Download as docx, pdf, or txt

You might also like

- General Conditions of Contract - Qatar - May 2007Document58 pagesGeneral Conditions of Contract - Qatar - May 2007Indula Siriwikum82% (17)

- Toyota Auris Corolla 2007 2013 Electrical Wiring DiagramDocument22 pagesToyota Auris Corolla 2007 2013 Electrical Wiring Diagrampriscillasalas040195ori100% (129)

- List of Transpo CasesDocument7 pagesList of Transpo CasesRodesa Lara Fea BongalonNo ratings yet

- Board Resolution-Commonwealth Rural Bank (Gangan)Document6 pagesBoard Resolution-Commonwealth Rural Bank (Gangan)Gaspar ascoNo ratings yet

- Col CasesDocument42 pagesCol CasesABNo ratings yet

- RCBC VS CaDocument2 pagesRCBC VS CaJan Rhoneil SantillanaNo ratings yet

- A. Soriano Aviation v. Employees Association of A. Soriano AviationDocument15 pagesA. Soriano Aviation v. Employees Association of A. Soriano AviationAnnie Herrera-LimNo ratings yet

- 20-Nonay V Bahia Shipping-2016Document4 pages20-Nonay V Bahia Shipping-2016Von VelascoNo ratings yet

- Insurance Lecture Notes ROXASDocument34 pagesInsurance Lecture Notes ROXASjerico lopezNo ratings yet

- Perez vs. HermanoDocument7 pagesPerez vs. HermanoRomy Ian LimNo ratings yet

- Complaint Against Count I AnDocument2 pagesComplaint Against Count I AnLea Tiffany LaohooNo ratings yet

- FsadasgfasDocument4 pagesFsadasgfassovxxxNo ratings yet

- Sales - 1 & 2Document23 pagesSales - 1 & 2innabNo ratings yet

- Batch 1 Case 3 Quinagoran Vs CADocument2 pagesBatch 1 Case 3 Quinagoran Vs CALex D. TabilogNo ratings yet

- Case Title: Gulf Resorts vs. Pcic G.R. No. 156167, May 16, 2005Document1 pageCase Title: Gulf Resorts vs. Pcic G.R. No. 156167, May 16, 2005Brey VelascoNo ratings yet

- Mercrev2 PDFDocument42 pagesMercrev2 PDFManuel VillanuevaNo ratings yet

- Jurisdiction of Cta Enbanc and DivisionDocument12 pagesJurisdiction of Cta Enbanc and DivisionJune Karl CepidaNo ratings yet

- Heirs of Ildelfonso CoscolluelaDocument1 pageHeirs of Ildelfonso CoscolluelaMaricar Corina CanayaNo ratings yet

- 21Document1 page21James WilliamNo ratings yet

- de Santos Versus City of ManilaDocument8 pagesde Santos Versus City of ManilaAnskee TejamNo ratings yet

- Insurance CodalDocument3 pagesInsurance CodalsakuraNo ratings yet

- Dlsu Pil Jan 2016Document28 pagesDlsu Pil Jan 2016Villar John EzraNo ratings yet

- 7 Authorized Driver Clause Vs Theft ClauseDocument2 pages7 Authorized Driver Clause Vs Theft ClauseJaymee Andomang Os-agNo ratings yet

- Case Study #3Document4 pagesCase Study #3Annie Morrison AshtonNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument17 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledGhatz CondaNo ratings yet

- CONFLICTSDocument7 pagesCONFLICTSIrish PrecionNo ratings yet

- 8 Villarico V SarmientoDocument5 pages8 Villarico V SarmientoLawrence RiodequeNo ratings yet

- Lam v. Kodak PhilippinesDocument16 pagesLam v. Kodak PhilippinesRam AdriasNo ratings yet

- Receivership CasesDocument12 pagesReceivership Casesjim peterick sisonNo ratings yet

- 13sara Vs AgarradoDocument2 pages13sara Vs Agarradojohn ryan anatanNo ratings yet

- Johannes Schuback & Sons Philippine Trading Corp. vs. Court of AppealsDocument5 pagesJohannes Schuback & Sons Philippine Trading Corp. vs. Court of AppealsKate DomingoNo ratings yet

