AnalystPresentn 2010

AnalystPresentn 2010

You might also like

- EduTap Finance Notes For RBI GradeB Merged (144 MB - 735 Pages) PDFDocument735 pagesEduTap Finance Notes For RBI GradeB Merged (144 MB - 735 Pages) PDFYashika Garg74% (35)

- FMP Assignement Key - Cases Fall 10Document16 pagesFMP Assignement Key - Cases Fall 10ahsan_anwar_1No ratings yet

- SADIF-Investment AnalyticsDocument12 pagesSADIF-Investment AnalyticsTony ZhangNo ratings yet

- CMS Info SystemsDocument29 pagesCMS Info Systemskrishna_buntyNo ratings yet

- NSE Concept Note (One Digital)Document3 pagesNSE Concept Note (One Digital)YasahNo ratings yet

- Q2FY19 Investor Update - PGCILDocument19 pagesQ2FY19 Investor Update - PGCILHemant SharmaNo ratings yet

- Q2-FY19 Result Update: CMP: 125 Target: 263Document7 pagesQ2-FY19 Result Update: CMP: 125 Target: 263Ashutosh GuptaNo ratings yet

- Industrial Analysis: Fast Moving Consumer Goods SectorDocument9 pagesIndustrial Analysis: Fast Moving Consumer Goods Sectorshashank nutiNo ratings yet

- KFin Technologies - Flash Note - 12 Dec 23Document6 pagesKFin Technologies - Flash Note - 12 Dec 23palakNo ratings yet

- Blockchain: The Power of Distributed Ledger in Healthcare Industry I. Sources of FinancingDocument4 pagesBlockchain: The Power of Distributed Ledger in Healthcare Industry I. Sources of Financingchatuuuu123No ratings yet

- Persistent Systems - One PagerDocument3 pagesPersistent Systems - One PagerKishor KrNo ratings yet

- Investor Presentation FY20Document49 pagesInvestor Presentation FY20Nitin ParasharNo ratings yet

- Nazara Technologies LimitedDocument35 pagesNazara Technologies LimitedMadhan RajNo ratings yet

- Q3 Update TelecosDocument6 pagesQ3 Update Telecosca.deepaktiwariNo ratings yet

- Resource Sharing For An Intelligent Future: Annual Report 2020Document176 pagesResource Sharing For An Intelligent Future: Annual Report 2020mailimailiNo ratings yet

- Grasim Q3FY09 PresentationDocument47 pagesGrasim Q3FY09 PresentationJasmine NayakNo ratings yet

- HCL Technologies Q3FY11 Result UpdateDocument4 pagesHCL Technologies Q3FY11 Result Updaterajarun85No ratings yet

- 2024 q1 Nokia Earnings Release EnglishDocument31 pages2024 q1 Nokia Earnings Release EnglishrmdirfantvNo ratings yet

- Advanc Conference - Call 2q2018 PDFDocument16 pagesAdvanc Conference - Call 2q2018 PDFtat angNo ratings yet

- PT XL Axiata TBK: Digital FocusDocument8 pagesPT XL Axiata TBK: Digital FocusTeguh PerdanaNo ratings yet

- Company DataDocument10 pagesCompany DataAvengers HeroesNo ratings yet

- Atlas Exports Limited FinalDocument22 pagesAtlas Exports Limited FinalKinza AsimNo ratings yet

- Software Services Relative ValuationDocument5 pagesSoftware Services Relative ValuationSrilekha BasavojuNo ratings yet

- Wipro Limited - Update On Material Event: Summary of Rating(s) OutstandingDocument7 pagesWipro Limited - Update On Material Event: Summary of Rating(s) OutstandingMegha PrakashNo ratings yet

- In Line Performance... : (Natmin) HoldDocument10 pagesIn Line Performance... : (Natmin) HoldMani SeshadrinathanNo ratings yet

