Download as pdf or txt

You might also like

- Solution Manual For Auditing A Risk Based Approach 11th Edition Karla M Johnstone Zehms Audrey A Gramling Larry e Rittenberg 2Document37 pagesSolution Manual For Auditing A Risk Based Approach 11th Edition Karla M Johnstone Zehms Audrey A Gramling Larry e Rittenberg 2MeredithFleminggztay100% (92)

- Seth Klarman Baupost Group LettersDocument58 pagesSeth Klarman Baupost Group LettersAndr Ei100% (4)

- Transcription Hub TestDocument3 pagesTranscription Hub TestMonaliza SequigNo ratings yet

- Hertz Write UpDocument5 pagesHertz Write UpAnna Lin100% (1)

- Current Year ($) Forecasted For Next Year ($) Book Value of Debt 50 50 Market Value of Debt 62Document9 pagesCurrent Year ($) Forecasted For Next Year ($) Book Value of Debt 50 50 Market Value of Debt 62Joel Christian MascariñaNo ratings yet

- Mark Yusko LetterDocument43 pagesMark Yusko LetterValueWalk100% (2)

- Greenlight Capital Letter (1-Oct-08)Document0 pagesGreenlight Capital Letter (1-Oct-08)brunomarz12345No ratings yet

- Booth Laird Q1 2015 LetterDocument14 pagesBooth Laird Q1 2015 LetterCanadianValue100% (1)

- Snowy Ridge Ski ResortDocument13 pagesSnowy Ridge Ski Resortgandhunk100% (1)

- IapmDocument129 pagesIapmKomal BagrodiaNo ratings yet

- FREE, 9-17-22 Weekend Metals ReportDocument16 pagesFREE, 9-17-22 Weekend Metals ReportMarco BourdonNo ratings yet

- Basic Points 2007Document455 pagesBasic Points 2007bschwartzieNo ratings yet

- Sprott - GoldDocument4 pagesSprott - Goldvariantperception100% (1)

- LTR To Investors Jan 11Document6 pagesLTR To Investors Jan 11the_knowledge_pileNo ratings yet

- Arlington Value 2014 Annual Letter PDFDocument8 pagesArlington Value 2014 Annual Letter PDFChrisNo ratings yet

- Distressed Debt InvestingDocument5 pagesDistressed Debt Investingjt322No ratings yet

- FAM Funds 2020 Annual LetterDocument9 pagesFAM Funds 2020 Annual LetterYog MehtaNo ratings yet

- Crossroads Capital 2019 Annual FINALDocument31 pagesCrossroads Capital 2019 Annual FINALYog MehtaNo ratings yet

- Investment Strategy: Turning Point?Document5 pagesInvestment Strategy: Turning Point?marketfolly.comNo ratings yet

- The Years 1999/2000 Were A Time of ExtremesDocument9 pagesThe Years 1999/2000 Were A Time of ExtremesAlbert L. PeiaNo ratings yet

- Insider Weekly 20161120Document8 pagesInsider Weekly 20161120alikarimiak1347No ratings yet

- Fig Gold Man 120611 Final2Document27 pagesFig Gold Man 120611 Final2aadricapitalNo ratings yet

- Booyah To Ya Executive SummaryDocument5 pagesBooyah To Ya Executive SummarySpearFinanceNo ratings yet

- Friedberg 3Q ReportDocument16 pagesFriedberg 3Q Reportrichardck61No ratings yet

- Gold: Still A Rodney Dangerfield AssetDocument4 pagesGold: Still A Rodney Dangerfield AssetadikhannaNo ratings yet

- 2 Grand Central Tower - 140 East 45 Street, 24 Floor - New York, NY 10017 Phone: 212-973-1900Document6 pages2 Grand Central Tower - 140 East 45 Street, 24 Floor - New York, NY 10017 Phone: 212-973-1900Yui ChuNo ratings yet

- Gold Ex Plainer September 19 2010Document6 pagesGold Ex Plainer September 19 2010Radu LucaNo ratings yet

- Cerberus LetterDocument5 pagesCerberus Letterakiva80100% (1)

- GreenlightDocument6 pagesGreenlightaugustaboundNo ratings yet

- The Broyhill Letter: Executive SummaryDocument3 pagesThe Broyhill Letter: Executive SummaryBroyhill Asset ManagementNo ratings yet

- Insight: Investing in CrisisDocument3 pagesInsight: Investing in Crisisvouzvouz7127No ratings yet

- IceCap Global Market OutlookDocument16 pagesIceCap Global Market OutlookZerohedge100% (2)