- Southern Lines Inc VS CA With Case DigestDocument4 pagesSouthern Lines Inc VS CA With Case DigestteepeeNo ratings yet

- Laura Velasco and Greta AcostaDocument4 pagesLaura Velasco and Greta AcostaSor ElleNo ratings yet

- 28 - Misamis Lumber Corp. v. Capital Insurance & Surety Co., Inc PDFDocument3 pages28 - Misamis Lumber Corp. v. Capital Insurance & Surety Co., Inc PDFKaryl Eric BardelasNo ratings yet

- Colegio de San Juan de Letran Vs Assn of Employees and Faculty of Letran GR 141471 Sept 18 2000 DigestDocument1 pageColegio de San Juan de Letran Vs Assn of Employees and Faculty of Letran GR 141471 Sept 18 2000 DigestMarkus AureliusNo ratings yet

- ASSIGNMENT - Gamit Leg MedDocument6 pagesASSIGNMENT - Gamit Leg MedIsabela Act CisNo ratings yet

- (A. Subject Matter) Paramount Insurance Corporation vs. Remondeulaz, 686 SCRA 567, G.R. No. 173773 November 28, 2012Document6 pages(A. Subject Matter) Paramount Insurance Corporation vs. Remondeulaz, 686 SCRA 567, G.R. No. 173773 November 28, 2012Alexiss Mace JuradoNo ratings yet

- Pil Summer SyllabusDocument10 pagesPil Summer SyllabusMika SantiagoNo ratings yet

- 48 Philippine American Life Insurance Co. v. PinedaDocument3 pages48 Philippine American Life Insurance Co. v. PinedaKaryl Eric BardelasNo ratings yet

- Torts Case Digests For FinalsDocument27 pagesTorts Case Digests For FinalsGerli Therese AbrilloNo ratings yet

- 3y1s Tax F 1 FullshemDocument38 pages3y1s Tax F 1 FullshemWolf DenNo ratings yet

- Heirs of Ildelfonso Coscolluela SR Inc Vs Rico General Insurance Corp 179 SCRA 511 Case DigestDocument3 pagesHeirs of Ildelfonso Coscolluela SR Inc Vs Rico General Insurance Corp 179 SCRA 511 Case DigestAriana Cristelle L. Pagdanganan100% (1)

- 50 - Pioneer Insurance vs. Olivia YapDocument1 page50 - Pioneer Insurance vs. Olivia YapN.SantosNo ratings yet

- Zafra-vs-CADocument10 pagesZafra-vs-CAMariam PetillaNo ratings yet

- Hall v. Piccio 86 Phil 603 (1950)Document3 pagesHall v. Piccio 86 Phil 603 (1950)gcantiverosNo ratings yet

- Agad V MabatoDocument3 pagesAgad V MabatoHudson CeeNo ratings yet

- Rule 19 - InterventionDocument5 pagesRule 19 - InterventionJereca Ubando JubaNo ratings yet

- Commissioner v. Burroughs, 142 SCRA 324 (1986) PDFDocument4 pagesCommissioner v. Burroughs, 142 SCRA 324 (1986) PDFHazel FernandezNo ratings yet

- (Torts) 21 - Wright V Manila Electric - LimDocument3 pages(Torts) 21 - Wright V Manila Electric - LimJosiah LimNo ratings yet

- Equitable Leasing Corporation vs. SuyomDocument16 pagesEquitable Leasing Corporation vs. SuyomsnhlaoNo ratings yet

- 10 Geagonia V CA G.R. No. 114427 February 6, 1995Document10 pages10 Geagonia V CA G.R. No. 114427 February 6, 1995ZydalgLadyz NeadNo ratings yet

- Insurance 2 - Ong - RCBC V CADocument2 pagesInsurance 2 - Ong - RCBC V CADaniel OngNo ratings yet

- Paternity Leave Act of 1996Document3 pagesPaternity Leave Act of 1996Anne BiagtanNo ratings yet

- Annulment, Divorce and Legal Separation in The PhilsDocument5 pagesAnnulment, Divorce and Legal Separation in The PhilsJocelyn HerreraNo ratings yet