- P&L Assumption BS Assumptions P&L Output BS FCFF Wacc DCF ValueDocument66 pagesP&L Assumption BS Assumptions P&L Output BS FCFF Wacc DCF ValuePrabhdeep DadyalNo ratings yet

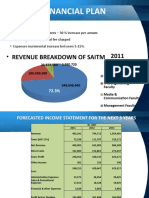

- Financial Plan: - Revenue Breakdown of SaitmDocument6 pagesFinancial Plan: - Revenue Breakdown of SaitmUdeeshan JonasNo ratings yet

- TATACOMM ICICIDirect 06082021Document8 pagesTATACOMM ICICIDirect 06082021gbNo ratings yet

- Tatva Chintan Limited. F: SubscribeDocument7 pagesTatva Chintan Limited. F: Subscribeturbulence iitismNo ratings yet

- Jamna Auto 2017-18Document184 pagesJamna Auto 2017-18Karun DevNo ratings yet

- IRCON PresentationDocument29 pagesIRCON Presentationjitendra76No ratings yet

- TitanDocument7 pagesTitan869jshh52hNo ratings yet

- AGTL - 2QCY20 Result Review - 29-07-2020Document2 pagesAGTL - 2QCY20 Result Review - 29-07-2020SHAHZAIB -No ratings yet

- Task 3 Sec A Group 12Document4 pagesTask 3 Sec A Group 12Pulkit AggarwalNo ratings yet

- Corporate ValuationDocument9 pagesCorporate ValuationPRACHI DASNo ratings yet

- Bajaj Motors ReportDocument11 pagesBajaj Motors Reportsatyammishra.p2325No ratings yet

- Mphasis - Company BriefDocument6 pagesMphasis - Company BriefSantosh KathiraNo ratings yet

- BOM-Pre-promotion Digital Training Program - Reading MaterialDocument486 pagesBOM-Pre-promotion Digital Training Program - Reading MaterialRohith RaoNo ratings yet

- Cipla: Performance HighlightsDocument8 pagesCipla: Performance HighlightsKapil AthwaniNo ratings yet

- Pricol - CU-IDirect-Mar 3, 2022Document6 pagesPricol - CU-IDirect-Mar 3, 2022rajesh katareNo ratings yet

- Corporate Financial ReviewDocument28 pagesCorporate Financial ReviewIshan KakkarNo ratings yet

- Nokia Financial Report 2023 Q2Document20 pagesNokia Financial Report 2023 Q2Ahmed HussainNo ratings yet

- One 97 Communications (Parent Org. of Paytm) - A Stock StoryDocument10 pagesOne 97 Communications (Parent Org. of Paytm) - A Stock StoryHariomNo ratings yet

- ASL Investor Presentation Q4FY24 Financial ResultsDocument23 pagesASL Investor Presentation Q4FY24 Financial ResultsAshok BodeddulaNo ratings yet

- Chandragupt Institute of Management Patna: Information Technology For Managers (Individual Assignment)Document9 pagesChandragupt Institute of Management Patna: Information Technology For Managers (Individual Assignment)si ranNo ratings yet

- GTPL Hathway LTD.: A) About The CompanyDocument10 pagesGTPL Hathway LTD.: A) About The CompanyPayal SinghNo ratings yet

- HT Media Limited HT Media Limited: Results Presentation Q1 FY2011 Q1 FY2011Document12 pagesHT Media Limited HT Media Limited: Results Presentation Q1 FY2011 Q1 FY2011itsmnjNo ratings yet

- Analysis Beyond Consensus: The New Abc of ResearchDocument15 pagesAnalysis Beyond Consensus: The New Abc of ResearchRimjhim BhatiaNo ratings yet

- Report For 4M.2020Document7 pagesReport For 4M.2020Lao Quoc BuuNo ratings yet

- Bharti Airtel: Company FocusDocument5 pagesBharti Airtel: Company FocusthomsoncltNo ratings yet

- Today.: Technology For The Next DecadeDocument26 pagesToday.: Technology For The Next DecadeBschool caseNo ratings yet

