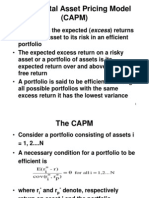

Outline: The Capital Asset Pricing Model (CAPM)

Outline: The Capital Asset Pricing Model (CAPM)

You might also like

- Day Trading With Price Action Volume 3 - Price PatternsDocument239 pagesDay Trading With Price Action Volume 3 - Price PatternsĐặngNhậtPhi100% (5)

- MOS 3311 Final NotesDocument33 pagesMOS 3311 Final Notesshakuntala12321No ratings yet

- SEC Compliance Checklist - GeneralDocument156 pagesSEC Compliance Checklist - GeneralAnujan RamanujanNo ratings yet

- Global Financial Markets and Instruments - Home - Coursera PDFDocument4 pagesGlobal Financial Markets and Instruments - Home - Coursera PDFsaurabh patil0% (3)

- Lecture 10 FINM2401 CAPM and Cost of CapitalDocument56 pagesLecture 10 FINM2401 CAPM and Cost of CapitalThomasNo ratings yet

- Bm410-10 Theory 3 - Capm and Apt 29sep05Document41 pagesBm410-10 Theory 3 - Capm and Apt 29sep05Adam KhaleelNo ratings yet

- FINALS Investment Cheat SheetDocument9 pagesFINALS Investment Cheat SheetNicholas YinNo ratings yet

- Chapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnDocument9 pagesChapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnBiloni KadakiaNo ratings yet

- Markowitz ModelDocument17 pagesMarkowitz ModelgultoNo ratings yet

- Capital Asset Pricing and Arbitrage Pricing TheoryDocument25 pagesCapital Asset Pricing and Arbitrage Pricing TheoryBen CannonNo ratings yet

- Solvency / Ratio/ Leverage / Liquididty AnalysisDocument142 pagesSolvency / Ratio/ Leverage / Liquididty AnalysisshobasridharNo ratings yet

- Portfolio TheoryDocument25 pagesPortfolio TheoryChhavi BhatnagarNo ratings yet

- 6 APT Slides ch10Document53 pages6 APT Slides ch10Zoe RossiNo ratings yet

- BKM Chapter 9Document4 pagesBKM Chapter 9Ana Nives RadovićNo ratings yet

- Asset Pricing ModelsDocument60 pagesAsset Pricing ModelsCharlyNo ratings yet

- Study Notes Modern Portfolio Theory (MPT) and The Capital Asset Pricing Model (CAPM)Document26 pagesStudy Notes Modern Portfolio Theory (MPT) and The Capital Asset Pricing Model (CAPM)alok kundaliaNo ratings yet

- Multifactor Models: A FactorDocument15 pagesMultifactor Models: A FactortigerjcNo ratings yet

- Efficient Frontier Construction Method 1Document9 pagesEfficient Frontier Construction Method 1scorn21No ratings yet

- Lezione 4Document42 pagesLezione 4gio040700No ratings yet

- Topic 4Document6 pagesTopic 4arp140102No ratings yet

- Umd Apt IcapmDocument4 pagesUmd Apt IcapmlxglobusNo ratings yet

- 2012 PPP III & SolutionDocument10 pages2012 PPP III & SolutiontimNo ratings yet

- An Introduction To Portfolio OptimizationDocument55 pagesAn Introduction To Portfolio OptimizationMarlee123100% (1)

- Module 2 CAPMDocument11 pagesModule 2 CAPMTanvi DevadigaNo ratings yet

- Capital Market TheoryDocument5 pagesCapital Market TheoryZakia ElhamNo ratings yet

- Topic06 - APT and Multifactor ModelsDocument28 pagesTopic06 - APT and Multifactor Modelsmatthiaskoerner19No ratings yet

- Portfolio ConstructionDocument27 pagesPortfolio ConstructionAgnivesh JayaNo ratings yet

- Capital Asset Pricing ModelDocument24 pagesCapital Asset Pricing ModelBrij MohanNo ratings yet

- L1 R50 HY NotesDocument7 pagesL1 R50 HY Notesayesha ansariNo ratings yet

- Capital Market Theory: An OverviewDocument38 pagesCapital Market Theory: An OverviewdevinamisraNo ratings yet

- Capital Market LineDocument8 pagesCapital Market Linecjpadin09No ratings yet

- APTDocument7 pagesAPTStefanNo ratings yet

- Resume CH 7 - 0098 - 0326Document5 pagesResume CH 7 - 0098 - 0326nur eka ayu danaNo ratings yet

