A Dismal Quarter For Volatility But Volumes Fare Better

A Dismal Quarter For Volatility But Volumes Fare Better

You might also like

- Get Rich with Dividends: A Proven System for Earning Double-Digit ReturnsFrom EverandGet Rich with Dividends: A Proven System for Earning Double-Digit ReturnsNo ratings yet

- Portfolio Construction Using Fundamental AnalysisDocument97 pagesPortfolio Construction Using Fundamental Analysisefreggg100% (2)

- of Insider TradingDocument15 pagesof Insider TradingSpUnky Rohit100% (1)

- Ascendere Daily Update - January 27, 2011 - Companies With Expanding ROIC Tend To Surprise To The UpsideDocument16 pagesAscendere Daily Update - January 27, 2011 - Companies With Expanding ROIC Tend To Surprise To The UpsideStephen CastellanoNo ratings yet

- Extraordinary When One Looks at The Performance of The Broader Universe" As Well As WhenDocument9 pagesExtraordinary When One Looks at The Performance of The Broader Universe" As Well As Whenravi_405No ratings yet

- BetterInvesting Weekly Stock Screen 5-15-17Document1 pageBetterInvesting Weekly Stock Screen 5-15-17BetterInvestingNo ratings yet

- Iop PMSDocument31 pagesIop PMSMAULESH PATELNo ratings yet

- BetterInvesting Weekly Stock Screen 5-22-17Document1 pageBetterInvesting Weekly Stock Screen 5-22-17BetterInvestingNo ratings yet

- Dividend Payout, IPOs and Bearish Market Trend - 200512Document8 pagesDividend Payout, IPOs and Bearish Market Trend - 200512ProshareNo ratings yet

- The S&P and On To Earnings Again: .DJI 12,266.75 (+65.16) .SPX 1,312.62 (+7.48) .IXIC 2,744.97 (+9.59)Document4 pagesThe S&P and On To Earnings Again: .DJI 12,266.75 (+65.16) .SPX 1,312.62 (+7.48) .IXIC 2,744.97 (+9.59)Andre_Setiawan_1986No ratings yet

- BetterInvesting Weekly Stock Screen 11-13-17Document1 pageBetterInvesting Weekly Stock Screen 11-13-17BetterInvestingNo ratings yet

- IDX Capital Market Investment Outlook 2018 - Tito Sulistio - 31 Oct 2017Document28 pagesIDX Capital Market Investment Outlook 2018 - Tito Sulistio - 31 Oct 2017Essantio DeniraNo ratings yet

- Aggressive Recommended Basket 02 Mar 16Document25 pagesAggressive Recommended Basket 02 Mar 16nnsriniNo ratings yet

- Allergan PLC.: Price, Consensus & SurpriseDocument1 pageAllergan PLC.: Price, Consensus & Surprisederek_2010No ratings yet

- Weekly Wrap For The Week Ended 270919Document1 pageWeekly Wrap For The Week Ended 270919Dilkaran SinghNo ratings yet

- BetterInvesting Weekly Stock Screen 2-5-18Document1 pageBetterInvesting Weekly Stock Screen 2-5-18BetterInvestingNo ratings yet

- History Favours The BraveDocument4 pagesHistory Favours The BraveNaresh KumarNo ratings yet

- BetterInvesting Weekly Stock Screen 2-27-17Document1 pageBetterInvesting Weekly Stock Screen 2-27-17BetterInvestingNo ratings yet

- BetterInvesting Weekly Stock Screen 9-9-19Document1 pageBetterInvesting Weekly Stock Screen 9-9-19BetterInvestingNo ratings yet

- BetterInvesting Weekly Stock Screen 10-10-16Document1 pageBetterInvesting Weekly Stock Screen 10-10-16BetterInvestingNo ratings yet

- Quantletter Q30Document3 pagesQuantletter Q30pareshpatel99No ratings yet

- Zydus Wellness Q3FY17 - Result Update - Axis Direct - 03022017 - 07-02-2017 - 14Document5 pagesZydus Wellness Q3FY17 - Result Update - Axis Direct - 03022017 - 07-02-2017 - 14ameya_rathodNo ratings yet

- Questions FolderDocument20 pagesQuestions FolderfaraNo ratings yet

- Running Head: RESEARCH PAPER 1: Name Institutional Affiliation DateDocument5 pagesRunning Head: RESEARCH PAPER 1: Name Institutional Affiliation DateSana FarhanNo ratings yet

