Download as pdf or txt

You might also like

- Chandana & Ambar Ghosh - Keynesian Macroeconomics Beyond The ISLM ModelDocument263 pagesChandana & Ambar Ghosh - Keynesian Macroeconomics Beyond The ISLM ModelShaurya Singru100% (1)

- Bond Prices and Interest RatesDocument27 pagesBond Prices and Interest RatesKoyakuNo ratings yet

- Financial E Chapter TwoDocument25 pagesFinancial E Chapter TwoGenemo FitalaNo ratings yet

- Chapter 3 Interest RateDocument15 pagesChapter 3 Interest RateEhab HosnyNo ratings yet

- Chapter 4. Present and Future ValueDocument43 pagesChapter 4. Present and Future ValueGirmay AbrhaNo ratings yet

- Managerial Finance chp5Document13 pagesManagerial Finance chp5Linda Mohammad FarajNo ratings yet

- Chapter 2: How Interest Rates Are DeterminedDocument62 pagesChapter 2: How Interest Rates Are DeterminedAykaNo ratings yet

- Issues in Corporate Finance: ValuationDocument52 pagesIssues in Corporate Finance: ValuationMD Hafizul Islam HafizNo ratings yet

- Lecture 7 9Document106 pagesLecture 7 9Nguyễn Thúy KiềuNo ratings yet

- BFW2140 Lecture Week 2: Corporate Financial Mathematics IDocument33 pagesBFW2140 Lecture Week 2: Corporate Financial Mathematics Iaa TANNo ratings yet

- Lecture 2Document21 pagesLecture 2Samantha YuNo ratings yet

- FINA2010 Financial Management: Lecture 3: Time Value of MoneyDocument62 pagesFINA2010 Financial Management: Lecture 3: Time Value of MoneymoonNo ratings yet

- FE Review - EconomyDocument26 pagesFE Review - EconomylonerstarNo ratings yet

- Time Value of Money - TVMDocument21 pagesTime Value of Money - TVMTh'bo Muzorewa ChizyukaNo ratings yet

- Time Value of MoneyDocument78 pagesTime Value of Moneyneha_baid_167% (3)

- Chapter 3 FMDocument79 pagesChapter 3 FMHananNo ratings yet

- Chapter 4 FinalDocument139 pagesChapter 4 FinaltomyidosaNo ratings yet

- Engineeringeconomics1 180421045801Document19 pagesEngineeringeconomics1 180421045801vielleshantelleNo ratings yet

- Financial Markets QuestionsDocument54 pagesFinancial Markets QuestionsMathias VindalNo ratings yet

- Valuation of Cash Flows: Chapter 3.1-3.3Document66 pagesValuation of Cash Flows: Chapter 3.1-3.3harshnvicky123No ratings yet

- Fidelia Agatha - 2106715765 - Summary & Problem MK - Pertemuan Ke-4Document12 pagesFidelia Agatha - 2106715765 - Summary & Problem MK - Pertemuan Ke-4Fidelia AgathaNo ratings yet

- Introduction To Time Value of MoneyDocument45 pagesIntroduction To Time Value of MoneyAnkit DwivediNo ratings yet

- Lecture 3 - Time Value of MoneyDocument22 pagesLecture 3 - Time Value of MoneyJason LuximonNo ratings yet

- Midterm RevisionDocument27 pagesMidterm RevisionTrang CaoNo ratings yet

- Engineering Economics CH 2Document81 pagesEngineering Economics CH 2karim kobeissiNo ratings yet

- Module 2Document60 pagesModule 2lizNo ratings yet

- Intuition Behind The Present Value RuleDocument34 pagesIntuition Behind The Present Value RuleAbhishek MishraNo ratings yet

- Strategic Capital Group Workshop #4: Bond ValuationDocument29 pagesStrategic Capital Group Workshop #4: Bond ValuationUniversity Securities Investment TeamNo ratings yet

- FM Chapter 06 1Document25 pagesFM Chapter 06 1shadmanakash101No ratings yet

- L3 Future Value, Present Value & Compund InterestDocument5 pagesL3 Future Value, Present Value & Compund InterestvivianNo ratings yet

- InvLecture - W10-11 Capital BudgettingDocument264 pagesInvLecture - W10-11 Capital BudgettingJuan Camilo Gómez RobayoNo ratings yet

- L1 Fixed Income Markets (v2)Document44 pagesL1 Fixed Income Markets (v2)Kruti BhattNo ratings yet

- Bond FundamentalsDocument19 pagesBond FundamentalsInstiRevenNo ratings yet

- Time Value of MoneyDocument73 pagesTime Value of MoneyZeenat NoorNo ratings yet

- Exercises For Revision With SolutionDocument4 pagesExercises For Revision With SolutionThùy LinhhNo ratings yet

- Engineering Economics Lect 2Document31 pagesEngineering Economics Lect 2Furqan ChaudhryNo ratings yet

- The Time Value of MoneyDocument39 pagesThe Time Value of MoneyAbhinav JainNo ratings yet

