

Principal / Immediate Employer: Esic Revenue Manual

You might also like

- Social Factors Affecting Educational PlanningDocument9 pagesSocial Factors Affecting Educational PlanningShaayongo Benjamin50% (2)

- Objective and Scope of Industrial EmployDocument9 pagesObjective and Scope of Industrial EmployLakshmi Narayan RNo ratings yet

- Amity University: Amity Law School, Lucknow CampusDocument9 pagesAmity University: Amity Law School, Lucknow CampusAK KhareNo ratings yet

- Contract Labour Act OverviewDocument21 pagesContract Labour Act OverviewDhriti SharmaNo ratings yet

- Labour Law 2 ProjectDocument12 pagesLabour Law 2 ProjectSrijeshNo ratings yet

- Standing OrderDocument11 pagesStanding OrderKeerthana RavichandranNo ratings yet

- FAQs - Rationalizing Labour During COVID-19Document22 pagesFAQs - Rationalizing Labour During COVID-19amirarsiwalaNo ratings yet

- Workman - Under Industrial Disputes Act, 1947 - Employee Rights - Labour Relations - IndiaDocument3 pagesWorkman - Under Industrial Disputes Act, 1947 - Employee Rights - Labour Relations - IndiaRomeshNo ratings yet

- Chapter ViDocument21 pagesChapter ViHarshada SinghNo ratings yet

- Definition of WorkmanDocument4 pagesDefinition of WorkmanJyoti Yogesh Rawat BantuNo ratings yet

- Labour Law AssignmentDocument11 pagesLabour Law Assignmentsarthak mohan shuklaNo ratings yet

- Dr. A.S. Anand and K.T. Thomas, JJ.: Equiv Alent Citation: 1996VIIAD (SC) 125Document23 pagesDr. A.S. Anand and K.T. Thomas, JJ.: Equiv Alent Citation: 1996VIIAD (SC) 125Adarsh KumarNo ratings yet

- Industrial Employment Standing Order Act CSJMDocument8 pagesIndustrial Employment Standing Order Act CSJMmanoramasingh679No ratings yet

- The Industrial Employment (Standing Orders) Act, 1946 & Chapter Iv of The Irc 2020Document39 pagesThe Industrial Employment (Standing Orders) Act, 1946 & Chapter Iv of The Irc 2020KanavNo ratings yet

- Indian Oil Cop. V. Chief Labour CommissionerDocument3 pagesIndian Oil Cop. V. Chief Labour CommissionerVida travel SolutionsNo ratings yet

- DEFINITIONDocument15 pagesDEFINITIONAbdul Kabir ShaikhNo ratings yet

- The Industrial Employment 2Document11 pagesThe Industrial Employment 2Knowledge PlanetNo ratings yet

- Labour Law Project On Workman: Prepared byDocument31 pagesLabour Law Project On Workman: Prepared byrajeevrvs083No ratings yet

- Interpretation of OccupierDocument4 pagesInterpretation of Occupiersathya1988gopal6349No ratings yet

- Worker: Factories Act, 1948:-2 (L) "Worker" Means A Person Employed, Directly or by or ThroughDocument10 pagesWorker: Factories Act, 1948:-2 (L) "Worker" Means A Person Employed, Directly or by or ThroughVicky DNo ratings yet

- Clra 1970Document37 pagesClra 1970Rituparna MallickNo ratings yet

- The Contract Labour (Regulation & Abolition) Act, 1970Document10 pagesThe Contract Labour (Regulation & Abolition) Act, 1970TAMANNANo ratings yet

- Labour & Industrial Law PDFDocument93 pagesLabour & Industrial Law PDFfarhat khanNo ratings yet

- Whole Time DirectorDocument4 pagesWhole Time DirectorBHUVANA THANGAMANINo ratings yet

- S 2 (N) of The Factories Act 1948 Whose Liability?Document2 pagesS 2 (N) of The Factories Act 1948 Whose Liability?Mohammad IrfanNo ratings yet

- Standing Orders Labour Law ProjectDocument12 pagesStanding Orders Labour Law ProjectMaaz Alam100% (1)

- Common ConceptsDocument591 pagesCommon ConceptsJaminder BibraNo ratings yet

- Unit 4 FinalDocument13 pagesUnit 4 FinalTariq HussainNo ratings yet

- Difference Between Workman and Contract LabourDocument4 pagesDifference Between Workman and Contract LabourGaurav mishraNo ratings yet

