Download as pdf or txt

You might also like

- Financial Management: M Y Khan - P K JainDocument29 pagesFinancial Management: M Y Khan - P K JainPrashant Kumbar29% (7)

- Couples Name: Ang PamamanhikanDocument31 pagesCouples Name: Ang PamamanhikanApple Joy Agda100% (1)

- Finance 5311 Solutions ManualDocument7 pagesFinance 5311 Solutions ManualTony WoodsNo ratings yet

- What Is The Economic Outlook For OECD Countries?: An Interim AssessmentDocument17 pagesWhat Is The Economic Outlook For OECD Countries?: An Interim AssessmentJohn RotheNo ratings yet

- Revenue and Spending (% of GDP)Document1 pageRevenue and Spending (% of GDP)penelopegerhardNo ratings yet

- Monthly Economic Bulletin: January 2011Document15 pagesMonthly Economic Bulletin: January 2011lrochekellyNo ratings yet

- FMI (2015) WEO Adjusting To Lower Commodity Prices 38 50Document13 pagesFMI (2015) WEO Adjusting To Lower Commodity Prices 38 50Briggette QuirozNo ratings yet

- Global Macro March 8 2023Document16 pagesGlobal Macro March 8 2023asdf23No ratings yet

- Esi 2019 06 enDocument21 pagesEsi 2019 06 enValter SilveiraNo ratings yet

- ECB: Taking Stock - Where Do We Stand in The Crisis - by Jurgen Stark, 15-APR-2010Document12 pagesECB: Taking Stock - Where Do We Stand in The Crisis - by Jurgen Stark, 15-APR-2010FloridaHossNo ratings yet

- Deroose Dubrovnik Convergence EaDocument20 pagesDeroose Dubrovnik Convergence Ea1234567890albertoNo ratings yet

- mb201402 Focus02.enDocument4 pagesmb201402 Focus02.enJorkosNo ratings yet

- Esi 2019 07 enDocument27 pagesEsi 2019 07 enValter SilveiraNo ratings yet

- Airline Profitability ChallengeDocument19 pagesAirline Profitability ChallengebeowlNo ratings yet

- Situation Analysis and Current Issues of Sri Lankan Economy With Special Emphasis On Fiscal and Debt IssuesDocument34 pagesSituation Analysis and Current Issues of Sri Lankan Economy With Special Emphasis On Fiscal and Debt IssuesuserabhishekNo ratings yet

- Aalberts 2020Document128 pagesAalberts 2020gaja babaNo ratings yet

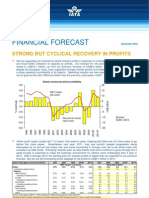

- Financial Forecast: Strong But Cyclical Recovery in ProfitsDocument4 pagesFinancial Forecast: Strong But Cyclical Recovery in ProfitsDaniel WongNo ratings yet

- The Open Economy: MacroeconomicsDocument32 pagesThe Open Economy: Macroeconomicsnoemi sfNo ratings yet

- Esm Capital Markets Integration Schoenmaker 8-12Document12 pagesEsm Capital Markets Integration Schoenmaker 8-12gaikwadswapnil0603No ratings yet

- CITATION HTT /L 1033Document55 pagesCITATION HTT /L 1033Miskatul ArafatNo ratings yet

- Macroeconomic Analysis For DenmarkDocument8 pagesMacroeconomic Analysis For DenmarkBozinoskaSNo ratings yet

- Resumer Du MemoireDocument10 pagesResumer Du Memoirerita tamohNo ratings yet

- Economic Developments and Investment Environment in TurkeyDocument30 pagesEconomic Developments and Investment Environment in TurkeyPolat ArıNo ratings yet

- JapanDocument4 pagesJapanMaria BuereNo ratings yet

- Chapter 1 ESSDocument2 pagesChapter 1 ESSHiếu TrầnNo ratings yet

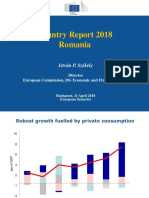

- Semestru European Raport de Tara Romania 2018 Istvan SzekelyDocument15 pagesSemestru European Raport de Tara Romania 2018 Istvan SzekelyClaudia FilipNo ratings yet

