Download as pdf or txt

You might also like

- CFCS Study Manual 6th EditionDocument311 pagesCFCS Study Manual 6th EditionTheresa BatisNo ratings yet

- Namibia Sector Policy On Inclusive EducationDocument52 pagesNamibia Sector Policy On Inclusive EducationJanine GoliathNo ratings yet

- ACFE Fraud Examination Report (Short)Document8 pagesACFE Fraud Examination Report (Short)Basit Sattar100% (1)

- Understanding International Relations by Chris BrownDocument31 pagesUnderstanding International Relations by Chris BrownKiwanis Montes AbundaNo ratings yet

- Creative AccountingDocument7 pagesCreative Accountingeugeniastefania raduNo ratings yet

- Fraud and ErrorDocument46 pagesFraud and ErrorE.D.J100% (1)

- Fraud - Risk - Assessment PWC PDFDocument2 pagesFraud - Risk - Assessment PWC PDFHarinakshi PoojaryNo ratings yet

- Information Security Threats and AttacksDocument20 pagesInformation Security Threats and AttacksWilber Ccacca ChipanaNo ratings yet

- Auditng External Business RelationshipsDocument19 pagesAuditng External Business RelationshipsFernando Ernesto CabralNo ratings yet

- Orlando Governance Risk and Compliance 7-1-2020Document7 pagesOrlando Governance Risk and Compliance 7-1-2020ibmkamal-1100% (1)

- Fraser2016 PDFDocument10 pagesFraser2016 PDFNoviansyah PamungkasNo ratings yet

- Wndi Rehab Vs RetributionDocument27 pagesWndi Rehab Vs RetributionLuke Roy100% (1)

- Fraud Investigation StrategyDocument24 pagesFraud Investigation StrategyOsama Sanabani100% (1)

- Fraud Position StatementDocument4 pagesFraud Position StatementsenoltoygarNo ratings yet

- Due Diligence: ChecklistDocument16 pagesDue Diligence: ChecklistRichard L. Dunnam100% (2)

- White Collar Crime Fraud Corruption Risks Survey Utica College ProtivitiDocument41 pagesWhite Collar Crime Fraud Corruption Risks Survey Utica College ProtivitiOlga KutnovaNo ratings yet

- Business Ethics CaseDocument14 pagesBusiness Ethics CaseMuhammad Saqib AwanNo ratings yet

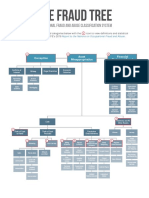

- Fraud-Tree SchemesDocument13 pagesFraud-Tree SchemessulthanhakimNo ratings yet

- Accountants Perceptions Fraud Detection Prevention MethodsDocument18 pagesAccountants Perceptions Fraud Detection Prevention MethodsSeptyy Ningtyas100% (1)

- The Anatomy of Corporate FraudDocument24 pagesThe Anatomy of Corporate FraudJe SuisNo ratings yet

- Fraud Control Jul08Document46 pagesFraud Control Jul08hmedlamineNo ratings yet

- Managing The Fraud Risk: Mustapha Mugisa SDocument48 pagesManaging The Fraud Risk: Mustapha Mugisa SMustapha MugisaNo ratings yet

- Fraud at The Engagement Level: Expositor: Javier BecerraDocument11 pagesFraud at The Engagement Level: Expositor: Javier BecerraWalter Córdova MacedoNo ratings yet

- Internal Audit Stakeholder Management and The Three Lines of Defense Slide DeckDocument12 pagesInternal Audit Stakeholder Management and The Three Lines of Defense Slide DeckSheyam SelvarajNo ratings yet

- Form 18 Sdi 2 - Loans - Risk of Material Misstatement (Romm) WorksheetDocument27 pagesForm 18 Sdi 2 - Loans - Risk of Material Misstatement (Romm) WorksheetwellawalalasithNo ratings yet

- Albrecht 4e Ch02 SolutionsDocument17 pagesAlbrecht 4e Ch02 SolutionsNana NurhayatiNo ratings yet

- Unit 1 Internal Audit RoleDocument7 pagesUnit 1 Internal Audit RoleMark Andrew CabaleNo ratings yet

- An Analysis of Fraud Triangle and Responsibilities of AuditorsDocument8 pagesAn Analysis of Fraud Triangle and Responsibilities of AuditorsPrihandani AntonNo ratings yet