- LFGHR FILE (Final)Document25 pagesLFGHR FILE (Final)Mitz JazNo ratings yet

- CLJU 2001 394 PSBDocument70 pagesCLJU 2001 394 PSBateezsuperbNo ratings yet

- RD-SC: R.K. Panda V. Steel Authority of India (1994) 315 (12 May 1994)Document6 pagesRD-SC: R.K. Panda V. Steel Authority of India (1994) 315 (12 May 1994)sandeshh11No ratings yet

- LAbourDocument12 pagesLAbourDhruv AghiNo ratings yet

- Madhuja Chatterjee Lil - Ii Cia 3Document5 pagesMadhuja Chatterjee Lil - Ii Cia 3Madhuja ChatterjeeNo ratings yet

- Labour Law Topic 2 AssignmentDocument14 pagesLabour Law Topic 2 AssignmentDeepika PatelNo ratings yet

- The Icfai University: Submitted byDocument11 pagesThe Icfai University: Submitted byRiya SinghNo ratings yet

- "Workman": Jai Narain Vyas University, JodhpurDocument13 pages"Workman": Jai Narain Vyas University, Jodhpurshahbaz khanNo ratings yet

- Contract Labour in India: A Critical Evaluation: Research PaperDocument4 pagesContract Labour in India: A Critical Evaluation: Research PaperAnkit Sourav SahooNo ratings yet

- The Industrial EmploymentDocument10 pagesThe Industrial EmploymentAnonymous tUnGov9No ratings yet

- Quest:-What Is Meant by Industrial Dispute and Individual Dipute? Ans: - Industrial Dispute Section 2 (K)Document4 pagesQuest:-What Is Meant by Industrial Dispute and Individual Dipute? Ans: - Industrial Dispute Section 2 (K)Teja AbNo ratings yet

- Labour MaterialDocument12 pagesLabour MaterialShurbhi YadavNo ratings yet

- LectureNLUDContract LabourDocument42 pagesLectureNLUDContract Laboursujit kumarNo ratings yet

- A "Workman" Under The Industrial Disputes Act, 1947Document4 pagesA "Workman" Under The Industrial Disputes Act, 1947Asha Anbalagan100% (1)

- labour-law-finalDocument18 pageslabour-law-finalNoor Hasan KhanNo ratings yet

- LL-II Final ReportDocument40 pagesLL-II Final Reportsaptarshi bhattacharjeeNo ratings yet

- Automotive Industry Workers Alliance v. RomuloDocument3 pagesAutomotive Industry Workers Alliance v. RomuloellavisdaNo ratings yet

- Amity Law School, Centre-Ii: LABOUR LAW Project OnDocument5 pagesAmity Law School, Centre-Ii: LABOUR LAW Project OnSarthak GaurNo ratings yet

- The Occupational Safety and Regulations Labour Code NewDocument10 pagesThe Occupational Safety and Regulations Labour Code NewMuskaan SinhaNo ratings yet

- CLRA Important NotesDocument7 pagesCLRA Important NotesGaurav ThakurNo ratings yet

- Annamalai University: Labour Law - IiDocument86 pagesAnnamalai University: Labour Law - IiPrabhakaran ChandrasekaranNo ratings yet

- Literature Review On Employment Standing Orders by T.nivedithaDocument17 pagesLiterature Review On Employment Standing Orders by T.nivedithaniveditha krishna100% (1)

- Commented (HK1) : Employees Come Under The Definition Of: PersonnelDocument3 pagesCommented (HK1) : Employees Come Under The Definition Of: PersonnelharshkumraNo ratings yet

- M/S Harrison Malyalam PVT - Ltd. & Ors.: ESI CorporationDocument17 pagesM/S Harrison Malyalam PVT - Ltd. & Ors.: ESI CorporationSounak VermaNo ratings yet

- Contract Labour (Regulation and Abolition) ActDocument37 pagesContract Labour (Regulation and Abolition) ActMridul CrystelleNo ratings yet

- Labour Law II - AnushkaDocument12 pagesLabour Law II - AnushkaRishabh JainNo ratings yet

- Employees Provident Fund Act, 1952Document0 pagesEmployees Provident Fund Act, 1952Sunil ShawNo ratings yet

- India Labor LawsDocument4 pagesIndia Labor Lawsgautam_hariharanNo ratings yet

- THE LABOUR LAW IN UGANDA: [A TeeParkots Inc Publishers Product]From EverandTHE LABOUR LAW IN UGANDA: [A TeeParkots Inc Publishers Product]No ratings yet

