Download as pdf or txt

You might also like

- Pre Finals Exam MathDocument17 pagesPre Finals Exam MathJohn Michael Cañero Maon100% (2)

- Assignment AnswerDocument13 pagesAssignment AnswerEisha-Nea Gumbahali100% (4)

- The Time Value of Money - Business FinanceDocument24 pagesThe Time Value of Money - Business FinanceMd. Ruhul- Amin33% (3)

- Summary Of "Principles Of Economics" By Alfred Marshall: UNIVERSITY SUMMARIESFrom EverandSummary Of "Principles Of Economics" By Alfred Marshall: UNIVERSITY SUMMARIESNo ratings yet

- Do It Yourself Credit Repair KitDocument77 pagesDo It Yourself Credit Repair Kitmajmikey100% (3)

- RB CAGMAT REVIEW Macroeconomics Reviewer - Yet Sample QuestionsDocument35 pagesRB CAGMAT REVIEW Macroeconomics Reviewer - Yet Sample QuestionsSylveth Novah Badal Denzo100% (1)

- Final Exam ReviewDocument47 pagesFinal Exam ReviewMelissa NagyNo ratings yet

- Sec 30-50 (Negotiation)Document10 pagesSec 30-50 (Negotiation)Arvin Glen BeltranNo ratings yet

- CH 8Document2 pagesCH 8Abbas Ali100% (6)

- Consumer Choice TheoryDocument59 pagesConsumer Choice TheoryVatandeep SinghNo ratings yet

- Intro Eco CH 3Document39 pagesIntro Eco CH 3Old mamas funny videoNo ratings yet

- Consumer Choice and Demand DecisionsDocument40 pagesConsumer Choice and Demand DecisionsNelly OdehNo ratings yet

- Chapter One Microeconomics For Business StudentsDocument32 pagesChapter One Microeconomics For Business StudentsBirhanu AberaNo ratings yet

- Economics Chap 3Document37 pagesEconomics Chap 3Temesgen workiyeNo ratings yet

- Microconomics 1Document146 pagesMicroconomics 1soretimohammed25No ratings yet

- Review of The Previous LectureDocument21 pagesReview of The Previous LectureMuhammad Usman AshrafNo ratings yet

- Distinguish Between Cardinal and Ordinal Approach To Explain The ConsumerDocument10 pagesDistinguish Between Cardinal and Ordinal Approach To Explain The ConsumerPoonam ThapaNo ratings yet

- Utility AnalysisDocument105 pagesUtility Analysisadib.shawpno.20No ratings yet

- Introductin To Economics AAUDocument42 pagesIntroductin To Economics AAUOnlyucan SteadymeNo ratings yet

- ECN 201 Principles of MicroeconomicsDocument17 pagesECN 201 Principles of MicroeconomicsZonayed HasanNo ratings yet

- Indifference Curve Analysis PDFDocument24 pagesIndifference Curve Analysis PDFArpita BanerjeeNo ratings yet

- Ordinal ApproachDocument39 pagesOrdinal ApproachStephan Mpundu (T4 enick)No ratings yet

- CH 3 Consumer BehaviorDocument37 pagesCH 3 Consumer BehaviorEstifanos DefaruNo ratings yet

- Topic 3Document28 pagesTopic 3TanNo ratings yet

- Unit 3 Grade 11Document38 pagesUnit 3 Grade 11Breket WonberaNo ratings yet

- Chapter ThreeDocument69 pagesChapter Threedream of lifesNo ratings yet

- Consumer Preferences and Choice & Consumer's EquilibriumDocument25 pagesConsumer Preferences and Choice & Consumer's EquilibriumAtul KashyapNo ratings yet

- Unit 4.2Document56 pagesUnit 4.2unstopable 7 rodiesNo ratings yet

- Ordinal Utility TheoryDocument20 pagesOrdinal Utility TheoryJagdish BhattNo ratings yet

- Saving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantDocument29 pagesSaving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantKoyakuNo ratings yet

- 03 Demand TheoryDocument32 pages03 Demand TheoryscribdwithyouNo ratings yet

- Unit 2 - Theory of Consumer Behaviour - Part 4Document10 pagesUnit 2 - Theory of Consumer Behaviour - Part 4kinnarieNo ratings yet

- Micro Economics 1Document39 pagesMicro Economics 1Mahek JainNo ratings yet

- Economics 2Document35 pagesEconomics 2singhpkk1966No ratings yet

- Economics Project 3rd SemesterDocument17 pagesEconomics Project 3rd SemestersahilNo ratings yet

- Lower SixthDocument25 pagesLower Sixthtaona madanhireNo ratings yet

- UNIT-II - Ordinal ApproachDocument27 pagesUNIT-II - Ordinal ApproachSuhaniNo ratings yet

- 7.2 - Indifference Curves and Budget LinesDocument28 pages7.2 - Indifference Curves and Budget LinesccsmithNo ratings yet