- Kenanga Today 240116 KenangaDocument6 pagesKenanga Today 240116 KenangaChee TonyNo ratings yet

- BetterInvesting Weekly Stock Screen 12-18-17Document1 pageBetterInvesting Weekly Stock Screen 12-18-17BetterInvestingNo ratings yet

- BetterInvesting Weekly Stock Screen 4-16-18Document1 pageBetterInvesting Weekly Stock Screen 4-16-18BetterInvestingNo ratings yet

- CMP: Inr1713 TP: Inr2260 (+32%) Buy: Can Fin HomesDocument2 pagesCMP: Inr1713 TP: Inr2260 (+32%) Buy: Can Fin HomesmilandeepNo ratings yet

- Inners & Osers: .DJI 12,319.73 (-30.88) .SPX 1,328.26 (-2.43) .IXIC 2,776.79 (+4.28)Document5 pagesInners & Osers: .DJI 12,319.73 (-30.88) .SPX 1,328.26 (-2.43) .IXIC 2,776.79 (+4.28)Andre SetiawanNo ratings yet

- 2022.07 Pavise Monthly Letter FlagshipDocument4 pages2022.07 Pavise Monthly Letter FlagshipKan ZhouNo ratings yet

- Key Tenets To Reduce Risks While Investing in EquitDocument8 pagesKey Tenets To Reduce Risks While Investing in EquitdigthreeNo ratings yet

- Monthly Report Aug 23 SeriesDocument17 pagesMonthly Report Aug 23 SeriesAyushi ShahNo ratings yet

- Technofunda Investing Excel Analysis - Version 2.0: Watch Screener TutorialDocument37 pagesTechnofunda Investing Excel Analysis - Version 2.0: Watch Screener TutorialRaman BajpaiNo ratings yet

- Project Report: Investment Analysis & Portfolio ManagementDocument8 pagesProject Report: Investment Analysis & Portfolio ManagementAnkita GoyalNo ratings yet

- Orporate Ews: .DJI 12,214.38 .SPX 1,321.82 .IXIC 2,765.77Document5 pagesOrporate Ews: .DJI 12,214.38 .SPX 1,321.82 .IXIC 2,765.77Andre SetiawanNo ratings yet

- BetterInvesting Weekly Stock Screen 11-5-18Document1 pageBetterInvesting Weekly Stock Screen 11-5-18BetterInvestingNo ratings yet

- BetterInvesting Weekly Stock Screen 7-17-17Document1 pageBetterInvesting Weekly Stock Screen 7-17-17BetterInvestingNo ratings yet

- Module1-Assignment 1 - 2017ABPS1332HDocument7 pagesModule1-Assignment 1 - 2017ABPS1332HNamitNo ratings yet

- Vaibhav Global Q4FY17 - Result Update - Axis Direct - 23052017 - 23!05!2017 - 14Document3 pagesVaibhav Global Q4FY17 - Result Update - Axis Direct - 23052017 - 23!05!2017 - 14Rohan ChauhanNo ratings yet

- American Life Insurance CompanyDocument13 pagesAmerican Life Insurance CompanyPatrick NokrekNo ratings yet

- BetterInvesting Weekly Stock Screen 11-6-17.xlxsDocument1 pageBetterInvesting Weekly Stock Screen 11-6-17.xlxsBetterInvesting100% (1)

- BetterInvesting Weekly Stock Screen 12-4-17Document1 pageBetterInvesting Weekly Stock Screen 12-4-17BetterInvestingNo ratings yet

- BetterInvesing Weekly Stock Screen 12-3-18Document1 pageBetterInvesing Weekly Stock Screen 12-3-18BetterInvesting100% (1)

- BetterInvesting Weekly Stock Screen 11-12-18Document1 pageBetterInvesting Weekly Stock Screen 11-12-18BetterInvestingNo ratings yet

- Or No Shutdown?Document6 pagesOr No Shutdown?Andre_Setiawan_1986No ratings yet

- Investor Diary Beginner Stock Analysis Excel (V-1) : How To Use This Spreadsheet?Document56 pagesInvestor Diary Beginner Stock Analysis Excel (V-1) : How To Use This Spreadsheet?SumitNo ratings yet