- AP05 AA6 EV06 Ingles Construccion Glosario TecnicoDocument3 pagesAP05 AA6 EV06 Ingles Construccion Glosario Tecnicoxeider สุดท้าย สุดท้ายNo ratings yet

- Calina - Patterson - Resistance To Change Discussion Handout #1Document2 pagesCalina - Patterson - Resistance To Change Discussion Handout #1Calina PattersonNo ratings yet

- Smriti Swar - Brij - Sharma Interim ReportDocument96 pagesSmriti Swar - Brij - Sharma Interim Reportsms0331No ratings yet

- Cyber Law and Ipr Issues: The Indian Perspective: Mr. Atul Satwa JaybhayeDocument14 pagesCyber Law and Ipr Issues: The Indian Perspective: Mr. Atul Satwa JaybhayeAmit TiwariNo ratings yet

- Analysis of GATE 2010Document25 pagesAnalysis of GATE 2010aloo_12345No ratings yet

- 160 76-PW4Document26 pages160 76-PW4Ali raajNo ratings yet

- Ibps Po Mains 2019 SolutionsDocument16 pagesIbps Po Mains 2019 SolutionssampleNo ratings yet

- Final BSR Road Bridge Nagaur of 2019Document66 pagesFinal BSR Road Bridge Nagaur of 2019Jakhar MukeshNo ratings yet

- Comparison Between C and C++ and Lisp and PrologDocument18 pagesComparison Between C and C++ and Lisp and PrologAhmed HeshamNo ratings yet

- KXMB 2230 JTDocument526 pagesKXMB 2230 JTkacperorNo ratings yet

- AnalogI PDFDocument48 pagesAnalogI PDFJerc ZajNo ratings yet

- Accenture AptitudeDocument122 pagesAccenture AptitudeHarshith P.BNo ratings yet

- ProjectDocument61 pagesProjectgoodvijay143No ratings yet

- Faculty of Management SciencesDocument24 pagesFaculty of Management SciencesMuhammad SafdarNo ratings yet

- HW3 SolDocument6 pagesHW3 Solmary_nailynNo ratings yet

- Ra 10639Document6 pagesRa 10639Rea Rosario MaliteNo ratings yet

- Monitoring Neuromuskular Kuantitatif Pada Penggunaan Muscle RelaxantDocument17 pagesMonitoring Neuromuskular Kuantitatif Pada Penggunaan Muscle RelaxantWidi Yuli HariantoNo ratings yet

- Bunkers Quality and Quantity ClaimsDocument36 pagesBunkers Quality and Quantity ClaimsParthiban NagarajanNo ratings yet

- Masabong Elementary School: Reading Action PlanDocument27 pagesMasabong Elementary School: Reading Action PlanMaribel BelarminoNo ratings yet

- Solve Splits Feedback ToolDocument6 pagesSolve Splits Feedback ToolkabyaNo ratings yet

- Makalah CJR BibDocument9 pagesMakalah CJR BibRyan AlfandiNo ratings yet

- Data Bulletin Variable Frequency Drives and Short-Circuit Current RatingsDocument12 pagesData Bulletin Variable Frequency Drives and Short-Circuit Current Ratingsrenzo_aspa_orgNo ratings yet

- VBC East South Hall Renovations Contract FINAL 2024Document46 pagesVBC East South Hall Renovations Contract FINAL 2024Kayode CrownNo ratings yet

- ADR Nego PlanDocument4 pagesADR Nego PlanDeeshaNo ratings yet

- Nix ManualDocument108 pagesNix ManualJérôme AntoineNo ratings yet

- Antivirus ListDocument3 pagesAntivirus ListAlekhyaNo ratings yet

- Earnings Surprises, Growth Expectations, and Stock Returns or Don't Let An Earnings Torpedo Sink Your PortfolioDocument24 pagesEarnings Surprises, Growth Expectations, and Stock Returns or Don't Let An Earnings Torpedo Sink Your PortfolioTomás Valenzuela TormNo ratings yet

- 2010 11 11 EreDocument3 pages2010 11 11 Eremet140No ratings yet

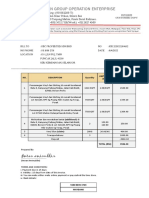

- Ilan Group Operation Enterprise: Imran AminuddinDocument1 pageIlan Group Operation Enterprise: Imran AminuddinIzhar AminuddinNo ratings yet