- ) It'ifi3m, : Bank BarodaDocument5 pages) It'ifi3m, : Bank BarodaKaushal KumarNo ratings yet

- Team RD-4 ITDocument16 pagesTeam RD-4 ITsukeshNo ratings yet

- Tesla FinModelDocument58 pagesTesla FinModelPrabhdeep DadyalNo ratings yet

- Icici Direct ResearchDocument9 pagesIcici Direct Researchfinanceharsh6No ratings yet

- September Quarter 2023 ResultsDocument20 pagesSeptember Quarter 2023 ResultsPony BakerNo ratings yet

- EdgeReport TATAELXSI ConcallAnalysis 14-10-2022 333Document3 pagesEdgeReport TATAELXSI ConcallAnalysis 14-10-2022 333RajatNo ratings yet

- "Turning Glove From GOLD To DIAMOND": Supermax Corporation Berhad Analyst Briefing Slides 4Q'2020 RESULTSDocument35 pages"Turning Glove From GOLD To DIAMOND": Supermax Corporation Berhad Analyst Briefing Slides 4Q'2020 RESULTSmroys mroysNo ratings yet

- ITC Limited: Resilient Quarter Amidst Weak Industry DemandDocument5 pagesITC Limited: Resilient Quarter Amidst Weak Industry DemandGeebeeNo ratings yet

- Financial Modelling ReportDocument15 pagesFinancial Modelling ReportakshaynamsaniNo ratings yet

- Tarun Financial Model - InFOSYSDocument49 pagesTarun Financial Model - InFOSYSANJALI SHARMANo ratings yet

- Intergrated Annual ReportDocument15 pagesIntergrated Annual ReportAbdelhkim KechNo ratings yet

- Unlocking the Potential of Digital Services Trade in Asia and the PacificFrom EverandUnlocking the Potential of Digital Services Trade in Asia and the PacificNo ratings yet

- IFRS 9 Financial InstrumentsDocument38 pagesIFRS 9 Financial InstrumentsKiri chrisNo ratings yet

- Trần Thị Thu Nguyệt-Pa3-Hwchapter17Document2 pagesTrần Thị Thu Nguyệt-Pa3-Hwchapter17Nguyet Tran Thi ThuNo ratings yet

- List of Largest Banks in The United States - WikipediaDocument5 pagesList of Largest Banks in The United States - WikipedialdNo ratings yet

- 07-Combining Rsi With Rsi PDFDocument5 pages07-Combining Rsi With Rsi PDFsudeshjhaNo ratings yet

- Next Edge Private Lending Presentation v1Document16 pagesNext Edge Private Lending Presentation v1dpbasicNo ratings yet

- Faurecia FY2019 Press Release vDEFDocument13 pagesFaurecia FY2019 Press Release vDEFSharmi antonyNo ratings yet

- Labour Relations ActDocument4 pagesLabour Relations Act孙涛No ratings yet

- Stanley (DeWalt) Annual Report 2021-22Document140 pagesStanley (DeWalt) Annual Report 2021-22tamoghno sahaNo ratings yet

- Mindanao Savings and Loans Inc Vs WillkomDocument2 pagesMindanao Savings and Loans Inc Vs Willkomis_still_artNo ratings yet

- A Basic Introduction To Stock Scanners and How I Use ThemDocument19 pagesA Basic Introduction To Stock Scanners and How I Use ThemtummalaajaybabuNo ratings yet

- Portfolio Management Tutorial 3: Prepared By: Ang Win Sun Pong Chong Bin Chin Chen Hong Jashvin Kaur Diong Seng LongDocument10 pagesPortfolio Management Tutorial 3: Prepared By: Ang Win Sun Pong Chong Bin Chin Chen Hong Jashvin Kaur Diong Seng LongchziNo ratings yet

- History of RbiDocument9 pagesHistory of RbiAditya JainNo ratings yet

- Introduction To M&ADocument6 pagesIntroduction To M&Avasundhara dagaNo ratings yet

