Download as docx, pdf, or txt

You might also like

- Esign Faq: 1. What Is The Online Esign Electronic Signature Service?Document10 pagesEsign Faq: 1. What Is The Online Esign Electronic Signature Service?kishing0905No ratings yet

- eSign-APIv2 1Document15 pageseSign-APIv2 1SujataNo ratings yet

- Esign - Online Electronic Signature Service: Government of IndiaDocument2 pagesEsign - Online Electronic Signature Service: Government of IndiaKumar SangamNo ratings yet

- FAQ EsignDocument4 pagesFAQ EsignDevdatta TareNo ratings yet

- Esign API SpecificationsDocument23 pagesEsign API SpecificationsBa Vũ ThịNo ratings yet

- eSign-API v1.0Document26 pageseSign-API v1.0sumandroNo ratings yet

- Esign Brochure 1.4-RC PDFDocument2 pagesEsign Brochure 1.4-RC PDFD BhaskarNo ratings yet

- BBA-VI Semester BBAN606 Fundamental of E-Commerce Unit Iii NotesDocument16 pagesBBA-VI Semester BBAN606 Fundamental of E-Commerce Unit Iii NotesIsha BhatiaNo ratings yet

- List of Live AuaDocument6 pagesList of Live AuaRaaju- Sys.AdminNo ratings yet

- RBI Circular E-KYCDocument4 pagesRBI Circular E-KYCadmiralninjaNo ratings yet

- E SignaturesDocument7 pagesE SignaturesArya SenNo ratings yet

- Secure E-Cheque Clearance Between Financial InstitutionsDocument18 pagesSecure E-Cheque Clearance Between Financial InstitutionsAmith Ram ReddyNo ratings yet

- DIGITALBanking Group 8Document28 pagesDIGITALBanking Group 8Amritesh BhattNo ratings yet

- What Is DSCDocument4 pagesWhat Is DSCsankalp sethNo ratings yet

- Electronic Fiscal Receipting and Invoicing Solution: KakasaDocument6 pagesElectronic Fiscal Receipting and Invoicing Solution: KakasaMichael Kazinda100% (1)

- E KYC PDFDocument4 pagesE KYC PDFCRGB PersonnelNo ratings yet

- Ekyc PDFDocument4 pagesEkyc PDFSandeep KumarNo ratings yet

- Internet Payment System: BM028-3-3-IPS Individual AssignmentDocument11 pagesInternet Payment System: BM028-3-3-IPS Individual AssignmentKevin FerdiansyahNo ratings yet

- Uidai Celc LG English 011117Document19 pagesUidai Celc LG English 011117Moidu alias Babu K MNo ratings yet

- Sezonline Online Duty Payment User ManualDocument12 pagesSezonline Online Duty Payment User ManualDUX Durgesh YadavNo ratings yet

- Aadhaar Based ProductsDocument1 pageAadhaar Based ProductsRam RNo ratings yet

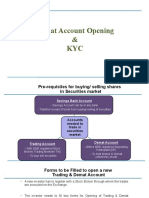

- Demat Account & KYCDocument17 pagesDemat Account & KYCRaja ShafkatNo ratings yet

- What Is Aadhaar KYC Know e KYC For Aadhaar CardDocument3 pagesWhat Is Aadhaar KYC Know e KYC For Aadhaar CardHARSHNo ratings yet

- Circular No Sebi Ho MRDDocument70 pagesCircular No Sebi Ho MRDgurubalaji15No ratings yet

- E-Way Bill User ManualDocument48 pagesE-Way Bill User ManualSivaRamanNo ratings yet

- Electronic Payment System: Presented byDocument43 pagesElectronic Payment System: Presented bysheetal28svNo ratings yet

- E Filing NoteDocument9 pagesE Filing NoteanymoneyNo ratings yet

- Electronic ChequesDocument4 pagesElectronic ChequesAtharvaNo ratings yet

- Taxguru - In-Procedure For Formation of Private and Public Company in IndiaDocument15 pagesTaxguru - In-Procedure For Formation of Private and Public Company in IndiaRam IyerNo ratings yet

- Unit 5 IT ActDocument25 pagesUnit 5 IT ActKeshav MaheshwariNo ratings yet

- FAQ On DGFT EDI System Q 1. What Are The DGFT Schemes For Which Online Applications Can Be Filed?Document4 pagesFAQ On DGFT EDI System Q 1. What Are The DGFT Schemes For Which Online Applications Can Be Filed?Anonymous jwHK79lNo ratings yet

