Download as docx, pdf, or txt

You might also like

- AccountStatement 3286686240 Oct09 104105Document1 pageAccountStatement 3286686240 Oct09 104105AvijitSinharoyNo ratings yet

- Statement of Account For The Period 30-Jun-2020 To 16-Oct-2020Document13 pagesStatement of Account For The Period 30-Jun-2020 To 16-Oct-2020Chandrakanth KhannaNo ratings yet

- Bank (Receive)Document1 pageBank (Receive)siti fatimatuzzahraNo ratings yet

- HDFC Bank LTDDocument6 pagesHDFC Bank LTDS.KamalarajanNo ratings yet

- Timmy (Be A pART)Document1 pageTimmy (Be A pART)Timmy OngNo ratings yet

- Be A Sales SuperstarDocument2 pagesBe A Sales SuperstarworksatyajeetNo ratings yet

- KARUNANITHI SRINIVASAN1647319871895-credit-reportDocument26 pagesKARUNANITHI SRINIVASAN1647319871895-credit-reportHaritUchilNo ratings yet

- Intan Risma Ayu Mondani - 2012110073Document4 pagesIntan Risma Ayu Mondani - 2012110073adjieprayogaNo ratings yet

- Enter Values Loan SummaryDocument8 pagesEnter Values Loan SummaryEnis Z. MurseliNo ratings yet

- Uttara Branch: H#79/A, RD#7, SEC#4 Uttara Dhaka Bangladesh Phone: 880-2-8957427 - 9 Fax: 880-2-8957431Document5 pagesUttara Branch: H#79/A, RD#7, SEC#4 Uttara Dhaka Bangladesh Phone: 880-2-8957427 - 9 Fax: 880-2-8957431Farid AhmedNo ratings yet

- Girdhar51 1603693312542 PDFDocument2 pagesGirdhar51 1603693312542 PDFjignesh parmarNo ratings yet

- ConsolidatedStatement Apr 2024Document8 pagesConsolidatedStatement Apr 2024ziandra saputraNo ratings yet

- Home Loan AmortizationDocument6 pagesHome Loan AmortizationsunyrawatNo ratings yet

- Corene Boyd - TransUnion Personal Credit Report - 20160125 2Document25 pagesCorene Boyd - TransUnion Personal Credit Report - 20160125 2jessica nulphNo ratings yet

- Loan Amortization Schedule ABC LoanDocument8 pagesLoan Amortization Schedule ABC LoanThalia SandersNo ratings yet

- Application Detail: (Common Information)Document1 pageApplication Detail: (Common Information)AidahNo ratings yet

- Pettycshslip2Document2 pagesPettycshslip2aslindamohdnoorNo ratings yet

- Raazshaw23 1631293910741Document3 pagesRaazshaw23 1631293910741Gaurav ShawNo ratings yet

- Kreditni KalkulatorDocument2 pagesKreditni KalkulatorrodavgaNo ratings yet

- 802818Document2 pages802818isabisabNo ratings yet

- M/S. TKR Trinidad LTD 5 Floor, Newton Centre, 30-36 Maraval Road, Newtown, Port of Spain, Trinidad Wi Date: 22/ 07 /2022Document26 pagesM/S. TKR Trinidad LTD 5 Floor, Newton Centre, 30-36 Maraval Road, Newtown, Port of Spain, Trinidad Wi Date: 22/ 07 /2022Anugraha RamNo ratings yet

- SUMA J - Credit Reflecting SOADocument5 pagesSUMA J - Credit Reflecting SOAVijayNo ratings yet

- HDFC Bank LTDDocument6 pagesHDFC Bank LTDutkarshlegal96No ratings yet

- HDFC Bank LTDDocument3 pagesHDFC Bank LTDAKSHAY GHADGENo ratings yet

- LPBNG00031722172Document5 pagesLPBNG00031722172Ashok GNo ratings yet

- 157 - 20220328012911 - KLH AKUBANK-AKTS Giro - Tabungan-2021Document18 pages157 - 20220328012911 - KLH AKUBANK-AKTS Giro - Tabungan-2021sandrina misckaNo ratings yet

- November 2023 - 98FC64150Document2 pagesNovember 2023 - 98FC64150RRq LemanNo ratings yet

- 57 BBNP Bank Nusantara Parahyangan TBKDocument3 pages57 BBNP Bank Nusantara Parahyangan TBKDjohan HarijonoNo ratings yet

- Payment Summary: Payment Details General Transaction DetailsDocument1 pagePayment Summary: Payment Details General Transaction DetailsDharmaraja MuthukrishnanNo ratings yet

- Paymentorder - XHTML - Joyful HeartsDocument1 pagePaymentorder - XHTML - Joyful Heartsoluchibia stevenNo ratings yet

- Bhavesh Chotalia SoaDocument44 pagesBhavesh Chotalia SoabhaveshNo ratings yet

- CFA TemplateDocument15 pagesCFA TemplateGaurav SinghNo ratings yet

- Dewata Raya Ep 3Document2 pagesDewata Raya Ep 3Betta UcupNo ratings yet

- HDFC Bank LTDDocument2 pagesHDFC Bank LTDKrishna Prasad KanchojuNo ratings yet

- Sushumitha Cus CibilDocument19 pagesSushumitha Cus Cibilabhi ramNo ratings yet

- OpTransactionHistoryUX315 07 2019 PDFDocument1 pageOpTransactionHistoryUX315 07 2019 PDFAmit DereNo ratings yet

- LM 12341Document2 pagesLM 12341Mohammed Uzair KhanNo ratings yet

- One Statement of Account For The Last Month(s)Document6 pagesOne Statement of Account For The Last Month(s)Chandrakanth KhannaNo ratings yet