- Quiz 4 CH 8 ACC563Document5 pagesQuiz 4 CH 8 ACC563scokni1973_130667106No ratings yet

- 224 23 BS BF 224Document3 pages224 23 BS BF 224D'zite JereNo ratings yet

- The Accounting EquationDocument8 pagesThe Accounting EquationYasotha RajendranNo ratings yet

- Wills & SuccessionDocument50 pagesWills & SuccessionJov May DimcoNo ratings yet

- AC414 - Audit and Investigations II - Audit of Cash and Bank BalanceDocument20 pagesAC414 - Audit and Investigations II - Audit of Cash and Bank BalanceTsitsi AbigailNo ratings yet

- NDC Vs Madrigal Wan Hai DigestDocument2 pagesNDC Vs Madrigal Wan Hai DigestAlexis Anne P. ArejolaNo ratings yet

- Account Receivable - 26092016Document38 pagesAccount Receivable - 26092016Khánh MinhNo ratings yet

- Candidate Orientation L2 FinalDocument42 pagesCandidate Orientation L2 FinalelyNo ratings yet

- Collateralized Mortgage Obligations (Cmos) : The Basics of The Cmo MarketDocument14 pagesCollateralized Mortgage Obligations (Cmos) : The Basics of The Cmo MarketGit90No ratings yet

- Issuer'S Quarterly Information Return For Mortgage Credit Certificates (MCCS)Document2 pagesIssuer'S Quarterly Information Return For Mortgage Credit Certificates (MCCS)IRSNo ratings yet

- Union Budget 2011-12Document11 pagesUnion Budget 2011-12rockyj47No ratings yet

- Statement of Changes in EquityDocument8 pagesStatement of Changes in EquityGonzalo Jr. RualesNo ratings yet

- Code of Ethics Conduct ValeDocument12 pagesCode of Ethics Conduct ValeDedi Tista AmijayaNo ratings yet

- Some ExercisesDocument3 pagesSome ExercisesMinh Tâm NguyễnNo ratings yet

Download as pdf or txt

You might also like

- EduTap Finance Notes For RBI GradeB Merged (144 MB - 735 Pages) PDFDocument735 pagesEduTap Finance Notes For RBI GradeB Merged (144 MB - 735 Pages) PDFYashika Garg74% (35)

- FMP Assignement Key - Cases Fall 10Document16 pagesFMP Assignement Key - Cases Fall 10ahsan_anwar_1No ratings yet

- SADIF-Investment AnalyticsDocument12 pagesSADIF-Investment AnalyticsTony ZhangNo ratings yet

- CMS Info SystemsDocument29 pagesCMS Info Systemskrishna_buntyNo ratings yet

- NSE Concept Note (One Digital)Document3 pagesNSE Concept Note (One Digital)YasahNo ratings yet

- Q2FY19 Investor Update - PGCILDocument19 pagesQ2FY19 Investor Update - PGCILHemant SharmaNo ratings yet

- Q2-FY19 Result Update: CMP: 125 Target: 263Document7 pagesQ2-FY19 Result Update: CMP: 125 Target: 263Ashutosh GuptaNo ratings yet

- Industrial Analysis: Fast Moving Consumer Goods SectorDocument9 pagesIndustrial Analysis: Fast Moving Consumer Goods Sectorshashank nutiNo ratings yet

- KFin Technologies - Flash Note - 12 Dec 23Document6 pagesKFin Technologies - Flash Note - 12 Dec 23palakNo ratings yet

- Blockchain: The Power of Distributed Ledger in Healthcare Industry I. Sources of FinancingDocument4 pagesBlockchain: The Power of Distributed Ledger in Healthcare Industry I. Sources of Financingchatuuuu123No ratings yet

- Persistent Systems - One PagerDocument3 pagesPersistent Systems - One PagerKishor KrNo ratings yet

- Investor Presentation FY20Document49 pagesInvestor Presentation FY20Nitin ParasharNo ratings yet