- Consumer BehaviorDocument15 pagesConsumer BehaviorSamia RasheedNo ratings yet

- Consumer Behaviour (Water-Diamond Theory)Document31 pagesConsumer Behaviour (Water-Diamond Theory)Mikaela Villaluna0% (1)

- Operational StructureDocument41 pagesOperational Structurecaptainsultan01No ratings yet

- Consumers EquilibriumDocument8 pagesConsumers EquilibriumananthanvaikomNo ratings yet

- Consumer TheoryDocument49 pagesConsumer TheoryScribdTranslationsNo ratings yet

- Topic 2 20151Document10 pagesTopic 2 20151shandil7No ratings yet

- Ind. Curve and BL Term 3Document31 pagesInd. Curve and BL Term 3richmonfNo ratings yet

- Consumer Behavior Theory - 1Document56 pagesConsumer Behavior Theory - 1Danny MgenyandaNo ratings yet

- Theory of EconomicsDocument63 pagesTheory of EconomicsSachin GirohNo ratings yet

- Analysis of Consumer Behaviour-Indifference Curves TechniqueDocument31 pagesAnalysis of Consumer Behaviour-Indifference Curves Techniquemohammed junaidNo ratings yet

- Consumer BehaviorDocument15 pagesConsumer BehaviorSaurabhGuptaNo ratings yet

- ZMJCF SL80 CDocument11 pagesZMJCF SL80 CbilalNo ratings yet

- Chapter Three EconomicsDocument36 pagesChapter Three Economicsnigusu deguNo ratings yet

- Some Concepts of EconomicsDocument105 pagesSome Concepts of EconomicsdeepakkavaNo ratings yet

- Indifference CurveDocument14 pagesIndifference Curverajeevbhandari82@gmail.comNo ratings yet

- Demand and Supply: Multiple Choice QuestionsDocument74 pagesDemand and Supply: Multiple Choice QuestionsTanisha ShahNo ratings yet

- ConsumptionDocument19 pagesConsumptionjimkagz6No ratings yet

- Indifference Curve EditedDocument18 pagesIndifference Curve Editedameeshapanwar1No ratings yet

- Consumer Choice: Indifference Theory: Lipsey & Chrystal Economics 12EDocument59 pagesConsumer Choice: Indifference Theory: Lipsey & Chrystal Economics 12EtatendaNo ratings yet

- CONSUMER EQ (Ordinal)Document6 pagesCONSUMER EQ (Ordinal)PranshuNo ratings yet

- Introduction To Economics - Chapter 3Document34 pagesIntroduction To Economics - Chapter 3Eyosi SoleNo ratings yet

- Chapter ThreeDocument53 pagesChapter ThreeshimelisNo ratings yet

- Consumer Behaviour - Unit 3Document59 pagesConsumer Behaviour - Unit 3Regal GandharvNo ratings yet

- Consumer Preferences and ChoiceDocument37 pagesConsumer Preferences and ChoiceAjay KumarNo ratings yet

- Consumer Choice TheoryDocument20 pagesConsumer Choice TheoryItti SinghNo ratings yet

- EEM Module IDocument95 pagesEEM Module INishant NNo ratings yet

- Arbaminch University: Arbaminch Institute of TechnologyDocument11 pagesArbaminch University: Arbaminch Institute of Technologyyohannisyohannis54No ratings yet

- Consumer ChoiceDocument41 pagesConsumer ChoiceGabriel Alexander BingeiNo ratings yet

- Principles of Economics 3Document34 pagesPrinciples of Economics 3reda gadNo ratings yet

- Econ Course 202 Academy SayDocument909 pagesEcon Course 202 Academy SayKoyakuNo ratings yet

- Example Example: (5.5) : Continuation of (5.4)Document22 pagesExample Example: (5.5) : Continuation of (5.4)KoyakuNo ratings yet

- Current Labor MarketDocument42 pagesCurrent Labor MarketKoyakuNo ratings yet

- Wage Determination: Collective BargainingDocument46 pagesWage Determination: Collective BargainingKoyakuNo ratings yet

- Shifts of The Curve: Price Level Money Supply ExogenousDocument28 pagesShifts of The Curve: Price Level Money Supply ExogenousKoyakuNo ratings yet

- Investment and The Stock Market: Stock Capital Same Same StockDocument32 pagesInvestment and The Stock Market: Stock Capital Same Same StockKoyakuNo ratings yet

- Determination of The Optimal Capital InvestmentDocument34 pagesDetermination of The Optimal Capital InvestmentKoyakuNo ratings yet

- Monetary Policy and Open Market OperationsDocument37 pagesMonetary Policy and Open Market OperationsKoyakuNo ratings yet

- Learning ObjectivesDocument33 pagesLearning ObjectivesKoyakuNo ratings yet

- Market For Goods in The Classical Model: Lower Discourages EncouragesDocument28 pagesMarket For Goods in The Classical Model: Lower Discourages EncouragesKoyakuNo ratings yet