- CAPM Prof. Pasquale Della CorteDocument46 pagesCAPM Prof. Pasquale Della Corteguzman87No ratings yet

- The Capital Asset Pricing Model (CAPM)Document31 pagesThe Capital Asset Pricing Model (CAPM)Tanmay AbhijeetNo ratings yet

- Lecture 10 - CAPMDocument19 pagesLecture 10 - CAPMroBinNo ratings yet

- Ec371 Topic 3Document13 pagesEc371 Topic 3Mohamed HussienNo ratings yet

- 2003 - Selecting A Risk-Adjusted Shareholder Performance MeasureDocument39 pages2003 - Selecting A Risk-Adjusted Shareholder Performance MeasureCarlosNo ratings yet

- FF6121 Investments: Week 7Document54 pagesFF6121 Investments: Week 7朱艺璇No ratings yet

- An Introduction To Modern Portfolio TheoryDocument38 pagesAn Introduction To Modern Portfolio Theoryhmme21No ratings yet

- FE 445 M1 CheatsheetDocument5 pagesFE 445 M1 Cheatsheetsaya1990No ratings yet

- RevisionDocument89 pagesRevision2tzf9tqpfpNo ratings yet

- CapmDocument26 pagesCapmNiravjain33No ratings yet

- Capm and AptDocument10 pagesCapm and AptRajkumar35No ratings yet

- FINNLEC Lecture Notes Section 6 - Equilibrium Asset Pricing Theories Part 2Document26 pagesFINNLEC Lecture Notes Section 6 - Equilibrium Asset Pricing Theories Part 2Philip ChengNo ratings yet

- Capital Asset Pricing ModelDocument18 pagesCapital Asset Pricing ModelSanjeevNo ratings yet

- CapmDocument26 pagesCapmapi-3814557100% (1)

- Aide Memoire: FTX3044F - TEST 2 (Chapters 5 - 12)Document18 pagesAide Memoire: FTX3044F - TEST 2 (Chapters 5 - 12)Callum Thain BlackNo ratings yet

- FDHDHFHGCHGFTHDGCGGDDocument13 pagesFDHDHFHGCHGFTHDGCGGDbabylovelylovelyNo ratings yet

- Topic 4Document17 pagesTopic 4andy033003No ratings yet

- Sem 1 - Capitulo 5 CvitanicDocument23 pagesSem 1 - Capitulo 5 CvitanicallisonNo ratings yet

- Problem Set 1 Financial Risk Management: DR Zoe TsesmelidakisDocument7 pagesProblem Set 1 Financial Risk Management: DR Zoe TsesmelidakisValentin IsNo ratings yet

- Analysis and Comparison of Capital Asset Pricing Model and Arbitrage Pricing Theory ModelDocument8 pagesAnalysis and Comparison of Capital Asset Pricing Model and Arbitrage Pricing Theory ModelAmal AsseyrNo ratings yet

- Chap 10 Bodie 9eDocument9 pagesChap 10 Bodie 9eCatherine WuNo ratings yet

- Multi FactorDocument22 pagesMulti FactorAnanda Rea KasanaNo ratings yet

- The Capital Asset Pricing Model and The Arbitrage Pricing TheoryDocument21 pagesThe Capital Asset Pricing Model and The Arbitrage Pricing TheoryKetz NKNo ratings yet

- CAPMDocument45 pagesCAPMkokmunwai717No ratings yet

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Quantitative Portfolio Management: with Applications in PythonFrom EverandQuantitative Portfolio Management: with Applications in PythonNo ratings yet

- A Machine Learning based Pairs Trading Investment StrategyFrom EverandA Machine Learning based Pairs Trading Investment StrategyNo ratings yet

- CH 05Document45 pagesCH 05peter sumNo ratings yet

- Natural Number ExponentsDocument5 pagesNatural Number Exponentspeter sumNo ratings yet

- Market Imperfections - Econ NotesDocument30 pagesMarket Imperfections - Econ Notespeter sumNo ratings yet

- Risk, Returns and WACC: CAPM and The Capital BudgetingDocument41 pagesRisk, Returns and WACC: CAPM and The Capital Budgetingpeter sumNo ratings yet