- Evercore Partners 8.6.13 PDFDocument6 pagesEvercore Partners 8.6.13 PDFChad Thayer VNo ratings yet

- Q3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleDocument12 pagesQ3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleSAGAR VAZIRANINo ratings yet

- Asustek: 3Q 2017 Investor ConferenceDocument30 pagesAsustek: 3Q 2017 Investor ConferenceAnthonyNo ratings yet

- BetterInvesting Weekly Stock Screen 8-7-17Document1 pageBetterInvesting Weekly Stock Screen 8-7-17BetterInvestingNo ratings yet

- Financial Accounting Assignment On Midcap: South Indian BankDocument28 pagesFinancial Accounting Assignment On Midcap: South Indian BankANKIT YADAVNo ratings yet

- Perhitungan Harga Wajar Bank Bca Tahun 2017 - 2018Document3 pagesPerhitungan Harga Wajar Bank Bca Tahun 2017 - 2018Jamaludin sihagNo ratings yet

- ICICI Prudential MF Head Start - 07062022Document2 pagesICICI Prudential MF Head Start - 07062022Chucha LullNo ratings yet

- EQTY Research Property Development UPDCDocument13 pagesEQTY Research Property Development UPDCavomanijNo ratings yet

- BetterInvesting Weekly Stock Screen 10-9-17Document1 pageBetterInvesting Weekly Stock Screen 10-9-17BetterInvestingNo ratings yet

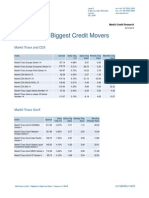

- Markit News: Biggest Credit Movers: Markit Itraxx and CDXDocument5 pagesMarkit News: Biggest Credit Movers: Markit Itraxx and CDXAndrea MacettiNo ratings yet

- Mansek Investor Digest 29 May 2024 - AVIA, 4M24 BNGA BNLIDocument6 pagesMansek Investor Digest 29 May 2024 - AVIA, 4M24 BNGA BNLIAndreas PaskalisNo ratings yet

- Beyond Smart Beta: Index Investment Strategies for Active Portfolio ManagementFrom EverandBeyond Smart Beta: Index Investment Strategies for Active Portfolio ManagementNo ratings yet

- Mongolia's Economic Prospects: Resource-Rich and Landlocked Between Two GiantsFrom EverandMongolia's Economic Prospects: Resource-Rich and Landlocked Between Two GiantsNo ratings yet

- Tile, Marble, Terrazzo & Mosaic Contractors World Summary: Market Values & Financials by CountryFrom EverandTile, Marble, Terrazzo & Mosaic Contractors World Summary: Market Values & Financials by CountryNo ratings yet

- Answer - Practice Question 1 - Statement of Changes in Equity.Document2 pagesAnswer - Practice Question 1 - Statement of Changes in Equity.Rizzy Ice-cream Milo0% (1)

- Tech ProDocument574 pagesTech ProMurali KrishnaNo ratings yet

- Investor Digest 23 Oktober 2019Document10 pagesInvestor Digest 23 Oktober 2019Rising PKN STANNo ratings yet

- Nego Reviewer (Finals)Document12 pagesNego Reviewer (Finals)jianmargareth100% (4)

- Sec MC 28 S2020Document1 pageSec MC 28 S2020mildredNo ratings yet

- New Microsoft Word DocumentDocument6 pagesNew Microsoft Word DocumentCharmi SatraNo ratings yet

- Debentures ProjectDocument28 pagesDebentures ProjectMT RA100% (1)

- Swift Standars 9 CategoryDocument173 pagesSwift Standars 9 Categoryliittokivi100% (1)

- Foreign Exchange Market in IndiaDocument14 pagesForeign Exchange Market in IndiaMukesh ManwaniNo ratings yet

- Time Value of Money: Pooja GuptaDocument24 pagesTime Value of Money: Pooja GuptaRagh KrishhNo ratings yet

- Chap 001Document29 pagesChap 001frankmarson100% (1)

- Answer To PTP - Final - Syllabus 2012 - Dec2014 - Set 2Document23 pagesAnswer To PTP - Final - Syllabus 2012 - Dec2014 - Set 2Cẩm ChiNo ratings yet

- Retail Trade: Foreign Investors: Sec Opinion No. 35-04Document3 pagesRetail Trade: Foreign Investors: Sec Opinion No. 35-04Shiela Hoylar-GasconNo ratings yet

