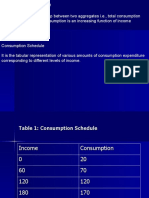

QTM

QTM

You might also like

- Principles of AccountingDocument657 pagesPrinciples of AccountingKhalid Aziz89% (107)

- Ambilikile Book 2-1 PDFDocument181 pagesAmbilikile Book 2-1 PDFplanet tz50% (6)

- Chapter-2 Public Finance by Pratham Singh PDFDocument13 pagesChapter-2 Public Finance by Pratham Singh PDFLavanya Tanwar100% (1)

- Valucon ReviewerDocument12 pagesValucon ReviewerAnjo Salonga del Rosario100% (4)

- ECONOMICS - Guided Reading and Study GuideDocument308 pagesECONOMICS - Guided Reading and Study GuideThorng Meng76% (21)

- Customs Valuation V2Document91 pagesCustoms Valuation V2natan makuNo ratings yet

- The Managerial Revolution - James Burnham (1941)Document235 pagesThe Managerial Revolution - James Burnham (1941)topbudget60% (5)

- Is LM ModelDocument3 pagesIs LM ModelAaquib AhmadNo ratings yet

- 12 Economics Balance of Payment Impq 1Document2 pages12 Economics Balance of Payment Impq 1RitikaNo ratings yet

- Is-LM Open EconomyDocument16 pagesIs-LM Open EconomyAppan Kandala VasudevacharyNo ratings yet

- Lectures 4 and 5 Modern Trade TheoriesDocument33 pagesLectures 4 and 5 Modern Trade TheoriesChenxi LiuNo ratings yet

- Concept of Money SupplyDocument7 pagesConcept of Money SupplyMD. IBRAHIM KHOLILULLAHNo ratings yet

- Ch. 4 Demand For MoneyDocument13 pagesCh. 4 Demand For Moneycoldpassion100% (1)

- STUDY MATERIAL ON Profit and Theories of Profit.Document63 pagesSTUDY MATERIAL ON Profit and Theories of Profit.Aparna ViswakumarNo ratings yet

- Supply - Class 11Document43 pagesSupply - Class 11bittomolla691No ratings yet

- NCERT Solutions For Class 12th Microeconomics - Chapter 3 - Production and Costs - AglaSem SchoolsDocument12 pagesNCERT Solutions For Class 12th Microeconomics - Chapter 3 - Production and Costs - AglaSem SchoolsNiranjan MishraNo ratings yet

- Grade - 11 Micro Economics Ch:03 Demand IDocument14 pagesGrade - 11 Micro Economics Ch:03 Demand IShubham GoelNo ratings yet

- Consumption FunctionDocument15 pagesConsumption FunctionAkshat MishraNo ratings yet

- Revised Tobin's Demand For MoneyDocument4 pagesRevised Tobin's Demand For MoneySnehasish MahataNo ratings yet

- Theory of Income and EmploymentDocument9 pagesTheory of Income and EmploymentsureshNo ratings yet

- Equilibrium Income and Output: Two-Sector Economy Y C+IDocument52 pagesEquilibrium Income and Output: Two-Sector Economy Y C+ISunu 3670100% (1)

- Producer's EquilibriumDocument19 pagesProducer's EquilibriumTejas ModiNo ratings yet

- Money & BankingDocument33 pagesMoney & BankingGeeta GhaiNo ratings yet

- Producer Equilibrium/Least Cost Combination: AssumptionsDocument5 pagesProducer Equilibrium/Least Cost Combination: AssumptionsJessy SinghNo ratings yet

- Submitted By: Biki Das Class - XI Stream - Commerce Roll No. - 5Document42 pagesSubmitted By: Biki Das Class - XI Stream - Commerce Roll No. - 5Biki DasNo ratings yet

- Namma Kalvi Economics Unit 5 Surya Economics Guide emDocument31 pagesNamma Kalvi Economics Unit 5 Surya Economics Guide emAakaash C.K.No ratings yet

- Cardinal Utility AnalysisDocument19 pagesCardinal Utility AnalysisShah MominNo ratings yet

- Economics NotesDocument71 pagesEconomics NotesUmer PrinceNo ratings yet

- ElasticityDocument25 pagesElasticityaljohn anticristoNo ratings yet

- Credit Creation in Commercial BanksDocument12 pagesCredit Creation in Commercial BanksprasanthmctNo ratings yet