- Nazara Technologies LimitedDocument35 pagesNazara Technologies LimitedMadhan RajNo ratings yet

- Q3 Update TelecosDocument6 pagesQ3 Update Telecosca.deepaktiwariNo ratings yet

- Resource Sharing For An Intelligent Future: Annual Report 2020Document176 pagesResource Sharing For An Intelligent Future: Annual Report 2020mailimailiNo ratings yet

- Grasim Q3FY09 PresentationDocument47 pagesGrasim Q3FY09 PresentationJasmine NayakNo ratings yet

- HCL Technologies Q3FY11 Result UpdateDocument4 pagesHCL Technologies Q3FY11 Result Updaterajarun85No ratings yet

- 2024 q1 Nokia Earnings Release EnglishDocument31 pages2024 q1 Nokia Earnings Release EnglishrmdirfantvNo ratings yet

- Advanc Conference - Call 2q2018 PDFDocument16 pagesAdvanc Conference - Call 2q2018 PDFtat angNo ratings yet

- PT XL Axiata TBK: Digital FocusDocument8 pagesPT XL Axiata TBK: Digital FocusTeguh PerdanaNo ratings yet

- Company DataDocument10 pagesCompany DataAvengers HeroesNo ratings yet

- Atlas Exports Limited FinalDocument22 pagesAtlas Exports Limited FinalKinza AsimNo ratings yet

- Software Services Relative ValuationDocument5 pagesSoftware Services Relative ValuationSrilekha BasavojuNo ratings yet

- Wipro Limited - Update On Material Event: Summary of Rating(s) OutstandingDocument7 pagesWipro Limited - Update On Material Event: Summary of Rating(s) OutstandingMegha PrakashNo ratings yet

- In Line Performance... : (Natmin) HoldDocument10 pagesIn Line Performance... : (Natmin) HoldMani SeshadrinathanNo ratings yet

- P&L Assumption BS Assumptions P&L Output BS FCFF Wacc DCF ValueDocument66 pagesP&L Assumption BS Assumptions P&L Output BS FCFF Wacc DCF ValuePrabhdeep DadyalNo ratings yet

- Financial Plan: - Revenue Breakdown of SaitmDocument6 pagesFinancial Plan: - Revenue Breakdown of SaitmUdeeshan JonasNo ratings yet

- TATACOMM ICICIDirect 06082021Document8 pagesTATACOMM ICICIDirect 06082021gbNo ratings yet

- Tatva Chintan Limited. F: SubscribeDocument7 pagesTatva Chintan Limited. F: Subscribeturbulence iitismNo ratings yet

- Jamna Auto 2017-18Document184 pagesJamna Auto 2017-18Karun DevNo ratings yet

- IRCON PresentationDocument29 pagesIRCON Presentationjitendra76No ratings yet

- TitanDocument7 pagesTitan869jshh52hNo ratings yet

- AGTL - 2QCY20 Result Review - 29-07-2020Document2 pagesAGTL - 2QCY20 Result Review - 29-07-2020SHAHZAIB -No ratings yet

- Task 3 Sec A Group 12Document4 pagesTask 3 Sec A Group 12Pulkit AggarwalNo ratings yet

- Corporate ValuationDocument9 pagesCorporate ValuationPRACHI DASNo ratings yet

- Bajaj Motors ReportDocument11 pagesBajaj Motors Reportsatyammishra.p2325No ratings yet

- Mphasis - Company BriefDocument6 pagesMphasis - Company BriefSantosh KathiraNo ratings yet

- BOM-Pre-promotion Digital Training Program - Reading MaterialDocument486 pagesBOM-Pre-promotion Digital Training Program - Reading MaterialRohith RaoNo ratings yet

- Cipla: Performance HighlightsDocument8 pagesCipla: Performance HighlightsKapil AthwaniNo ratings yet