- Financial RatiosDocument4 pagesFinancial Ratiospeter sumNo ratings yet

- Logarithm Rules - Log (X) RulesDocument3 pagesLogarithm Rules - Log (X) Rulespeter sumNo ratings yet

- CUHK IB RequirementDocument2 pagesCUHK IB Requirementpeter sumNo ratings yet

- Module 01 - Humans As OrganismsDocument5 pagesModule 01 - Humans As Organismspeter sumNo ratings yet

- Accounting Theory PDFDocument61 pagesAccounting Theory PDFrabin khatriNo ratings yet

- S T R A T e G I C M A N A G e M e N T A C C o U N T I N G (C - 2)Document4 pagesS T R A T e G I C M A N A G e M e N T A C C o U N T I N G (C - 2)Zubair AhmedNo ratings yet

- Cambridge O Level: Accounting 7707/12Document12 pagesCambridge O Level: Accounting 7707/12Geerish BissessurNo ratings yet

- 2020 Preqin Global Infrastructure Report Sample PagesDocument12 pages2020 Preqin Global Infrastructure Report Sample PagesMarco ErmantazziNo ratings yet

- Standalone Balance SheetDocument1 pageStandalone Balance SheetPrerna ChavanNo ratings yet

- Case Study - ArcelorDocument3 pagesCase Study - ArcelorAshish MittalNo ratings yet

- Mutual Fund Analysis & Portfolio Management in Mutual FundsDocument76 pagesMutual Fund Analysis & Portfolio Management in Mutual FundsVipulNo ratings yet

- 0450 - s23 - in - 23 Business Past PapersDocument4 pages0450 - s23 - in - 23 Business Past Papersdillmustafa645No ratings yet

- Regulation 33 of SebiDocument4 pagesRegulation 33 of SebirqpNo ratings yet

- Time Value of MoneyDocument18 pagesTime Value of MoneyIIMnotesNo ratings yet

- Prospectus MICFLDocument122 pagesProspectus MICFLIftekhar AlamNo ratings yet

- ACCT212 - Individual - Learning - Project - Answersdocx CompleteDocument10 pagesACCT212 - Individual - Learning - Project - Answersdocx CompleteAmir ShahzadNo ratings yet

- Cryptocurrencies Vs Real EstateDocument3 pagesCryptocurrencies Vs Real EstateAnunobi JaneNo ratings yet

- STRATEGIC COST MANAGEMENT Module 2Document2 pagesSTRATEGIC COST MANAGEMENT Module 2Mary Ann GurreaNo ratings yet

- MIBOR Vs MIFORDocument3 pagesMIBOR Vs MIFORsubrat nandaNo ratings yet

- (Financial Accounting & Reporting 2) : Lecture AidDocument29 pages(Financial Accounting & Reporting 2) : Lecture AidMay Grethel Joy PeranteNo ratings yet

- Share Based Payment Implementation Guidance PDFDocument30 pagesShare Based Payment Implementation Guidance PDFNhel AlvaroNo ratings yet

- Chapter 5 Solutions 6th EditionDocument6 pagesChapter 5 Solutions 6th EditionSarah Martin Edwards50% (2)

- 13633921Document3 pages13633921Ika Zuliani NofitaNo ratings yet

- Consolidation of Financial StatementsDocument2 pagesConsolidation of Financial StatementsmanojjecrcNo ratings yet

- Fa Unit 1 - Notes - 20200718004241Document21 pagesFa Unit 1 - Notes - 20200718004241Vignesh CNo ratings yet

- CH 4 - Brief Exercises - 16thDocument18 pagesCH 4 - Brief Exercises - 16thkesey100% (2)

- Document 3Document3 pagesDocument 3jean hmidoNo ratings yet

- Analisis Ekonomi Lingkungan Terhadap Tempat Pemrosesan Akhir Sampah (Tpa) Jatibarang Kota SemarangDocument12 pagesAnalisis Ekonomi Lingkungan Terhadap Tempat Pemrosesan Akhir Sampah (Tpa) Jatibarang Kota Semarangferdin sitinjakNo ratings yet

- FCFE Analysis of TATA SteelDocument8 pagesFCFE Analysis of TATA SteelJobin Jose KadavilNo ratings yet

- Acc 252 Practice ExamDocument5 pagesAcc 252 Practice ExamEmy ManiyarNo ratings yet

- Trident The U S Based Company Discussed in This Chapter Has Concluded Another LargeDocument1 pageTrident The U S Based Company Discussed in This Chapter Has Concluded Another Largetrilocksp SinghNo ratings yet

