Preliminary Pages

Preliminary Pages

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Letter of RequestDocument1 pageLetter of RequestUsman Samuel BabalolaNo ratings yet

- 1.0 Executive SummaryDocument24 pages1.0 Executive SummaryUsman Samuel BabalolaNo ratings yet

- 13 Buyikunmi Close, Off Magada Road, Ibafo, Ogun State.: Letter of AttestationDocument1 page13 Buyikunmi Close, Off Magada Road, Ibafo, Ogun State.: Letter of AttestationUsman Samuel BabalolaNo ratings yet

- KG 2Document9 pagesKG 2Usman Samuel BabalolaNo ratings yet

- NyscDocument1 pageNyscUsman Samuel BabalolaNo ratings yet

- Faith CellDocument1 pageFaith CellUsman Samuel BabalolaNo ratings yet

- Our Lady of Apostles Group of Schools: 4, Ogunfolaji Street, Ibafo, Ogun State Phone: 08148924728, 0806906005Document1 pageOur Lady of Apostles Group of Schools: 4, Ogunfolaji Street, Ibafo, Ogun State Phone: 08148924728, 0806906005Usman Samuel BabalolaNo ratings yet

- Basic 4 3rd Term MidDocument10 pagesBasic 4 3rd Term MidUsman Samuel BabalolaNo ratings yet

- Our Lady of Apostles Group of Schools: 4, Ogunfolaji Street, Ibafo, Ogun State Phone: 08148924728, 0806906005Document1 pageOur Lady of Apostles Group of Schools: 4, Ogunfolaji Street, Ibafo, Ogun State Phone: 08148924728, 0806906005Usman Samuel BabalolaNo ratings yet

- Basic 3 Ex.Document21 pagesBasic 3 Ex.Usman Samuel BabalolaNo ratings yet

- 2nd Term Ex 4Document28 pages2nd Term Ex 4Usman Samuel BabalolaNo ratings yet

- CSC 102 MaterialsDocument74 pagesCSC 102 MaterialsUsman Samuel BabalolaNo ratings yet

- MTS 101 (C)Document6 pagesMTS 101 (C)Usman Samuel BabalolaNo ratings yet

- Solution To CSC 201 (Practical) Questions: Courtesy: Education Committee (08069018655), MSSN - Futa, Obakekere MosqueDocument11 pagesSolution To CSC 201 (Practical) Questions: Courtesy: Education Committee (08069018655), MSSN - Futa, Obakekere MosqueUsman Samuel BabalolaNo ratings yet

- CSC Assignment by Oluokun Basirat Olanike de 69017302CgDocument4 pagesCSC Assignment by Oluokun Basirat Olanike de 69017302CgUsman Samuel BabalolaNo ratings yet

- CSC 102 MaterialsDocument74 pagesCSC 102 MaterialsUsman Samuel BabalolaNo ratings yet

- Chapter 8 MCQDocument4 pagesChapter 8 MCQcik sitiNo ratings yet

- Income TaxatioDocument78 pagesIncome TaxatioHoney BiNo ratings yet

- 13 Task Performance 1 - BUSINESS LAW AND REGULATIONSDocument3 pages13 Task Performance 1 - BUSINESS LAW AND REGULATIONSRynalin De JesusNo ratings yet

- NetflixDocument1 pageNetflixMadhur GoelNo ratings yet

- CIR Vs SolidbankDocument3 pagesCIR Vs SolidbankJoel MilanNo ratings yet

- The Shadow Economy in Portugal An AnalysDocument50 pagesThe Shadow Economy in Portugal An Analysfread3No ratings yet

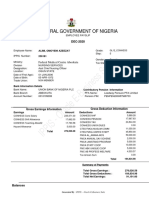

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaAlimi kehinde100% (1)

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErwin TorresNo ratings yet

- QuestionsDocument9 pagesQuestionsOlivia Jane100% (1)

- CIR v. First Express PawnshopDocument16 pagesCIR v. First Express PawnshopHansel Jake B. PampiloNo ratings yet

- Jason Ouwendyk Bankruptcy Trustee Final Report - 16 Feb 2010Document4 pagesJason Ouwendyk Bankruptcy Trustee Final Report - 16 Feb 2010aewljtlakejflNo ratings yet

- Marble Head Mat Own Meeting Report Turf 2009Document283 pagesMarble Head Mat Own Meeting Report Turf 2009uncleadolphNo ratings yet

- Gepco Online BillDocument2 pagesGepco Online BillHafiz RizwanNo ratings yet

- NOTES Limited Liability PartnershipDocument4 pagesNOTES Limited Liability Partnershipragini dadwalNo ratings yet

- FACTURA AaDocument1 pageFACTURA AaHeidy RGNo ratings yet

- Important Changes Introduced by The Finance Act, 2022 - ACNABINDocument40 pagesImportant Changes Introduced by The Finance Act, 2022 - ACNABINZamanNo ratings yet

