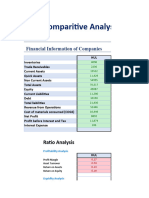

Download as xlsx, pdf, or txt

You might also like

- Club Pilates - 2020-04-29 - FDD - Xponential FitnessDocument284 pagesClub Pilates - 2020-04-29 - FDD - Xponential FitnessFuzzy PandaNo ratings yet

- NP EX 6 OrthoDocument41 pagesNP EX 6 OrthoEphraim Uhuru0% (1)

- A Project Report On Sundaram Finance LimitedDocument53 pagesA Project Report On Sundaram Finance LimitedAnonymous lOz8e6tl080% (5)

- Finance Simulation - Capital BudgetingDocument1 pageFinance Simulation - Capital BudgetingKarthi KeyanNo ratings yet

- E8-29 Segmented Income Statement: Conceptual ConnectionDocument5 pagesE8-29 Segmented Income Statement: Conceptual ConnectionDhiva Rianitha Manurung100% (1)

- FMDocument5 pagesFMbpsc08No ratings yet

- Economic Analysis: Company Name Suscok Jaya GemilangDocument1 pageEconomic Analysis: Company Name Suscok Jaya GemilangSamuel ArelianoNo ratings yet

- Numbers Sheet Name Numbers Table Name Excel Worksheet NameDocument15 pagesNumbers Sheet Name Numbers Table Name Excel Worksheet NameSridhar KatnamNo ratings yet

- Rafeeqa Begum (DPR)Document13 pagesRafeeqa Begum (DPR)syedNo ratings yet

- DPR PDFDocument17 pagesDPR PDFDipankar DasNo ratings yet

- Rdy Mad e Pmegp 10 LacsDocument13 pagesRdy Mad e Pmegp 10 LacssyedNo ratings yet

- CopperDocument4 pagesCopperChip choiNo ratings yet

- Rdy Mad e Pmegp 5lacsDocument12 pagesRdy Mad e Pmegp 5lacssyedNo ratings yet

- Bank Appraisal Memo For CC TLDocument16 pagesBank Appraisal Memo For CC TLYash BaneNo ratings yet

- Cost of Project (In Millions)Document14 pagesCost of Project (In Millions)Gaurav GuptaNo ratings yet

- Shawl EmbroiideryDocument11 pagesShawl EmbroiiderysyedNo ratings yet

- CRDocument19 pagesCRVijay HemwaniNo ratings yet

- WC 4.5 TL .50 WalnutDocument13 pagesWC 4.5 TL .50 WalnutsyedNo ratings yet

- Directions For Using The Model:: Capital ExpendituresDocument204 pagesDirections For Using The Model:: Capital Expenditureschintandesai20083112No ratings yet

- Monmouth Inc Solution 5 PDF FreeDocument12 pagesMonmouth Inc Solution 5 PDF FreePedro José ZapataNo ratings yet

- Monmouth Inc Solution 5 PDF FreeDocument12 pagesMonmouth Inc Solution 5 PDF FreePedro José ZapataNo ratings yet

- Group 5 - Diamond Chemicals AssignmentDocument11 pagesGroup 5 - Diamond Chemicals AssignmentRijul AgrawalNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print FinancialsdeepNo ratings yet

- Finance Assignment Reviewed FinalDocument19 pagesFinance Assignment Reviewed FinalpranalraiNo ratings yet

- A Project Report On Agri-Input Supply CentreDocument14 pagesA Project Report On Agri-Input Supply CentreSuresh Varma0% (1)

- Project Report For: Royal StarDocument14 pagesProject Report For: Royal StarSUREMAN FINANCIAL SERVICESNo ratings yet

- 22 HulDocument10 pages22 HulAnushka Chhabra H22067No ratings yet

- ASL Industries 18th Oct 2023 V2.2Document23 pagesASL Industries 18th Oct 2023 V2.2Shubham KothawadeNo ratings yet

- Sl. Particulars Total No. 1 Vehicle B. SLX (Mahindra) 6.87 6.87Document17 pagesSl. Particulars Total No. 1 Vehicle B. SLX (Mahindra) 6.87 6.87Amit SoniNo ratings yet

- CMADocument12 pagesCMADhruv ChandwaniNo ratings yet

- Diamond Chemicals Team 6's DCF Analysis of Merseyside ProjectDocument1 pageDiamond Chemicals Team 6's DCF Analysis of Merseyside Projectkwarden13No ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document4 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- Emmar Paints and HardwaresDocument22 pagesEmmar Paints and HardwaresRahul NathNo ratings yet

- UPA Vs NDA - Decoding India's Economic RealitiesDocument11 pagesUPA Vs NDA - Decoding India's Economic Realitiesmadhu.maadzNo ratings yet