- Paul Kasriel: Great Depression, Just The FactsDocument7 pagesPaul Kasriel: Great Depression, Just The Factshblodget100% (3)

- Chapter 03 PDFDocument80 pagesChapter 03 PDFnasim dashkhaneNo ratings yet

- Worksheet in GlobalFree-CashBank - Case Study - 2018Document2 pagesWorksheet in GlobalFree-CashBank - Case Study - 2018rashmianand712No ratings yet

- Osborne2 09 Transforming GovernmentDocument62 pagesOsborne2 09 Transforming GovernmentBrian CumminsNo ratings yet

- Revenue Statistics in Africa 2020 Democratic Republic of The CongoDocument2 pagesRevenue Statistics in Africa 2020 Democratic Republic of The CongoDawitNo ratings yet

- Presentacion 2019 PDFDocument9 pagesPresentacion 2019 PDFWilsonNo ratings yet

- Chapter 1 ESSDocument1 pageChapter 1 ESSVân AnhNo ratings yet

- Size of The Public Sector Data Set Nov 2015Document250 pagesSize of The Public Sector Data Set Nov 2015Bbaoc BbaocNo ratings yet

- Industry Outlook March2011Document4 pagesIndustry Outlook March2011iminvisibleNo ratings yet

- Schimbări Macroeconomice in RomaniaDocument19 pagesSchimbări Macroeconomice in Romaniachiratcu.valyNo ratings yet

- 7105 EcDocument18 pages7105 EcbostexNo ratings yet

- The Balance of Payments: Speech Given by DR Martin WealeDocument14 pagesThe Balance of Payments: Speech Given by DR Martin WealeImamjafar SiddiqNo ratings yet

- Q1 - 2023 24 Investor PresentationDocument27 pagesQ1 - 2023 24 Investor PresentationashwinsadvayofficialNo ratings yet

- PBI Nominal y Real, Ingresos y Egresos Del Gobierno, Inflación, CreciemientoDocument8 pagesPBI Nominal y Real, Ingresos y Egresos Del Gobierno, Inflación, CreciemientoMelissa RamirezNo ratings yet

- Islp 4Document5 pagesIslp 4amithx100No ratings yet

- March GragphDocument3 pagesMarch GragphsucijaNo ratings yet

- Chapter Two Theory of Production 2.1. The Production FunctionDocument24 pagesChapter Two Theory of Production 2.1. The Production Functionabadi gebruNo ratings yet

- Alia, Tax Rates. Because They Are Determined Directly Through A Political Process, Rates Provide ADocument14 pagesAlia, Tax Rates. Because They Are Determined Directly Through A Political Process, Rates Provide AGandhi Jenny Rakeshkumar BD20029No ratings yet

- Ashokley 14-05 IprzDocument56 pagesAshokley 14-05 IprzRasmi RanjanNo ratings yet

- The Effects of Globalisation On Labour Markets, Productivity and InflationDocument27 pagesThe Effects of Globalisation On Labour Markets, Productivity and InflationAmar Kumar JhaNo ratings yet

- Edom Getiye... DecemberDocument1 pageEdom Getiye... Decemberyohans bisetNo ratings yet

- 25 Inflation Rate: Exports, Imports and Trade BalanceDocument4 pages25 Inflation Rate: Exports, Imports and Trade BalanceKenjin SaiNo ratings yet

- Us Charts CondDocument8 pagesUs Charts CondJonathan NixonNo ratings yet

- Day 8 FsDocument44 pagesDay 8 Fs무루파털뭉치No ratings yet

- Applied Econometric Time Series 3Rd Ed.: Chapter 3: Modeling VolatilityDocument80 pagesApplied Econometric Time Series 3Rd Ed.: Chapter 3: Modeling Volatilityjhonatan AlaniaNo ratings yet

- Topics in International Macroeconomics Lecture 2: International Financial Crises and Regulation of Capital FlowsDocument42 pagesTopics in International Macroeconomics Lecture 2: International Financial Crises and Regulation of Capital FlowsKadirNo ratings yet

