M09 Soln8117 06 SM C09

M09 Soln8117 06 SM C09

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Answer PDFDocument17 pagesAnswer PDFميلاد نوروزي رهبرNo ratings yet

- Chapter 8: Risk and ReturnDocument56 pagesChapter 8: Risk and ReturnMohamed HussienNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Multiple Choice Questions Subject: Accountancy Class: XiDocument4 pagesMultiple Choice Questions Subject: Accountancy Class: XiShahid NaikNo ratings yet

- Always Trust The Customer How Zara Has Revolutionized The Fashion Industry and Become A Worldwide LeaderDocument27 pagesAlways Trust The Customer How Zara Has Revolutionized The Fashion Industry and Become A Worldwide LeaderbeatriceNo ratings yet

- Black-Litterman Portfolio Allocation Stability and Financial Performance With MGARCH-M Derived ViewsDocument65 pagesBlack-Litterman Portfolio Allocation Stability and Financial Performance With MGARCH-M Derived ViewsMohamed HussienNo ratings yet

- Introduction & Research: Factor InvestingDocument44 pagesIntroduction & Research: Factor InvestingMohamed HussienNo ratings yet

- TN1 Basic Pre-Calculus: AcronymsDocument11 pagesTN1 Basic Pre-Calculus: AcronymsMohamed HussienNo ratings yet

- TN 2 - Basic Calculus With Financial Applications: 1 Functions and LimitsDocument16 pagesTN 2 - Basic Calculus With Financial Applications: 1 Functions and LimitsMohamed HussienNo ratings yet

- The Dark Side of Passive Investing: White PaperDocument11 pagesThe Dark Side of Passive Investing: White PaperMohamed HussienNo ratings yet

- Index Smart BetaDocument44 pagesIndex Smart BetaMohamed HussienNo ratings yet

- Giorgio S. Questa Induction To Quantitative Methods in FinanceDocument2 pagesGiorgio S. Questa Induction To Quantitative Methods in FinanceMohamed HussienNo ratings yet

- From Smart Beta To Hard Reality: Executive SummaryDocument8 pagesFrom Smart Beta To Hard Reality: Executive SummaryMohamed Hussien100% (1)

- Transportation Methods PDFDocument24 pagesTransportation Methods PDFMohamed Hussien100% (1)

- Factor Model Notes:: R α β f β f …+β f ϵ R α β ' f ϵDocument2 pagesFactor Model Notes:: R α β f β f …+β f ϵ R α β ' f ϵMohamed HussienNo ratings yet

- Week 1 NotesDocument72 pagesWeek 1 NotesMohamed HussienNo ratings yet

- PerformanceAnalytics PDFDocument214 pagesPerformanceAnalytics PDFMohamed HussienNo ratings yet

- Probability Distribution and Statistics: Key Points of LearningDocument24 pagesProbability Distribution and Statistics: Key Points of LearningMohamed HussienNo ratings yet

- The Efficient Market Theory and Evidence Implications For Active Investment Management PDFDocument93 pagesThe Efficient Market Theory and Evidence Implications For Active Investment Management PDFMohamed HussienNo ratings yet

- VX Python For Finance EuroScipy 2012 Y HilpischDocument47 pagesVX Python For Finance EuroScipy 2012 Y HilpischMohamed HussienNo ratings yet

- 16 Mexico18 Dorantes PDFDocument43 pages16 Mexico18 Dorantes PDFMohamed HussienNo ratings yet

- Introduction To Computational Finance and Financial Econometrics With RDocument527 pagesIntroduction To Computational Finance and Financial Econometrics With RMohamed HussienNo ratings yet

- Philip J. Romero - Tucker Balch - Hedge Fund Secrets - An Introduction To Quantitative Portfolio Management-Business Expert Press (2018)Document117 pagesPhilip J. Romero - Tucker Balch - Hedge Fund Secrets - An Introduction To Quantitative Portfolio Management-Business Expert Press (2018)Mohamed Hussien100% (1)

- Ec371 Topic 3Document13 pagesEc371 Topic 3Mohamed HussienNo ratings yet

- Correction For Exercise 7.2Document2 pagesCorrection For Exercise 7.2Mohamed HussienNo ratings yet

- Chaos Theory and The Science of Fractals, and Their Application in Risk ManagementDocument78 pagesChaos Theory and The Science of Fractals, and Their Application in Risk ManagementMohamed HussienNo ratings yet