- G.R. No 174689Document8 pagesG.R. No 174689Arste GimoNo ratings yet

- Valenzuela Vs Kalayaan OnwardsDocument9 pagesValenzuela Vs Kalayaan OnwardsAmanda ButtkissNo ratings yet

- PD 705 - "Revised Forestry Code of The Philippines." Criminal Offenses and PenaltiesDocument44 pagesPD 705 - "Revised Forestry Code of The Philippines." Criminal Offenses and PenaltiesJannina Pinson RanceNo ratings yet

- Baguio Vs NLRCDocument1 pageBaguio Vs NLRCHeidiPagdangananNo ratings yet

- 54-Wellington Investment & MFG Corp. vs. Trajano, Et Al.Document4 pages54-Wellington Investment & MFG Corp. vs. Trajano, Et Al.Nimpa Pichay100% (1)

- Chongoy V People GR No. 173824 August 28, 2008Document32 pagesChongoy V People GR No. 173824 August 28, 2008Mike E DmNo ratings yet

- Negado V MakabentaDocument2 pagesNegado V MakabentaAnonymous WiMoSEqIdNo ratings yet

- Armando L. Abad, Sr. For Plaintiff-Appellant. Gamelo, Francisco and Aquino For Defendant-AppelleeDocument9 pagesArmando L. Abad, Sr. For Plaintiff-Appellant. Gamelo, Francisco and Aquino For Defendant-AppelleeasdfghjklmppNo ratings yet

- Republic vs. ObrecidoDocument3 pagesRepublic vs. ObrecidoAnonymous 33LIOv6LNo ratings yet

- Perkins vs. DizonDocument3 pagesPerkins vs. DizonAnonymous 33LIOv6LNo ratings yet

- Gotesco Investment Corp. vs. ChattoDocument6 pagesGotesco Investment Corp. vs. ChattoAnonymous 33LIOv6LNo ratings yet

- People vs. HectoDocument5 pagesPeople vs. HectoAnonymous 33LIOv6LNo ratings yet

- China Airlines vs. Daniel ChiokDocument7 pagesChina Airlines vs. Daniel ChiokAnonymous 33LIOv6LNo ratings yet

- People vs. Mora DumpoDocument1 pagePeople vs. Mora DumpoAnonymous 33LIOv6LNo ratings yet

- Bryan vs. Eastern & Australian S.S. Co.Document2 pagesBryan vs. Eastern & Australian S.S. Co.Anonymous 33LIOv6LNo ratings yet

- Santos vs. Northwest Orient AirlinesDocument6 pagesSantos vs. Northwest Orient AirlinesAnonymous 33LIOv6LNo ratings yet

- Molina vs. de RivaDocument3 pagesMolina vs. de RivaAnonymous 33LIOv6LNo ratings yet

- Garcia vs. RecioDocument4 pagesGarcia vs. RecioAnonymous 33LIOv6LNo ratings yet

- King Mau Wu vs. SycipDocument2 pagesKing Mau Wu vs. SycipAnonymous 33LIOv6LNo ratings yet

- Western Equiptment Co. Vs ReyesDocument5 pagesWestern Equiptment Co. Vs ReyesAnonymous 33LIOv6LNo ratings yet

- Saudi Arabian Airline vs. CADocument6 pagesSaudi Arabian Airline vs. CAAnonymous 33LIOv6LNo ratings yet

- Transworld Airlines vs. CADocument2 pagesTransworld Airlines vs. CAAnonymous 33LIOv6LNo ratings yet

- Ayala Corp vs. Ray Buston Dev. CorpDocument9 pagesAyala Corp vs. Ray Buston Dev. CorpAnonymous 33LIOv6LNo ratings yet

- Gotesco Investment Corp. vs. ChattoDocument6 pagesGotesco Investment Corp. vs. ChattoAnonymous 33LIOv6LNo ratings yet

- Lalman Shukla Vs Gauri Dutt - Case Study: Submitted To Submitted byDocument12 pagesLalman Shukla Vs Gauri Dutt - Case Study: Submitted To Submitted byprashant dwivediNo ratings yet