- Crowding OutDocument3 pagesCrowding OutsattysattuNo ratings yet

- Producer's Equilibrium: Total Revenue & Total Cost ApproachDocument12 pagesProducer's Equilibrium: Total Revenue & Total Cost ApproachSarim KhanNo ratings yet

- Lecture Notes IS LM CurveDocument13 pagesLecture Notes IS LM CurvemNo ratings yet

- IB Econ Chap 16 Macro EQDocument11 pagesIB Econ Chap 16 Macro EQsweetlunaticNo ratings yet

- The IS-LM Model: Equilibrium: Goods and Money Markets Understanding Public PolicyDocument37 pagesThe IS-LM Model: Equilibrium: Goods and Money Markets Understanding Public PolicyShashank Shekhar SinghNo ratings yet

- Harrod Model of GrowthDocument6 pagesHarrod Model of Growthvikram inamdarNo ratings yet

- Monetary Policy: Monetary Policy Mechanism Objectives of Monetary Policy Tools of Monetary PolicyDocument20 pagesMonetary Policy: Monetary Policy Mechanism Objectives of Monetary Policy Tools of Monetary Policysuga29No ratings yet

- Mundell FlemingDocument40 pagesMundell FlemingAnkita Singhai100% (1)

- DemandDocument22 pagesDemandSerenity Kerr100% (1)

- Market EquilibriumDocument38 pagesMarket EquilibriumAbhi KumNo ratings yet

- Eco Dev - OrendayDocument17 pagesEco Dev - OrendayZhaira OrendayNo ratings yet

- Determinants of Investment: - Investment in Economics Means Addition ToDocument22 pagesDeterminants of Investment: - Investment in Economics Means Addition ToASHISHRD100% (1)

- Managerial Economics AssignmentDocument17 pagesManagerial Economics AssignmentDeepshikha Gupta50% (2)

- Macro Econom I eDocument9 pagesMacro Econom I eguy3hil8927No ratings yet

- 1.2 National Income Accounting PDFDocument24 pages1.2 National Income Accounting PDFdivya90% (10)

- Consumption Function and Its TypesDocument13 pagesConsumption Function and Its TypesTashiTamangNo ratings yet

- Baumol Inventory Theory - Amitabha SarkarDocument3 pagesBaumol Inventory Theory - Amitabha SarkarTripti Dutta100% (1)

- 2.theory of Demand and Supply.Document30 pages2.theory of Demand and Supply.punte77100% (1)

- Economics Case StudyDocument2 pagesEconomics Case StudyKUSH SHAH100% (1)

- Fiscal and Monetary Policies of IndiaDocument13 pagesFiscal and Monetary Policies of IndiaRidhika GuptaNo ratings yet

- Laws of ReturnDocument8 pagesLaws of ReturnSparsh MalhotraNo ratings yet

- Lec3 Harrod-Domar GrowthDocument17 pagesLec3 Harrod-Domar GrowthMehul GargNo ratings yet

- Extension and ContractionDocument5 pagesExtension and ContractionMonika Shekhawat100% (1)

- Classical Theory of Ecomomics 1Document46 pagesClassical Theory of Ecomomics 1Shireen YakubNo ratings yet

- Elasticity of DemandDocument17 pagesElasticity of DemandDental Sloss100% (1)

- Business Economics FYBComDocument3 pagesBusiness Economics FYBCompravin963No ratings yet

- Functions of MoneyDocument17 pagesFunctions of MoneyAnonymous ytZsBOVNo ratings yet

- Indian Economy 1950 1990Document8 pagesIndian Economy 1950 1990arpit9964100% (1)

- National Income Accounting PPT at MBADocument58 pagesNational Income Accounting PPT at MBABabasab Patil (Karrisatte)No ratings yet

- Unit 1-Fundamentals of EconomicsDocument35 pagesUnit 1-Fundamentals of EconomicsAyush SatyamNo ratings yet

- Macro-Economics Lecture (BBA)Document262 pagesMacro-Economics Lecture (BBA)Sahil NoorzaiNo ratings yet

- Production Possibility CurvesDocument6 pagesProduction Possibility CurvesFari AliNo ratings yet

