Download as pdf or txt

You might also like

- Furniture Industry in VietnamDocument11 pagesFurniture Industry in Vietnambhavani100% (2)

- Industrial Report On Furniture IndustryDocument23 pagesIndustrial Report On Furniture IndustryNagula Bala Ajesh Goud67% (3)

- Ethics and Accountability The Philippine Experrience by CSCDocument5 pagesEthics and Accountability The Philippine Experrience by CSCLinda Himoldang Marcaida100% (2)

- Restricted Joint Chiefs of Staff Manual 3212.02C Electronic Attack Exercises in U.S. and Canada PDFDocument82 pagesRestricted Joint Chiefs of Staff Manual 3212.02C Electronic Attack Exercises in U.S. and Canada PDFSHTF PLAN100% (2)

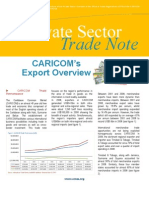

- CRNM - Private Sector Trade Note - Vol 11 2009Document3 pagesCRNM - Private Sector Trade Note - Vol 11 2009Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- Vietnam Wood Processing Industry - Ho Chi Minh City - Vietnam - 06-11-2020Document8 pagesVietnam Wood Processing Industry - Ho Chi Minh City - Vietnam - 06-11-2020Ngọc ĐoànNo ratings yet

- Hardy Hanson-Introduction: Page - 1Document18 pagesHardy Hanson-Introduction: Page - 1Rashil ShahNo ratings yet

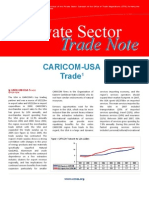

- OTN - Private Sector Trade Note - Vol 3 2011Document3 pagesOTN - Private Sector Trade Note - Vol 3 2011Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- Global Carpet Tile Market - Now Available ThroughDocument3 pagesGlobal Carpet Tile Market - Now Available ThroughFortune Research Reports Private LimitedNo ratings yet

- Mexican Furniture IndustryDocument41 pagesMexican Furniture Industrydaniel_fernandes7867% (3)

- MCL OrganizationDocument30 pagesMCL OrganizationDeekshith KumarNo ratings yet

- Furniture IndustryDocument45 pagesFurniture IndustrySara Ghulam Muhammed Sheikha0% (2)

- 1.worldwide Revenue in Million USDDocument3 pages1.worldwide Revenue in Million USDFernando LPNo ratings yet

- OTN - Private Sector Trade Note - Vol 16 2010Document4 pagesOTN - Private Sector Trade Note - Vol 16 2010Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- DLSU AKI - Local Cooperation and Upgrading in Response To GlobalizationDocument51 pagesDLSU AKI - Local Cooperation and Upgrading in Response To GlobalizationBenedict RazonNo ratings yet

- Mexico:: Market Opportunities For Canadian Wood ProductsDocument19 pagesMexico:: Market Opportunities For Canadian Wood ProductsGillian ZhangNo ratings yet

- Articol Prod Mobila 2013Document14 pagesArticol Prod Mobila 2013Dana BesliuNo ratings yet

- Romanian Export FurnitureDocument8 pagesRomanian Export FurnitureAlexandra CoșcovelnițăNo ratings yet

- D.troian Case Study-LibreDocument29 pagesD.troian Case Study-LibreRamona ElenaNo ratings yet

- Leather IndustryDocument11 pagesLeather Industrytahir_altafNo ratings yet

- SI Wooden FurnitureDocument7 pagesSI Wooden FurnituresalmanNo ratings yet

- Top 20 Largest Timber Exporting CountriesDocument20 pagesTop 20 Largest Timber Exporting CountriesAmbika MSNo ratings yet

- Sai RamDocument43 pagesSai Ramnirmala periasamyNo ratings yet

- Tissari To ITC and ITTO On World Furniture Markets 22 04 2005 PDFDocument265 pagesTissari To ITC and ITTO On World Furniture Markets 22 04 2005 PDFaneekNo ratings yet

- Ceramic Tiles Industry in IndiaDocument9 pagesCeramic Tiles Industry in Indiaaltaf_catsNo ratings yet

- 2013 Furniture Industry WatchDocument12 pages2013 Furniture Industry WatchAlexandra CoșcovelnițăNo ratings yet

- Indian Furniture IndustryDocument5 pagesIndian Furniture Industryanas018izharNo ratings yet

- Industry ProfileDocument3 pagesIndustry ProfileHà Quảng TâyNo ratings yet

- Branded Furniture in IndiaDocument23 pagesBranded Furniture in IndiaSharmila PandeyNo ratings yet

- Export Prospects GraniteDocument13 pagesExport Prospects Graniteabhi_singh17No ratings yet

- 4o-New Bamboo Industries and Pro-Poor Impact-ChinaDocument21 pages4o-New Bamboo Industries and Pro-Poor Impact-ChinaTalha SiddiquiNo ratings yet

- 2nd Part Bus485 ReportDocument13 pages2nd Part Bus485 ReportAffan AhmedNo ratings yet

