Download as pdf or txt

You might also like

- UntitledDocument26 pagesUntitledanandpandatNo ratings yet

- Social Impact Bond CaseDocument21 pagesSocial Impact Bond CaseTest123No ratings yet

- Positive and Negative Effects of GlobalizationDocument24 pagesPositive and Negative Effects of GlobalizationJames Dagohoy Ambay100% (2)

- Compact For Home OpportunityDocument30 pagesCompact For Home OpportunityRobert ValenciaNo ratings yet

- Project Report On Financial InstitutionDocument86 pagesProject Report On Financial Institutionarchana_anuragi83% (6)

- A Study On Role of Financial Institutions in Providing Housing Loans To Middle Income Group in Bangalore City.Document72 pagesA Study On Role of Financial Institutions in Providing Housing Loans To Middle Income Group in Bangalore City.Nadeem Naddu100% (1)

- Letter To Secretary Geithner On Changes To HARP To Assist More HomeownersDocument3 pagesLetter To Secretary Geithner On Changes To HARP To Assist More HomeownersThe Partnership for a Secure Financial FutureNo ratings yet

- Hud Dasp RTC v15Document11 pagesHud Dasp RTC v15Foreclosure FraudNo ratings yet

- Senate Hearing, 112TH Congress - Transportation and Housing and Urban Development, and Related Agencies Appropriations For Fiscal Year 2013Document159 pagesSenate Hearing, 112TH Congress - Transportation and Housing and Urban Development, and Related Agencies Appropriations For Fiscal Year 2013Scribd Government DocsNo ratings yet

- Administration Efforts Around Foreclosure ProcessingDocument8 pagesAdministration Efforts Around Foreclosure ProcessingfuriouscalvesNo ratings yet

- Hamp Hafa November 2010 ReportDocument12 pagesHamp Hafa November 2010 ReportTom LangNo ratings yet

- Macro Term PPDocument7 pagesMacro Term PPapi-285793077No ratings yet

- The Low-Income Housing Tax Credit: How It Works and Who It ServesDocument28 pagesThe Low-Income Housing Tax Credit: How It Works and Who It ServesAna Milena Prada100% (1)

- Departments of Transportation, Treas-Ury, The Judiciary, Housing and Urban Development, and Related Agencies Appropriations For Fiscal YEAR 2006Document54 pagesDepartments of Transportation, Treas-Ury, The Judiciary, Housing and Urban Development, and Related Agencies Appropriations For Fiscal YEAR 2006Scribd Government DocsNo ratings yet

- New Orleans Soft Second Mortgage FundingDocument23 pagesNew Orleans Soft Second Mortgage FundingPropertywizzNo ratings yet

- HOU Development Updates 12082023 Friday Memo MADocument3 pagesHOU Development Updates 12082023 Friday Memo MAApril ToweryNo ratings yet

- Testimony Julia Gordon 10-26-2010Document36 pagesTestimony Julia Gordon 10-26-2010Dawn HoganNo ratings yet

- Brookings Institution Principal ForgivenessDocument22 pagesBrookings Institution Principal ForgivenessDinSFLANo ratings yet

- The Reader: Finally Some Good News: HUD Announces 2010 Budget RequestDocument12 pagesThe Reader: Finally Some Good News: HUD Announces 2010 Budget RequestanhdincNo ratings yet

- Testimony - Ceo Citimortgage 6-24-10Document8 pagesTestimony - Ceo Citimortgage 6-24-10lbyrd55No ratings yet

- Summary of Performance and Financial Information Report: Fiscal YearDocument12 pagesSummary of Performance and Financial Information Report: Fiscal YearJohn FormosaNo ratings yet

- Navigating the Mortgage Modification Mess ¡V a Cautionary Tale: A Cautionary TaleFrom EverandNavigating the Mortgage Modification Mess ¡V a Cautionary Tale: A Cautionary TaleNo ratings yet

- Responses To Council Questions On Homelessness InvestmentDocument26 pagesResponses To Council Questions On Homelessness InvestmentUSA TODAY NetworkNo ratings yet

- Making Money From The MeltdownDocument52 pagesMaking Money From The Meltdownrnj1230100% (1)

- Donor Brief: Helping To Improve Donor Effectiveness in MicrofinanceDocument2 pagesDonor Brief: Helping To Improve Donor Effectiveness in MicrofinanceKripa SriramNo ratings yet

- Hearing Before The House Committee On Financial Services Subcommittee On InsuranceDocument9 pagesHearing Before The House Committee On Financial Services Subcommittee On InsuranceCarla Muss-JacobsNo ratings yet