- Fixed IncomeDocument36 pagesFixed IncomeAnkit ShahNo ratings yet

- Techniques of Asset/liability Management: Futures, Options, and SwapsDocument43 pagesTechniques of Asset/liability Management: Futures, Options, and SwapsSushmita BarlaNo ratings yet

- 2023 Time Value of MoneyDocument81 pages2023 Time Value of Moneylynthehunkyapple205No ratings yet

- Time Value of Money-PowerpointDocument83 pagesTime Value of Money-Powerpointhaljordan313No ratings yet

- Principles of Managerial Finance: Time Value of MoneyDocument45 pagesPrinciples of Managerial Finance: Time Value of MoneyJoshNo ratings yet

- The Keynesian System (Money, Interest and Income)Document59 pagesThe Keynesian System (Money, Interest and Income)Almas100% (1)

- CFDocument11 pagesCFPreetesh ChoudhariNo ratings yet

- 7.2 Bond ValuationDocument59 pages7.2 Bond ValuationAlperen KaragozNo ratings yet

- Lecture 02dm Time Value of MoneyDocument42 pagesLecture 02dm Time Value of Moneylja92No ratings yet

- CF - 04Document54 pagesCF - 04Нндн Н'No ratings yet

- Lecture 4 PostDocument29 pagesLecture 4 PostSamantha YuNo ratings yet

- Time Value of MoneyDocument60 pagesTime Value of MoneyZain AbbasNo ratings yet

- Power Notes: Bonds Payable and Investments in BondsDocument38 pagesPower Notes: Bonds Payable and Investments in BondsiVONo ratings yet

- Understanding Interest RatesDocument19 pagesUnderstanding Interest RatesAmsalu WalelignNo ratings yet

- The Concepts of Return and Value-Explained-PppDocument48 pagesThe Concepts of Return and Value-Explained-PppJcharlesvNo ratings yet

- Bonds and Their ValuationDocument41 pagesBonds and Their ValuationRenz Ian DeeNo ratings yet

- Time Value of MoneyDocument47 pagesTime Value of MoneyPrashant JhakarwarNo ratings yet

- WK13-14 Valuation and Rates of ReturnDocument49 pagesWK13-14 Valuation and Rates of ReturnJAEZAR PHILIP GRAGASINNo ratings yet

- Engineering Economics Lect 3Document43 pagesEngineering Economics Lect 3Furqan ChaudhryNo ratings yet

- Compound Interest, Future Value, and Present Value: - When Money Is Borrowed, The Amount Borrowed Is Known As TheDocument41 pagesCompound Interest, Future Value, and Present Value: - When Money Is Borrowed, The Amount Borrowed Is Known As ThetwinklenoorNo ratings yet

- Timevalueofmoney 160502121318Document30 pagesTimevalueofmoney 160502121318S BALAJI VH10788No ratings yet

- Chapter 6 NotesDocument6 pagesChapter 6 NoteshannahandrearosarioNo ratings yet

- Econ Course 202 Academy SayDocument909 pagesEcon Course 202 Academy SayKoyakuNo ratings yet

- Example Example: (5.5) : Continuation of (5.4)Document22 pagesExample Example: (5.5) : Continuation of (5.4)KoyakuNo ratings yet

- Current Labor MarketDocument42 pagesCurrent Labor MarketKoyakuNo ratings yet

- Wage Determination: Collective BargainingDocument46 pagesWage Determination: Collective BargainingKoyakuNo ratings yet

- Shifts of The Curve: Price Level Money Supply ExogenousDocument28 pagesShifts of The Curve: Price Level Money Supply ExogenousKoyakuNo ratings yet

- Investment and The Stock Market: Stock Capital Same Same StockDocument32 pagesInvestment and The Stock Market: Stock Capital Same Same StockKoyakuNo ratings yet

- Determination of The Optimal Capital InvestmentDocument34 pagesDetermination of The Optimal Capital InvestmentKoyakuNo ratings yet

- Consumption: Disposable IncomeDocument49 pagesConsumption: Disposable IncomeKoyakuNo ratings yet

- Learning ObjectivesDocument33 pagesLearning ObjectivesKoyakuNo ratings yet

- Market For Goods in The Classical Model: Lower Discourages EncouragesDocument28 pagesMarket For Goods in The Classical Model: Lower Discourages EncouragesKoyakuNo ratings yet

- Money Demand Function: Increase Increases Reduces Increase Increases Reduces One For OneDocument30 pagesMoney Demand Function: Increase Increases Reduces Increase Increases Reduces One For OneKoyakuNo ratings yet

- Bond Prices and Interest RatesDocument27 pagesBond Prices and Interest RatesKoyakuNo ratings yet

- Money: Assets PaymentDocument25 pagesMoney: Assets PaymentKoyakuNo ratings yet

- The Government Sector: - Income Taxes and Automatic StabilizersDocument44 pagesThe Government Sector: - Income Taxes and Automatic StabilizersKoyakuNo ratings yet

- Saving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantDocument29 pagesSaving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantKoyakuNo ratings yet