- Ethics, Fraud, and Internal ControlDocument32 pagesEthics, Fraud, and Internal ControlMonica Ferrer100% (2)

- Forensic Accounting by Makanju 2Document12 pagesForensic Accounting by Makanju 2Babajide AdedapoNo ratings yet

- Chapter 17Document21 pagesChapter 17Talia AdaNo ratings yet

- Toshiba Fraud CaseDocument23 pagesToshiba Fraud CaseShashank Varma100% (1)

- Forensic Accounting-Mid SemDocument16 pagesForensic Accounting-Mid SemSaloni Parakh50% (2)

- Enterprise-Wide Business Process Management Drives PerformanceDocument3 pagesEnterprise-Wide Business Process Management Drives PerformancePatrick OwNo ratings yet

- Corruption PDFDocument219 pagesCorruption PDFmiligramNo ratings yet

- FRAUD INTERVIEW 02-Inv-Interview-TheoryDocument35 pagesFRAUD INTERVIEW 02-Inv-Interview-TheoryEmin Saftarov100% (2)

- Forensic Accounting PDFDocument9 pagesForensic Accounting PDFZain ul AbidinNo ratings yet

- 3 2018 L8 Gov.,Risk Management, ComplianceDocument13 pages3 2018 L8 Gov.,Risk Management, ComplianceTing Phin Yuan100% (1)

- Laundering The Proceeds of CorruptionDocument54 pagesLaundering The Proceeds of CorruptionouestlechatdememeNo ratings yet

- Forensic Accounting and Fraud Mitigation in The Manufacturing Industry in NigeriaDocument8 pagesForensic Accounting and Fraud Mitigation in The Manufacturing Industry in Nigeriaresearchparks0% (1)

- Erm Coso PDFDocument2 pagesErm Coso PDFLindsay0% (1)

- FRAUD Risk Assessment TemplateDocument10 pagesFRAUD Risk Assessment TemplaterickmortyNo ratings yet

- Case Study Opportunity FA PDFDocument39 pagesCase Study Opportunity FA PDFDiarany SucahyatiNo ratings yet

- Test of Controls For Some Major ActivitiesDocument22 pagesTest of Controls For Some Major ActivitiesMohsin RazaNo ratings yet

- 04 - Fraud Risk Management A Guide To GOOD PRACTICEDocument48 pages04 - Fraud Risk Management A Guide To GOOD PRACTICEEd Gonzales GonzalesNo ratings yet

- Fraud Risk ManagementDocument32 pagesFraud Risk ManagementO. Ch. Gabriel J.No ratings yet

- Creative Accounting - SatyamDocument21 pagesCreative Accounting - SatyamAkshat JainNo ratings yet

- Fraud Examiners Manual (International Edition)Document14 pagesFraud Examiners Manual (International Edition)Alper Hücümenoğlu0% (3)

- Defining A Forensic AuditDocument21 pagesDefining A Forensic AuditDINGDINGWALANo ratings yet

- Who Created The Model?: The Eight Variables AreDocument4 pagesWho Created The Model?: The Eight Variables AreArbaz BabarNo ratings yet

- Fraud Indicators AuditorsDocument35 pagesFraud Indicators AuditorsMutabarKhanNo ratings yet

- Case Study Operational RiskDocument27 pagesCase Study Operational RiskDikankatla SelahleNo ratings yet

- The Rise and Fall of Enron PDFDocument8 pagesThe Rise and Fall of Enron PDFsuriya vasanth bNo ratings yet

- Fraud Detection and Investigation-CmapDocument209 pagesFraud Detection and Investigation-CmapGerald HernandezNo ratings yet

- Consideration of Management Override of ControlsDocument2 pagesConsideration of Management Override of ControlsCaterina De LucaNo ratings yet

- Red Flags FraudDocument15 pagesRed Flags FraudRizael Jrs100% (1)

- 5 Computer FraudDocument15 pages5 Computer FraudayutitiekNo ratings yet

- Fraud AuditingDocument38 pagesFraud AuditingTauqeer100% (3)

- De Rebus September 2018Document48 pagesDe Rebus September 2018ConeliusNo ratings yet

- Business Marketing Planning: Strategic PerspectivesDocument35 pagesBusiness Marketing Planning: Strategic Perspectivessmithkumar88No ratings yet