- Departments of Transportation, Treas-Ury, The Judiciary, Housing and Urban Development, and Related Agencies Appropriations For Fiscal YEAR 2007Document50 pagesDepartments of Transportation, Treas-Ury, The Judiciary, Housing and Urban Development, and Related Agencies Appropriations For Fiscal YEAR 2007Scribd Government DocsNo ratings yet

- Valerie F. Leonard: Re: Public Comment-Neighborhood Stabilization Program State Action PlanDocument3 pagesValerie F. Leonard: Re: Public Comment-Neighborhood Stabilization Program State Action PlanValerie F. LeonardNo ratings yet

- Silver Jubilee Year 2012-13: Keynote AddressDocument13 pagesSilver Jubilee Year 2012-13: Keynote AddresspvenkyNo ratings yet

- Testimony of Brian Moynihan Chief Executive Officer Bank of America May 26, 2021Document32 pagesTestimony of Brian Moynihan Chief Executive Officer Bank of America May 26, 2021Joseph Adinolfi Jr.No ratings yet

- Real Estate Services Update: September 2011Document4 pagesReal Estate Services Update: September 2011narwebteamNo ratings yet

- HIPC Initiative: The IMF's Response To CriticsDocument6 pagesHIPC Initiative: The IMF's Response To CriticsAichaEssNo ratings yet

- Senate Hearing, 112TH Congress - Strengthening The Housing Market and Minimizing Losses To TaxpayersDocument45 pagesSenate Hearing, 112TH Congress - Strengthening The Housing Market and Minimizing Losses To TaxpayersScribd Government DocsNo ratings yet

- The Reader: Hundreds Rally For Affordable HousingDocument12 pagesThe Reader: Hundreds Rally For Affordable HousinganhdincNo ratings yet

- DesoerDocument8 pagesDesoerWARWICKJNo ratings yet

- WI RHS Brochure Getting To Know Rural Development Financing FuturesDocument6 pagesWI RHS Brochure Getting To Know Rural Development Financing FuturesSarah CornNo ratings yet

- Frequently Asked Questions: Pay For Success/Social Impact BondsDocument10 pagesFrequently Asked Questions: Pay For Success/Social Impact Bondsar15t0tleNo ratings yet

- Government SubsidiesDocument6 pagesGovernment Subsidiessamy7541No ratings yet

- Departments of Veterans Affairs and Housing and Urban Development and Independent Agencies Appropriations For Fiscal Year 2004Document74 pagesDepartments of Veterans Affairs and Housing and Urban Development and Independent Agencies Appropriations For Fiscal Year 2004Scribd Government DocsNo ratings yet

- Banking of BPMDocument20 pagesBanking of BPMSai DheerajNo ratings yet

- Housing Finance & Regulatory Affairs: David L. Ledford Senior Vice PresidentDocument14 pagesHousing Finance & Regulatory Affairs: David L. Ledford Senior Vice PresidentMatthew ConnorNo ratings yet

- INTRODUCTIONDocument4 pagesINTRODUCTIONpavika91No ratings yet

- Dissecting The OG Brady PlanDocument4 pagesDissecting The OG Brady PlanAyush YadavNo ratings yet

- Review of Options Available For Underwater Borrowers and Principal ForgivenessDocument15 pagesReview of Options Available For Underwater Borrowers and Principal ForgivenessForeclosure FraudNo ratings yet

- May 22,2009Document10 pagesMay 22,2009anhdincNo ratings yet

- 4-15-15 ForTheRecord - Private Sector in PubHsg-CLPHADocument4 pages4-15-15 ForTheRecord - Private Sector in PubHsg-CLPHAfrajam79No ratings yet

- Real Estate Services Update: November/December 2011Document4 pagesReal Estate Services Update: November/December 2011narwebteamNo ratings yet

- Reaching Communities Key MessagesDocument4 pagesReaching Communities Key MessagesMohammed AminNo ratings yet

- 2012 02 02 Letter To Edward Demarco Re Fannie Mae Freddie MacDocument2 pages2012 02 02 Letter To Edward Demarco Re Fannie Mae Freddie MacDinSFLANo ratings yet

- Assignment On Housing Development Finance Corporation LTDDocument27 pagesAssignment On Housing Development Finance Corporation LTDShubhra Agarwal100% (2)

- US Consumer Debt Relief: Industry, Overview, Laws & RegulationsFrom EverandUS Consumer Debt Relief: Industry, Overview, Laws & RegulationsNo ratings yet