- HDFC Bank LTDDocument6 pagesHDFC Bank LTDutkarshlegal96No ratings yet

- GD 6 XMUVAJ3 S8 H9 B YDocument1 pageGD 6 XMUVAJ3 S8 H9 B Yvivek PandeyNo ratings yet

- Unit Holder Previleges: Account Statement 3192455114 Folio NumberDocument2 pagesUnit Holder Previleges: Account Statement 3192455114 Folio NumberDheeraj SharmaNo ratings yet

- Estatement20230706 000233440Document3 pagesEstatement20230706 000233440Mia NahilaNo ratings yet

- QSS20 07 1186 10Document1 pageQSS20 07 1186 10jimmytambunan544No ratings yet

- JOD13969Document2 pagesJOD13969Abhishek SinghviNo ratings yet

- Loan CalculatorDocument2 pagesLoan CalculatorAsadul AlamNo ratings yet

- Aug2010Document4 pagesAug2010Mohd ShoaibNo ratings yet

- Wa0011.Document4 pagesWa0011.Putra UtamaNo ratings yet

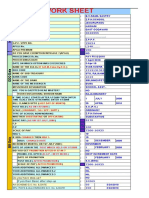

- Work Sheet: Do You Have Step-Up? If Yes Then Basic After Step-UpDocument41 pagesWork Sheet: Do You Have Step-Up? If Yes Then Basic After Step-UpAKRISHNAMURTY,HEADMASTER,ZPHS(G),DOWLESWARAMNo ratings yet

- NZ 7 Ab SV Dwa 11 Heb HDocument1 pageNZ 7 Ab SV Dwa 11 Heb HShyam GuptaNo ratings yet

- InitiateSingleEntryPaymentSummary02 12 2023 PDFDocument1 pageInitiateSingleEntryPaymentSummary02 12 2023 PDFkhz76070No ratings yet

- Sumit FD OF STATEBANKDocument2 pagesSumit FD OF STATEBANKrockkaindalNo ratings yet

- Cyber Treasury 2Document1 pageCyber Treasury 2Husain TinwalaNo ratings yet

- OpTransactionHistoryTpr06 08 2020Document1 pageOpTransactionHistoryTpr06 08 2020sumit chakrabortyNo ratings yet

- Bill Payment Confirmation (Step 4 of 4)Document1 pageBill Payment Confirmation (Step 4 of 4)Mohd Fairul AzharNo ratings yet

- Reference No: 866033: American International University - BangladeshDocument1 pageReference No: 866033: American International University - BangladeshTanvir PrantoNo ratings yet

- EsignPdf - 2023-12-06T150004.915Document34 pagesEsignPdf - 2023-12-06T150004.915digiekycrathiNo ratings yet

- Tanggal Uraian Transaksi Nominal Transaksi SaldoDocument1 pageTanggal Uraian Transaksi Nominal Transaksi Saldorudianto banezNo ratings yet

- Statementofaccountfortheperiod 01-Jan-2022To 21-Apr-2022Document6 pagesStatementofaccountfortheperiod 01-Jan-2022To 21-Apr-2022Vishnu Kumar100% (1)

- Map Parti Ch6Document5 pagesMap Parti Ch6Sunil ShawNo ratings yet

- Inventory Management, Just-in-Time, and Backflush CostingDocument30 pagesInventory Management, Just-in-Time, and Backflush Costingsiti fatimatuzzahraNo ratings yet

- Capital Budgeting and Cost AnalysisDocument26 pagesCapital Budgeting and Cost Analysissiti fatimatuzzahraNo ratings yet

- Chapter 5 - Profit CentersDocument15 pagesChapter 5 - Profit Centerssiti fatimatuzzahraNo ratings yet

- Formulation Forward Rate: Spot Rate +/-Forward Point Forward Point Spot Rate X Interst Diffential X Tenor 360Document1 pageFormulation Forward Rate: Spot Rate +/-Forward Point Forward Point Spot Rate X Interst Diffential X Tenor 360siti fatimatuzzahraNo ratings yet

- Foreing Exchange 1Document7 pagesForeing Exchange 1siti fatimatuzzahraNo ratings yet

- Bank (Receive)Document1 pageBank (Receive)siti fatimatuzzahraNo ratings yet

- CG Edit-1Document75 pagesCG Edit-1siti fatimatuzzahraNo ratings yet

- Chapter 6 - Internal ControlDocument36 pagesChapter 6 - Internal Controlsiti fatimatuzzahraNo ratings yet

- Indication SWP Point Int DepoDocument1 pageIndication SWP Point Int Depositi fatimatuzzahraNo ratings yet

- Chapter 5 - Business Processes and RisksDocument36 pagesChapter 5 - Business Processes and Riskssiti fatimatuzzahra100% (2)

- Chapter 4 - Risk ManagementDocument32 pagesChapter 4 - Risk Managementsiti fatimatuzzahraNo ratings yet

- Chapter 4 - Risk ManagementDocument32 pagesChapter 4 - Risk Managementsiti fatimatuzzahraNo ratings yet

- 07 HO Systemconstruction Implementation&SupportDocument5 pages07 HO Systemconstruction Implementation&Supportsiti fatimatuzzahraNo ratings yet

- CH 1 - Introduction To Internal AuditingDocument39 pagesCH 1 - Introduction To Internal Auditingsiti fatimatuzzahraNo ratings yet

- Chapter 3 - GovernanceDocument17 pagesChapter 3 - Governancesiti fatimatuzzahra100% (1)