Download as pdf or txt

You might also like

- The Little Book of Behavioral Investing by James Montier - Novel InvestorDocument11 pagesThe Little Book of Behavioral Investing by James Montier - Novel InvestorkkblrNo ratings yet

- Isgpore PDFDocument16 pagesIsgpore PDFGabriel La MottaNo ratings yet

- Investment Management: The Wisco TeamDocument4 pagesInvestment Management: The Wisco TeamGreg SchroederNo ratings yet

- ING Global Real Estate FundDocument3 pagesING Global Real Estate FundManoj V ReddyNo ratings yet

- 3Q12 Wisco Client LetterDocument4 pages3Q12 Wisco Client LetterGreg SchroederNo ratings yet

- Weekly Market Commentary 11/18/2013Document3 pagesWeekly Market Commentary 11/18/2013monarchadvisorygroupNo ratings yet

- Weekly Market Commentary 6-24-13Document3 pagesWeekly Market Commentary 6-24-13Stephen GierlNo ratings yet

- Q 12011 QuarterlyDocument4 pagesQ 12011 QuarterlyedoneyNo ratings yet

- 4Q 2015 Market CommentaryDocument3 pages4Q 2015 Market CommentaryAnonymous Ht0MIJNo ratings yet

- Spotlight Key Themes For Uk Real Estate 2016Document6 pagesSpotlight Key Themes For Uk Real Estate 2016mannantawaNo ratings yet

- Kovitz Newsletter 2016-12-31Document18 pagesKovitz Newsletter 2016-12-31superinvestorbulletiNo ratings yet

- Empower February 2017Document104 pagesEmpower February 2017Arjun BhatnagarNo ratings yet

- Investment Management: The Wisco TeamDocument4 pagesInvestment Management: The Wisco TeamGreg SchroederNo ratings yet

- Wisco Team: Third QuarterDocument4 pagesWisco Team: Third QuarterGreg SchroederNo ratings yet

- Market Commentary 1.28.2013Document3 pagesMarket Commentary 1.28.2013CLORIS4No ratings yet

- March Madness: Update - Spring 2017Document3 pagesMarch Madness: Update - Spring 2017Amin KhakianiNo ratings yet

- Tracking The World Economy... - 05/10/2010Document2 pagesTracking The World Economy... - 05/10/2010Rhb InvestNo ratings yet

- AnalyinDocument4 pagesAnalyinCarissa PalomoNo ratings yet

- Brookfield Asset Management - "Real Assets, The New Essential"Document23 pagesBrookfield Asset Management - "Real Assets, The New Essential"Equicapita Income TrustNo ratings yet

- 2019 Investment OutlookDocument22 pages2019 Investment OutlookAnonymous HsoXPyNo ratings yet

- JLL Real Estate As A Global Asset ClassDocument9 pagesJLL Real Estate As A Global Asset Classashraf187100% (1)

- Weekly Market Commentary 3-18-13Document3 pagesWeekly Market Commentary 3-18-13Stephen GierlNo ratings yet

- Bumps On The SlopeDocument2 pagesBumps On The SlopeJanet BarrNo ratings yet

- II Considering Brexit 07072016Document4 pagesII Considering Brexit 07072016ranjan1491No ratings yet

- Investor Letter 2013 Q3 PDFDocument4 pagesInvestor Letter 2013 Q3 PDFdpbasicNo ratings yet

- Global Market Perspective q3 2016Document43 pagesGlobal Market Perspective q3 2016iguhstwNo ratings yet

- Weekly Market Commentary 3-19-2012Document4 pagesWeekly Market Commentary 3-19-2012monarchadvisorygroupNo ratings yet

- Tilson - t2 Annual LetterDocument27 pagesTilson - t2 Annual Lettermwolcott4No ratings yet

- Q3 - 2015 Commentary: 5.1% and 10.3%, RespectivelyDocument5 pagesQ3 - 2015 Commentary: 5.1% and 10.3%, RespectivelyJohn MathiasNo ratings yet