Download as pdf or txt

You might also like

- Day Trading With Price Action Volume 3 - Price PatternsDocument239 pagesDay Trading With Price Action Volume 3 - Price PatternsĐặngNhậtPhi100% (5)

- MOS 3311 Final NotesDocument33 pagesMOS 3311 Final Notesshakuntala12321No ratings yet

- SEC Compliance Checklist - GeneralDocument156 pagesSEC Compliance Checklist - GeneralAnujan RamanujanNo ratings yet

- Global Financial Markets and Instruments - Home - Coursera PDFDocument4 pagesGlobal Financial Markets and Instruments - Home - Coursera PDFsaurabh patil0% (3)

- Lecture 10 FINM2401 CAPM and Cost of CapitalDocument56 pagesLecture 10 FINM2401 CAPM and Cost of CapitalThomasNo ratings yet

- Bm410-10 Theory 3 - Capm and Apt 29sep05Document41 pagesBm410-10 Theory 3 - Capm and Apt 29sep05Adam KhaleelNo ratings yet

- FINALS Investment Cheat SheetDocument9 pagesFINALS Investment Cheat SheetNicholas YinNo ratings yet

- Chapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnDocument9 pagesChapter 10: Arbitrage Pricing Theory and Multifactor Models of Risk and ReturnBiloni KadakiaNo ratings yet

- Markowitz ModelDocument17 pagesMarkowitz ModelgultoNo ratings yet

- Capital Asset Pricing and Arbitrage Pricing TheoryDocument25 pagesCapital Asset Pricing and Arbitrage Pricing TheoryBen CannonNo ratings yet

- Solvency / Ratio/ Leverage / Liquididty AnalysisDocument142 pagesSolvency / Ratio/ Leverage / Liquididty AnalysisshobasridharNo ratings yet

- Portfolio TheoryDocument25 pagesPortfolio TheoryChhavi BhatnagarNo ratings yet

- 6 APT Slides ch10Document53 pages6 APT Slides ch10Zoe RossiNo ratings yet

- BKM Chapter 9Document4 pagesBKM Chapter 9Ana Nives RadovićNo ratings yet

- Asset Pricing ModelsDocument60 pagesAsset Pricing ModelsCharlyNo ratings yet

- Study Notes Modern Portfolio Theory (MPT) and The Capital Asset Pricing Model (CAPM)Document26 pagesStudy Notes Modern Portfolio Theory (MPT) and The Capital Asset Pricing Model (CAPM)alok kundaliaNo ratings yet

- Multifactor Models: A FactorDocument15 pagesMultifactor Models: A FactortigerjcNo ratings yet

- Efficient Frontier Construction Method 1Document9 pagesEfficient Frontier Construction Method 1scorn21No ratings yet

- Lezione 4Document42 pagesLezione 4gio040700No ratings yet

- Topic 4Document6 pagesTopic 4arp140102No ratings yet

- Umd Apt IcapmDocument4 pagesUmd Apt IcapmlxglobusNo ratings yet

- 2012 PPP III & SolutionDocument10 pages2012 PPP III & SolutiontimNo ratings yet

- An Introduction To Portfolio OptimizationDocument55 pagesAn Introduction To Portfolio OptimizationMarlee123100% (1)

- Module 2 CAPMDocument11 pagesModule 2 CAPMTanvi DevadigaNo ratings yet

- Capital Market TheoryDocument5 pagesCapital Market TheoryZakia ElhamNo ratings yet

- Topic06 - APT and Multifactor ModelsDocument28 pagesTopic06 - APT and Multifactor Modelsmatthiaskoerner19No ratings yet

- Portfolio ConstructionDocument27 pagesPortfolio ConstructionAgnivesh JayaNo ratings yet

- Capital Asset Pricing ModelDocument24 pagesCapital Asset Pricing ModelBrij MohanNo ratings yet

- L1 R50 HY NotesDocument7 pagesL1 R50 HY Notesayesha ansariNo ratings yet

- Capital Market Theory: An OverviewDocument38 pagesCapital Market Theory: An OverviewdevinamisraNo ratings yet

- Capital Market LineDocument8 pagesCapital Market Linecjpadin09No ratings yet

- APTDocument7 pagesAPTStefanNo ratings yet

- Resume CH 7 - 0098 - 0326Document5 pagesResume CH 7 - 0098 - 0326nur eka ayu danaNo ratings yet