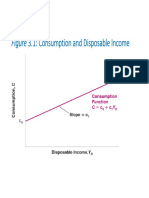

- Figure 3.1: Consumption and Disposable IncomeDocument33 pagesFigure 3.1: Consumption and Disposable IncomeKoyakuNo ratings yet

- Borrowing Constraints: - SameDocument29 pagesBorrowing Constraints: - SameKoyakuNo ratings yet

- The Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeDocument33 pagesThe Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeKoyakuNo ratings yet

- Requirements For The Management of Liquidity Risk 28 June 2006 Regulatory Document For Credit Institutions From The Financial RegulatorDocument42 pagesRequirements For The Management of Liquidity Risk 28 June 2006 Regulatory Document For Credit Institutions From The Financial RegulatorMark MaloneNo ratings yet

- Banking Thesis PDFDocument6 pagesBanking Thesis PDFMary Montoya100% (2)

- JLL Colombo Property Market Monitor 4q20Document12 pagesJLL Colombo Property Market Monitor 4q20jatin girotraNo ratings yet

- Makerere University: Business SchoolDocument5 pagesMakerere University: Business SchoolKobutungi ClaireNo ratings yet

- Richard Werner - Secrets of Banking Trade 2014Document59 pagesRichard Werner - Secrets of Banking Trade 2014TREND_7425100% (1)

- Forex FlashcardsDocument63 pagesForex Flashcardssting74100% (2)

- Princ Ch29 Presentation7eDocument41 pagesPrinc Ch29 Presentation7eAbhishek M SNo ratings yet

- Banking Digests 02Document21 pagesBanking Digests 02Rin KNo ratings yet

- An Empirical Analysis of Balance of Payment in Ghana Using The Monetary ApproachDocument11 pagesAn Empirical Analysis of Balance of Payment in Ghana Using The Monetary ApproachAlexander DeckerNo ratings yet

- Liberalised Remittance Scheme (LRS)Document20 pagesLiberalised Remittance Scheme (LRS)Ramachandran PskNo ratings yet

- Commercial Banks, FI and NBIFDocument17 pagesCommercial Banks, FI and NBIFVikash kumarNo ratings yet

- The Only Game in Town Central Banks Instability and Avoiding The Next CollapseDocument3 pagesThe Only Game in Town Central Banks Instability and Avoiding The Next CollapsedanarasmussenNo ratings yet

- Financial Stability AssignmentDocument4 pagesFinancial Stability AssignmentSanjok Kc UnitedforeverNo ratings yet

- CBSE Class 12 Economics Question Paper 2019 PDFDocument21 pagesCBSE Class 12 Economics Question Paper 2019 PDFVaishali AggarwalNo ratings yet

- MCQs Chapters 156 - The Monetary PolicyDocument40 pagesMCQs Chapters 156 - The Monetary PolicyLộc TrầnNo ratings yet

- Philippine Money - MicsDocument9 pagesPhilippine Money - MicsMichaela VillanuevaNo ratings yet

- A Rothschild Plan For World GovernmentDocument6 pagesA Rothschild Plan For World GovernmentJason LambNo ratings yet

- Bnppre Forecast - h2 21Document30 pagesBnppre Forecast - h2 21RomeroNo ratings yet

- News Trading Forex StrategyDocument13 pagesNews Trading Forex StrategyRadical Ntuk100% (3)

- Banking and Financial Sector Implications of Covid-19 - Preparedness of Banks in BangladeshDocument34 pagesBanking and Financial Sector Implications of Covid-19 - Preparedness of Banks in BangladeshFaysal Haque100% (1)

- Eco120g4 Group 2 Written Report AssignmentDocument23 pagesEco120g4 Group 2 Written Report AssignmentDylan JoshuaNo ratings yet

- Ecb TargetDocument59 pagesEcb TargetSönke AhrensNo ratings yet

- INVESTMENT POLICY OF COMMERCIAL GLOBAL IME BANK LTDDocument35 pagesINVESTMENT POLICY OF COMMERCIAL GLOBAL IME BANK LTDNa Ge ShNo ratings yet

- Small and Medium Enterprises in Egypt: New Facts From A New DatasetDocument21 pagesSmall and Medium Enterprises in Egypt: New Facts From A New DatasetMohamed AbdelhamidNo ratings yet

- JOHN HAY PEOPLE'S ALTERNATIVE COALITION v. LIM, GR 119775 (2003)Document13 pagesJOHN HAY PEOPLE'S ALTERNATIVE COALITION v. LIM, GR 119775 (2003)JMae MagatNo ratings yet

- Did Hayek and Robbins Deepen The Great Depression 2008Document19 pagesDid Hayek and Robbins Deepen The Great Depression 2008profkaplanNo ratings yet

- Functions of RbiDocument4 pagesFunctions of RbiMunish PathaniaNo ratings yet

- BDNG 3103Document11 pagesBDNG 3103prithinahNo ratings yet

- Tche 303 - Money and Banking Tutorial 9Document3 pagesTche 303 - Money and Banking Tutorial 9Phương Anh TrầnNo ratings yet