- GSAM 2010: Year in ReviewDocument6 pagesGSAM 2010: Year in Reviewed_nycNo ratings yet

- Fourth Quarter Items For Consideration: Global Monetary Policy EffectivenessDocument9 pagesFourth Quarter Items For Consideration: Global Monetary Policy EffectivenessClay Ulman, CFP®No ratings yet

- Oceanus Growth Fund 2023 Year-End LetterDocument12 pagesOceanus Growth Fund 2023 Year-End LetterKan ZhouNo ratings yet

- Weekly Market Commentary: Two and ADocument2 pagesWeekly Market Commentary: Two and Aapi-234126528No ratings yet

- Lombard - O - CIO Office Viewpoint - Ten Investment Convictions - 2023.06.26 - ENDocument6 pagesLombard - O - CIO Office Viewpoint - Ten Investment Convictions - 2023.06.26 - ENblkjack8No ratings yet

- GIC On The MarketsDocument18 pagesGIC On The MarketsDD97No ratings yet

- Sector Strategies: U.S. TreasuriesDocument5 pagesSector Strategies: U.S. TreasuriesAbe MartinNo ratings yet

- The Monarch Report 1/22/2013Document3 pagesThe Monarch Report 1/22/2013monarchadvisorygroupNo ratings yet

- Fall 2016 Investor LetterDocument4 pagesFall 2016 Investor LetterAnonymous Ht0MIJNo ratings yet

- Investment Management: The Wisco TeamDocument4 pagesInvestment Management: The Wisco TeamGreg SchroederNo ratings yet

- Goldman - July 25Document27 pagesGoldman - July 25Xavier Strauss100% (2)

- JP Morgan Global Research 8 Dec 2023 2024 Year Ahe 240116 152842Document71 pagesJP Morgan Global Research 8 Dec 2023 2024 Year Ahe 240116 152842ruri tandiansyahNo ratings yet

- Bond Market PerspectivesDocument5 pagesBond Market PerspectivesdpbasicNo ratings yet

- Lane Asset Management Market Commentary For Q3 2017Document15 pagesLane Asset Management Market Commentary For Q3 2017Edward C LaneNo ratings yet

- Bam 2012 q2 LTR To ShareholdersDocument7 pagesBam 2012 q2 LTR To ShareholdersDan-S. ErmicioiNo ratings yet

- 2Q12 Wisco Client LetterDocument4 pages2Q12 Wisco Client LetterGreg SchroederNo ratings yet

- Weekly Market Commentary 3/18/2013Document4 pagesWeekly Market Commentary 3/18/2013monarchadvisorygroupNo ratings yet

- Weekly Commentary January 22, 2013: The MarketsDocument4 pagesWeekly Commentary January 22, 2013: The MarketsStephen GierlNo ratings yet

- Investment Management: The Wisco TeamDocument4 pagesInvestment Management: The Wisco TeamGreg SchroederNo ratings yet

- WPDocument DisplayDocument2 pagesWPDocument Displaytanner7552No ratings yet

- Best Ideas Financials Traditional - Jonathan Casteleyn, AnalystDocument14 pagesBest Ideas Financials Traditional - Jonathan Casteleyn, AnalystJonathanNo ratings yet

- Real Estate Outlook Global Edition March 2023Document6 pagesReal Estate Outlook Global Edition March 2023Saif MonajedNo ratings yet

- GF Letter 09-30-16 FinalDocument4 pagesGF Letter 09-30-16 FinalAnonymous Feglbx5No ratings yet

- AIA Quarterly Investment InsightsDocument10 pagesAIA Quarterly Investment InsightsdesmondNo ratings yet

- Ulman Financial Fourth Quarter Newsletter - 2018-10Document8 pagesUlman Financial Fourth Quarter Newsletter - 2018-10Clay Ulman, CFP®No ratings yet

- Asia Maxima (Delirium) - 3Q14 20140703Document100 pagesAsia Maxima (Delirium) - 3Q14 20140703Hans WidjajaNo ratings yet