- Time Value of MoneyDocument48 pagesTime Value of MoneyMohamed HussienNo ratings yet

- A Portfolio Selection and Capital Asset Pricing Model: Luigi Buzzacchi, Luca L. GhezziDocument15 pagesA Portfolio Selection and Capital Asset Pricing Model: Luigi Buzzacchi, Luca L. GhezziMohamed HussienNo ratings yet

- Financial Statement AnalysisDocument29 pagesFinancial Statement AnalysisMohamed HussienNo ratings yet

- Geogonia v. Court of Appeals DigestDocument6 pagesGeogonia v. Court of Appeals DigestJoy RaguindinNo ratings yet

- (3.) Interphil Laboratories Employees Union (Digest)Document2 pages(3.) Interphil Laboratories Employees Union (Digest)Dom Robinson BaggayanNo ratings yet

- SOA TemplateDocument1 pageSOA TemplateNoorasyaLya RozikinNo ratings yet

- Responsibility CentresDocument9 pagesResponsibility Centresparminder261090No ratings yet

- FLENDER D20-1 English HELICAL AND BEVEL GEARDocument25 pagesFLENDER D20-1 English HELICAL AND BEVEL GEARParcela Pinares NorteNo ratings yet

- CH 1 To 8Document4 pagesCH 1 To 8John WickNo ratings yet

- DEP 37.91.10.11-Gen Mobile Mooring Systems (Endorsement of API RP 2SK, API RP 2SM and API RP 2I)Document9 pagesDEP 37.91.10.11-Gen Mobile Mooring Systems (Endorsement of API RP 2SK, API RP 2SM and API RP 2I)Sd MahmoodNo ratings yet

- Quiz Techno Group1 ECEEEMEDocument2 pagesQuiz Techno Group1 ECEEEMEJohn Mark BallesterosNo ratings yet

- Bbsu Graduate Directory2 2016 1Document45 pagesBbsu Graduate Directory2 2016 1Ehsaan NooraliNo ratings yet

- 5 Characteristics-Defined ProjectDocument1 page5 Characteristics-Defined ProjectHarpreet SinghNo ratings yet

- 10-11-2016 - The Hindu - Shashi ThakurDocument26 pages10-11-2016 - The Hindu - Shashi ThakurSunilSainiNo ratings yet

- Khyber City Fee ScheduleDocument2 pagesKhyber City Fee ScheduleMohsin KhanNo ratings yet

- NetApp SnapMirrorDocument4 pagesNetApp SnapMirrorVijay1506No ratings yet

- It 41Document2 pagesIt 41रवींद्र वैद्यNo ratings yet

- Name Shehnila Azam Registration No# 45736 Course Cost and Management Accounting DAY Sunday Timing 3 To 6 Practice#1Document6 pagesName Shehnila Azam Registration No# 45736 Course Cost and Management Accounting DAY Sunday Timing 3 To 6 Practice#1yousuf AhmedNo ratings yet

- Tutorial 4 - Multivariable FunctionsDocument3 pagesTutorial 4 - Multivariable FunctionssurojiddinNo ratings yet

- Conjoint AnalysisDocument17 pagesConjoint Analysismark david sabellaNo ratings yet

- 2.0 Element of Conversion (Latest)Document5 pages2.0 Element of Conversion (Latest)b2utifulxxxNo ratings yet

- Franchise ProjectDocument3 pagesFranchise ProjectNicollete Limguangco SablaonNo ratings yet

- Kongunadu College of Engineering and Technology: Quantitative Aptitude PartnershipDocument16 pagesKongunadu College of Engineering and Technology: Quantitative Aptitude PartnershipGnana Prakasam RNo ratings yet

- Aca 2024 PlannerDocument1 pageAca 2024 Planneryfarhana2002No ratings yet

- Definition of IrrDocument3 pagesDefinition of IrrRajesh ShresthaNo ratings yet

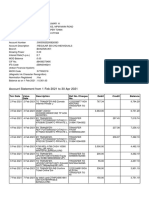

- Account Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUday AbhiNo ratings yet

- Touc Hin G Li Ves, Imp Ro Ving Life - Proc Ter & GambleDocument30 pagesTouc Hin G Li Ves, Imp Ro Ving Life - Proc Ter & Gamblechandni kundel75% (12)

- PCB Quote 1003Document1 pagePCB Quote 1003rhedmishNo ratings yet

- DBLDocument3 pagesDBLLeafe MendozaNo ratings yet

- Audit Non Conformance ReportDocument4 pagesAudit Non Conformance Reportbudi_alamsyah100% (2)

Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Answer PDFDocument17 pagesAnswer PDFميلاد نوروزي رهبرNo ratings yet

- Chapter 8: Risk and ReturnDocument56 pagesChapter 8: Risk and ReturnMohamed HussienNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Multiple Choice Questions Subject: Accountancy Class: XiDocument4 pagesMultiple Choice Questions Subject: Accountancy Class: XiShahid NaikNo ratings yet

- Always Trust The Customer How Zara Has Revolutionized The Fashion Industry and Become A Worldwide LeaderDocument27 pagesAlways Trust The Customer How Zara Has Revolutionized The Fashion Industry and Become A Worldwide LeaderbeatriceNo ratings yet

- Black-Litterman Portfolio Allocation Stability and Financial Performance With MGARCH-M Derived ViewsDocument65 pagesBlack-Litterman Portfolio Allocation Stability and Financial Performance With MGARCH-M Derived ViewsMohamed HussienNo ratings yet

- Introduction & Research: Factor InvestingDocument44 pagesIntroduction & Research: Factor InvestingMohamed HussienNo ratings yet

- TN1 Basic Pre-Calculus: AcronymsDocument11 pagesTN1 Basic Pre-Calculus: AcronymsMohamed HussienNo ratings yet

- TN 2 - Basic Calculus With Financial Applications: 1 Functions and LimitsDocument16 pagesTN 2 - Basic Calculus With Financial Applications: 1 Functions and LimitsMohamed HussienNo ratings yet

- The Dark Side of Passive Investing: White PaperDocument11 pagesThe Dark Side of Passive Investing: White PaperMohamed HussienNo ratings yet

- Index Smart BetaDocument44 pagesIndex Smart BetaMohamed HussienNo ratings yet

- Giorgio S. Questa Induction To Quantitative Methods in FinanceDocument2 pagesGiorgio S. Questa Induction To Quantitative Methods in FinanceMohamed HussienNo ratings yet

- From Smart Beta To Hard Reality: Executive SummaryDocument8 pagesFrom Smart Beta To Hard Reality: Executive SummaryMohamed Hussien100% (1)

- Transportation Methods PDFDocument24 pagesTransportation Methods PDFMohamed Hussien100% (1)

- Factor Model Notes:: R α β f β f …+β f ϵ R α β ' f ϵDocument2 pagesFactor Model Notes:: R α β f β f …+β f ϵ R α β ' f ϵMohamed HussienNo ratings yet

- Week 1 NotesDocument72 pagesWeek 1 NotesMohamed HussienNo ratings yet

- PerformanceAnalytics PDFDocument214 pagesPerformanceAnalytics PDFMohamed HussienNo ratings yet

- Probability Distribution and Statistics: Key Points of LearningDocument24 pagesProbability Distribution and Statistics: Key Points of LearningMohamed HussienNo ratings yet

- The Efficient Market Theory and Evidence Implications For Active Investment Management PDFDocument93 pagesThe Efficient Market Theory and Evidence Implications For Active Investment Management PDFMohamed HussienNo ratings yet

- VX Python For Finance EuroScipy 2012 Y HilpischDocument47 pagesVX Python For Finance EuroScipy 2012 Y HilpischMohamed HussienNo ratings yet

- 16 Mexico18 Dorantes PDFDocument43 pages16 Mexico18 Dorantes PDFMohamed HussienNo ratings yet

- Introduction To Computational Finance and Financial Econometrics With RDocument527 pagesIntroduction To Computational Finance and Financial Econometrics With RMohamed HussienNo ratings yet

- Philip J. Romero - Tucker Balch - Hedge Fund Secrets - An Introduction To Quantitative Portfolio Management-Business Expert Press (2018)Document117 pagesPhilip J. Romero - Tucker Balch - Hedge Fund Secrets - An Introduction To Quantitative Portfolio Management-Business Expert Press (2018)Mohamed Hussien100% (1)

- Ec371 Topic 3Document13 pagesEc371 Topic 3Mohamed HussienNo ratings yet

- Correction For Exercise 7.2Document2 pagesCorrection For Exercise 7.2Mohamed HussienNo ratings yet

- Chaos Theory and The Science of Fractals, and Their Application in Risk ManagementDocument78 pagesChaos Theory and The Science of Fractals, and Their Application in Risk ManagementMohamed HussienNo ratings yet

- Time Value of MoneyDocument48 pagesTime Value of MoneyMohamed HussienNo ratings yet