![THE LABOUR LAW IN UGANDA: [A TeeParkots Inc Publishers Product]](https://imgv2-1-f.scribdassets.com/img/word_document/702714789/149x198/ac277f344e/1706724197?v=1)

Download as doc, pdf, or txt

You might also like

- Social Factors Affecting Educational PlanningDocument9 pagesSocial Factors Affecting Educational PlanningShaayongo Benjamin50% (2)

- Objective and Scope of Industrial EmployDocument9 pagesObjective and Scope of Industrial EmployLakshmi Narayan RNo ratings yet

- Amity University: Amity Law School, Lucknow CampusDocument9 pagesAmity University: Amity Law School, Lucknow CampusAK KhareNo ratings yet

- Contract Labour Act OverviewDocument21 pagesContract Labour Act OverviewDhriti SharmaNo ratings yet

- Labour Law 2 ProjectDocument12 pagesLabour Law 2 ProjectSrijeshNo ratings yet

- Standing OrderDocument11 pagesStanding OrderKeerthana RavichandranNo ratings yet

- FAQs - Rationalizing Labour During COVID-19Document22 pagesFAQs - Rationalizing Labour During COVID-19amirarsiwalaNo ratings yet

- Workman - Under Industrial Disputes Act, 1947 - Employee Rights - Labour Relations - IndiaDocument3 pagesWorkman - Under Industrial Disputes Act, 1947 - Employee Rights - Labour Relations - IndiaRomeshNo ratings yet

- Chapter ViDocument21 pagesChapter ViHarshada SinghNo ratings yet

- Definition of WorkmanDocument4 pagesDefinition of WorkmanJyoti Yogesh Rawat BantuNo ratings yet

- Labour Law AssignmentDocument11 pagesLabour Law Assignmentsarthak mohan shuklaNo ratings yet

- Dr. A.S. Anand and K.T. Thomas, JJ.: Equiv Alent Citation: 1996VIIAD (SC) 125Document23 pagesDr. A.S. Anand and K.T. Thomas, JJ.: Equiv Alent Citation: 1996VIIAD (SC) 125Adarsh KumarNo ratings yet

- Industrial Employment Standing Order Act CSJMDocument8 pagesIndustrial Employment Standing Order Act CSJMmanoramasingh679No ratings yet

- The Industrial Employment (Standing Orders) Act, 1946 & Chapter Iv of The Irc 2020Document39 pagesThe Industrial Employment (Standing Orders) Act, 1946 & Chapter Iv of The Irc 2020KanavNo ratings yet

- Indian Oil Cop. V. Chief Labour CommissionerDocument3 pagesIndian Oil Cop. V. Chief Labour CommissionerVida travel SolutionsNo ratings yet

- DEFINITIONDocument15 pagesDEFINITIONAbdul Kabir ShaikhNo ratings yet

- The Industrial Employment 2Document11 pagesThe Industrial Employment 2Knowledge PlanetNo ratings yet

- Labour Law Project On Workman: Prepared byDocument31 pagesLabour Law Project On Workman: Prepared byrajeevrvs083No ratings yet

- Interpretation of OccupierDocument4 pagesInterpretation of Occupiersathya1988gopal6349No ratings yet

- Worker: Factories Act, 1948:-2 (L) "Worker" Means A Person Employed, Directly or by or ThroughDocument10 pagesWorker: Factories Act, 1948:-2 (L) "Worker" Means A Person Employed, Directly or by or ThroughVicky DNo ratings yet

- Clra 1970Document37 pagesClra 1970Rituparna MallickNo ratings yet

- The Contract Labour (Regulation & Abolition) Act, 1970Document10 pagesThe Contract Labour (Regulation & Abolition) Act, 1970TAMANNANo ratings yet

- Labour & Industrial Law PDFDocument93 pagesLabour & Industrial Law PDFfarhat khanNo ratings yet

- Whole Time DirectorDocument4 pagesWhole Time DirectorBHUVANA THANGAMANINo ratings yet

- S 2 (N) of The Factories Act 1948 Whose Liability?Document2 pagesS 2 (N) of The Factories Act 1948 Whose Liability?Mohammad IrfanNo ratings yet

- Standing Orders Labour Law ProjectDocument12 pagesStanding Orders Labour Law ProjectMaaz Alam100% (1)

- Common ConceptsDocument591 pagesCommon ConceptsJaminder BibraNo ratings yet

- Unit 4 FinalDocument13 pagesUnit 4 FinalTariq HussainNo ratings yet

- Difference Between Workman and Contract LabourDocument4 pagesDifference Between Workman and Contract LabourGaurav mishraNo ratings yet