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNo ratings yet

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNo ratings yet

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNo ratings yet

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNo ratings yet

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNo ratings yet

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNo ratings yet

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNo ratings yet

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNo ratings yet

- Debt and The Millennium Development Goals: A New Deal For Low-Income CountriesDocument11 pagesDebt and The Millennium Development Goals: A New Deal For Low-Income CountriesOxfamNo ratings yet

- Land to Lots: How to Borrow Money You Don't Have to Pay Back and LAUNCH Master Planned CommunitiesFrom EverandLand to Lots: How to Borrow Money You Don't Have to Pay Back and LAUNCH Master Planned CommunitiesNo ratings yet

- Chapter 14 - Provisions, Contingent Liabilities and Contingent AssetsDocument38 pagesChapter 14 - Provisions, Contingent Liabilities and Contingent AssetsamiteshNo ratings yet

- Sample Project Report - PLUMBINGDocument2 pagesSample Project Report - PLUMBINGVirendra ChavdaNo ratings yet

- WAQ Produces A Single Product XDocument2 pagesWAQ Produces A Single Product Xmj192No ratings yet

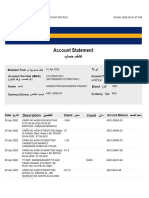

- Account StatementDocument2 pagesAccount StatementReziir rmcNo ratings yet

- Creative Problem Solving - Great Depression LessonDocument12 pagesCreative Problem Solving - Great Depression Lessonapi-287347463No ratings yet

- Consumables Procurement Scenario in Sap MMDocument2 pagesConsumables Procurement Scenario in Sap MMkhanmdNo ratings yet

- Kim Fuller: Case Written by Prof. Robert N. AnthonyDocument2 pagesKim Fuller: Case Written by Prof. Robert N. AnthonyJohn Carlos WeeNo ratings yet

- Home Loan - A Comparitive Study at BOIDocument86 pagesHome Loan - A Comparitive Study at BOIRuchi Prabhu100% (2)

- Exam Ifm CBT TableDocument2 pagesExam Ifm CBT Tablemasayoshi0ogawaNo ratings yet

- Corporate Law FInal BA0150032Document19 pagesCorporate Law FInal BA0150032Guru PrashannaNo ratings yet

- MisDocument264 pagesMisArul Kumaran KothandapaniNo ratings yet

- Evaly ModelDocument2 pagesEvaly ModelZR BhemelNo ratings yet

- CV-Mabexly Sitohang PDFDocument9 pagesCV-Mabexly Sitohang PDFmpsitohangNo ratings yet

- Export GuidanceDocument45 pagesExport GuidanceRomi PatelNo ratings yet

- Khadi Natural HealthcareDocument5 pagesKhadi Natural HealthcareNivedita ChoudharyNo ratings yet

- Margalla Services Officers Mess-169Document1 pageMargalla Services Officers Mess-169Wasi MohammadNo ratings yet

- Customer Perception Towards Bajaj's VehiclesDocument85 pagesCustomer Perception Towards Bajaj's VehiclesЯoнiт Яagнavaи100% (1)

- Efe and Ife Matrix: Strategic ManagementDocument30 pagesEfe and Ife Matrix: Strategic ManagementAnkitNo ratings yet

- FABM1 11 Quarter 4 Week 4 Las 3Document2 pagesFABM1 11 Quarter 4 Week 4 Las 3Janna PleteNo ratings yet

- Taylor&taylor PPP JEP PDFDocument24 pagesTaylor&taylor PPP JEP PDFCosmin TurcuNo ratings yet

- Indonesia Compliance Assessment Tools 012015Document31 pagesIndonesia Compliance Assessment Tools 012015Julius HabibiNo ratings yet

- Homeworks CH09Document3 pagesHomeworks CH09Loma Al-MahraNo ratings yet

- Data ExpedisiDocument42 pagesData ExpedisiPanjirahmanNo ratings yet

- QIP - Vol.1 - Section 1 - Instruction To Bidders - With JICA Comments - 271114 PDFDocument12 pagesQIP - Vol.1 - Section 1 - Instruction To Bidders - With JICA Comments - 271114 PDFادزسر بانديكو هادولهNo ratings yet

- Digital Banking in India 2016Document21 pagesDigital Banking in India 2016Prof Dr Chowdari Prasad100% (3)

- Annadatta: Uncompromised QualityDocument18 pagesAnnadatta: Uncompromised QualityANJU PALLENo ratings yet

- Lecture 1 2editedDocument13 pagesLecture 1 2editedIon CaraNo ratings yet

- Case Study Best Value Procurement Performance Information Procurement System DevelopmentDocument36 pagesCase Study Best Value Procurement Performance Information Procurement System DevelopmentCharles BinuNo ratings yet