- ALEMANIA Germany Home TextilesDocument9 pagesALEMANIA Germany Home TextilesSandraNo ratings yet

- CRNM - Private Sector Trade Note - Vol 7 2009Document4 pagesCRNM - Private Sector Trade Note - Vol 7 2009Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- Major Research ReportDocument10 pagesMajor Research ReportShubham SinghNo ratings yet

- Biz Quiz 081010Document3 pagesBiz Quiz 081010arshaNo ratings yet

- An Organisational Study On Rubco Huat Woods (P) LTDDocument69 pagesAn Organisational Study On Rubco Huat Woods (P) LTDasifkt100% (1)

- A See ReDocument12 pagesA See ReAndrian DregleaNo ratings yet

- Ekonomi Paint SectorDocument4 pagesEkonomi Paint SectorDilansu KahramanNo ratings yet

- CRNM - Private Sector Trade Note - Vol 5 2009Document3 pagesCRNM - Private Sector Trade Note - Vol 5 2009Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- Ceramics Industry in IndiaDocument19 pagesCeramics Industry in IndiaAkhilesh MishraNo ratings yet

- Some Market Trends of Wood Products Exports in Ghana and Their Implications For Stakeholders PDFDocument8 pagesSome Market Trends of Wood Products Exports in Ghana and Their Implications For Stakeholders PDFRichard Nkosuo AcquahNo ratings yet

- HTTP Service - OntarioexportsDocument1 pageHTTP Service - OntarioexportsSvitlana IavorenkoNo ratings yet

- Global Scenerio: Industry ProfileDocument6 pagesGlobal Scenerio: Industry Profilegreshma jayakumarNo ratings yet

- A Project Report On Ceramic Tile IndustryDocument44 pagesA Project Report On Ceramic Tile IndustryRavi KiranNo ratings yet

- Wood Products and Panels: Chilean Plywood Exports Increase Slightly in 2020Document1 pageWood Products and Panels: Chilean Plywood Exports Increase Slightly in 2020Pablo Carrasco OrozcoNo ratings yet

- Industry Analysis: Furniture ManufactureDocument45 pagesIndustry Analysis: Furniture ManufactureAniketh JalanNo ratings yet

- OTN - Private Sector Trade Note - Vol 2 2011Document4 pagesOTN - Private Sector Trade Note - Vol 2 2011Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- Furniture 2010 PDFDocument32 pagesFurniture 2010 PDFkeane3108No ratings yet

- Building Products Top Markets ReportDocument99 pagesBuilding Products Top Markets ReportHector Arturo Camejo FandiñoNo ratings yet

- BB Ukraine-Baumaterial2006 enDocument245 pagesBB Ukraine-Baumaterial2006 enmelikeder100% (1)

- Sample Chapter 2Document27 pagesSample Chapter 2Louise Joseph PeraltaNo ratings yet

- Marble Industry of RajasthanDocument26 pagesMarble Industry of Rajasthanmanishakalaga60% (5)

- Sample 10257179 PDFDocument12 pagesSample 10257179 PDFrohitNo ratings yet

- Vitreous China, Fine Earthenware & Pottery Products World Summary: Market Values & Financials by CountryFrom EverandVitreous China, Fine Earthenware & Pottery Products World Summary: Market Values & Financials by CountryNo ratings yet

- Household Furniture World Summary: Market Values & Financials by CountryFrom EverandHousehold Furniture World Summary: Market Values & Financials by CountryNo ratings yet

- 2014-03-03 OTN Special Update (The Focus of The WTO MC9)Document8 pages2014-03-03 OTN Special Update (The Focus of The WTO MC9)Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- The Association of Caribbean States (ACS) : 1994-2014 - 20 Years Promoting Cooperation in The Greater CaribbeanDocument124 pagesThe Association of Caribbean States (ACS) : 1994-2014 - 20 Years Promoting Cooperation in The Greater CaribbeanOffice of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- TTIP: The Economic Analysis ExplainedDocument18 pagesTTIP: The Economic Analysis ExplainedOffice of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- OTN Special Update - Innovation - A New Frontier in Trade Multilateralism - 2013-04-25Document4 pagesOTN Special Update - Innovation - A New Frontier in Trade Multilateralism - 2013-04-25Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- OTN - Private Sector Trade Note - Vol 4 2013Document2 pagesOTN - Private Sector Trade Note - Vol 4 2013Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- OTN Special Update - Economic and Trade Policies Related To Diet and Obesity in CARICOM (2013!11!21)Document5 pagesOTN Special Update - Economic and Trade Policies Related To Diet and Obesity in CARICOM (2013!11!21)Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- 2013 National Trade Estimate Report On Foreign Trade Barriers, United States Trade RepresentativeDocument406 pages2013 National Trade Estimate Report On Foreign Trade Barriers, United States Trade RepresentativekeithedwhiteNo ratings yet