- Balance of PaymentDocument9 pagesBalance of PaymentMuskanNo ratings yet

- IME WS 23 24 Problemset 01Document2 pagesIME WS 23 24 Problemset 01salih.durmusNo ratings yet

- University of Chicago Press Is Collaborating With JSTOR To Digitize, Preserve and Extend Access To Journal of Political EconomyDocument11 pagesUniversity of Chicago Press Is Collaborating With JSTOR To Digitize, Preserve and Extend Access To Journal of Political EconomyEdgar Diaz NietoNo ratings yet

- Mint Cash WhitepaperDocument40 pagesMint Cash Whitepaperyankees leeNo ratings yet

- Date Sheet PDFDocument1 pageDate Sheet PDFKhalid AzizNo ratings yet

- B-Com GP 1 2018 FinalDocument10 pagesB-Com GP 1 2018 FinalKhalid AzizNo ratings yet

- Cir CBE March 2017Document1 pageCir CBE March 2017Khalid AzizNo ratings yet

- Chapter 19 Operations and Value Chain Management: True/False QuestionsDocument33 pagesChapter 19 Operations and Value Chain Management: True/False QuestionsWaseem KambohNo ratings yet

- Final Test Advanced Accounting B-COM Part 2: Sir Khalid AzizDocument6 pagesFinal Test Advanced Accounting B-COM Part 2: Sir Khalid AzizKhalid AzizNo ratings yet

- Feb 2018 AnsDocument7 pagesFeb 2018 AnsKhalid AzizNo ratings yet

- Macro Economics NotesDocument18 pagesMacro Economics NotesKhalid Aziz100% (1)

- Guess Papers BY Sir Khalid Aziz: Iqra Commerce NetworkDocument14 pagesGuess Papers BY Sir Khalid Aziz: Iqra Commerce NetworkAnonymous NKjJIpNo ratings yet

- Marks Question No. 2 (A) (I) Conditions Need To Fulfill To Get A Licence: 05Document8 pagesMarks Question No. 2 (A) (I) Conditions Need To Fulfill To Get A Licence: 05Khalid AzizNo ratings yet

- B-Com GP 1Document10 pagesB-Com GP 1Khalid AzizNo ratings yet

- Guess Papers BY Sir Khalid Aziz: Iqra Commerce NetworkDocument14 pagesGuess Papers BY Sir Khalid Aziz: Iqra Commerce NetworkAnonymous NKjJIpNo ratings yet

- First Division Seat Nos:: University of Karachi Karachi (Examinations Department)Document5 pagesFirst Division Seat Nos:: University of Karachi Karachi (Examinations Department)Khalid AzizNo ratings yet

- Sir Khalid Aziz: According To New SyllabusDocument1 pageSir Khalid Aziz: According To New SyllabusKhalid AzizNo ratings yet

- q2 Half Yearly Financial Report Fifth Draft August 2015 PDFDocument26 pagesq2 Half Yearly Financial Report Fifth Draft August 2015 PDFKhalid AzizNo ratings yet

- Institute of Cost and Management Accountants of Pakistan: Assignment Questions - (Fall - 2013 Session)Document4 pagesInstitute of Cost and Management Accountants of Pakistan: Assignment Questions - (Fall - 2013 Session)Khalid AzizNo ratings yet

- Economics Mcqs Kit PDFDocument241 pagesEconomics Mcqs Kit PDFKhalid AzizNo ratings yet

- What Are The Main Problems of Agriculture SectorDocument4 pagesWhat Are The Main Problems of Agriculture SectorKhalid AzizNo ratings yet

- M.A. (Previous) External, Annual Examination 2014.Document2 pagesM.A. (Previous) External, Annual Examination 2014.Khalid AzizNo ratings yet

- Factory Overhead Idle Capacity VarianceDocument4 pagesFactory Overhead Idle Capacity VarianceKhalid Aziz100% (1)

- LL.B. PART - I, Annual Examination 2015.Document3 pagesLL.B. PART - I, Annual Examination 2015.Khalid AzizNo ratings yet

- MA Eco SyllabusDocument27 pagesMA Eco SyllabusRana AsimNo ratings yet

- Issue of SharesDocument20 pagesIssue of SharesKhalid AzizNo ratings yet

- Schumpeter ModelDocument5 pagesSchumpeter ModelKhalid Aziz100% (1)