- December 31, 2000Document3 pagesDecember 31, 2000grrarrNo ratings yet

- FPA Crescent Qtrly Commentary 0911Document4 pagesFPA Crescent Qtrly Commentary 0911James HouNo ratings yet

- Diamonds Amidst RubbleDocument4 pagesDiamonds Amidst RubbleTim PriceNo ratings yet

- Boyar's Intrinsic Value Research Forgotten FourtyDocument49 pagesBoyar's Intrinsic Value Research Forgotten FourtyValueWalk100% (1)

- Amalthea Fund: Investors' Letter For July 2013Document4 pagesAmalthea Fund: Investors' Letter For July 2013BongNo ratings yet

- The Broyhill Letter: Executive SummaryDocument4 pagesThe Broyhill Letter: Executive SummaryBroyhill Asset ManagementNo ratings yet

- EconomyDocument9 pagesEconomytiru.bollam765No ratings yet

- Warren Buffet Investing WisdomDocument15 pagesWarren Buffet Investing Wisdomroy_kohinoorNo ratings yet

- Akre Capital Management, LLC: Second Quarter 2010Document4 pagesAkre Capital Management, LLC: Second Quarter 2010eric695No ratings yet

- Selector September 2007 Quarterly NewsletterDocument12 pagesSelector September 2007 Quarterly Newsletterapi-237451731No ratings yet

- Inflated Treasuries and Deflated StockholdersDocument4 pagesInflated Treasuries and Deflated Stockholdersarbbee4095305No ratings yet

- January 3, 2011 PostsDocument168 pagesJanuary 3, 2011 PostsAlbert L. PeiaNo ratings yet

- Letter To Our Co Investors 2Q20Document26 pagesLetter To Our Co Investors 2Q20Andy HuffNo ratings yet

- Corona Associates Capital Management, LLC - Q1 2019 Invesment Letter-4!29!19Document4 pagesCorona Associates Capital Management, LLC - Q1 2019 Invesment Letter-4!29!19Julian ScurciNo ratings yet

- 2014 4th Q Call With DI Transcript FINAL PDFDocument14 pages2014 4th Q Call With DI Transcript FINAL PDFJohn Hadriano Mellon FundNo ratings yet

- Corona Associates Capital Management, LLC - August 2019 Investment LetterDocument6 pagesCorona Associates Capital Management, LLC - August 2019 Investment LetterJulian ScurciNo ratings yet

- Coho Capital 2020 Q4 LetterDocument11 pagesCoho Capital 2020 Q4 LetterEast CoastNo ratings yet

- TranscriptDocument4 pagesTranscriptMuhammad Saleh Masaud80% (5)

- Special Report Year Ahead 121609Document5 pagesSpecial Report Year Ahead 121609ejlamasNo ratings yet

- Tami Q2 2011Document9 pagesTami Q2 2011fstreetNo ratings yet

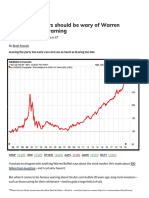

- Opinion:: Investors Should Be Wary of Warren Buffett's Crash WarningDocument5 pagesOpinion:: Investors Should Be Wary of Warren Buffett's Crash WarningNayeem RajaNo ratings yet

- UntitledDocument1 pageUntitledapi-74004141No ratings yet

- Once in A Blue Moon Sentiment and BreadthDocument7 pagesOnce in A Blue Moon Sentiment and BreadthJuan CalfunNo ratings yet

- January, 2021: The Moment Has PassedDocument7 pagesJanuary, 2021: The Moment Has Passedl chanNo ratings yet

- Once Bullish, Contrarian Jim Grant Likes Cash Now: AdchoicesDocument4 pagesOnce Bullish, Contrarian Jim Grant Likes Cash Now: AdchoicesBrandywine84No ratings yet

- What Will Happen If Dollar CollapsedDocument7 pagesWhat Will Happen If Dollar CollapsedMoneyShifuNo ratings yet

- C CC CCCDocument7 pagesC CC CCCKelvingrove Partners, LLCNo ratings yet

- This Time Is Different - Novel InvestorDocument9 pagesThis Time Is Different - Novel InvestorGSNo ratings yet

- Seth Klarman CFA Presentation PDFDocument11 pagesSeth Klarman CFA Presentation PDFRam Narayanan100% (1)

- Position Yourself for the Next Bull Market: Financial Freedom, #104From EverandPosition Yourself for the Next Bull Market: Financial Freedom, #104No ratings yet

- Second Chance: How to Make and Keep Big Money from the Coming Gold and Silver Shock - WaveFrom EverandSecond Chance: How to Make and Keep Big Money from the Coming Gold and Silver Shock - WaveNo ratings yet