- Hola KolaDocument3 pagesHola KolaAmit BiswalNo ratings yet

- Pg1 3 MergedDocument10 pagesPg1 3 MergedAryan DhamechaNo ratings yet

- Non-Retirement - Future - InstantXRay 2011 05 09Document2 pagesNon-Retirement - Future - InstantXRay 2011 05 09RaghavanJayaramanNo ratings yet

- Financials SaharaDocument19 pagesFinancials SaharaJitendra NikhareNo ratings yet

- Parle Biscut CompanyDocument5 pagesParle Biscut CompanyBharat RajputNo ratings yet

- Liabilities 2.1.current Liabilities I. Borrowings From IOB From Other Banks Commercial Paper Sub-TotalDocument11 pagesLiabilities 2.1.current Liabilities I. Borrowings From IOB From Other Banks Commercial Paper Sub-TotalsethigaganNo ratings yet

- Tunis Marine Hatchery One PagerDocument1 pageTunis Marine Hatchery One PagerMajid BouchaNo ratings yet

- 44 BricksDocument1 page44 BricksGreatHavokNo ratings yet

- Mango Processing & Canning Unit 1Document5 pagesMango Processing & Canning Unit 1juanNo ratings yet

- Financial Projections Cost of Project and Means of FinanceDocument22 pagesFinancial Projections Cost of Project and Means of FinancehimanshiNo ratings yet

- Welcome: Class of AFS-2010 by Zain Javed, CFADocument14 pagesWelcome: Class of AFS-2010 by Zain Javed, CFASufyan FaridiNo ratings yet

- Schottky Barrier Diode RB088B150Document5 pagesSchottky Barrier Diode RB088B150rosvm rosvmNo ratings yet

- RP Infra Cma ReportDocument12 pagesRP Infra Cma ReportJitendra NikhareNo ratings yet

- Black Gold - AnalysisDocument12 pagesBlack Gold - AnalysisAbdulrahman DhabaanNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- 28 - Swati Aggarwal - VedantaDocument11 pages28 - Swati Aggarwal - Vedantarajat_singlaNo ratings yet

- North Compiled TasksDocument19 pagesNorth Compiled Tasksbc150201683 Asad RazaNo ratings yet

- Annual Report 2000Document43 pagesAnnual Report 2000Enamul HaqueNo ratings yet

- CMA Statement of Trading ActivityDocument17 pagesCMA Statement of Trading ActivitySubrato MukherjeeNo ratings yet

- Energy Saving Choke - LED LightsDocument10 pagesEnergy Saving Choke - LED LightsSabhaya ChiragNo ratings yet

- Safety Report Weekly 1st - Project TMCT 9-15 2023 (Week 2)Document19 pagesSafety Report Weekly 1st - Project TMCT 9-15 2023 (Week 2)Ahmad FikriNo ratings yet

- Air Freshener CakesDocument10 pagesAir Freshener CakesRekha KuttappanNo ratings yet

- Particulars Upto To Be Incurred Total Amount Rs. Amount Rs. Amount Rs. I Cost of ProjectDocument11 pagesParticulars Upto To Be Incurred Total Amount Rs. Amount Rs. Amount Rs. I Cost of ProjectAnand H LuharNo ratings yet

- Private Company Financials Balance Sheet: Xchanging Software Europe LimitedDocument1 pagePrivate Company Financials Balance Sheet: Xchanging Software Europe Limitedprabhav2050No ratings yet

- Retail Company With Simple DCFDocument51 pagesRetail Company With Simple DCFJames Mitchell100% (1)

- EC (A) .XLS: Model FactsDocument2 pagesEC (A) .XLS: Model FactsEnriqueNo ratings yet

- Cma DataDocument9 pagesCma Datapk9079885245No ratings yet

- JuniorMasculino FS ScoresDocument1 pageJuniorMasculino FS ScorespedrolamelasNo ratings yet

- Quantitative Finance: Its Development, Mathematical Foundations, and Current ScopeFrom EverandQuantitative Finance: Its Development, Mathematical Foundations, and Current ScopeNo ratings yet

- Reimbursement Claim SheetDocument1 pageReimbursement Claim SheetAditya Kumar SinghNo ratings yet

- Group 15-Div A SubmissionDocument3 pagesGroup 15-Div A SubmissionAditya Kumar SinghNo ratings yet

- In The Sands of TimeDocument3 pagesIn The Sands of TimeAditya Kumar SinghNo ratings yet

- Inventory - Item Stock Sheet: Your Company NameDocument17 pagesInventory - Item Stock Sheet: Your Company NameAditya Kumar SinghNo ratings yet