- BlackRock Midyear Investment Outlook 2014Document8 pagesBlackRock Midyear Investment Outlook 2014w24nyNo ratings yet

- Monetary Policy Summary and Minutes of The Monetary Policy Committee Meeting Ending On 6 February 2019Document13 pagesMonetary Policy Summary and Minutes of The Monetary Policy Committee Meeting Ending On 6 February 2019leseNo ratings yet

- Weeklymarket: UpdateDocument2 pagesWeeklymarket: Updateapi-94222682No ratings yet

- Asia Pacific Vision Q4 2012 ABRIDGEDDocument32 pagesAsia Pacific Vision Q4 2012 ABRIDGEDKw LohNo ratings yet

- Q1 2015 Market Review & Outlook: in BriefDocument3 pagesQ1 2015 Market Review & Outlook: in Briefapi-284581037No ratings yet

- China Credit Spotlight: The Lending Landscape Is Shifting For Property DevelopersDocument7 pagesChina Credit Spotlight: The Lending Landscape Is Shifting For Property Developersapi-227433089No ratings yet

- 2015: Outlook for Stocks, Bonds, Commodities, Currencies and Real EstateFrom Everand2015: Outlook for Stocks, Bonds, Commodities, Currencies and Real EstateNo ratings yet

- Commercial Property Tax Appeal ServicesDocument7 pagesCommercial Property Tax Appeal ServicescutmytaxesNo ratings yet

- Property Tax Consultants & Their RulesDocument7 pagesProperty Tax Consultants & Their RulescutmytaxesNo ratings yet

- Are Your Property Taxes Too HighDocument8 pagesAre Your Property Taxes Too HighcutmytaxesNo ratings yet

- What Is Business Personal Property TaxDocument7 pagesWhat Is Business Personal Property TaxcutmytaxesNo ratings yet

- Tips To Win A Property Tax ProtestDocument7 pagesTips To Win A Property Tax ProtestcutmytaxesNo ratings yet

- Texans, Fight Property Tax Increase Amidst COVID 19!Document7 pagesTexans, Fight Property Tax Increase Amidst COVID 19!cutmytaxesNo ratings yet

- Property Appeal Protest ServicesDocument7 pagesProperty Appeal Protest ServicescutmytaxesNo ratings yet

- Property Tax in Texas - Research Report 2017Document12 pagesProperty Tax in Texas - Research Report 2017cutmytaxesNo ratings yet

- Top 10 Property Tax TipsDocument7 pagesTop 10 Property Tax TipscutmytaxesNo ratings yet

- Property Tax Deferral Disabled Senior CitizensDocument16 pagesProperty Tax Deferral Disabled Senior CitizenscutmytaxesNo ratings yet

- Udget: H C A DDocument49 pagesUdget: H C A DO'Connor AssociateNo ratings yet

- HFF Investment OverviewDocument4 pagesHFF Investment OverviewcutmytaxesNo ratings yet

- Property Tax Bills 2017Document16 pagesProperty Tax Bills 2017cutmytaxesNo ratings yet

- BREAStrategicPlan PDFDocument16 pagesBREAStrategicPlan PDFcutmytaxesNo ratings yet

- Real Estate Education Course CatalogDocument81 pagesReal Estate Education Course CatalogcutmytaxesNo ratings yet

- Week 2 Requirement: Name: Puray, Ma. Lorraine M - Course: BSA-1 Class Schedule: M-F (7:00-8:50 Am)Document10 pagesWeek 2 Requirement: Name: Puray, Ma. Lorraine M - Course: BSA-1 Class Schedule: M-F (7:00-8:50 Am)Lorraine Millama PurayNo ratings yet

- Chapter - 7: Case/Source Based Questions:: Kvs Ziet Bhubaneswar 12/10/2021Document18 pagesChapter - 7: Case/Source Based Questions:: Kvs Ziet Bhubaneswar 12/10/2021abiNo ratings yet