- E Stamp ManualDocument5 pagesE Stamp ManualNavin RajaNo ratings yet

- SOP BC Interoperability - Interface SpecificationsDocument90 pagesSOP BC Interoperability - Interface SpecificationsutnfrbaNo ratings yet

- CA Focused AttachmentsDocument8 pagesCA Focused AttachmentssatishNo ratings yet

- Assignment RahulDocument6 pagesAssignment RahulRahul Gupta RoyNo ratings yet

- UNIT 1 E Payment SystemDocument76 pagesUNIT 1 E Payment SystemRahul DesuNo ratings yet

- Computer Banking: E - BankingDocument14 pagesComputer Banking: E - BankingMALKANI DISHA DEEPAKNo ratings yet

- Controller of Certifying AuthoritiesDocument2 pagesController of Certifying AuthoritiesArya SenNo ratings yet

- Functional Steps To Use Efiling &epaymentDocument66 pagesFunctional Steps To Use Efiling &epaymentAmanuelNo ratings yet

- Draft E-Payment Gateway Concepts by Amjad AliDocument14 pagesDraft E-Payment Gateway Concepts by Amjad AliAmjad AliNo ratings yet

- Cca EauthDocument20 pagesCca Eauthneevshah5686No ratings yet

- Digital India 1Document15 pagesDigital India 1Yogesh GargNo ratings yet

- Digital SignatureDocument7 pagesDigital Signatureshriyash kalbandeNo ratings yet

- 74821bos60500 cp12Document37 pages74821bos60500 cp12Looney ApacheNo ratings yet

- E-Way Bill System: User Manual For Tax PayersDocument56 pagesE-Way Bill System: User Manual For Tax PayersashokNo ratings yet

- Assignment On Secure Electronic TransactionDocument10 pagesAssignment On Secure Electronic TransactionSubhash SagarNo ratings yet

- DSC Registration in IndiaDocument6 pagesDSC Registration in IndiaKriti vardhanNo ratings yet

- Central KYC Note - MFINDocument5 pagesCentral KYC Note - MFINvayusena123No ratings yet

- E-Way Bill ManualDocument42 pagesE-Way Bill ManualshahtaralsNo ratings yet

- Banking 5Document29 pagesBanking 5Rakshitha. A GedamNo ratings yet

- Jhulaghat FinalDocument108 pagesJhulaghat FinalAltafNo ratings yet

- E-Invoice (Electronic Invoice) : List of AbbreviationsDocument5 pagesE-Invoice (Electronic Invoice) : List of AbbreviationsChirag SolankiNo ratings yet

- E-Way Bill System: User ManualDocument60 pagesE-Way Bill System: User ManualharishNo ratings yet

- E-Invoice System: User Manual - Bulk Generation & Cancellation ToolDocument23 pagesE-Invoice System: User Manual - Bulk Generation & Cancellation Toolsuman.neel59386100% (1)

- High-Tech Banking: Unit VDocument24 pagesHigh-Tech Banking: Unit VtkashvinNo ratings yet

- Instructions For E-Voting: Biocon LimitedDocument4 pagesInstructions For E-Voting: Biocon LimitedAnand Kumar SinghNo ratings yet

- Self KYC ProcessDocument3 pagesSelf KYC ProcessJay SwaminarayanNo ratings yet

- E-Invoicing For Certificate Course On GSTDocument16 pagesE-Invoicing For Certificate Course On GSTShweta Prathamesh BadgujarNo ratings yet

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersFrom EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersFrom EverandEvaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersNo ratings yet

- Assessment & AuditDocument17 pagesAssessment & AuditRam SewakNo ratings yet

- Inspection, Search, Seizure and ArrestDocument40 pagesInspection, Search, Seizure and ArrestRam SewakNo ratings yet

- Miscellaneous ProvisionsDocument51 pagesMiscellaneous ProvisionsRam SewakNo ratings yet

- Joining ReportDocument5 pagesJoining ReportRam SewakNo ratings yet

- Nomination Form For GPFDocument3 pagesNomination Form For GPFRam SewakNo ratings yet

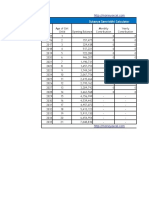

- Sukanya Samriddhi Calculator VariableDocument38 pagesSukanya Samriddhi Calculator VariableRam SewakNo ratings yet

- DP 900T00A ENU TrainerHandbookDocument288 pagesDP 900T00A ENU TrainerHandbookAndré baungatnerNo ratings yet