- ClosingDocument1 pageClosingKhalid AzizNo ratings yet

- S.S.C. Part II General (Regular & Private) Group Results 2015Document106 pagesS.S.C. Part II General (Regular & Private) Group Results 2015Khalid AzizNo ratings yet

- Central BankingDocument22 pagesCentral BankingKhalid AzizNo ratings yet

- Semester - II, Subject - Sociology, Roll No. - 31, Name - Anand SinghDocument24 pagesSemester - II, Subject - Sociology, Roll No. - 31, Name - Anand SinghAnand SinghNo ratings yet

- 11 Economics sp01Document14 pages11 Economics sp01DËV DÃSNo ratings yet

- Grossman 1972 Health CapitalDocument33 pagesGrossman 1972 Health CapitalLeonardo SimonciniNo ratings yet

- Value AnalysisDocument6 pagesValue AnalysisAMIYA KUMAR SAMALNo ratings yet

- ABM B GROUP 1 Business PlanDocument142 pagesABM B GROUP 1 Business PlanGwen Ashley Dela PenaNo ratings yet

- Basic Appraisal For Real Estate BrokersDocument4 pagesBasic Appraisal For Real Estate Brokersbea100% (1)

- Eliot S Insight The Future of Urban DesignDocument5 pagesEliot S Insight The Future of Urban DesignPrudhvi Nagasaikumar RaviNo ratings yet

- Classical EconomicsDocument54 pagesClassical EconomicsAlionie FreyNo ratings yet

- Chapter 1: Production and Operation Management Self Assessment QuestionsDocument31 pagesChapter 1: Production and Operation Management Self Assessment QuestionsJasonSpringNo ratings yet

- When Things Impoverish An Approach To Marx S Analysis of Capitalism in Conjunction With Heidegger S Concern Over TechnologyDocument20 pagesWhen Things Impoverish An Approach To Marx S Analysis of Capitalism in Conjunction With Heidegger S Concern Over TechnologyDiego MartinezNo ratings yet

- THE EFFECT OF PROMOTION ON CONSUMER BASED BRAND EQUITY AN EMPIRICAL STUDY ON ETHIOPIAN INSURANCE INDUSTRY AAU Comerce (Marketing Dept)Document85 pagesTHE EFFECT OF PROMOTION ON CONSUMER BASED BRAND EQUITY AN EMPIRICAL STUDY ON ETHIOPIAN INSURANCE INDUSTRY AAU Comerce (Marketing Dept)Henok TesfayeNo ratings yet

- Grad Project Final SubmissionDocument25 pagesGrad Project Final SubmissionDina AlfawalNo ratings yet

- Demkt503 Marketing ManagementDocument238 pagesDemkt503 Marketing ManagementPriya NaharNo ratings yet

- Advanced PricingDocument59 pagesAdvanced PricingVarun Rao Yegnam100% (3)

- Pricing Strategy - AssignmentDocument19 pagesPricing Strategy - AssignmentHitesh PatniNo ratings yet

- WWW - Ecoholics.in: Largest Platform For EconomicsDocument22 pagesWWW - Ecoholics.in: Largest Platform For EconomicsjegeNo ratings yet

- Understanding Market Capitalization Versus Market ValueDocument8 pagesUnderstanding Market Capitalization Versus Market ValuejunNo ratings yet

- Cost-Benefit Analysis PPT FinalDocument26 pagesCost-Benefit Analysis PPT FinalShashikantShigwan100% (1)

- Chapter 01Document12 pagesChapter 01Dianne BallonNo ratings yet

- Methods of ValuationDocument53 pagesMethods of ValuationAmit SinghNo ratings yet

- Define Marketing and Describe Marketing Process.: AnswerDocument6 pagesDefine Marketing and Describe Marketing Process.: AnswerNishan HamalNo ratings yet

- Exam OpmanDocument4 pagesExam OpmanCarla ValenciaNo ratings yet

- M-301 PROJECT MANAGEMENT Segment I Basic Concept, Project Life CycleDocument21 pagesM-301 PROJECT MANAGEMENT Segment I Basic Concept, Project Life CycleAjay Singh Rathore100% (1)

- The Big Market DelusionDocument38 pagesThe Big Market DelusionsarpbNo ratings yet

- Contingent Valuation Method (CVM) For Urban RestorationDocument9 pagesContingent Valuation Method (CVM) For Urban RestorationΟδυσσεας ΚοψιδαςNo ratings yet

