Download as doc, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

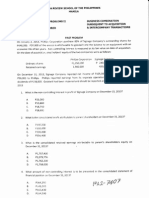

- CPAR - P2 - 7407 - Business Combination Subsequent To Acquisition PDFDocument5 pagesCPAR - P2 - 7407 - Business Combination Subsequent To Acquisition PDFAngelo Villadores100% (3)

- Primarchs DatasheetsDocument24 pagesPrimarchs DatasheetsJosiah Young1100% (5)

- I. Multiple ChoicesDocument7 pagesI. Multiple ChoicesAlain Fung Land MakNo ratings yet

- MAS PreweekDocument46 pagesMAS Preweekclaire_charm27100% (1)

- Auditing: Integral To The Economy: Chapter 1Document48 pagesAuditing: Integral To The Economy: Chapter 1Alain Fung Land MakNo ratings yet

- Pythagoras: BackgroundDocument17 pagesPythagoras: BackgroundAlain Fung Land MakNo ratings yet

- Rocks and Minerals: Rocks: Rock Types Metamorphic Magma LavaDocument3 pagesRocks and Minerals: Rocks: Rock Types Metamorphic Magma LavaAlain Fung Land MakNo ratings yet

- This Paper Is A Advance Accounting Solution Manual For Beams Book 12Th EditionDocument1 pageThis Paper Is A Advance Accounting Solution Manual For Beams Book 12Th EditionAlain Fung Land MakNo ratings yet

- Jahaziel Notarte Zalaver: Adress: Calle 7, Lawang Bato, Valenzuela City Email: CellDocument2 pagesJahaziel Notarte Zalaver: Adress: Calle 7, Lawang Bato, Valenzuela City Email: CellAlain Fung Land MakNo ratings yet

- Recruitment & Selection Reliance Jio Full Report - 100 Page MANU SHARMA MBA 3rd SEMDocument102 pagesRecruitment & Selection Reliance Jio Full Report - 100 Page MANU SHARMA MBA 3rd SEMImpression Graphics100% (4)

- PET-UT-U4 Without AnswersDocument2 pagesPET-UT-U4 Without AnswersAlejandroNo ratings yet

- 中论Document112 pages中论张晓亮No ratings yet

- Tabel PeriodikDocument2 pagesTabel PeriodikNisrina KalyaNo ratings yet

- 2.06 Correlation Is Not CausationDocument2 pages2.06 Correlation Is Not CausationKavya GopakumarNo ratings yet

- 2intro To LLMDDocument2 pages2intro To LLMDKristal ManriqueNo ratings yet

- Six C's of Effective MessagesDocument40 pagesSix C's of Effective MessagessheilaNo ratings yet

- Economists' Corner: Weighing The Procompetitive and Anticompetitive Effects of RPM Under The Rule of ReasonDocument3 pagesEconomists' Corner: Weighing The Procompetitive and Anticompetitive Effects of RPM Under The Rule of ReasonHarsh GandhiNo ratings yet

- Mini Capstone Final Project Implementation and AssessmentDocument8 pagesMini Capstone Final Project Implementation and AssessmentSodium ChlorideNo ratings yet

- GEC PE003 Module 1 CheckedDocument21 pagesGEC PE003 Module 1 CheckedJianica SalesNo ratings yet

- ISO 9001 Awareness AmaDocument51 pagesISO 9001 Awareness AmaHisar SimanjuntakNo ratings yet

- How To Define A Chart of Accounts in Oracle Apps R12: Month End ProcessDocument18 pagesHow To Define A Chart of Accounts in Oracle Apps R12: Month End ProcessCGNo ratings yet

- David RohlDocument3 pagesDavid RohlPhil CaudleNo ratings yet

- BobliDocument2 pagesBoblisuman karNo ratings yet

- 2021 HhhhhhhterqasdwqwDocument1 page2021 HhhhhhhterqasdwqwHassan KhanNo ratings yet

- Prasanna Uday Patil, Supriya Sudhir Pendke, Mousumi Bandyopadhyay, Purban GangulyDocument4 pagesPrasanna Uday Patil, Supriya Sudhir Pendke, Mousumi Bandyopadhyay, Purban GangulyMinh NguyenNo ratings yet

- ClaytonDocument1 pageClaytonapi-3831340No ratings yet

- Department of Education: Republic of The PhilippinesDocument4 pagesDepartment of Education: Republic of The PhilippinesLOIDA AGUILARNo ratings yet

- Congenital Heart Defect-VsdDocument53 pagesCongenital Heart Defect-VsdAuni Akif AleesaNo ratings yet

- Raga Purna Pancama: Analysis ModesDocument1 pageRaga Purna Pancama: Analysis ModesKermitNo ratings yet

- Bishop 1997Document25 pagesBishop 1997Celina AgostinhoNo ratings yet

- Organisational BehaviourDocument9 pagesOrganisational BehaviourMuthu RamalakshmiNo ratings yet

- DK Pocket Genius - HorsesDocument158 pagesDK Pocket Genius - HorsesAnamaria RaduNo ratings yet

- NIDAR, Franced Haggai G. The Brain Is The Vehicle of The MindDocument1 pageNIDAR, Franced Haggai G. The Brain Is The Vehicle of The MindHaggai NidarNo ratings yet

- Tone and MoodDocument8 pagesTone and MoodKristine PanalNo ratings yet

- 1.the Perception of Local Street Food VendorsDocument28 pages1.the Perception of Local Street Food VendorsJay Vince Agpoon MendozaNo ratings yet

- Matrices of Violence: A Post-Structural Feminist Rendering of Nawal El Saadawi's Woman at Point Zero and Lola Soneyin's The Secrets of Baba Segi's WivesDocument6 pagesMatrices of Violence: A Post-Structural Feminist Rendering of Nawal El Saadawi's Woman at Point Zero and Lola Soneyin's The Secrets of Baba Segi's WivesIJELS Research JournalNo ratings yet

- CH 12Document31 pagesCH 12asin12336No ratings yet

- RHA Market Study 2020Document6 pagesRHA Market Study 2020N SayNo ratings yet