- Tribhuvan University Institute of Engineering, Pulchowk Campus Lalitpur, NepalDocument8 pagesTribhuvan University Institute of Engineering, Pulchowk Campus Lalitpur, NepalPhantom BeingNo ratings yet

- Cognos Cloud Best Practices:: Moving From A Single-To A Multiple-Image TopologyDocument12 pagesCognos Cloud Best Practices:: Moving From A Single-To A Multiple-Image TopologyDean DjordjevicNo ratings yet

- Agile Based KanbanDocument6 pagesAgile Based KanbanCarlos Ernesto Flores AlbinoNo ratings yet

- Ai Powered Marketing and Sales Reach New Heights With Generative AiDocument11 pagesAi Powered Marketing and Sales Reach New Heights With Generative AiCésar Caramelo100% (1)

- Serviio Online Resource Plugin Implementation GuideDocument12 pagesServiio Online Resource Plugin Implementation GuidejannisgoskiNo ratings yet

- Empress Trucking-MOA - Revised PDFDocument5 pagesEmpress Trucking-MOA - Revised PDFJoviNo ratings yet

- Ccna Acl Lab: School of Information Studies Syracuse University Created by 4/22/2008 By: James Benninger Used in CCNADocument18 pagesCcna Acl Lab: School of Information Studies Syracuse University Created by 4/22/2008 By: James Benninger Used in CCNAFaby ReveloNo ratings yet

- Schneider SoMachine M Series EthernetDocument10 pagesSchneider SoMachine M Series EthernetSalome BitutuNo ratings yet

- Docker Scenario Based QuestionsDocument2 pagesDocker Scenario Based QuestionsvijayhclNo ratings yet

- IEEE DAY in A Box 2022Document8 pagesIEEE DAY in A Box 2022Gerardo MtzNo ratings yet

- As400 QuestionsDocument32 pagesAs400 QuestionsvgrynyukNo ratings yet

- Selectron On Track: Together For The Future: Visions of Today For The Mobility of TomorrowDocument21 pagesSelectron On Track: Together For The Future: Visions of Today For The Mobility of TomorrowsalidosoNo ratings yet

- CPE Architecture: Alvarion Training ServicesDocument36 pagesCPE Architecture: Alvarion Training ServicesTonzayNo ratings yet

- Docker ComposeDocument3 pagesDocker ComposeAlvian RizaldiNo ratings yet

- Service Oriented Computing in RoboticDocument14 pagesService Oriented Computing in RoboticDaredevils MarvelNo ratings yet

- PR4100 User Manual enDocument140 pagesPR4100 User Manual enRavi Indra67% (3)

- Opencv2refman CPPDocument409 pagesOpencv2refman CPPWasim KaraniNo ratings yet

- Six Sigma Black Belt Introduction - YouTube PDFDocument2 pagesSix Sigma Black Belt Introduction - YouTube PDFRajkishor TripathyNo ratings yet

- DL1 Interview QuestionsDocument41 pagesDL1 Interview QuestionsGanesh WarangNo ratings yet

- Getting Started: Ocean Software Development Framework For TechlogDocument58 pagesGetting Started: Ocean Software Development Framework For TechlogNicolas UrupukinaNo ratings yet

- Lecture 0 - Web - ProgrammingDocument10 pagesLecture 0 - Web - Programminghojayas860No ratings yet

- Flood Map Planning 2021 11 01T18 - 17 - 31.700ZDocument2 pagesFlood Map Planning 2021 11 01T18 - 17 - 31.700ZPerrytkNo ratings yet

- Exploring Sas ViyaDocument78 pagesExploring Sas ViyaAlexandre AlvesNo ratings yet

- EVB Schematic For RK3399ProDocument36 pagesEVB Schematic For RK3399ProChu Tiến Thịnh100% (1)

- BUT000 Business Partner: Topic / Contains..Document6 pagesBUT000 Business Partner: Topic / Contains..Rahul MalhotraNo ratings yet

- Chapter 2 - Microprocessor ArchitectureDocument52 pagesChapter 2 - Microprocessor ArchitectureAhmed QaziNo ratings yet

- Punjabi University, Computer Science DepartmentDocument9 pagesPunjabi University, Computer Science DepartmentAbdela Aman MtechNo ratings yet

- Internet Service ProviderDocument4 pagesInternet Service Providerbiratgiri00No ratings yet

- Repot PLCDocument7 pagesRepot PLCkupirzz88No ratings yet