- Forever Green: Montgomery County, Maryland Park Lands and Open SpacesDocument1 pageForever Green: Montgomery County, Maryland Park Lands and Open SpacesM-NCPPCNo ratings yet

- Ebor Lex June 2014Document31 pagesEbor Lex June 2014AdamWalterWoodleyNo ratings yet

- Situational Prevention and The Reduction of White Collar Crime by Dr. Neil R. VanceDocument22 pagesSituational Prevention and The Reduction of White Collar Crime by Dr. Neil R. VancePedroNo ratings yet

- BECKER, Gary S., LANDES, William Gary Becker-Essays in The Economics of Crime and PunishmentDocument281 pagesBECKER, Gary S., LANDES, William Gary Becker-Essays in The Economics of Crime and Punishmentalejandro1307100% (1)

- Hate Crime Hoaxes: Hoaxes To See Bing's Links To 4,650,000 Items. This Item Count Is Accurate As of MarchDocument4 pagesHate Crime Hoaxes: Hoaxes To See Bing's Links To 4,650,000 Items. This Item Count Is Accurate As of MarchtarnawtNo ratings yet

- Napolcom Review QuestionsDocument22 pagesNapolcom Review QuestionsMicheal NavarroNo ratings yet

- Jurisprudence NotesDocument40 pagesJurisprudence NotesKunal Singh86% (21)

- Public Prosecutor V Muhari Bin Mohd JaniDocument16 pagesPublic Prosecutor V Muhari Bin Mohd JaniHezekiah TanNo ratings yet

- (2017) Sgca 69Document59 pages(2017) Sgca 69A HNo ratings yet

- Essay On Death PenaltyDocument2 pagesEssay On Death Penaltyapi-376185650% (2)

- Correctional Administration Review QuestionsDocument30 pagesCorrectional Administration Review QuestionsKimberly Lucero LeuterioNo ratings yet

- Criminal Law - Friedman Chapter 15Document45 pagesCriminal Law - Friedman Chapter 15awesomeprussiaNo ratings yet

- 2011-2012 Prison Reform Topic PaperDocument12 pages2011-2012 Prison Reform Topic PaperbhjNo ratings yet

- OECDEDocument245 pagesOECDECarolinaTataruNo ratings yet

- Conference Proceedings Crime Justice and Social Democracy An International ConferenceDocument406 pagesConference Proceedings Crime Justice and Social Democracy An International ConferenceAndrés AntillanoNo ratings yet

- Theories of PunishmentDocument7 pagesTheories of Punishmentapi-376666984No ratings yet

- Shepherd - Posner Economic TheoryDocument40 pagesShepherd - Posner Economic TheoryhenfaNo ratings yet

- Guide To First Principles - Tim SonnreichDocument18 pagesGuide To First Principles - Tim Sonnreichchandra_w809590No ratings yet

- A G T C L: Pplication of AME Heory To Riminal AWDocument19 pagesA G T C L: Pplication of AME Heory To Riminal AWVrindaNo ratings yet

- The State Versus C Van WykDocument18 pagesThe State Versus C Van WykAndré Le RouxNo ratings yet

- Crime and Punishment in Sports and Society: PhilipDocument25 pagesCrime and Punishment in Sports and Society: PhilipmalNo ratings yet

- Criminological Theory 4Document28 pagesCriminological Theory 4Orecic Si-iugnod SapmocNo ratings yet

- The Rationales and Goals of Sentencing (2/2)Document14 pagesThe Rationales and Goals of Sentencing (2/2)Ashley Diane HenryNo ratings yet

- USA vs. Barry EdwardsDocument10 pagesUSA vs. Barry EdwardsWSETNo ratings yet

- Administration of JusticeDocument3 pagesAdministration of JusticeShubham Jain ModiNo ratings yet

- Philippine Crime Rate Up by 46Document6 pagesPhilippine Crime Rate Up by 46RmLyn Mclnao100% (1)

- Serious Problem JuvenilesDocument17 pagesSerious Problem JuvenilesSanjay Kumar PatelNo ratings yet

- William A. Edmundson-Death PenaltyDocument11 pagesWilliam A. Edmundson-Death PenaltyVlad SurdeaNo ratings yet

- Steven Finkler Sentencing Memo - DefendantDocument5 pagesSteven Finkler Sentencing Memo - DefendanttomwclearyNo ratings yet