- JPM - Cap and FloorDocument7 pagesJPM - Cap and FloorRR BakshNo ratings yet

- Derivatives and Foreign Currency TransacDocument2 pagesDerivatives and Foreign Currency TransacJade jade jadeNo ratings yet

- QP Accountancy XIIDocument9 pagesQP Accountancy XIITûshar ThakúrNo ratings yet

- Hot or Not PDFDocument1 pageHot or Not PDFJotham SederstromNo ratings yet

- Business Combination and Consolidation On Acquisition Date (Summary)Document6 pagesBusiness Combination and Consolidation On Acquisition Date (Summary)Ma Hadassa O. Foliente33% (3)

- Practical Accounting 1Document14 pagesPractical Accounting 1Anonymous Lih1laaxNo ratings yet

- #2 - What Do You Think This Company Does Right? What Do You Think We Do Wrong?Document8 pages#2 - What Do You Think This Company Does Right? What Do You Think We Do Wrong?helloNo ratings yet

- Real Estate FinanceDocument33 pagesReal Estate FinanceAVICK BISWASNo ratings yet

- Amendments To Fourth and Fifth Schedule To The Companies Ordinance, 1984Document5 pagesAmendments To Fourth and Fifth Schedule To The Companies Ordinance, 1984Khalid MahmoodNo ratings yet

- Allen Stanford Criminal Trial Transcript Volume 11 Feb. 6, 2012Document317 pagesAllen Stanford Criminal Trial Transcript Volume 11 Feb. 6, 2012Stanford Victims CoalitionNo ratings yet

- Course Outline BA142Document4 pagesCourse Outline BA142Marinette Baquiran Dela FuenteNo ratings yet

- Chapter 12 Determinants of Beta and WACCDocument7 pagesChapter 12 Determinants of Beta and WACCAbdul-Aziz A. AldayelNo ratings yet

- Annexure I PDFDocument7 pagesAnnexure I PDFRenjithNo ratings yet

- Metallgesellschaft AG: A Case StudyDocument24 pagesMetallgesellschaft AG: A Case StudyTariq KhanNo ratings yet

- Lawsuit Against Tribune Publishing Over Stock SaleDocument28 pagesLawsuit Against Tribune Publishing Over Stock SalecraignewmanNo ratings yet

Download as pdf or txt

You might also like

- Get Rich with Dividends: A Proven System for Earning Double-Digit ReturnsFrom EverandGet Rich with Dividends: A Proven System for Earning Double-Digit ReturnsNo ratings yet

- Portfolio Construction Using Fundamental AnalysisDocument97 pagesPortfolio Construction Using Fundamental Analysisefreggg100% (2)

- of Insider TradingDocument15 pagesof Insider TradingSpUnky Rohit100% (1)

- Ascendere Daily Update - January 27, 2011 - Companies With Expanding ROIC Tend To Surprise To The UpsideDocument16 pagesAscendere Daily Update - January 27, 2011 - Companies With Expanding ROIC Tend To Surprise To The UpsideStephen CastellanoNo ratings yet

- Extraordinary When One Looks at The Performance of The Broader Universe" As Well As WhenDocument9 pagesExtraordinary When One Looks at The Performance of The Broader Universe" As Well As Whenravi_405No ratings yet

- BetterInvesting Weekly Stock Screen 5-15-17Document1 pageBetterInvesting Weekly Stock Screen 5-15-17BetterInvestingNo ratings yet

- Iop PMSDocument31 pagesIop PMSMAULESH PATELNo ratings yet

- BetterInvesting Weekly Stock Screen 5-22-17Document1 pageBetterInvesting Weekly Stock Screen 5-22-17BetterInvestingNo ratings yet

- Dividend Payout, IPOs and Bearish Market Trend - 200512Document8 pagesDividend Payout, IPOs and Bearish Market Trend - 200512ProshareNo ratings yet

- The S&P and On To Earnings Again: .DJI 12,266.75 (+65.16) .SPX 1,312.62 (+7.48) .IXIC 2,744.97 (+9.59)Document4 pagesThe S&P and On To Earnings Again: .DJI 12,266.75 (+65.16) .SPX 1,312.62 (+7.48) .IXIC 2,744.97 (+9.59)Andre_Setiawan_1986No ratings yet