Download as pdf or txt

You might also like

- Principles of AccountingDocument657 pagesPrinciples of AccountingKhalid Aziz89% (107)

- Ambilikile Book 2-1 PDFDocument181 pagesAmbilikile Book 2-1 PDFplanet tz50% (6)

- Chapter-2 Public Finance by Pratham Singh PDFDocument13 pagesChapter-2 Public Finance by Pratham Singh PDFLavanya Tanwar100% (1)

- Valucon ReviewerDocument12 pagesValucon ReviewerAnjo Salonga del Rosario100% (4)

- ECONOMICS - Guided Reading and Study GuideDocument308 pagesECONOMICS - Guided Reading and Study GuideThorng Meng76% (21)

- Customs Valuation V2Document91 pagesCustoms Valuation V2natan makuNo ratings yet

- The Managerial Revolution - James Burnham (1941)Document235 pagesThe Managerial Revolution - James Burnham (1941)topbudget60% (5)

- Is LM ModelDocument3 pagesIs LM ModelAaquib AhmadNo ratings yet

- 12 Economics Balance of Payment Impq 1Document2 pages12 Economics Balance of Payment Impq 1RitikaNo ratings yet

- Is-LM Open EconomyDocument16 pagesIs-LM Open EconomyAppan Kandala VasudevacharyNo ratings yet

- Lectures 4 and 5 Modern Trade TheoriesDocument33 pagesLectures 4 and 5 Modern Trade TheoriesChenxi LiuNo ratings yet

- Concept of Money SupplyDocument7 pagesConcept of Money SupplyMD. IBRAHIM KHOLILULLAHNo ratings yet

- Ch. 4 Demand For MoneyDocument13 pagesCh. 4 Demand For Moneycoldpassion100% (1)

- STUDY MATERIAL ON Profit and Theories of Profit.Document63 pagesSTUDY MATERIAL ON Profit and Theories of Profit.Aparna ViswakumarNo ratings yet

- Supply - Class 11Document43 pagesSupply - Class 11bittomolla691No ratings yet

- NCERT Solutions For Class 12th Microeconomics - Chapter 3 - Production and Costs - AglaSem SchoolsDocument12 pagesNCERT Solutions For Class 12th Microeconomics - Chapter 3 - Production and Costs - AglaSem SchoolsNiranjan MishraNo ratings yet

- Grade - 11 Micro Economics Ch:03 Demand IDocument14 pagesGrade - 11 Micro Economics Ch:03 Demand IShubham GoelNo ratings yet

- Consumption FunctionDocument15 pagesConsumption FunctionAkshat MishraNo ratings yet

- Revised Tobin's Demand For MoneyDocument4 pagesRevised Tobin's Demand For MoneySnehasish MahataNo ratings yet

- Theory of Income and EmploymentDocument9 pagesTheory of Income and EmploymentsureshNo ratings yet

- Equilibrium Income and Output: Two-Sector Economy Y C+IDocument52 pagesEquilibrium Income and Output: Two-Sector Economy Y C+ISunu 3670100% (1)

- Producer's EquilibriumDocument19 pagesProducer's EquilibriumTejas ModiNo ratings yet

- Money & BankingDocument33 pagesMoney & BankingGeeta GhaiNo ratings yet

- Producer Equilibrium/Least Cost Combination: AssumptionsDocument5 pagesProducer Equilibrium/Least Cost Combination: AssumptionsJessy SinghNo ratings yet

- Submitted By: Biki Das Class - XI Stream - Commerce Roll No. - 5Document42 pagesSubmitted By: Biki Das Class - XI Stream - Commerce Roll No. - 5Biki DasNo ratings yet

- Namma Kalvi Economics Unit 5 Surya Economics Guide emDocument31 pagesNamma Kalvi Economics Unit 5 Surya Economics Guide emAakaash C.K.No ratings yet

- Cardinal Utility AnalysisDocument19 pagesCardinal Utility AnalysisShah MominNo ratings yet

- Economics NotesDocument71 pagesEconomics NotesUmer PrinceNo ratings yet

- ElasticityDocument25 pagesElasticityaljohn anticristoNo ratings yet

- Credit Creation in Commercial BanksDocument12 pagesCredit Creation in Commercial BanksprasanthmctNo ratings yet

