Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5835)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 1601 CDocument6 pages1601 CJose Venturina Villacorta100% (1)

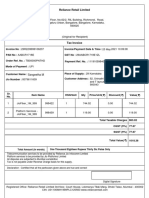

- Reliance Retail Limited: Sangeetha MDocument3 pagesReliance Retail Limited: Sangeetha MHariharan RNo ratings yet

- Devin J Simon 2004 MOHAWK RD APT. 321 Pueblo, Co 81001: Employer Use Only Corp. DeptDocument2 pagesDevin J Simon 2004 MOHAWK RD APT. 321 Pueblo, Co 81001: Employer Use Only Corp. DeptemtteachNo ratings yet

- Income Tax Form 2020 IDocument1 pageIncome Tax Form 2020 ISuvashreePradhanNo ratings yet

- CIR vs. Esso Standard: Compensation and Set-OffDocument2 pagesCIR vs. Esso Standard: Compensation and Set-OffGabriel HernandezNo ratings yet

- Evolution of Philippine TaxationDocument4 pagesEvolution of Philippine TaxationMay MayNo ratings yet

- Tax AssignmentDocument13 pagesTax AssignmentYitera SisayNo ratings yet

- Bsa 2105 Atty. F. R. Soriano Value-Added TaxDocument2 pagesBsa 2105 Atty. F. R. Soriano Value-Added Taxela kikayNo ratings yet

- 23061100002934ICIC ChallanReceiptDocument2 pages23061100002934ICIC ChallanReceiptSamyak DahaleNo ratings yet

- Lembar Kerja Tryout - JurnalDocument5 pagesLembar Kerja Tryout - JurnalArif RamadhaniNo ratings yet

- Combine For Print Part TwoDocument13 pagesCombine For Print Part TwoEloiza Lajara RamosNo ratings yet

- False 6. The Final Withholding VAT Is 12% of The Contract Price of Purchased Services From WithinDocument2 pagesFalse 6. The Final Withholding VAT Is 12% of The Contract Price of Purchased Services From WithinLazy LeathNo ratings yet

- Paye Calculator-2Document11 pagesPaye Calculator-2MORRIS MURIGINo ratings yet

- GP Fund Calculation Formula Sheet For GP Fund StatementDocument4 pagesGP Fund Calculation Formula Sheet For GP Fund StatementLucky KhanNo ratings yet

- Matekar PDFDocument1 pageMatekar PDFdharmveer singhNo ratings yet

- Definitions - Punjab Land Revenue Act, 1887Document2 pagesDefinitions - Punjab Land Revenue Act, 1887Lokendra SinghNo ratings yet

- Package One - Lowering The Personal Income Tax - #TaxReformNowDocument4 pagesPackage One - Lowering The Personal Income Tax - #TaxReformNowJarwikNo ratings yet

- Invoices 22feb2022Document21 pagesInvoices 22feb2022Merliza JusayanNo ratings yet

- Max Bupa Premium Reeipt Parents PDFDocument1 pageMax Bupa Premium Reeipt Parents PDFSatya0% (1)

- Ewt Exam - FormareDocument3 pagesEwt Exam - FormareMikaela SalvadorNo ratings yet

- Test 4Document3 pagesTest 4rehmamali98oNo ratings yet

- MR Shaik Mansoor Hussain H NO 87 1101 P 363 A, Ganesh Nagar, 4Th Class Colony, KURNOOL, KURNOOL-518002Document1 pageMR Shaik Mansoor Hussain H NO 87 1101 P 363 A, Ganesh Nagar, 4Th Class Colony, KURNOOL, KURNOOL-518002Shaik MansoorhussainNo ratings yet

- Tax QuizDocument6 pagesTax QuizAshley GanaNo ratings yet

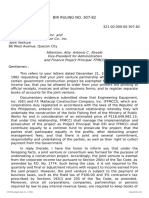

- BIR Ruling No. 307-82Document2 pagesBIR Ruling No. 307-82Alfred Hernandez CampañanoNo ratings yet

- Tax On Rental Income 2015-16Document8 pagesTax On Rental Income 2015-16Uganda Revenue AuthorityNo ratings yet

- Nirc and TrainDocument5 pagesNirc and TrainJasmine Marie Ng CheongNo ratings yet

- Zimra 2016 Tax Tables PDFDocument2 pagesZimra 2016 Tax Tables PDFKathryn BrownNo ratings yet

- Income Tax Calculation Sheet For 2020-21 VER 9.0: (Fill Colum N Only)Document8 pagesIncome Tax Calculation Sheet For 2020-21 VER 9.0: (Fill Colum N Only)Jnv MANACAMP RAIPURNo ratings yet

- Hindustan Unilever: PrintDocument2 pagesHindustan Unilever: PrintAbhay Kumar SinghNo ratings yet

- 1 Useful Calender For Every Accountant 2010Document13 pages1 Useful Calender For Every Accountant 2010bharat100% (1)