- WTO - Supply Chain Perspectives and Issues: A Literature ReviewDocument234 pagesWTO - Supply Chain Perspectives and Issues: A Literature ReviewOffice of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- OTN - Private Sector Trade Note - Vol 2 2013Document4 pagesOTN - Private Sector Trade Note - Vol 2 2013Office of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- CARICOM View: 40 Years of Integration, Come Celebrate With UsDocument64 pagesCARICOM View: 40 Years of Integration, Come Celebrate With UsOffice of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- Condolences For Former CRNM DG Ambassador Henry S GillDocument1 pageCondolences For Former CRNM DG Ambassador Henry S GillOffice of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- PR282013 - 'Key Architect' of CARIFORUM - EU EPA Passes AwayDocument2 pagesPR282013 - 'Key Architect' of CARIFORUM - EU EPA Passes AwayOffice of Trade Negotiations (OTN), CARICOM SecretariatNo ratings yet

- Unctad Wir2012 Full enDocument239 pagesUnctad Wir2012 Full enAnaDraghiaNo ratings yet

- GIMC: Semi-Finalists - RespondentsDocument45 pagesGIMC: Semi-Finalists - RespondentsAmol Mehta75% (4)

- Autographics v. PALDocument4 pagesAutographics v. PALCristelle Elaine Collera100% (1)

- Affidavit For Cancellation of Registration For Lost Plate(s) - C19 FormDocument1 pageAffidavit For Cancellation of Registration For Lost Plate(s) - C19 Formdflakjs_sldkfa_comNo ratings yet

- Alexander - Images of EmpireDocument321 pagesAlexander - Images of EmpireWillian ManciniNo ratings yet

- NSN Policy Paper 2012 Candidates Nov2011 FINALDocument8 pagesNSN Policy Paper 2012 Candidates Nov2011 FINALNatSecNetNo ratings yet

- Minutes of Lisbon Meeting - 2010Document10 pagesMinutes of Lisbon Meeting - 2010Branko BrkicNo ratings yet

- Theory of Judicial ReviewDocument311 pagesTheory of Judicial ReviewJo-Al GealonNo ratings yet

- The American Presidency Fill in The BlanksDocument1 pageThe American Presidency Fill in The BlanksAmber StrawserNo ratings yet

- Handbook On The Construction and Interpretation of The LawDocument1 pageHandbook On The Construction and Interpretation of The Lawlicopodicum7670No ratings yet

- Affidavit Contracts TemplateDocument239 pagesAffidavit Contracts TemplateFritz Corgado100% (1)

- The Legislative: Reported By: Group 3Document42 pagesThe Legislative: Reported By: Group 3Hpesoj SemlapNo ratings yet

- Job Search LogDocument2 pagesJob Search LogMichael CurtisNo ratings yet

- Reaction Paper-Effects of Globalization On Public AdministrationDocument1 pageReaction Paper-Effects of Globalization On Public Administrationericson igual100% (1)

- United States Court of Appeals, Third CircuitDocument11 pagesUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- Nonhegemonic International Relations: A Preliminary ConceptualizationDocument22 pagesNonhegemonic International Relations: A Preliminary ConceptualizationPriya NaikNo ratings yet

- Wallstreetjournal 20171102 TheWallStreetJournalDocument36 pagesWallstreetjournal 20171102 TheWallStreetJournalsadaq84No ratings yet

- Surety Bond Callable On DemandDocument3 pagesSurety Bond Callable On DemandVeronica RiveraNo ratings yet

- Jonathan Soberanis December 2018 Probable Cause StatementDocument2 pagesJonathan Soberanis December 2018 Probable Cause StatementAdam ForgieNo ratings yet

- Shantanu Upadhyay - Sec C - Eco - Roll No 132Document17 pagesShantanu Upadhyay - Sec C - Eco - Roll No 132Abhishek TiwariNo ratings yet

- The Deeds of The Divine AugustusDocument7 pagesThe Deeds of The Divine AugustusxziadinNo ratings yet

- Questionnaire For Future BLICZerDocument1 pageQuestionnaire For Future BLICZerAlejandra GheorghiuNo ratings yet

- Ahiara DeclarationDocument28 pagesAhiara DeclarationChukwunonso ArinzeNo ratings yet

- DR Nadeem Shafiq Malik PDFDocument4 pagesDR Nadeem Shafiq Malik PDFRitu Raj RamanNo ratings yet

- Sex Traffickers Took Hundreds From Thailand To USDocument3 pagesSex Traffickers Took Hundreds From Thailand To USjohndeereNo ratings yet

- SveepDocument269 pagesSveepsuryanathNo ratings yet

- Jagualing v. CA (Digest)Document2 pagesJagualing v. CA (Digest)Tini GuanioNo ratings yet

- Award Certificates EDITABLEDocument6 pagesAward Certificates EDITABLEikhsan MubarokNo ratings yet

- January 2007 NSA PowerPoint On Bulk Collection of Telephony Metadata For AnalystsDocument18 pagesJanuary 2007 NSA PowerPoint On Bulk Collection of Telephony Metadata For AnalystsMatthew KeysNo ratings yet