- Givingpresentations PDFDocument15 pagesGivingpresentations PDFvolkan_kaya1798No ratings yet

- 10winning StrategiesDocument45 pages10winning Strategiesvolkan_kaya1798No ratings yet

- 10winning StrategiesDocument45 pages10winning Strategiesvolkan_kaya1798No ratings yet

- Memory Model 1 0 PRD SpecDocument43 pagesMemory Model 1 0 PRD Specvolkan_kaya1798No ratings yet

- Chap.5 FINANCIAL ASSET ValuationDocument39 pagesChap.5 FINANCIAL ASSET ValuationJeanette FormenteraNo ratings yet

- CBO Oil and Gas White Paper - The Billion US$ Oil Business + 2013 Marginal Fields Sale Special Report + Full Oil Sector ValuationDocument96 pagesCBO Oil and Gas White Paper - The Billion US$ Oil Business + 2013 Marginal Fields Sale Special Report + Full Oil Sector ValuationD. AtanuNo ratings yet

- Seminar Topics of AuditingDocument2 pagesSeminar Topics of AuditingNIDHIN RAJNo ratings yet

- Critique Paper Bdo - Far4Document9 pagesCritique Paper Bdo - Far4John Jet TanNo ratings yet

- Financial AccountingDocument944 pagesFinancial Accountingsivachandirang695492% (24)

- Evolution of AccountingDocument5 pagesEvolution of AccountingCHRISTINE ELAINE TOLENTINONo ratings yet

- Letter To CoJ Integrity Commissioner (GOOD) Commercial Property RatesDocument2 pagesLetter To CoJ Integrity Commissioner (GOOD) Commercial Property RatesCameron J ArendseNo ratings yet

- May 2011 Strategic Financial ManagementDocument10 pagesMay 2011 Strategic Financial ManagementchandreshNo ratings yet

- Written By: Unknown: Yardsticks To Value Stocks in Different SectorsDocument5 pagesWritten By: Unknown: Yardsticks To Value Stocks in Different SectorsKrs_Rs_4407No ratings yet

- Chapter 12 PPT - Holthausen & Zmijewski 2019Document140 pagesChapter 12 PPT - Holthausen & Zmijewski 2019royNo ratings yet

- Valuation of StartupsDocument28 pagesValuation of StartupsSahil JoshiNo ratings yet

- Valuing Dot ComsDocument11 pagesValuing Dot ComsEchuOkan1No ratings yet

- CenvatDocument10 pagesCenvatincometaxreckonerNo ratings yet

- University of Cambridge International Examinations General Certificate of Education Ordinary LevelDocument16 pagesUniversity of Cambridge International Examinations General Certificate of Education Ordinary Levelmeelas123No ratings yet

- International Corporate Finance: Value Creation With Currency Derivatives in Global Capital Markets Second Edition. Edition JacqueDocument43 pagesInternational Corporate Finance: Value Creation With Currency Derivatives in Global Capital Markets Second Edition. Edition Jacquerobert.hacker681100% (7)

- Syllabus of B - Vocational (BPO)Document34 pagesSyllabus of B - Vocational (BPO)Algean JabagatonNo ratings yet

- Chapter Nineteen: The Analysis of Credit RiskDocument4 pagesChapter Nineteen: The Analysis of Credit RiskHarsh SaxenaNo ratings yet

- Sap MM Interview Questions by Team Tagskills - : 1. What MRP Procedures Are Available in MM-CBP?Document13 pagesSap MM Interview Questions by Team Tagskills - : 1. What MRP Procedures Are Available in MM-CBP?VASEEMNo ratings yet

- Corporate Valuation - Lesson and Session PlanDocument4 pagesCorporate Valuation - Lesson and Session PlansumandirancspNo ratings yet

- Facebook IPO Case Study: Group Project - Investment BankingDocument18 pagesFacebook IPO Case Study: Group Project - Investment BankingLakshmi SrinivasanNo ratings yet

- ChipotleDocument22 pagesChipotleChen JinghanNo ratings yet

- How To Invest - Raamdeo AgrawalDocument31 pagesHow To Invest - Raamdeo AgrawalAshwinNo ratings yet

- Chrysaor Holdings LTD PDFDocument107 pagesChrysaor Holdings LTD PDFSohini ChatterjeeNo ratings yet

- Hind. UnileverDocument37 pagesHind. UnileveradasdasNo ratings yet

- 2022 10 20 PH S CNVRGDocument7 pages2022 10 20 PH S CNVRGValiente RandzNo ratings yet