- Crowding OutDocument3 pagesCrowding OutsattysattuNo ratings yet

- Producer's Equilibrium: Total Revenue & Total Cost ApproachDocument12 pagesProducer's Equilibrium: Total Revenue & Total Cost ApproachSarim KhanNo ratings yet

- Lecture Notes IS LM CurveDocument13 pagesLecture Notes IS LM CurvemNo ratings yet

- IB Econ Chap 16 Macro EQDocument11 pagesIB Econ Chap 16 Macro EQsweetlunaticNo ratings yet

- The IS-LM Model: Equilibrium: Goods and Money Markets Understanding Public PolicyDocument37 pagesThe IS-LM Model: Equilibrium: Goods and Money Markets Understanding Public PolicyShashank Shekhar SinghNo ratings yet

- Harrod Model of GrowthDocument6 pagesHarrod Model of Growthvikram inamdarNo ratings yet

- Monetary Policy: Monetary Policy Mechanism Objectives of Monetary Policy Tools of Monetary PolicyDocument20 pagesMonetary Policy: Monetary Policy Mechanism Objectives of Monetary Policy Tools of Monetary Policysuga29No ratings yet

- Mundell FlemingDocument40 pagesMundell FlemingAnkita Singhai100% (1)

- DemandDocument22 pagesDemandSerenity Kerr100% (1)

- Market EquilibriumDocument38 pagesMarket EquilibriumAbhi KumNo ratings yet

- Eco Dev - OrendayDocument17 pagesEco Dev - OrendayZhaira OrendayNo ratings yet

- Determinants of Investment: - Investment in Economics Means Addition ToDocument22 pagesDeterminants of Investment: - Investment in Economics Means Addition ToASHISHRD100% (1)

- Managerial Economics AssignmentDocument17 pagesManagerial Economics AssignmentDeepshikha Gupta50% (2)

- Macro Econom I eDocument9 pagesMacro Econom I eguy3hil8927No ratings yet

- 1.2 National Income Accounting PDFDocument24 pages1.2 National Income Accounting PDFdivya90% (10)

- Consumption Function and Its TypesDocument13 pagesConsumption Function and Its TypesTashiTamangNo ratings yet

- Baumol Inventory Theory - Amitabha SarkarDocument3 pagesBaumol Inventory Theory - Amitabha SarkarTripti Dutta100% (1)

- 2.theory of Demand and Supply.Document30 pages2.theory of Demand and Supply.punte77100% (1)

- Economics Case StudyDocument2 pagesEconomics Case StudyKUSH SHAH100% (1)

- Fiscal and Monetary Policies of IndiaDocument13 pagesFiscal and Monetary Policies of IndiaRidhika GuptaNo ratings yet

- Laws of ReturnDocument8 pagesLaws of ReturnSparsh MalhotraNo ratings yet

- Lec3 Harrod-Domar GrowthDocument17 pagesLec3 Harrod-Domar GrowthMehul GargNo ratings yet

- Extension and ContractionDocument5 pagesExtension and ContractionMonika Shekhawat100% (1)

- Classical Theory of Ecomomics 1Document46 pagesClassical Theory of Ecomomics 1Shireen YakubNo ratings yet

- Elasticity of DemandDocument17 pagesElasticity of DemandDental Sloss100% (1)

- Business Economics FYBComDocument3 pagesBusiness Economics FYBCompravin963No ratings yet

- Functions of MoneyDocument17 pagesFunctions of MoneyAnonymous ytZsBOVNo ratings yet

- Indian Economy 1950 1990Document8 pagesIndian Economy 1950 1990arpit9964100% (1)

- National Income Accounting PPT at MBADocument58 pagesNational Income Accounting PPT at MBABabasab Patil (Karrisatte)No ratings yet

- Unit 1-Fundamentals of EconomicsDocument35 pagesUnit 1-Fundamentals of EconomicsAyush SatyamNo ratings yet

- Macro-Economics Lecture (BBA)Document262 pagesMacro-Economics Lecture (BBA)Sahil NoorzaiNo ratings yet

- Production Possibility CurvesDocument6 pagesProduction Possibility CurvesFari AliNo ratings yet

- Balance of PaymentDocument9 pagesBalance of PaymentMuskanNo ratings yet

- IME WS 23 24 Problemset 01Document2 pagesIME WS 23 24 Problemset 01salih.durmusNo ratings yet