- MSFIN 223 - Case 1 - Du Pont (Cauton, Cortez, Dy, Lui, Mamaril, Papa, Rasco)Document3 pagesMSFIN 223 - Case 1 - Du Pont (Cauton, Cortez, Dy, Lui, Mamaril, Papa, Rasco)Leophil RascoNo ratings yet

- OPIM-274 HW2-SolutionsDocument4 pagesOPIM-274 HW2-SolutionsJSNo ratings yet

- Supplier Evaluasi Result - Aug2020Document18 pagesSupplier Evaluasi Result - Aug2020Januari SudrajatNo ratings yet

- Fig. 2.2Document1 pageFig. 2.2Cyruss MeranoNo ratings yet

- SCM 3250 Lecture 1Document28 pagesSCM 3250 Lecture 1Changmin JiangNo ratings yet

- IIF Argentina's Sudden StopDocument2 pagesIIF Argentina's Sudden StopCronista.comNo ratings yet

- Ptmcctchap 13 EarningsDocument27 pagesPtmcctchap 13 EarningsjgmvmNo ratings yet

- The Spanish Monetary NightmareDocument4 pagesThe Spanish Monetary NightmareLuis Riestra DelgadoNo ratings yet

- Middle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsFrom EverandMiddle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsNo ratings yet

- Eprs Bri (2016) 577971 enDocument8 pagesEprs Bri (2016) 577971 en1234567890albertoNo ratings yet

- Deadlines September STR 2017.07.12 enDocument2 pagesDeadlines September STR 2017.07.12 en1234567890albertoNo ratings yet

- UK Withdrawal From The European Union: In-Depth AnalysisDocument40 pagesUK Withdrawal From The European Union: In-Depth Analysis1234567890albertoNo ratings yet

- EN - EP Brochure Citizen VoicesDocument25 pagesEN - EP Brochure Citizen Voices1234567890albertoNo ratings yet

- European ParliamentDocument8 pagesEuropean Parliament1234567890albertoNo ratings yet

- The European Parliament: Organisation and Operation: Legal BasisDocument4 pagesThe European Parliament: Organisation and Operation: Legal Basis1234567890albertoNo ratings yet

- Working For You enDocument60 pagesWorking For You en1234567890albertoNo ratings yet

- 2nd Report State Energy Union enDocument15 pages2nd Report State Energy Union en1234567890albertoNo ratings yet

- Financial Transaction Taxes in The European Union: Taxation PapersDocument36 pagesFinancial Transaction Taxes in The European Union: Taxation Papers1234567890albertoNo ratings yet

- Financial Transaction Taxes in The European Union: Taxation PapersDocument36 pagesFinancial Transaction Taxes in The European Union: Taxation Papers1234567890albertoNo ratings yet

- Deroose Dubrovnik Emu Which Way How Many SpeedsDocument25 pagesDeroose Dubrovnik Emu Which Way How Many Speeds1234567890albertoNo ratings yet

- Deroose Berlin Fiscal Stance EaDocument27 pagesDeroose Berlin Fiscal Stance Ea1234567890albertoNo ratings yet

- How To Strengthen Health Care Systems Through Fiscal SustainabilityDocument10 pagesHow To Strengthen Health Care Systems Through Fiscal Sustainability1234567890albertoNo ratings yet

- Deroose Sto Two Speed Europe BruegelDocument24 pagesDeroose Sto Two Speed Europe Bruegel1234567890albertoNo ratings yet

- Deroose Dubrovnik Convergence EaDocument20 pagesDeroose Dubrovnik Convergence Ea1234567890albertoNo ratings yet

- Deroose Zagreb Par in CroatiaDocument7 pagesDeroose Zagreb Par in Croatia1234567890albertoNo ratings yet

- Australian Governent Eu General InformationDocument1 pageAustralian Governent Eu General Information1234567890albertoNo ratings yet

- Deroose Bucharestlaunch2016crfinal PDFDocument15 pagesDeroose Bucharestlaunch2016crfinal PDF1234567890albertoNo ratings yet