- Professional Solved VRNDocument33 pagesProfessional Solved VRNAditya Kumar SinghNo ratings yet

- India Kailasa 4.1.3Document17 pagesIndia Kailasa 4.1.3Aditya Kumar SinghNo ratings yet

- Financial Accounting ProjectDocument1 pageFinancial Accounting ProjectAditya Kumar SinghNo ratings yet

- Cutting 2Document39 pagesCutting 2Aditya Kumar SinghNo ratings yet

- Saw Aw ADocument19 pagesSaw Aw AAditya Kumar SinghNo ratings yet

- Assignment On Merchandising Business Answer Only. TH 12:00-3:00 Due Sunday 10/2 6:00 PMDocument5 pagesAssignment On Merchandising Business Answer Only. TH 12:00-3:00 Due Sunday 10/2 6:00 PMMarinella LosaNo ratings yet

- Perpetual Inventory - JOURNALDocument3 pagesPerpetual Inventory - JOURNALG09 CARGANILLA, Angelika M.No ratings yet

- Tchibo Ideas: Group5Document10 pagesTchibo Ideas: Group5Diksharth HarshNo ratings yet

- Brokerage Calculation Sapphire AnarockDocument4 pagesBrokerage Calculation Sapphire AnarockShubham DwivediNo ratings yet

- Comparative Study Report Between Adidas and NikeDocument60 pagesComparative Study Report Between Adidas and Nikeshivamgoyal390No ratings yet

- Branch Home PuzzleDocument12 pagesBranch Home PuzzleDainika ShettyNo ratings yet

- Financial Management, MBA511, Section: 01 Chapter 3: ProblemsDocument2 pagesFinancial Management, MBA511, Section: 01 Chapter 3: ProblemsShakilNo ratings yet

- Mad Keen MotorsDocument21 pagesMad Keen MotorsAljun Bonsobre100% (1)

- Designing Marketing Programs To Build Brand EquityDocument57 pagesDesigning Marketing Programs To Build Brand EquitySuman MalasNo ratings yet

- Anthony Brain Bumiller: UltravisiónDocument2 pagesAnthony Brain Bumiller: UltravisiónMaria Fernanda Camacho TorresNo ratings yet

- Chapter One: Integrated Marketing CommunicationsDocument14 pagesChapter One: Integrated Marketing CommunicationsNina MchantafNo ratings yet

- I. Manufacturing Costs ( Direct Production Cost + Fixed Charges + Plant Overhead CostDocument8 pagesI. Manufacturing Costs ( Direct Production Cost + Fixed Charges + Plant Overhead CostDEMI PADILLANo ratings yet

- Presentation 1 (VPA) Supply Chain ManagementDocument240 pagesPresentation 1 (VPA) Supply Chain ManagementArjun SinghNo ratings yet

- PRINCIPLES OF ECONOMICS Vol 1 - Za CipDocument428 pagesPRINCIPLES OF ECONOMICS Vol 1 - Za CipasasaNo ratings yet

- Quiz #1Document6 pagesQuiz #1Ioana Stroica100% (3)

- SAS#10-BAM 191 1st EXAMDocument7 pagesSAS#10-BAM 191 1st EXAMKhel SedaNo ratings yet

- Philip Roberts Resume - 2017bDocument3 pagesPhilip Roberts Resume - 2017bPhilip RobertsNo ratings yet

- Investigacion de Mercado InfografiaDocument1 pageInvestigacion de Mercado InfografiaGeidy Alexandra Jimenez RoaNo ratings yet

- Fortune 500 ProjectDocument14 pagesFortune 500 Projectcody johnsonNo ratings yet

- Social Media & Digital Marketing: About The CourseDocument1 pageSocial Media & Digital Marketing: About The CourseScottNo ratings yet

- S4 Cambridge IGCSE Revision SheetsDocument6 pagesS4 Cambridge IGCSE Revision SheetsSteven Patrick YuNo ratings yet

- WARC - What We Know About Point of Purchase and Instore MarketingDocument6 pagesWARC - What We Know About Point of Purchase and Instore MarketingJames LittlewoodNo ratings yet

- Introduction of Digital Media Chapter 1 - MyDocument2 pagesIntroduction of Digital Media Chapter 1 - MyTahseen Raza100% (1)

- Strategic Marketing MKT703: Virtual University of PakistanDocument9 pagesStrategic Marketing MKT703: Virtual University of PakistanRABIANo ratings yet

- Cohorts and Retention Playbook 3Document12 pagesCohorts and Retention Playbook 3Kratvesh PandeyNo ratings yet

- I. Accounting Methods For By-Products: Exercise 3Document2 pagesI. Accounting Methods For By-Products: Exercise 3Crescent OsamuNo ratings yet