- BetterInvesting Weekly Stock Screen 11-13-17Document1 pageBetterInvesting Weekly Stock Screen 11-13-17BetterInvestingNo ratings yet

- IDX Capital Market Investment Outlook 2018 - Tito Sulistio - 31 Oct 2017Document28 pagesIDX Capital Market Investment Outlook 2018 - Tito Sulistio - 31 Oct 2017Essantio DeniraNo ratings yet

- Aggressive Recommended Basket 02 Mar 16Document25 pagesAggressive Recommended Basket 02 Mar 16nnsriniNo ratings yet

- Allergan PLC.: Price, Consensus & SurpriseDocument1 pageAllergan PLC.: Price, Consensus & Surprisederek_2010No ratings yet

- Weekly Wrap For The Week Ended 270919Document1 pageWeekly Wrap For The Week Ended 270919Dilkaran SinghNo ratings yet

- BetterInvesting Weekly Stock Screen 2-5-18Document1 pageBetterInvesting Weekly Stock Screen 2-5-18BetterInvestingNo ratings yet

- History Favours The BraveDocument4 pagesHistory Favours The BraveNaresh KumarNo ratings yet

- BetterInvesting Weekly Stock Screen 2-27-17Document1 pageBetterInvesting Weekly Stock Screen 2-27-17BetterInvestingNo ratings yet

- BetterInvesting Weekly Stock Screen 9-9-19Document1 pageBetterInvesting Weekly Stock Screen 9-9-19BetterInvestingNo ratings yet

- BetterInvesting Weekly Stock Screen 10-10-16Document1 pageBetterInvesting Weekly Stock Screen 10-10-16BetterInvestingNo ratings yet

- Quantletter Q30Document3 pagesQuantletter Q30pareshpatel99No ratings yet

- Zydus Wellness Q3FY17 - Result Update - Axis Direct - 03022017 - 07-02-2017 - 14Document5 pagesZydus Wellness Q3FY17 - Result Update - Axis Direct - 03022017 - 07-02-2017 - 14ameya_rathodNo ratings yet

- Questions FolderDocument20 pagesQuestions FolderfaraNo ratings yet

- Running Head: RESEARCH PAPER 1: Name Institutional Affiliation DateDocument5 pagesRunning Head: RESEARCH PAPER 1: Name Institutional Affiliation DateSana FarhanNo ratings yet

- Kenanga Today 240116 KenangaDocument6 pagesKenanga Today 240116 KenangaChee TonyNo ratings yet

- BetterInvesting Weekly Stock Screen 12-18-17Document1 pageBetterInvesting Weekly Stock Screen 12-18-17BetterInvestingNo ratings yet

- BetterInvesting Weekly Stock Screen 4-16-18Document1 pageBetterInvesting Weekly Stock Screen 4-16-18BetterInvestingNo ratings yet

- CMP: Inr1713 TP: Inr2260 (+32%) Buy: Can Fin HomesDocument2 pagesCMP: Inr1713 TP: Inr2260 (+32%) Buy: Can Fin HomesmilandeepNo ratings yet

- Inners & Osers: .DJI 12,319.73 (-30.88) .SPX 1,328.26 (-2.43) .IXIC 2,776.79 (+4.28)Document5 pagesInners & Osers: .DJI 12,319.73 (-30.88) .SPX 1,328.26 (-2.43) .IXIC 2,776.79 (+4.28)Andre SetiawanNo ratings yet

- 2022.07 Pavise Monthly Letter FlagshipDocument4 pages2022.07 Pavise Monthly Letter FlagshipKan ZhouNo ratings yet

- Key Tenets To Reduce Risks While Investing in EquitDocument8 pagesKey Tenets To Reduce Risks While Investing in EquitdigthreeNo ratings yet

- Monthly Report Aug 23 SeriesDocument17 pagesMonthly Report Aug 23 SeriesAyushi ShahNo ratings yet

- Technofunda Investing Excel Analysis - Version 2.0: Watch Screener TutorialDocument37 pagesTechnofunda Investing Excel Analysis - Version 2.0: Watch Screener TutorialRaman BajpaiNo ratings yet

- Project Report: Investment Analysis & Portfolio ManagementDocument8 pagesProject Report: Investment Analysis & Portfolio ManagementAnkita GoyalNo ratings yet