- LFGHR FILE (Final)Document25 pagesLFGHR FILE (Final)Mitz JazNo ratings yet

- CLJU 2001 394 PSBDocument70 pagesCLJU 2001 394 PSBateezsuperbNo ratings yet

- RD-SC: R.K. Panda V. Steel Authority of India (1994) 315 (12 May 1994)Document6 pagesRD-SC: R.K. Panda V. Steel Authority of India (1994) 315 (12 May 1994)sandeshh11No ratings yet

- LAbourDocument12 pagesLAbourDhruv AghiNo ratings yet

- Madhuja Chatterjee Lil - Ii Cia 3Document5 pagesMadhuja Chatterjee Lil - Ii Cia 3Madhuja ChatterjeeNo ratings yet

- Labour Law Topic 2 AssignmentDocument14 pagesLabour Law Topic 2 AssignmentDeepika PatelNo ratings yet

- The Icfai University: Submitted byDocument11 pagesThe Icfai University: Submitted byRiya SinghNo ratings yet

- "Workman": Jai Narain Vyas University, JodhpurDocument13 pages"Workman": Jai Narain Vyas University, Jodhpurshahbaz khanNo ratings yet

- Contract Labour in India: A Critical Evaluation: Research PaperDocument4 pagesContract Labour in India: A Critical Evaluation: Research PaperAnkit Sourav SahooNo ratings yet

- The Industrial EmploymentDocument10 pagesThe Industrial EmploymentAnonymous tUnGov9No ratings yet

- Quest:-What Is Meant by Industrial Dispute and Individual Dipute? Ans: - Industrial Dispute Section 2 (K)Document4 pagesQuest:-What Is Meant by Industrial Dispute and Individual Dipute? Ans: - Industrial Dispute Section 2 (K)Teja AbNo ratings yet

- Labour MaterialDocument12 pagesLabour MaterialShurbhi YadavNo ratings yet

- LectureNLUDContract LabourDocument42 pagesLectureNLUDContract Laboursujit kumarNo ratings yet

- A "Workman" Under The Industrial Disputes Act, 1947Document4 pagesA "Workman" Under The Industrial Disputes Act, 1947Asha Anbalagan100% (1)

- labour-law-finalDocument18 pageslabour-law-finalNoor Hasan KhanNo ratings yet

- LL-II Final ReportDocument40 pagesLL-II Final Reportsaptarshi bhattacharjeeNo ratings yet

- Automotive Industry Workers Alliance v. RomuloDocument3 pagesAutomotive Industry Workers Alliance v. RomuloellavisdaNo ratings yet

- Amity Law School, Centre-Ii: LABOUR LAW Project OnDocument5 pagesAmity Law School, Centre-Ii: LABOUR LAW Project OnSarthak GaurNo ratings yet

- The Occupational Safety and Regulations Labour Code NewDocument10 pagesThe Occupational Safety and Regulations Labour Code NewMuskaan SinhaNo ratings yet

- CLRA Important NotesDocument7 pagesCLRA Important NotesGaurav ThakurNo ratings yet

- Annamalai University: Labour Law - IiDocument86 pagesAnnamalai University: Labour Law - IiPrabhakaran ChandrasekaranNo ratings yet

- Literature Review On Employment Standing Orders by T.nivedithaDocument17 pagesLiterature Review On Employment Standing Orders by T.nivedithaniveditha krishna100% (1)

- Commented (HK1) : Employees Come Under The Definition Of: PersonnelDocument3 pagesCommented (HK1) : Employees Come Under The Definition Of: PersonnelharshkumraNo ratings yet

- M/S Harrison Malyalam PVT - Ltd. & Ors.: ESI CorporationDocument17 pagesM/S Harrison Malyalam PVT - Ltd. & Ors.: ESI CorporationSounak VermaNo ratings yet

- Contract Labour (Regulation and Abolition) ActDocument37 pagesContract Labour (Regulation and Abolition) ActMridul CrystelleNo ratings yet

- Labour Law II - AnushkaDocument12 pagesLabour Law II - AnushkaRishabh JainNo ratings yet

- Employees Provident Fund Act, 1952Document0 pagesEmployees Provident Fund Act, 1952Sunil ShawNo ratings yet