- Council Policy: Land DevelopmentDocument4 pagesCouncil Policy: Land Developmentsenthilkumar kNo ratings yet

- Tax Audit Clause Remembering TechniqueDocument19 pagesTax Audit Clause Remembering TechniqueRohankumar KshirsagarNo ratings yet

- H Nagenhalli M N Kote Post, Gubbi TQ, Tumkur DT, Karnataka, India Mob: +91 8095252881Document1 pageH Nagenhalli M N Kote Post, Gubbi TQ, Tumkur DT, Karnataka, India Mob: +91 8095252881Akhil KumarNo ratings yet

- P21 Balancing Statement 2018 124615500017Document2 pagesP21 Balancing Statement 2018 124615500017Aurimas AurisNo ratings yet

- Full Download Digital Control System Analysis and Design 4th Edition Phillips Solutions Manual PDF Full ChapterDocument35 pagesFull Download Digital Control System Analysis and Design 4th Edition Phillips Solutions Manual PDF Full Chapterfeasiblenadde46r66100% (20)

- Fishwealth Canning Corporation Vs CirDocument2 pagesFishwealth Canning Corporation Vs CirKateBarrionEspinosaNo ratings yet

- General Energy Storage Systems-CFDocument3 pagesGeneral Energy Storage Systems-CFrajsacksNo ratings yet

- (Tax-Ho) Ease of Paying Taxes ActDocument8 pages(Tax-Ho) Ease of Paying Taxes ActJoshua Neil AdrinedaNo ratings yet

- Minimum Wages and Taxes Concerns of Filipino EntrepreneursDocument63 pagesMinimum Wages and Taxes Concerns of Filipino EntrepreneursMarie Nicole SalmasanNo ratings yet

- Oil&Gas Industry NorwayDocument3 pagesOil&Gas Industry NorwayAnge LexiusNo ratings yet

- Opportunity ScreeningDocument39 pagesOpportunity Screeningglaide lojero100% (1)

- Flowchart of Tax Refund RemediesDocument8 pagesFlowchart of Tax Refund RemedieschenezNo ratings yet

- Property Owner's Notice of Protest: Form 50-132Document3 pagesProperty Owner's Notice of Protest: Form 50-132Raghu ReddyNo ratings yet

- Publicación 963 IRS (Seguro Social) PDFDocument172 pagesPublicación 963 IRS (Seguro Social) PDFEmily RamosNo ratings yet

Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Letter of RequestDocument1 pageLetter of RequestUsman Samuel BabalolaNo ratings yet

- 1.0 Executive SummaryDocument24 pages1.0 Executive SummaryUsman Samuel BabalolaNo ratings yet

- 13 Buyikunmi Close, Off Magada Road, Ibafo, Ogun State.: Letter of AttestationDocument1 page13 Buyikunmi Close, Off Magada Road, Ibafo, Ogun State.: Letter of AttestationUsman Samuel BabalolaNo ratings yet

- KG 2Document9 pagesKG 2Usman Samuel BabalolaNo ratings yet

- NyscDocument1 pageNyscUsman Samuel BabalolaNo ratings yet

- Faith CellDocument1 pageFaith CellUsman Samuel BabalolaNo ratings yet

- Our Lady of Apostles Group of Schools: 4, Ogunfolaji Street, Ibafo, Ogun State Phone: 08148924728, 0806906005Document1 pageOur Lady of Apostles Group of Schools: 4, Ogunfolaji Street, Ibafo, Ogun State Phone: 08148924728, 0806906005Usman Samuel BabalolaNo ratings yet

- Basic 4 3rd Term MidDocument10 pagesBasic 4 3rd Term MidUsman Samuel BabalolaNo ratings yet

- Our Lady of Apostles Group of Schools: 4, Ogunfolaji Street, Ibafo, Ogun State Phone: 08148924728, 0806906005Document1 pageOur Lady of Apostles Group of Schools: 4, Ogunfolaji Street, Ibafo, Ogun State Phone: 08148924728, 0806906005Usman Samuel BabalolaNo ratings yet

- Basic 3 Ex.Document21 pagesBasic 3 Ex.Usman Samuel BabalolaNo ratings yet

- 2nd Term Ex 4Document28 pages2nd Term Ex 4Usman Samuel BabalolaNo ratings yet

- CSC 102 MaterialsDocument74 pagesCSC 102 MaterialsUsman Samuel BabalolaNo ratings yet

- MTS 101 (C)Document6 pagesMTS 101 (C)Usman Samuel BabalolaNo ratings yet

- Solution To CSC 201 (Practical) Questions: Courtesy: Education Committee (08069018655), MSSN - Futa, Obakekere MosqueDocument11 pagesSolution To CSC 201 (Practical) Questions: Courtesy: Education Committee (08069018655), MSSN - Futa, Obakekere MosqueUsman Samuel BabalolaNo ratings yet