- A Portfolio Selection and Capital Asset Pricing Model: Luigi Buzzacchi, Luca L. GhezziDocument15 pagesA Portfolio Selection and Capital Asset Pricing Model: Luigi Buzzacchi, Luca L. GhezziMohamed HussienNo ratings yet

- Financial Statement AnalysisDocument29 pagesFinancial Statement AnalysisMohamed HussienNo ratings yet

- Geogonia v. Court of Appeals DigestDocument6 pagesGeogonia v. Court of Appeals DigestJoy RaguindinNo ratings yet

- (3.) Interphil Laboratories Employees Union (Digest)Document2 pages(3.) Interphil Laboratories Employees Union (Digest)Dom Robinson BaggayanNo ratings yet

- SOA TemplateDocument1 pageSOA TemplateNoorasyaLya RozikinNo ratings yet

- Responsibility CentresDocument9 pagesResponsibility Centresparminder261090No ratings yet

- FLENDER D20-1 English HELICAL AND BEVEL GEARDocument25 pagesFLENDER D20-1 English HELICAL AND BEVEL GEARParcela Pinares NorteNo ratings yet

- CH 1 To 8Document4 pagesCH 1 To 8John WickNo ratings yet

- DEP 37.91.10.11-Gen Mobile Mooring Systems (Endorsement of API RP 2SK, API RP 2SM and API RP 2I)Document9 pagesDEP 37.91.10.11-Gen Mobile Mooring Systems (Endorsement of API RP 2SK, API RP 2SM and API RP 2I)Sd MahmoodNo ratings yet

- Quiz Techno Group1 ECEEEMEDocument2 pagesQuiz Techno Group1 ECEEEMEJohn Mark BallesterosNo ratings yet

- Bbsu Graduate Directory2 2016 1Document45 pagesBbsu Graduate Directory2 2016 1Ehsaan NooraliNo ratings yet

- 5 Characteristics-Defined ProjectDocument1 page5 Characteristics-Defined ProjectHarpreet SinghNo ratings yet

- 10-11-2016 - The Hindu - Shashi ThakurDocument26 pages10-11-2016 - The Hindu - Shashi ThakurSunilSainiNo ratings yet

- Khyber City Fee ScheduleDocument2 pagesKhyber City Fee ScheduleMohsin KhanNo ratings yet

- NetApp SnapMirrorDocument4 pagesNetApp SnapMirrorVijay1506No ratings yet

- It 41Document2 pagesIt 41रवींद्र वैद्यNo ratings yet

- Name Shehnila Azam Registration No# 45736 Course Cost and Management Accounting DAY Sunday Timing 3 To 6 Practice#1Document6 pagesName Shehnila Azam Registration No# 45736 Course Cost and Management Accounting DAY Sunday Timing 3 To 6 Practice#1yousuf AhmedNo ratings yet

- Tutorial 4 - Multivariable FunctionsDocument3 pagesTutorial 4 - Multivariable FunctionssurojiddinNo ratings yet

- Conjoint AnalysisDocument17 pagesConjoint Analysismark david sabellaNo ratings yet

- 2.0 Element of Conversion (Latest)Document5 pages2.0 Element of Conversion (Latest)b2utifulxxxNo ratings yet

- Franchise ProjectDocument3 pagesFranchise ProjectNicollete Limguangco SablaonNo ratings yet

- Kongunadu College of Engineering and Technology: Quantitative Aptitude PartnershipDocument16 pagesKongunadu College of Engineering and Technology: Quantitative Aptitude PartnershipGnana Prakasam RNo ratings yet

- Aca 2024 PlannerDocument1 pageAca 2024 Planneryfarhana2002No ratings yet

- Definition of IrrDocument3 pagesDefinition of IrrRajesh ShresthaNo ratings yet

- Account Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument11 pagesAccount Statement From 1 Feb 2021 To 30 Apr 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceUday AbhiNo ratings yet

- Touc Hin G Li Ves, Imp Ro Ving Life - Proc Ter & GambleDocument30 pagesTouc Hin G Li Ves, Imp Ro Ving Life - Proc Ter & Gamblechandni kundel75% (12)

- PCB Quote 1003Document1 pagePCB Quote 1003rhedmishNo ratings yet

- DBLDocument3 pagesDBLLeafe MendozaNo ratings yet

- Audit Non Conformance ReportDocument4 pagesAudit Non Conformance Reportbudi_alamsyah100% (2)