- CAPM Prof. Pasquale Della CorteDocument46 pagesCAPM Prof. Pasquale Della Corteguzman87No ratings yet

- The Capital Asset Pricing Model (CAPM)Document31 pagesThe Capital Asset Pricing Model (CAPM)Tanmay AbhijeetNo ratings yet

- Lecture 10 - CAPMDocument19 pagesLecture 10 - CAPMroBinNo ratings yet

- Ec371 Topic 3Document13 pagesEc371 Topic 3Mohamed HussienNo ratings yet

- 2003 - Selecting A Risk-Adjusted Shareholder Performance MeasureDocument39 pages2003 - Selecting A Risk-Adjusted Shareholder Performance MeasureCarlosNo ratings yet

- FF6121 Investments: Week 7Document54 pagesFF6121 Investments: Week 7朱艺璇No ratings yet

- An Introduction To Modern Portfolio TheoryDocument38 pagesAn Introduction To Modern Portfolio Theoryhmme21No ratings yet

- FE 445 M1 CheatsheetDocument5 pagesFE 445 M1 Cheatsheetsaya1990No ratings yet

- RevisionDocument89 pagesRevision2tzf9tqpfpNo ratings yet

- CapmDocument26 pagesCapmNiravjain33No ratings yet

- Capm and AptDocument10 pagesCapm and AptRajkumar35No ratings yet

- FINNLEC Lecture Notes Section 6 - Equilibrium Asset Pricing Theories Part 2Document26 pagesFINNLEC Lecture Notes Section 6 - Equilibrium Asset Pricing Theories Part 2Philip ChengNo ratings yet

- Capital Asset Pricing ModelDocument18 pagesCapital Asset Pricing ModelSanjeevNo ratings yet

- CapmDocument26 pagesCapmapi-3814557100% (1)

- Aide Memoire: FTX3044F - TEST 2 (Chapters 5 - 12)Document18 pagesAide Memoire: FTX3044F - TEST 2 (Chapters 5 - 12)Callum Thain BlackNo ratings yet

- FDHDHFHGCHGFTHDGCGGDDocument13 pagesFDHDHFHGCHGFTHDGCGGDbabylovelylovelyNo ratings yet

- Topic 4Document17 pagesTopic 4andy033003No ratings yet

- Sem 1 - Capitulo 5 CvitanicDocument23 pagesSem 1 - Capitulo 5 CvitanicallisonNo ratings yet

- Problem Set 1 Financial Risk Management: DR Zoe TsesmelidakisDocument7 pagesProblem Set 1 Financial Risk Management: DR Zoe TsesmelidakisValentin IsNo ratings yet

- Analysis and Comparison of Capital Asset Pricing Model and Arbitrage Pricing Theory ModelDocument8 pagesAnalysis and Comparison of Capital Asset Pricing Model and Arbitrage Pricing Theory ModelAmal AsseyrNo ratings yet

- Chap 10 Bodie 9eDocument9 pagesChap 10 Bodie 9eCatherine WuNo ratings yet

- Multi FactorDocument22 pagesMulti FactorAnanda Rea KasanaNo ratings yet

- The Capital Asset Pricing Model and The Arbitrage Pricing TheoryDocument21 pagesThe Capital Asset Pricing Model and The Arbitrage Pricing TheoryKetz NKNo ratings yet

- CAPMDocument45 pagesCAPMkokmunwai717No ratings yet

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Quantitative Portfolio Management: with Applications in PythonFrom EverandQuantitative Portfolio Management: with Applications in PythonNo ratings yet

- A Machine Learning based Pairs Trading Investment StrategyFrom EverandA Machine Learning based Pairs Trading Investment StrategyNo ratings yet

- CH 05Document45 pagesCH 05peter sumNo ratings yet

- Natural Number ExponentsDocument5 pagesNatural Number Exponentspeter sumNo ratings yet

- Market Imperfections - Econ NotesDocument30 pagesMarket Imperfections - Econ Notespeter sumNo ratings yet

- Risk, Returns and WACC: CAPM and The Capital BudgetingDocument41 pagesRisk, Returns and WACC: CAPM and The Capital Budgetingpeter sumNo ratings yet

- Financial RatiosDocument4 pagesFinancial Ratiospeter sumNo ratings yet

- Logarithm Rules - Log (X) RulesDocument3 pagesLogarithm Rules - Log (X) Rulespeter sumNo ratings yet