- Orporate Ews: .DJI 12,214.38 .SPX 1,321.82 .IXIC 2,765.77Document5 pagesOrporate Ews: .DJI 12,214.38 .SPX 1,321.82 .IXIC 2,765.77Andre SetiawanNo ratings yet

- BetterInvesting Weekly Stock Screen 11-5-18Document1 pageBetterInvesting Weekly Stock Screen 11-5-18BetterInvestingNo ratings yet

- BetterInvesting Weekly Stock Screen 7-17-17Document1 pageBetterInvesting Weekly Stock Screen 7-17-17BetterInvestingNo ratings yet

- Module1-Assignment 1 - 2017ABPS1332HDocument7 pagesModule1-Assignment 1 - 2017ABPS1332HNamitNo ratings yet

- Vaibhav Global Q4FY17 - Result Update - Axis Direct - 23052017 - 23!05!2017 - 14Document3 pagesVaibhav Global Q4FY17 - Result Update - Axis Direct - 23052017 - 23!05!2017 - 14Rohan ChauhanNo ratings yet

- American Life Insurance CompanyDocument13 pagesAmerican Life Insurance CompanyPatrick NokrekNo ratings yet

- BetterInvesting Weekly Stock Screen 11-6-17.xlxsDocument1 pageBetterInvesting Weekly Stock Screen 11-6-17.xlxsBetterInvesting100% (1)

- BetterInvesting Weekly Stock Screen 12-4-17Document1 pageBetterInvesting Weekly Stock Screen 12-4-17BetterInvestingNo ratings yet

- BetterInvesing Weekly Stock Screen 12-3-18Document1 pageBetterInvesing Weekly Stock Screen 12-3-18BetterInvesting100% (1)

- BetterInvesting Weekly Stock Screen 11-12-18Document1 pageBetterInvesting Weekly Stock Screen 11-12-18BetterInvestingNo ratings yet

- Or No Shutdown?Document6 pagesOr No Shutdown?Andre_Setiawan_1986No ratings yet

- Investor Diary Beginner Stock Analysis Excel (V-1) : How To Use This Spreadsheet?Document56 pagesInvestor Diary Beginner Stock Analysis Excel (V-1) : How To Use This Spreadsheet?SumitNo ratings yet

- Evercore Partners 8.6.13 PDFDocument6 pagesEvercore Partners 8.6.13 PDFChad Thayer VNo ratings yet

- Q3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleDocument12 pagesQ3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleSAGAR VAZIRANINo ratings yet

- Asustek: 3Q 2017 Investor ConferenceDocument30 pagesAsustek: 3Q 2017 Investor ConferenceAnthonyNo ratings yet

- BetterInvesting Weekly Stock Screen 8-7-17Document1 pageBetterInvesting Weekly Stock Screen 8-7-17BetterInvestingNo ratings yet

- Financial Accounting Assignment On Midcap: South Indian BankDocument28 pagesFinancial Accounting Assignment On Midcap: South Indian BankANKIT YADAVNo ratings yet

- Perhitungan Harga Wajar Bank Bca Tahun 2017 - 2018Document3 pagesPerhitungan Harga Wajar Bank Bca Tahun 2017 - 2018Jamaludin sihagNo ratings yet

- ICICI Prudential MF Head Start - 07062022Document2 pagesICICI Prudential MF Head Start - 07062022Chucha LullNo ratings yet

- EQTY Research Property Development UPDCDocument13 pagesEQTY Research Property Development UPDCavomanijNo ratings yet

- BetterInvesting Weekly Stock Screen 10-9-17Document1 pageBetterInvesting Weekly Stock Screen 10-9-17BetterInvestingNo ratings yet

- Markit News: Biggest Credit Movers: Markit Itraxx and CDXDocument5 pagesMarkit News: Biggest Credit Movers: Markit Itraxx and CDXAndrea MacettiNo ratings yet

- Mansek Investor Digest 29 May 2024 - AVIA, 4M24 BNGA BNLIDocument6 pagesMansek Investor Digest 29 May 2024 - AVIA, 4M24 BNGA BNLIAndreas PaskalisNo ratings yet

- Beyond Smart Beta: Index Investment Strategies for Active Portfolio ManagementFrom EverandBeyond Smart Beta: Index Investment Strategies for Active Portfolio ManagementNo ratings yet

- Mongolia's Economic Prospects: Resource-Rich and Landlocked Between Two GiantsFrom EverandMongolia's Economic Prospects: Resource-Rich and Landlocked Between Two GiantsNo ratings yet