- Notes - Obli 2Document14 pagesNotes - Obli 2Matthew WittNo ratings yet

- Pepsi Cola Distributors of The Phils., Inc. vs. Gal-LangDocument9 pagesPepsi Cola Distributors of The Phils., Inc. vs. Gal-LangjokuanNo ratings yet

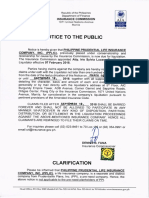

- Notice To The Public PPLIC Placed Under Liquidation Effective 07 Feb 2018Document1 pageNotice To The Public PPLIC Placed Under Liquidation Effective 07 Feb 2018Jerry MisterinoNo ratings yet

- Who Is Competent To Enter Into A Contract?Document16 pagesWho Is Competent To Enter Into A Contract?lelsocNo ratings yet

- Bussiness Law Exam 2Document4 pagesBussiness Law Exam 2Morely MejiaNo ratings yet

- Daywalt vs. La Corporacion de Los Padres Agustinos RecoletosDocument9 pagesDaywalt vs. La Corporacion de Los Padres Agustinos Recoletosbingkydoodle1012No ratings yet

- Addition ClaimsDocument1 pageAddition ClaimsDanuNo ratings yet

- General Power of Attorney Rolinda Khey YoungDocument3 pagesGeneral Power of Attorney Rolinda Khey Youngmanlapaoedmund97No ratings yet

- Position PaperDocument7 pagesPosition PaperJurilBrokaPatiñoNo ratings yet

- Draft Sale Deed KNMDocument4 pagesDraft Sale Deed KNMNeel Amar NaamNo ratings yet

- Vda Dejacinto vs. Vda de JacintoDocument2 pagesVda Dejacinto vs. Vda de JacintoEdvangelineManaloRodriguezNo ratings yet

- Chattel Mortgage: Pull-Out, Safekeeping, Disposal and Application of ProceedsDocument4 pagesChattel Mortgage: Pull-Out, Safekeeping, Disposal and Application of ProceedsJan RootsNo ratings yet

- DasdsaDocument34 pagesDasdsaFrederick TaylorNo ratings yet

- Section 37, para 1, of The Contract Act Lays Down That, "The Parties To A Contract Must Either PerformDocument1 pageSection 37, para 1, of The Contract Act Lays Down That, "The Parties To A Contract Must Either PerformRabbi Al RahatNo ratings yet

- Mridu Synopsis LLMDocument20 pagesMridu Synopsis LLMtarun aggarwalNo ratings yet

- Draft MOU Garage TieupDocument3 pagesDraft MOU Garage Tieupjassi7nishad100% (1)

- 5.bachrach VS Seifert 87 Phil 117Document1 page5.bachrach VS Seifert 87 Phil 117gokudera hayatoNo ratings yet

- Legal Department Delhi Indradev RayDocument1 pageLegal Department Delhi Indradev Rayshivamraj780840No ratings yet

- Law - Insider - Agora Digital Holdings Inc - Sale of Goods Agreement - Filed - 19 11 2021 - ContractDocument6 pagesLaw - Insider - Agora Digital Holdings Inc - Sale of Goods Agreement - Filed - 19 11 2021 - ContractE-25 Siddhesh BNo ratings yet

- Banking Law Notes 10Document6 pagesBanking Law Notes 10Afiqah IsmailNo ratings yet

- Cukr Skateboard Waiver 082307Document2 pagesCukr Skateboard Waiver 082307michaelcukr100% (9)

- Ang vs. Associated BankDocument3 pagesAng vs. Associated Bankmichi barrancoNo ratings yet

- G.R. NoDocument9 pagesG.R. NoDaniel Danjur DagumanNo ratings yet

- CIAP Document 102 FAQsDocument2 pagesCIAP Document 102 FAQsjamcarzadon.scNo ratings yet

- Higher National Diploma in International Business ManagementDocument37 pagesHigher National Diploma in International Business ManagementBuxon AntonyNo ratings yet

- Chapter 6 - Void, Voidable and Illegal ContractsDocument4 pagesChapter 6 - Void, Voidable and Illegal Contractstata cocoNo ratings yet

- Fundamentals of Laws, Obligations and ContractsDocument22 pagesFundamentals of Laws, Obligations and ContractsChel RaymundoNo ratings yet