- Pricol - CU-IDirect-Mar 3, 2022Document6 pagesPricol - CU-IDirect-Mar 3, 2022rajesh katareNo ratings yet

- Corporate Financial ReviewDocument28 pagesCorporate Financial ReviewIshan KakkarNo ratings yet

- Nokia Financial Report 2023 Q2Document20 pagesNokia Financial Report 2023 Q2Ahmed HussainNo ratings yet

- One 97 Communications (Parent Org. of Paytm) - A Stock StoryDocument10 pagesOne 97 Communications (Parent Org. of Paytm) - A Stock StoryHariomNo ratings yet

- ASL Investor Presentation Q4FY24 Financial ResultsDocument23 pagesASL Investor Presentation Q4FY24 Financial ResultsAshok BodeddulaNo ratings yet

- Chandragupt Institute of Management Patna: Information Technology For Managers (Individual Assignment)Document9 pagesChandragupt Institute of Management Patna: Information Technology For Managers (Individual Assignment)si ranNo ratings yet

- GTPL Hathway LTD.: A) About The CompanyDocument10 pagesGTPL Hathway LTD.: A) About The CompanyPayal SinghNo ratings yet

- HT Media Limited HT Media Limited: Results Presentation Q1 FY2011 Q1 FY2011Document12 pagesHT Media Limited HT Media Limited: Results Presentation Q1 FY2011 Q1 FY2011itsmnjNo ratings yet

- Analysis Beyond Consensus: The New Abc of ResearchDocument15 pagesAnalysis Beyond Consensus: The New Abc of ResearchRimjhim BhatiaNo ratings yet

- Report For 4M.2020Document7 pagesReport For 4M.2020Lao Quoc BuuNo ratings yet

- Bharti Airtel: Company FocusDocument5 pagesBharti Airtel: Company FocusthomsoncltNo ratings yet

- Today.: Technology For The Next DecadeDocument26 pagesToday.: Technology For The Next DecadeBschool caseNo ratings yet

- ) It'ifi3m, : Bank BarodaDocument5 pages) It'ifi3m, : Bank BarodaKaushal KumarNo ratings yet

- Team RD-4 ITDocument16 pagesTeam RD-4 ITsukeshNo ratings yet

- Tesla FinModelDocument58 pagesTesla FinModelPrabhdeep DadyalNo ratings yet

- Icici Direct ResearchDocument9 pagesIcici Direct Researchfinanceharsh6No ratings yet

- September Quarter 2023 ResultsDocument20 pagesSeptember Quarter 2023 ResultsPony BakerNo ratings yet

- EdgeReport TATAELXSI ConcallAnalysis 14-10-2022 333Document3 pagesEdgeReport TATAELXSI ConcallAnalysis 14-10-2022 333RajatNo ratings yet

- "Turning Glove From GOLD To DIAMOND": Supermax Corporation Berhad Analyst Briefing Slides 4Q'2020 RESULTSDocument35 pages"Turning Glove From GOLD To DIAMOND": Supermax Corporation Berhad Analyst Briefing Slides 4Q'2020 RESULTSmroys mroysNo ratings yet

- ITC Limited: Resilient Quarter Amidst Weak Industry DemandDocument5 pagesITC Limited: Resilient Quarter Amidst Weak Industry DemandGeebeeNo ratings yet

- Financial Modelling ReportDocument15 pagesFinancial Modelling ReportakshaynamsaniNo ratings yet

- Tarun Financial Model - InFOSYSDocument49 pagesTarun Financial Model - InFOSYSANJALI SHARMANo ratings yet

- Intergrated Annual ReportDocument15 pagesIntergrated Annual ReportAbdelhkim KechNo ratings yet

- Unlocking the Potential of Digital Services Trade in Asia and the PacificFrom EverandUnlocking the Potential of Digital Services Trade in Asia and the PacificNo ratings yet

- IFRS 9 Financial InstrumentsDocument38 pagesIFRS 9 Financial InstrumentsKiri chrisNo ratings yet