- Re & BVDocument3 pagesRe & BV-100% (1)

- Ule 504/small Company Offering Registration ("SCOR")Document7 pagesUle 504/small Company Offering Registration ("SCOR")Douglas SlainNo ratings yet

- FMG Africa Fund - PresentationDocument9 pagesFMG Africa Fund - Presentationkalle4133No ratings yet

- Ratio Analysis - CEAT Tyres LTDDocument18 pagesRatio Analysis - CEAT Tyres LTDagrawal.ace911450% (2)

- CH 16Document11 pagesCH 16Fahad Javaid50% (2)

- REG CPA - Entity Basis IssuesDocument2 pagesREG CPA - Entity Basis IssuesManny MarroquinNo ratings yet

- The Investing Secrets Of: ISA MillionairesDocument6 pagesThe Investing Secrets Of: ISA MillionairesRamNo ratings yet

- Financial Market TextBook (Dragged) 3Document1 pageFinancial Market TextBook (Dragged) 3Nick OoiNo ratings yet

- Bu040815 PDFDocument86 pagesBu040815 PDFNikita JoshiNo ratings yet

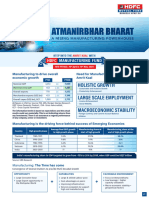

- NFO Leaflet - HDFC Manufacturing Fund - 240422 - 142358Document2 pagesNFO Leaflet - HDFC Manufacturing Fund - 240422 - 142358bitsthechampNo ratings yet

- Measuring Bank Risk - An Exploration of Z-Score PDFDocument38 pagesMeasuring Bank Risk - An Exploration of Z-Score PDFsisayNo ratings yet

- MERISTEM Breweries Sector Update 10 June 2010Document24 pagesMERISTEM Breweries Sector Update 10 June 2010Rasaq Muhammed AbiolaNo ratings yet

- Understanding Faq Rule 144a Equity OfferingsDocument12 pagesUnderstanding Faq Rule 144a Equity OfferingskcetconsultingNo ratings yet

- Solution Ipa Week 1 Chapter 3Document47 pagesSolution Ipa Week 1 Chapter 3Aura MaghfiraNo ratings yet

- Financial Analysis On Easyjet and Iag 15 17Document51 pagesFinancial Analysis On Easyjet and Iag 15 17Suraxya GurungNo ratings yet

- Introduction To Brokerage IndustryDocument13 pagesIntroduction To Brokerage Industryapriti29No ratings yet

- A Study On Financial Analysis of Tri Van Drum AirportDocument81 pagesA Study On Financial Analysis of Tri Van Drum AirportN.MUTHUKUMARAN100% (1)

- Introduction Investment PlanningDocument5 pagesIntroduction Investment Planningapi-3770163No ratings yet

- MSC Financial Economics Dissertation TopicsDocument8 pagesMSC Financial Economics Dissertation TopicsCheapestPaperWritingServiceSingapore100% (1)

- BL.2802 Drill 1 - Corporation MAY 2020: Business Law Atty. Ong/LopezDocument2 pagesBL.2802 Drill 1 - Corporation MAY 2020: Business Law Atty. Ong/LopezMaeNo ratings yet

- Documentary Stamp TaxDocument19 pagesDocumentary Stamp TaxFiliusdeiNo ratings yet

- Kami Export - The Rights of Stock Holders Activity Sheet 2Document1 pageKami Export - The Rights of Stock Holders Activity Sheet 2Sama NazimiNo ratings yet

- Indian Real Estate Opening Doors PDFDocument18 pagesIndian Real Estate Opening Doors PDFkoolyogesh1No ratings yet

- A Study On Investment Portfolio PDFDocument127 pagesA Study On Investment Portfolio PDFBijaya DhakalNo ratings yet

- Bear Put Spread: Montréal ExchangeDocument2 pagesBear Put Spread: Montréal ExchangepkkothariNo ratings yet

- Business ValuationDocument5 pagesBusiness Valuationvaibhavi DhordaNo ratings yet