- University of Chicago Press Is Collaborating With JSTOR To Digitize, Preserve and Extend Access To Journal of Political EconomyDocument11 pagesUniversity of Chicago Press Is Collaborating With JSTOR To Digitize, Preserve and Extend Access To Journal of Political EconomyEdgar Diaz NietoNo ratings yet

- Mint Cash WhitepaperDocument40 pagesMint Cash Whitepaperyankees leeNo ratings yet

- Date Sheet PDFDocument1 pageDate Sheet PDFKhalid AzizNo ratings yet

- B-Com GP 1 2018 FinalDocument10 pagesB-Com GP 1 2018 FinalKhalid AzizNo ratings yet

- Cir CBE March 2017Document1 pageCir CBE March 2017Khalid AzizNo ratings yet

- Chapter 19 Operations and Value Chain Management: True/False QuestionsDocument33 pagesChapter 19 Operations and Value Chain Management: True/False QuestionsWaseem KambohNo ratings yet

- Final Test Advanced Accounting B-COM Part 2: Sir Khalid AzizDocument6 pagesFinal Test Advanced Accounting B-COM Part 2: Sir Khalid AzizKhalid AzizNo ratings yet

- Feb 2018 AnsDocument7 pagesFeb 2018 AnsKhalid AzizNo ratings yet

- Macro Economics NotesDocument18 pagesMacro Economics NotesKhalid Aziz100% (1)

- Guess Papers BY Sir Khalid Aziz: Iqra Commerce NetworkDocument14 pagesGuess Papers BY Sir Khalid Aziz: Iqra Commerce NetworkAnonymous NKjJIpNo ratings yet

- Marks Question No. 2 (A) (I) Conditions Need To Fulfill To Get A Licence: 05Document8 pagesMarks Question No. 2 (A) (I) Conditions Need To Fulfill To Get A Licence: 05Khalid AzizNo ratings yet

- B-Com GP 1Document10 pagesB-Com GP 1Khalid AzizNo ratings yet

- Guess Papers BY Sir Khalid Aziz: Iqra Commerce NetworkDocument14 pagesGuess Papers BY Sir Khalid Aziz: Iqra Commerce NetworkAnonymous NKjJIpNo ratings yet

- First Division Seat Nos:: University of Karachi Karachi (Examinations Department)Document5 pagesFirst Division Seat Nos:: University of Karachi Karachi (Examinations Department)Khalid AzizNo ratings yet

- Sir Khalid Aziz: According To New SyllabusDocument1 pageSir Khalid Aziz: According To New SyllabusKhalid AzizNo ratings yet

- q2 Half Yearly Financial Report Fifth Draft August 2015 PDFDocument26 pagesq2 Half Yearly Financial Report Fifth Draft August 2015 PDFKhalid AzizNo ratings yet

- Institute of Cost and Management Accountants of Pakistan: Assignment Questions - (Fall - 2013 Session)Document4 pagesInstitute of Cost and Management Accountants of Pakistan: Assignment Questions - (Fall - 2013 Session)Khalid AzizNo ratings yet

- Economics Mcqs Kit PDFDocument241 pagesEconomics Mcqs Kit PDFKhalid AzizNo ratings yet

- What Are The Main Problems of Agriculture SectorDocument4 pagesWhat Are The Main Problems of Agriculture SectorKhalid AzizNo ratings yet

- M.A. (Previous) External, Annual Examination 2014.Document2 pagesM.A. (Previous) External, Annual Examination 2014.Khalid AzizNo ratings yet

- Factory Overhead Idle Capacity VarianceDocument4 pagesFactory Overhead Idle Capacity VarianceKhalid Aziz100% (1)

- LL.B. PART - I, Annual Examination 2015.Document3 pagesLL.B. PART - I, Annual Examination 2015.Khalid AzizNo ratings yet

- MA Eco SyllabusDocument27 pagesMA Eco SyllabusRana AsimNo ratings yet

- Issue of SharesDocument20 pagesIssue of SharesKhalid AzizNo ratings yet

- Schumpeter ModelDocument5 pagesSchumpeter ModelKhalid Aziz100% (1)