- Trần Thị Thu Nguyệt-Pa3-Hwchapter17Document2 pagesTrần Thị Thu Nguyệt-Pa3-Hwchapter17Nguyet Tran Thi ThuNo ratings yet

- List of Largest Banks in The United States - WikipediaDocument5 pagesList of Largest Banks in The United States - WikipedialdNo ratings yet

- 07-Combining Rsi With Rsi PDFDocument5 pages07-Combining Rsi With Rsi PDFsudeshjhaNo ratings yet

- Next Edge Private Lending Presentation v1Document16 pagesNext Edge Private Lending Presentation v1dpbasicNo ratings yet

- Faurecia FY2019 Press Release vDEFDocument13 pagesFaurecia FY2019 Press Release vDEFSharmi antonyNo ratings yet

- Labour Relations ActDocument4 pagesLabour Relations Act孙涛No ratings yet

- Stanley (DeWalt) Annual Report 2021-22Document140 pagesStanley (DeWalt) Annual Report 2021-22tamoghno sahaNo ratings yet

- Mindanao Savings and Loans Inc Vs WillkomDocument2 pagesMindanao Savings and Loans Inc Vs Willkomis_still_artNo ratings yet

- A Basic Introduction To Stock Scanners and How I Use ThemDocument19 pagesA Basic Introduction To Stock Scanners and How I Use ThemtummalaajaybabuNo ratings yet

- Portfolio Management Tutorial 3: Prepared By: Ang Win Sun Pong Chong Bin Chin Chen Hong Jashvin Kaur Diong Seng LongDocument10 pagesPortfolio Management Tutorial 3: Prepared By: Ang Win Sun Pong Chong Bin Chin Chen Hong Jashvin Kaur Diong Seng LongchziNo ratings yet

- History of RbiDocument9 pagesHistory of RbiAditya JainNo ratings yet

- Introduction To M&ADocument6 pagesIntroduction To M&Avasundhara dagaNo ratings yet

- Quiz 4 CH 8 ACC563Document5 pagesQuiz 4 CH 8 ACC563scokni1973_130667106No ratings yet

- 224 23 BS BF 224Document3 pages224 23 BS BF 224D'zite JereNo ratings yet

- The Accounting EquationDocument8 pagesThe Accounting EquationYasotha RajendranNo ratings yet

- Wills & SuccessionDocument50 pagesWills & SuccessionJov May DimcoNo ratings yet

- AC414 - Audit and Investigations II - Audit of Cash and Bank BalanceDocument20 pagesAC414 - Audit and Investigations II - Audit of Cash and Bank BalanceTsitsi AbigailNo ratings yet

- NDC Vs Madrigal Wan Hai DigestDocument2 pagesNDC Vs Madrigal Wan Hai DigestAlexis Anne P. ArejolaNo ratings yet

- Account Receivable - 26092016Document38 pagesAccount Receivable - 26092016Khánh MinhNo ratings yet

- Candidate Orientation L2 FinalDocument42 pagesCandidate Orientation L2 FinalelyNo ratings yet

- Collateralized Mortgage Obligations (Cmos) : The Basics of The Cmo MarketDocument14 pagesCollateralized Mortgage Obligations (Cmos) : The Basics of The Cmo MarketGit90No ratings yet

- Issuer'S Quarterly Information Return For Mortgage Credit Certificates (MCCS)Document2 pagesIssuer'S Quarterly Information Return For Mortgage Credit Certificates (MCCS)IRSNo ratings yet

- Union Budget 2011-12Document11 pagesUnion Budget 2011-12rockyj47No ratings yet

- Statement of Changes in EquityDocument8 pagesStatement of Changes in EquityGonzalo Jr. RualesNo ratings yet

- Code of Ethics Conduct ValeDocument12 pagesCode of Ethics Conduct ValeDedi Tista AmijayaNo ratings yet

- Some ExercisesDocument3 pagesSome ExercisesMinh Tâm NguyễnNo ratings yet