- India Labor LawsDocument4 pagesIndia Labor Lawsgautam_hariharanNo ratings yet

- THE LABOUR LAW IN UGANDA: [A TeeParkots Inc Publishers Product]From EverandTHE LABOUR LAW IN UGANDA: [A TeeParkots Inc Publishers Product]No ratings yet

- AP05 AA6 EV06 Ingles Construccion Glosario TecnicoDocument3 pagesAP05 AA6 EV06 Ingles Construccion Glosario Tecnicoxeider สุดท้าย สุดท้ายNo ratings yet

- Calina - Patterson - Resistance To Change Discussion Handout #1Document2 pagesCalina - Patterson - Resistance To Change Discussion Handout #1Calina PattersonNo ratings yet

- Smriti Swar - Brij - Sharma Interim ReportDocument96 pagesSmriti Swar - Brij - Sharma Interim Reportsms0331No ratings yet

- Cyber Law and Ipr Issues: The Indian Perspective: Mr. Atul Satwa JaybhayeDocument14 pagesCyber Law and Ipr Issues: The Indian Perspective: Mr. Atul Satwa JaybhayeAmit TiwariNo ratings yet

- Analysis of GATE 2010Document25 pagesAnalysis of GATE 2010aloo_12345No ratings yet

- 160 76-PW4Document26 pages160 76-PW4Ali raajNo ratings yet

- Ibps Po Mains 2019 SolutionsDocument16 pagesIbps Po Mains 2019 SolutionssampleNo ratings yet

- Final BSR Road Bridge Nagaur of 2019Document66 pagesFinal BSR Road Bridge Nagaur of 2019Jakhar MukeshNo ratings yet

- Comparison Between C and C++ and Lisp and PrologDocument18 pagesComparison Between C and C++ and Lisp and PrologAhmed HeshamNo ratings yet

- KXMB 2230 JTDocument526 pagesKXMB 2230 JTkacperorNo ratings yet

- AnalogI PDFDocument48 pagesAnalogI PDFJerc ZajNo ratings yet

- Accenture AptitudeDocument122 pagesAccenture AptitudeHarshith P.BNo ratings yet

- ProjectDocument61 pagesProjectgoodvijay143No ratings yet

- Faculty of Management SciencesDocument24 pagesFaculty of Management SciencesMuhammad SafdarNo ratings yet

- HW3 SolDocument6 pagesHW3 Solmary_nailynNo ratings yet

- Ra 10639Document6 pagesRa 10639Rea Rosario MaliteNo ratings yet

- Monitoring Neuromuskular Kuantitatif Pada Penggunaan Muscle RelaxantDocument17 pagesMonitoring Neuromuskular Kuantitatif Pada Penggunaan Muscle RelaxantWidi Yuli HariantoNo ratings yet

- Bunkers Quality and Quantity ClaimsDocument36 pagesBunkers Quality and Quantity ClaimsParthiban NagarajanNo ratings yet

- Masabong Elementary School: Reading Action PlanDocument27 pagesMasabong Elementary School: Reading Action PlanMaribel BelarminoNo ratings yet

- Solve Splits Feedback ToolDocument6 pagesSolve Splits Feedback ToolkabyaNo ratings yet

- Makalah CJR BibDocument9 pagesMakalah CJR BibRyan AlfandiNo ratings yet

- Data Bulletin Variable Frequency Drives and Short-Circuit Current RatingsDocument12 pagesData Bulletin Variable Frequency Drives and Short-Circuit Current Ratingsrenzo_aspa_orgNo ratings yet

- VBC East South Hall Renovations Contract FINAL 2024Document46 pagesVBC East South Hall Renovations Contract FINAL 2024Kayode CrownNo ratings yet

- ADR Nego PlanDocument4 pagesADR Nego PlanDeeshaNo ratings yet

- Nix ManualDocument108 pagesNix ManualJérôme AntoineNo ratings yet

- Antivirus ListDocument3 pagesAntivirus ListAlekhyaNo ratings yet

- Earnings Surprises, Growth Expectations, and Stock Returns or Don't Let An Earnings Torpedo Sink Your PortfolioDocument24 pagesEarnings Surprises, Growth Expectations, and Stock Returns or Don't Let An Earnings Torpedo Sink Your PortfolioTomás Valenzuela TormNo ratings yet

- 2010 11 11 EreDocument3 pages2010 11 11 Eremet140No ratings yet

- Ilan Group Operation Enterprise: Imran AminuddinDocument1 pageIlan Group Operation Enterprise: Imran AminuddinIzhar AminuddinNo ratings yet