- Tile, Marble, Terrazzo & Mosaic Contractors World Summary: Market Values & Financials by CountryFrom EverandTile, Marble, Terrazzo & Mosaic Contractors World Summary: Market Values & Financials by CountryNo ratings yet

- Answer - Practice Question 1 - Statement of Changes in Equity.Document2 pagesAnswer - Practice Question 1 - Statement of Changes in Equity.Rizzy Ice-cream Milo0% (1)

- Tech ProDocument574 pagesTech ProMurali KrishnaNo ratings yet

- Investor Digest 23 Oktober 2019Document10 pagesInvestor Digest 23 Oktober 2019Rising PKN STANNo ratings yet

- Nego Reviewer (Finals)Document12 pagesNego Reviewer (Finals)jianmargareth100% (4)

- Sec MC 28 S2020Document1 pageSec MC 28 S2020mildredNo ratings yet

- New Microsoft Word DocumentDocument6 pagesNew Microsoft Word DocumentCharmi SatraNo ratings yet

- Debentures ProjectDocument28 pagesDebentures ProjectMT RA100% (1)

- Swift Standars 9 CategoryDocument173 pagesSwift Standars 9 Categoryliittokivi100% (1)

- Foreign Exchange Market in IndiaDocument14 pagesForeign Exchange Market in IndiaMukesh ManwaniNo ratings yet

- Time Value of Money: Pooja GuptaDocument24 pagesTime Value of Money: Pooja GuptaRagh KrishhNo ratings yet

- Chap 001Document29 pagesChap 001frankmarson100% (1)

- Answer To PTP - Final - Syllabus 2012 - Dec2014 - Set 2Document23 pagesAnswer To PTP - Final - Syllabus 2012 - Dec2014 - Set 2Cẩm ChiNo ratings yet

- Retail Trade: Foreign Investors: Sec Opinion No. 35-04Document3 pagesRetail Trade: Foreign Investors: Sec Opinion No. 35-04Shiela Hoylar-GasconNo ratings yet

- JPM - Cap and FloorDocument7 pagesJPM - Cap and FloorRR BakshNo ratings yet

- Derivatives and Foreign Currency TransacDocument2 pagesDerivatives and Foreign Currency TransacJade jade jadeNo ratings yet

- QP Accountancy XIIDocument9 pagesQP Accountancy XIITûshar ThakúrNo ratings yet

- Hot or Not PDFDocument1 pageHot or Not PDFJotham SederstromNo ratings yet

- Business Combination and Consolidation On Acquisition Date (Summary)Document6 pagesBusiness Combination and Consolidation On Acquisition Date (Summary)Ma Hadassa O. Foliente33% (3)

- Practical Accounting 1Document14 pagesPractical Accounting 1Anonymous Lih1laaxNo ratings yet

- #2 - What Do You Think This Company Does Right? What Do You Think We Do Wrong?Document8 pages#2 - What Do You Think This Company Does Right? What Do You Think We Do Wrong?helloNo ratings yet

- Real Estate FinanceDocument33 pagesReal Estate FinanceAVICK BISWASNo ratings yet

- Amendments To Fourth and Fifth Schedule To The Companies Ordinance, 1984Document5 pagesAmendments To Fourth and Fifth Schedule To The Companies Ordinance, 1984Khalid MahmoodNo ratings yet

- Allen Stanford Criminal Trial Transcript Volume 11 Feb. 6, 2012Document317 pagesAllen Stanford Criminal Trial Transcript Volume 11 Feb. 6, 2012Stanford Victims CoalitionNo ratings yet

- Course Outline BA142Document4 pagesCourse Outline BA142Marinette Baquiran Dela FuenteNo ratings yet

- Chapter 12 Determinants of Beta and WACCDocument7 pagesChapter 12 Determinants of Beta and WACCAbdul-Aziz A. AldayelNo ratings yet

- Annexure I PDFDocument7 pagesAnnexure I PDFRenjithNo ratings yet

- Metallgesellschaft AG: A Case StudyDocument24 pagesMetallgesellschaft AG: A Case StudyTariq KhanNo ratings yet

- Lawsuit Against Tribune Publishing Over Stock SaleDocument28 pagesLawsuit Against Tribune Publishing Over Stock SalecraignewmanNo ratings yet