- Money Demand Function: Increase Increases Reduces Increase Increases Reduces One For OneDocument30 pagesMoney Demand Function: Increase Increases Reduces Increase Increases Reduces One For OneKoyakuNo ratings yet

- Bond Prices and Interest RatesDocument27 pagesBond Prices and Interest RatesKoyakuNo ratings yet

- Money: Assets PaymentDocument25 pagesMoney: Assets PaymentKoyakuNo ratings yet

- The Government Sector: - Income Taxes and Automatic StabilizersDocument44 pagesThe Government Sector: - Income Taxes and Automatic StabilizersKoyakuNo ratings yet

- Saving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantDocument29 pagesSaving and Wealth Over The Life Cycle: Income High Low Short Long Together Constant ConstantKoyakuNo ratings yet

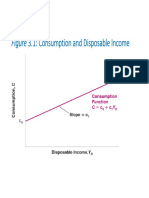

- Figure 3.1: Consumption and Disposable IncomeDocument33 pagesFigure 3.1: Consumption and Disposable IncomeKoyakuNo ratings yet

- Borrowing Constraints: - SameDocument29 pagesBorrowing Constraints: - SameKoyakuNo ratings yet

- The Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeDocument33 pagesThe Determination of Equilibrium Output in A Graph: Building Output Fiscal Policy Income Production Equal IncomeKoyakuNo ratings yet

- ReportDocument122 pagesReportPrasanjeetNo ratings yet

- Tai Tong Chuache & Co. v. Insurance CommissionDocument1 pageTai Tong Chuache & Co. v. Insurance CommissionmastaacaNo ratings yet

- Fast Formula For Education Loan - Oracle HRMSDocument7 pagesFast Formula For Education Loan - Oracle HRMSAravind AlavantharNo ratings yet

- MONEY AND CREDIT Worksheet - 1639023786Document11 pagesMONEY AND CREDIT Worksheet - 1639023786pratimaNo ratings yet

- Migration New 2015 PDFDocument2 pagesMigration New 2015 PDFJohnMactavishPalmerNo ratings yet

- 5 The Expenditure CycleDocument28 pages5 The Expenditure CycleEris GilNo ratings yet

- Capitec Case StudyDocument6 pagesCapitec Case StudyMpho SeutloaliNo ratings yet

- Debits and Credits - Bad DebtDocument25 pagesDebits and Credits - Bad DebtRevilyn Grace Bangayan100% (1)

- Legal Disclosure - Fannie MaeDocument16 pagesLegal Disclosure - Fannie MaeDUTCH551400No ratings yet

- Analysis of Liquidity, Solvency, Credit Policy For Fu-Wang Food Ltd.Document27 pagesAnalysis of Liquidity, Solvency, Credit Policy For Fu-Wang Food Ltd.Imam Iqramul Hasan 1420493030No ratings yet

- Unknown PDFDocument2 pagesUnknown PDFMadalina MadaNo ratings yet

- Final KEC ReportDocument116 pagesFinal KEC Reports2410100% (4)

- ACCT504 Case Study 1 The Complete Accounting Cycle-13Document12 pagesACCT504 Case Study 1 The Complete Accounting Cycle-13Mohammad Islam100% (1)

- Problem StatementDocument7 pagesProblem StatementViệt Vi VuNo ratings yet

- Credit Rating Report On Pinaki Garments LimitedDocument1 pageCredit Rating Report On Pinaki Garments LimitedNishita AkterNo ratings yet

- Communication PolicyDocument8 pagesCommunication PolicykarltennramNo ratings yet

- Quick Credit Reference Guide (DC17 - )Document12 pagesQuick Credit Reference Guide (DC17 - )Horace0% (1)

- Local Economic Enterprise and Non-Traditional Revenue SourcesDocument57 pagesLocal Economic Enterprise and Non-Traditional Revenue SourcesGlyzel SaplaNo ratings yet

- HOW DOES ASSET-BACKED CREDIT-LINKED NOTES (CLN) WORKS - Keval ShahDocument5 pagesHOW DOES ASSET-BACKED CREDIT-LINKED NOTES (CLN) WORKS - Keval ShahKeval ShahNo ratings yet

- Latih Soal Untuk Mhs Fin MGTDocument13 pagesLatih Soal Untuk Mhs Fin MGTnajNo ratings yet

- GL Codes Used by PosDocument18 pagesGL Codes Used by PosGanesh KiranNo ratings yet

- Harry Gibson v. First Federal Savings and Loan Association of Detroit, 504 F.2d 826, 1st Cir. (1974)Document5 pagesHarry Gibson v. First Federal Savings and Loan Association of Detroit, 504 F.2d 826, 1st Cir. (1974)Scribd Government DocsNo ratings yet