- CSC Assignment by Oluokun Basirat Olanike de 69017302CgDocument4 pagesCSC Assignment by Oluokun Basirat Olanike de 69017302CgUsman Samuel BabalolaNo ratings yet

- CSC 102 MaterialsDocument74 pagesCSC 102 MaterialsUsman Samuel BabalolaNo ratings yet

- Chapter 8 MCQDocument4 pagesChapter 8 MCQcik sitiNo ratings yet

- Income TaxatioDocument78 pagesIncome TaxatioHoney BiNo ratings yet

- 13 Task Performance 1 - BUSINESS LAW AND REGULATIONSDocument3 pages13 Task Performance 1 - BUSINESS LAW AND REGULATIONSRynalin De JesusNo ratings yet

- NetflixDocument1 pageNetflixMadhur GoelNo ratings yet

- CIR Vs SolidbankDocument3 pagesCIR Vs SolidbankJoel MilanNo ratings yet

- The Shadow Economy in Portugal An AnalysDocument50 pagesThe Shadow Economy in Portugal An Analysfread3No ratings yet

- IPPIS - Oracle E-Business Suite: Federal Government of NigeriaDocument1 pageIPPIS - Oracle E-Business Suite: Federal Government of NigeriaAlimi kehinde100% (1)

- Module TX003 Types On Income TaxpayersDocument3 pagesModule TX003 Types On Income TaxpayersErwin TorresNo ratings yet

- QuestionsDocument9 pagesQuestionsOlivia Jane100% (1)

- CIR v. First Express PawnshopDocument16 pagesCIR v. First Express PawnshopHansel Jake B. PampiloNo ratings yet

- Jason Ouwendyk Bankruptcy Trustee Final Report - 16 Feb 2010Document4 pagesJason Ouwendyk Bankruptcy Trustee Final Report - 16 Feb 2010aewljtlakejflNo ratings yet

- Marble Head Mat Own Meeting Report Turf 2009Document283 pagesMarble Head Mat Own Meeting Report Turf 2009uncleadolphNo ratings yet

- Gepco Online BillDocument2 pagesGepco Online BillHafiz RizwanNo ratings yet

- NOTES Limited Liability PartnershipDocument4 pagesNOTES Limited Liability Partnershipragini dadwalNo ratings yet

- FACTURA AaDocument1 pageFACTURA AaHeidy RGNo ratings yet

- Important Changes Introduced by The Finance Act, 2022 - ACNABINDocument40 pagesImportant Changes Introduced by The Finance Act, 2022 - ACNABINZamanNo ratings yet

- Council Policy: Land DevelopmentDocument4 pagesCouncil Policy: Land Developmentsenthilkumar kNo ratings yet

- Tax Audit Clause Remembering TechniqueDocument19 pagesTax Audit Clause Remembering TechniqueRohankumar KshirsagarNo ratings yet

- H Nagenhalli M N Kote Post, Gubbi TQ, Tumkur DT, Karnataka, India Mob: +91 8095252881Document1 pageH Nagenhalli M N Kote Post, Gubbi TQ, Tumkur DT, Karnataka, India Mob: +91 8095252881Akhil KumarNo ratings yet

- P21 Balancing Statement 2018 124615500017Document2 pagesP21 Balancing Statement 2018 124615500017Aurimas AurisNo ratings yet

- Full Download Digital Control System Analysis and Design 4th Edition Phillips Solutions Manual PDF Full ChapterDocument35 pagesFull Download Digital Control System Analysis and Design 4th Edition Phillips Solutions Manual PDF Full Chapterfeasiblenadde46r66100% (20)

- Fishwealth Canning Corporation Vs CirDocument2 pagesFishwealth Canning Corporation Vs CirKateBarrionEspinosaNo ratings yet

- General Energy Storage Systems-CFDocument3 pagesGeneral Energy Storage Systems-CFrajsacksNo ratings yet

- (Tax-Ho) Ease of Paying Taxes ActDocument8 pages(Tax-Ho) Ease of Paying Taxes ActJoshua Neil AdrinedaNo ratings yet

- Minimum Wages and Taxes Concerns of Filipino EntrepreneursDocument63 pagesMinimum Wages and Taxes Concerns of Filipino EntrepreneursMarie Nicole SalmasanNo ratings yet

- Oil&Gas Industry NorwayDocument3 pagesOil&Gas Industry NorwayAnge LexiusNo ratings yet

- Opportunity ScreeningDocument39 pagesOpportunity Screeningglaide lojero100% (1)

- Flowchart of Tax Refund RemediesDocument8 pagesFlowchart of Tax Refund RemedieschenezNo ratings yet

- Property Owner's Notice of Protest: Form 50-132Document3 pagesProperty Owner's Notice of Protest: Form 50-132Raghu ReddyNo ratings yet

- Publicación 963 IRS (Seguro Social) PDFDocument172 pagesPublicación 963 IRS (Seguro Social) PDFEmily RamosNo ratings yet