- Hanapbuhay at Relihiyon NG Mga TausugDocument4 pagesHanapbuhay at Relihiyon NG Mga TausugAntoinette Genevieve LopezNo ratings yet

- Procedure Ship Security Officer Training Module WorkbookDocument19 pagesProcedure Ship Security Officer Training Module WorkbookBao TranNo ratings yet

- (From ACCRA Law Office) First, Second Third: Conuangco Vs Palma FactsDocument3 pages(From ACCRA Law Office) First, Second Third: Conuangco Vs Palma FactsMa Gloria Trinidad ArafolNo ratings yet

- Screening-Test-Class-Reading-Record6 CamelliaDocument2 pagesScreening-Test-Class-Reading-Record6 CamelliaAlona Ledesma IgnacioNo ratings yet

- Philosophical Issues in TourismDocument2 pagesPhilosophical Issues in TourismLana Talita100% (1)

- 98-368 Test Bank Lesson 01Document7 pages98-368 Test Bank Lesson 01yassinedoNo ratings yet

- Econ 122 Week 1 9 by DwexDocument19 pagesEcon 122 Week 1 9 by DwexDestinyNo ratings yet

- Agriculture in AustraliaDocument213 pagesAgriculture in AustraliaUsama ShahNo ratings yet

- VA-02 - Grammar-1 Article and PronounsDocument46 pagesVA-02 - Grammar-1 Article and PronounsJaya SahuNo ratings yet

- Nationalism in India 2023 Padhai Ak Mazza NotesDocument10 pagesNationalism in India 2023 Padhai Ak Mazza NotesShaikh FarhaanNo ratings yet

- Harikumar Mohanachandran: Accounts 84455.11Document3 pagesHarikumar Mohanachandran: Accounts 84455.11Devil ArtistNo ratings yet

- Making of A Mahatma (Film) by Shyam BenegalDocument4 pagesMaking of A Mahatma (Film) by Shyam BenegalellehcimNo ratings yet

- Qualities of A Good SpeakerDocument7 pagesQualities of A Good SpeakerKanshi BhoynaNo ratings yet

- Corporate Finance Pattern in BangladeshDocument20 pagesCorporate Finance Pattern in BangladeshKhanNo ratings yet

- Trade Trapeze - The Hindu Editorial On India's Exports - The HinduDocument3 pagesTrade Trapeze - The Hindu Editorial On India's Exports - The Hinduksingh25103No ratings yet

- Rulebook WoW Mini PDFDocument24 pagesRulebook WoW Mini PDFCesarRabadanGarciaNo ratings yet

- Resumen Valuation MckinseyDocument11 pagesResumen Valuation MckinseycarlosvallejoNo ratings yet

- Research On Drug Abuse in St. HubertDocument16 pagesResearch On Drug Abuse in St. HubertSt. Gabby100% (1)

- Global Health Is More Than Just Public Health Somewhere Else'Document3 pagesGlobal Health Is More Than Just Public Health Somewhere Else'danfer_99No ratings yet

- Ce 151P Building PermitDocument3 pagesCe 151P Building PermitJenina LogmaoNo ratings yet

- Satip M 100 09Document10 pagesSatip M 100 09munnaNo ratings yet

- Sat Prakash Meena v. Alka MeenaDocument13 pagesSat Prakash Meena v. Alka MeenaDeepanshuNo ratings yet

- CJL 5000 Hsa Plan 2024 SBC Final 10182023Document8 pagesCJL 5000 Hsa Plan 2024 SBC Final 10182023dominicvjohnson03No ratings yet

- Coa Gov Ph-UntitledDocument3 pagesCoa Gov Ph-UntitledPalanas A. VinceNo ratings yet

- Aziz Fatimah Medical & Dental College: Merit List Displayed by Pakistan Medical Commision For AFMDCDocument5 pagesAziz Fatimah Medical & Dental College: Merit List Displayed by Pakistan Medical Commision For AFMDCAkhtar AliNo ratings yet

- The Monkees - I'm A Believer LyricsDocument1 pageThe Monkees - I'm A Believer LyricsMercy YilmaNo ratings yet