- CUHK IB RequirementDocument2 pagesCUHK IB Requirementpeter sumNo ratings yet

- Module 01 - Humans As OrganismsDocument5 pagesModule 01 - Humans As Organismspeter sumNo ratings yet

- Accounting Theory PDFDocument61 pagesAccounting Theory PDFrabin khatriNo ratings yet

- S T R A T e G I C M A N A G e M e N T A C C o U N T I N G (C - 2)Document4 pagesS T R A T e G I C M A N A G e M e N T A C C o U N T I N G (C - 2)Zubair AhmedNo ratings yet

- Cambridge O Level: Accounting 7707/12Document12 pagesCambridge O Level: Accounting 7707/12Geerish BissessurNo ratings yet

- 2020 Preqin Global Infrastructure Report Sample PagesDocument12 pages2020 Preqin Global Infrastructure Report Sample PagesMarco ErmantazziNo ratings yet

- Standalone Balance SheetDocument1 pageStandalone Balance SheetPrerna ChavanNo ratings yet

- Case Study - ArcelorDocument3 pagesCase Study - ArcelorAshish MittalNo ratings yet

- Mutual Fund Analysis & Portfolio Management in Mutual FundsDocument76 pagesMutual Fund Analysis & Portfolio Management in Mutual FundsVipulNo ratings yet

- 0450 - s23 - in - 23 Business Past PapersDocument4 pages0450 - s23 - in - 23 Business Past Papersdillmustafa645No ratings yet

- Regulation 33 of SebiDocument4 pagesRegulation 33 of SebirqpNo ratings yet

- Time Value of MoneyDocument18 pagesTime Value of MoneyIIMnotesNo ratings yet

- Prospectus MICFLDocument122 pagesProspectus MICFLIftekhar AlamNo ratings yet

- ACCT212 - Individual - Learning - Project - Answersdocx CompleteDocument10 pagesACCT212 - Individual - Learning - Project - Answersdocx CompleteAmir ShahzadNo ratings yet

- Cryptocurrencies Vs Real EstateDocument3 pagesCryptocurrencies Vs Real EstateAnunobi JaneNo ratings yet

- STRATEGIC COST MANAGEMENT Module 2Document2 pagesSTRATEGIC COST MANAGEMENT Module 2Mary Ann GurreaNo ratings yet

- MIBOR Vs MIFORDocument3 pagesMIBOR Vs MIFORsubrat nandaNo ratings yet

- (Financial Accounting & Reporting 2) : Lecture AidDocument29 pages(Financial Accounting & Reporting 2) : Lecture AidMay Grethel Joy PeranteNo ratings yet

- Share Based Payment Implementation Guidance PDFDocument30 pagesShare Based Payment Implementation Guidance PDFNhel AlvaroNo ratings yet

- Chapter 5 Solutions 6th EditionDocument6 pagesChapter 5 Solutions 6th EditionSarah Martin Edwards50% (2)

- 13633921Document3 pages13633921Ika Zuliani NofitaNo ratings yet

- Consolidation of Financial StatementsDocument2 pagesConsolidation of Financial StatementsmanojjecrcNo ratings yet

- Fa Unit 1 - Notes - 20200718004241Document21 pagesFa Unit 1 - Notes - 20200718004241Vignesh CNo ratings yet

- CH 4 - Brief Exercises - 16thDocument18 pagesCH 4 - Brief Exercises - 16thkesey100% (2)

- Document 3Document3 pagesDocument 3jean hmidoNo ratings yet

- Analisis Ekonomi Lingkungan Terhadap Tempat Pemrosesan Akhir Sampah (Tpa) Jatibarang Kota SemarangDocument12 pagesAnalisis Ekonomi Lingkungan Terhadap Tempat Pemrosesan Akhir Sampah (Tpa) Jatibarang Kota Semarangferdin sitinjakNo ratings yet

- FCFE Analysis of TATA SteelDocument8 pagesFCFE Analysis of TATA SteelJobin Jose KadavilNo ratings yet

- Acc 252 Practice ExamDocument5 pagesAcc 252 Practice ExamEmy ManiyarNo ratings yet

- Trident The U S Based Company Discussed in This Chapter Has Concluded Another LargeDocument1 pageTrident The U S Based Company Discussed in This Chapter Has Concluded Another Largetrilocksp SinghNo ratings yet