- ClosingDocument1 pageClosingKhalid AzizNo ratings yet

- S.S.C. Part II General (Regular & Private) Group Results 2015Document106 pagesS.S.C. Part II General (Regular & Private) Group Results 2015Khalid AzizNo ratings yet

- Central BankingDocument22 pagesCentral BankingKhalid AzizNo ratings yet

- Semester - II, Subject - Sociology, Roll No. - 31, Name - Anand SinghDocument24 pagesSemester - II, Subject - Sociology, Roll No. - 31, Name - Anand SinghAnand SinghNo ratings yet

- 11 Economics sp01Document14 pages11 Economics sp01DËV DÃSNo ratings yet

- Grossman 1972 Health CapitalDocument33 pagesGrossman 1972 Health CapitalLeonardo SimonciniNo ratings yet

- Value AnalysisDocument6 pagesValue AnalysisAMIYA KUMAR SAMALNo ratings yet

- ABM B GROUP 1 Business PlanDocument142 pagesABM B GROUP 1 Business PlanGwen Ashley Dela PenaNo ratings yet

- Basic Appraisal For Real Estate BrokersDocument4 pagesBasic Appraisal For Real Estate Brokersbea100% (1)

- Eliot S Insight The Future of Urban DesignDocument5 pagesEliot S Insight The Future of Urban DesignPrudhvi Nagasaikumar RaviNo ratings yet

- Classical EconomicsDocument54 pagesClassical EconomicsAlionie FreyNo ratings yet

- Chapter 1: Production and Operation Management Self Assessment QuestionsDocument31 pagesChapter 1: Production and Operation Management Self Assessment QuestionsJasonSpringNo ratings yet

- When Things Impoverish An Approach To Marx S Analysis of Capitalism in Conjunction With Heidegger S Concern Over TechnologyDocument20 pagesWhen Things Impoverish An Approach To Marx S Analysis of Capitalism in Conjunction With Heidegger S Concern Over TechnologyDiego MartinezNo ratings yet

- THE EFFECT OF PROMOTION ON CONSUMER BASED BRAND EQUITY AN EMPIRICAL STUDY ON ETHIOPIAN INSURANCE INDUSTRY AAU Comerce (Marketing Dept)Document85 pagesTHE EFFECT OF PROMOTION ON CONSUMER BASED BRAND EQUITY AN EMPIRICAL STUDY ON ETHIOPIAN INSURANCE INDUSTRY AAU Comerce (Marketing Dept)Henok TesfayeNo ratings yet

- Grad Project Final SubmissionDocument25 pagesGrad Project Final SubmissionDina AlfawalNo ratings yet

- Demkt503 Marketing ManagementDocument238 pagesDemkt503 Marketing ManagementPriya NaharNo ratings yet

- Advanced PricingDocument59 pagesAdvanced PricingVarun Rao Yegnam100% (3)

- Pricing Strategy - AssignmentDocument19 pagesPricing Strategy - AssignmentHitesh PatniNo ratings yet

- WWW - Ecoholics.in: Largest Platform For EconomicsDocument22 pagesWWW - Ecoholics.in: Largest Platform For EconomicsjegeNo ratings yet

- Understanding Market Capitalization Versus Market ValueDocument8 pagesUnderstanding Market Capitalization Versus Market ValuejunNo ratings yet

- Cost-Benefit Analysis PPT FinalDocument26 pagesCost-Benefit Analysis PPT FinalShashikantShigwan100% (1)

- Chapter 01Document12 pagesChapter 01Dianne BallonNo ratings yet

- Methods of ValuationDocument53 pagesMethods of ValuationAmit SinghNo ratings yet

- Define Marketing and Describe Marketing Process.: AnswerDocument6 pagesDefine Marketing and Describe Marketing Process.: AnswerNishan HamalNo ratings yet

- Exam OpmanDocument4 pagesExam OpmanCarla ValenciaNo ratings yet

- M-301 PROJECT MANAGEMENT Segment I Basic Concept, Project Life CycleDocument21 pagesM-301 PROJECT MANAGEMENT Segment I Basic Concept, Project Life CycleAjay Singh Rathore100% (1)

- The Big Market DelusionDocument38 pagesThe Big Market DelusionsarpbNo ratings yet

- Contingent Valuation Method (CVM) For Urban RestorationDocument9 pagesContingent Valuation Method (CVM) For Urban RestorationΟδυσσεας ΚοψιδαςNo ratings yet